DNTUF - WPP: Global Marketing Powerhouse

2023-08-05 14:02:06 ET

Summary

- WPP is a multinational advertising and public relations company offering marketing and branding services worldwide.

- The company's share price and growth trajectory has been materially impacted by the threat from technology businesses, taking market share as advertising spend transitions online.

- In addition to a growth slowdown, WPP's margins have contracted, as increased competition compounds the negative impact on the business.

- WPP remains inherently a strong business, with a range of leading agencies and clients, supporting a market-leading position.

- WPP's financial performance compared to other Advertising businesses is poor, compounding the unattractiveness of the business, despite its cheap valuation.

Investment thesis

Our current investment thesis is:

- WPP ( WPP) has a strong fundamental position, with a large number of leading agencies, a global presence, and a strong variety of leading clients.

- The company's position has been materially challenged, as a rise in technological development has driven marketing spending to a remit WPP has significantly less control over.

- Despite its strong commercial position in the advertising industry, WPP's financial performance has been underwhelming.

- Although WPP looks undervalued, with a deep discount, we believe this is a reflection of its current weakness.

Company description

WPP ( WPP ) is a British multinational advertising and public relations company headquartered in London. The company operates as a global communications services provider, offering a wide range of marketing, advertising, and branding services to clients worldwide.

WPP owns several well-known advertising agencies and media companies, making it one of the world's largest advertising and marketing services conglomerates.

Share price

WPP's share price has performed poorly in the last decade, losing over 30% of its value while the S&P 500 has made impressive gains. This has been driven by mediocre financial performance and increased competition.

Financial analysis

WPP Financial analysis (Capital IQ)

{kind=link}

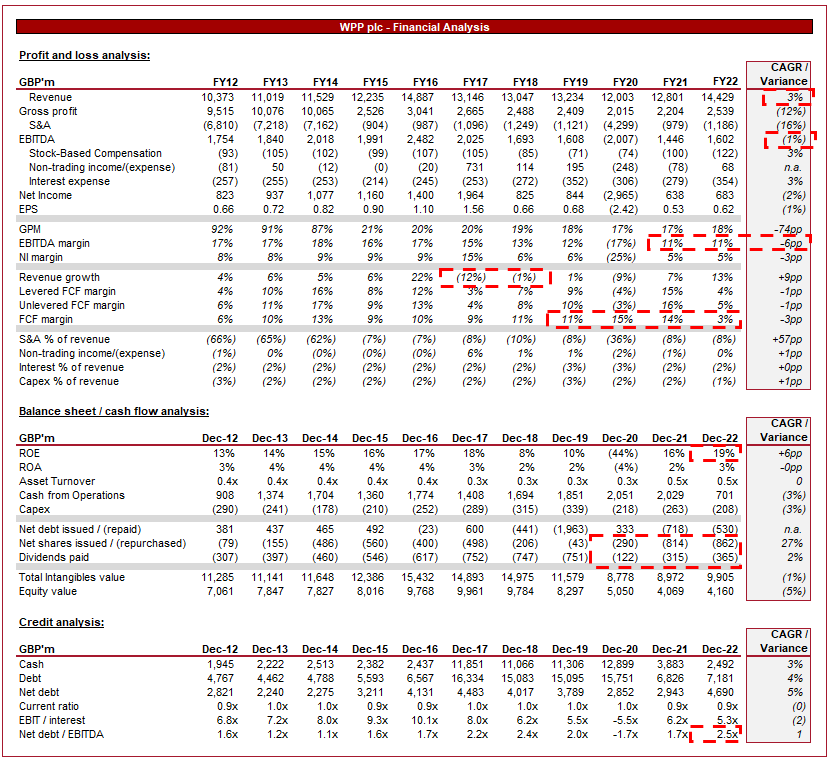

Presented above is WPP's financial performance for the last decade.

