WUXAY - WuXi Biologics: Holiday Fire Sale For Leading CRDMO

2023-12-06 02:05:56 ET

Summary

- WuXi Biologics is a contract-based drug developer in China, but recent share price performance has lagged.

- The company is expecting a major miss in revenues for FY 2023 due mostly to over-optimism, causing a 30% decline in share price.

- Despite the temporary issues, WuXi Biologics remains a great company with fast growth, profitability, and a solid financial foundation.

Introduction

WuXi Biologics (Cayman) Inc. ( WXXWY ) is one of the world's largest contract-based drug developers. With services falling under common acronyms such as CDMO, CMO, CRDMO, and more, WuXi provides a full-spectrum approach to biologic therapy Research, Development, and Manufacture. While WuXi is undoubtedly one of China's best-performing companies and is financially competitive against other top-tier global investments, recent share price performance has lagged.

The geopolitical risks and volatile industry do harm share price performance, but I believe these have led to a gift in this holiday season. All that was needed was one business update that highlighted the volatility of this asset. As so, I will provide a short summary providing the reasons why I am buying up this deal, just in time for the holidays.

A Great Company vs. A Bad Quarter

WuXi Biologics (~$20 billion market cap) is a fully-owned subsidiary of the larger life, chemistry, and material sciences contractor WuXi AppTec ( WUXIF ) (~$30 billion market cap and formerly NYSE listed). While AppTec is fully China-based with headquarters in the Shanghai area, WuXi Biologics is a more approachable segment based in Hong Kong with Cayman Island registration.

WuXi Biologics covers the specialties of biopharma and biotechnology, primarily contracted to perform the production of the chemicals, base ingredients, and small samples for the research phase of the industry. The company also assists in the research process itself, with the company having experience with a wide range of areas such as antibodies, antigens, computer-aided drug discovery, B cells, and more. The main competition includes Lonza, Catalent, Thermo Fisher's Life PPD/Pantheon subunits ( TMO ), and Samsung Biologics, and these names offer a further look into the unique CRDMO industry.

Unfortunately, to some, the high need industry led to a great increase in revenues due to the pandemic. WuXi was a major vaccine component contract organization and revenues increased by over 60% per year over the pandemic period. However, as of a business update released on December 4th, 2023, the end of the pandemic is reflected quite clearly by a shocking miss to revenues by $400 million (for full-year revenues). This has caused the share price to fall over 30% in just two market days as I write this on the 5th.

While going back to a more realistic outlook makes sense, I believe the 30% tumble in value is more a gift than a worry for long-term investors. Especially as revenue growth still remains positive for the year, COVID projects only accounted for 7-10% of all new projects in 2021/22. Plus, while the broader market remains in a slump, there are many signs of a turnaround in the coming quarters and years.

Diving into company commentary on what happened with the last earnings, the issue was still related to over-optimism. Forecasted revenues related to the Development sector are now 20% lower than anticipated due to the lack of new projects being generated due to the lack of biotech funding. This makes sense as the speculative industry cuts back on spending with interest rates being so high. However, this is a temporary issue. Growth will resume within a year or two due to both Research revenues remaining stable, which leads to larger development contracts, along with the swift growth of the newly formed conjugates and vaccine segments that are slated to grow over 50% per year.

Also, Manufacturing revenues were adversely affected by delayed FDA approvals, which are also a temporary issue that will always plague the company. Nothing extraordinary, and are importantly not related to the quality of WuXi's production facilities. So yes, it is good that the valuation has been reset to a non-COVID boosted level, the base level still remains high quality.

WuXi Business Update Dec 4, 2023

Other Financial Factors For Long-term Success

One thing that was lacking from the business update was the financial reports, which are due in the coming days. However, if the financials work out to be less impacted than the 30% share price decline would suggest, then shares may rally. Therefore, I have decided to initiate a position prior to the report release (expected on the 7th).

I also believe that one quarter's earnings are not enough to distract me from seeing the long-term opportunity. However, I will submit this article as a standalone update on the recent results, and provide long-term commentary after the full year earnings report is released. In that article, I will also dive into the industry outlook, competition, and WuXi AppTec as a whole.

For now, I will point out just the key factors that I am using to initiate a buy:

-

Fast growth, even when not taking COVID into consideration. Revenues are also well diversified. For the first half of 2023, 33% of revenues came from preclinical, 23% from Ph 1 or 2, and 42% from Ph 3 or commercial services. Revenues were up 17% in 1H23 compared to 1H22.

-

The company is well established outside of China. Over 76% of revenues are based on North American and European customers. Production facilities are located around the world, although there have been no issues with the Chinese facilities. According to the company in 2019, they were the first and only Chinese CDRMO approved by the FDA.

- They are extremely profitable. WuXi Biologics has 25% current net income margins, although the 5-year average margins are over 30%. This highlights the company's market-leading position, safety, and conservatism.

-

No leverage equates to a solid foundation. With cash of $1.3 billion compared to debt of $777 billion, there is plenty of flexibility in this downturn. Watch for acquisitions and other uses of the cash. Many well-integrated acquisitions over the past two decades led to the company we see today.

-

Dilution is slowing down and free cash flow generation is turning positive. This increases company valuation with more shareholder-friendly tactics. Less speculation-based cash burn, capex, and intense growth. However, there is still plenty of profits being invested in R&D and maintaining approval-quality facilities.