Revenue & Commercial Factors

WPP's revenue has grown at a CAGR of 3% in the last 10 years, with 3 periods of negative growth (one of which was pandemic impacted). WPP's revenue is materially supported by M&A, with over £3bn in cash spent during this period. This is an inherent characteristic of the industry, with smaller agencies acquired by larger consolidators.

Recent acquisitions (WPP)

Business Model

WPP's business model revolves around providing integrated marketing and communication services to its clients. The company operates through a network of advertising, media, public relations, branding, and digital agencies, offering services such as advertising campaign creation, media planning and buying, brand consulting, market research, and data analytics. The company's various agencies, and its wider brand(s), have a strong reputation in the market, with a strong track record of high-profile projects and clients. In the WARC ( ACENY ) 2023 ranking, WPP achieved impressive recognition for its ability to execute, underpinning deep expertise and relative ability.

WARC (WPP)

The company aims to create a seamless experience for clients by offering a one-stop-shop for all their marketing and communication needs. This integrated approach is underappreciated by many, as with businesses increasingly reliant on external consultants to help navigate a continually developing environment, the ability to have one service provider cover a range of topics is highly appreciated.

WPP's decentralized structure allows each agency within its portfolio to have its own brand identity, management team, and specialized expertise. This model provides agility and flexibility, allowing agencies to adapt to local market conditions and tailor their services to specific client needs. Further, this allows the business to foster specialization, improving its ability to illustrate its capabilities to clients. This structure is seen across the professional services spectrum for these very reasons.

{kind=link}

Some of the notable agencies under the WPP umbrella include Ogilvy, JWT, GroupM (Wavemaker, Mindshare), Grey, and Kantar. This extensive portfolio gives WPP an unrivaled competitive advantage by offering a wide range of services to clients and attracting global brands seeking integrated marketing solutions.

The approach of specialization in conjunction with an integrated solution and a wide range of leading agencies allows WPP to offer a compelling service to any business, regardless of size, geography, or industry. Clients include L'Oreal ( LRLCF ), Mondelez ( MDLZ ), Tiffany ( LVMHF ), Chevron ( XOM ), Colgate-Palmolive ( CL ), and Beiersdorf ( BDRFF ). WPP has won over $1.5bn of new business in 2023.

{kind=link}

The advertising and marketing industry has undergone significant disruption in recent years due to digital transformation, changing consumer behaviors, and giving rise to digital advertising platforms like Google and Facebook. Traditional advertising agencies, such as those under WPP, have faced significant challenges in adapting to this rapidly evolving landscape. We consider this the largest factor underpinning the company's recent and future performance. With an increasing movement toward the utilization of digital marketing, WPP faces being "locked out" of the industry it has helped develop.

WPP is attempting to respond to changing industry conditions, seeking to develop its metaverse and AI capabilities, both through partnerships (such as with Nvidia ( NVDA )), and acquisitions (such as with AMP). It remains to be see if this has the ability to contribute materially to the top-line.

In conjunction with this, the rise of influencer marketing and social media platforms is an underrepresented risk to this business. Influencers are increasingly able to develop their own strategy for monetizing their platform, working directly with brands. Further, brands are relying more heavily on their own social media marketing teams, reducing the capital allocated to more traditional avenues.

FGS Global, a subsidiary of WPP, that provides strategic advisory and communications consultancy services was partially sold to KKR (29%), with an implied valuation of $1.4bn ( 3.2x FY22 Revenue ). FGS Global represents one of the most influential businesses in the world, with the likes of Apple (AAPL) as its client. The business is growing well and represents an opportunity for outsized returns in the coming years.

More broadly, this transaction is significantly above WPP's current valuation of 1x Revenue. With the share price issues in recent years, we could see WPP increasingly seek to sell all or parts of its high-performing businesses, unlocking value for shareholders and maximizing its portfolio's return.

Competitive Positioning

WPP faces competition from other global advertising and marketing services companies such as Omnicom Group Inc. ( OMC ), Publicis Groupe SA ( PUBGY ), Interpublic Group of Companies Inc. ( IPG ), and Dentsu Group Inc. ( DNTUF ). The industry is highly competitive, which has contributed to pricing pressures to ensure projects are continually won. Further, with industry headwinds, this further contributes to aggressive pricing.

Economic & External Consideration

Current economic conditions represent near-term issues for the business. With high inflation and elevated rates, consumer spending is under pressure, with finances squeezed. As a result of this, we expect marketing spending to soften, as returns are less lucrative.

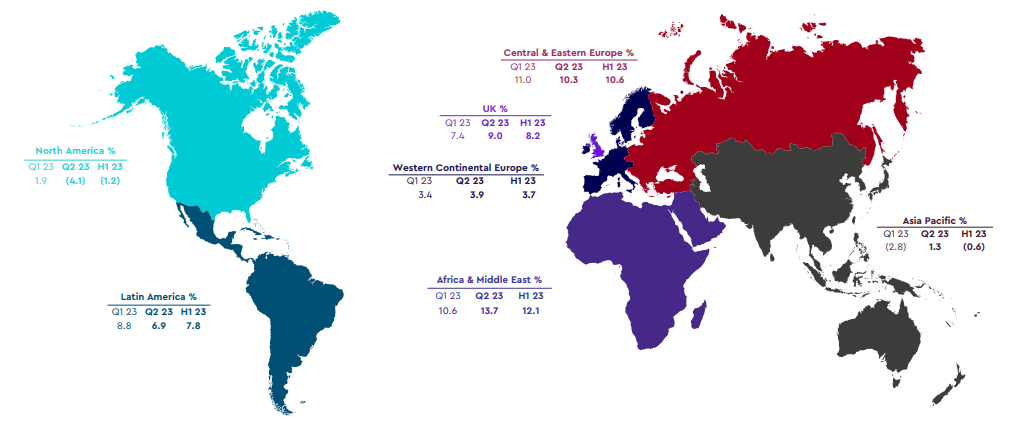

This said, the current conditions are slightly unique, in that despite the clear indication of an impending recession, consumer spending and employment remains robust. This is partially the reason for the sticky inflation. LTM revenue illustrates this perfectly, with 13% growth.

As the following illustrates, growth is not uplifted by any one region, but the business is experiencing healthy demand across the globe. For this reason, we remain cautiously optimistic that WPP is positioned to navigate this well.

{kind=link}

Margins

WPP's margins have trended down, with an EBITDA-M off 11% (down 6ppts from FY12) and a NIM of 5% (down 3ppts).

As previously mentioned, the advertising industry is highly competitive, leading to cost pressures on agency fees and margins. This is exacerbated by the cost-effective nature of social media marketing, contributing to less appetite for traditional marketing spending. Further, WPP's decentralized model, with each agency operating independently, may have led to inefficiencies and increased costs in certain cases. For this reason, we are not surprised to see WPP's EBITDA-M trend down in the last decade, even prior to the pandemic.

H1

WPP's posted a disastrous H1, with its share price down (7)% at the time of writing. The company's revenue (less pass-through costs) grew 5.5%, with operating profits up 4.3%, YoY. Although strong, the business has seen growth declining in North America and Asia Pacific (LFL) in H1, as well as a Management downgrading its LFL growth forecast to 1.5-3% from 3-5%. With the cost of capital higher, its likely acquisitions will be more difficult to execute, contributing to a difficult period for the business.

Balance sheet & Cash Flows

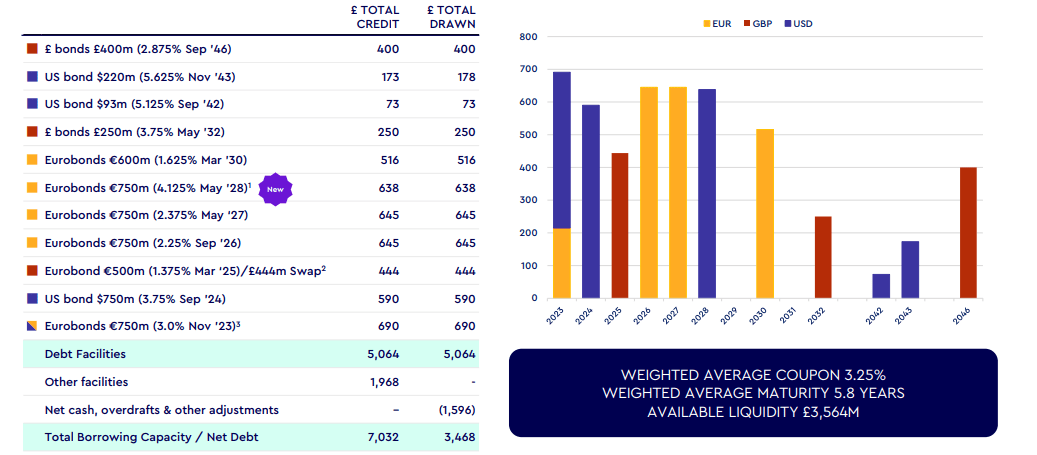

WPP is reasonably financed, with a ND/EBITDA ratio of 2.5x. This gives the business some room to further finance transactions, but the business is approaching a healthy maximum (our view is 3x). This stresses the importance of improved growth.

WPP's maturity profile is well managed, with near-term debt well covered with cash.

{kind=link}

Industry analysis

{kind=link}

Presented above is a comparison of WPP's growth and profitability to the average of its industry, as defined by Seeking Alpha (16 companies).

WPP performs poorly relative to peers. The company's growth has underperformed, primarily due to increased competition, in conjunction with its size making it difficult to achieve absolute gains relative to its smaller peers.

Further, the business is less profitable than the average, again, owing to competition eroding its pricing advantage.

Based on this, we believe WPP should trade at a discount relative to its peers, reflecting its underperformance.

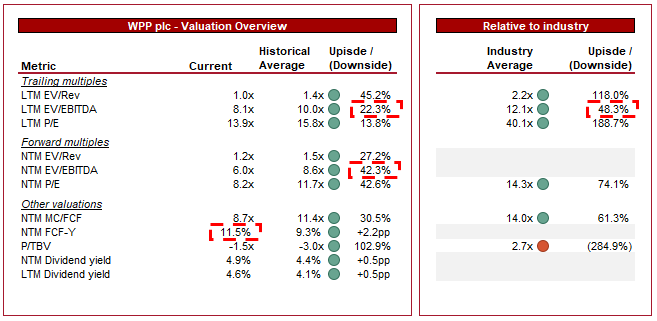

Valuation

{kind=link}

WPP is currently trading at 8x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to WPP's historical average is warranted in our view, primarily due to the margin erosion thus far, as well as the increased competition from tech firms. We believe competition will continue to remain high, restricting its ability to grow. A discount of 20% is reasonable in our view, which on an LTM basis suggests upside is currently lacking. We do not put much stock into the NTM forecast, as it would imply 50% EBITDA growth from the current level, which is unreasonable in our view.

Relative to its peers, a discount is also warranted. The entire industry is experiencing competition from tech businesses but we would not expect WPP to underperform in profitability, even if growth is mediocre. This implies a fundamental weakness in the business. To this peer group, we would suggest a 30-35% discount, implying moderate upside at the current share price.

Final thoughts

WPP has a substantial global presence, with a market-leading presence across a range of industries and countries. With a strong reputation across its agencies and an impressive client book, the business is positioned well long-term to maintain its current position. This said, the scope for a fruitful future is restricted by the rise of technology-driven marketing, with firms such as Meta ( META ) and Google ( GOOG ) taking market share consistently. When considering this commercial weakness alongside its financial weakness and H1, we do not believe the business is a good investment today

For further details see:

WPP: Global Marketing Powerhouse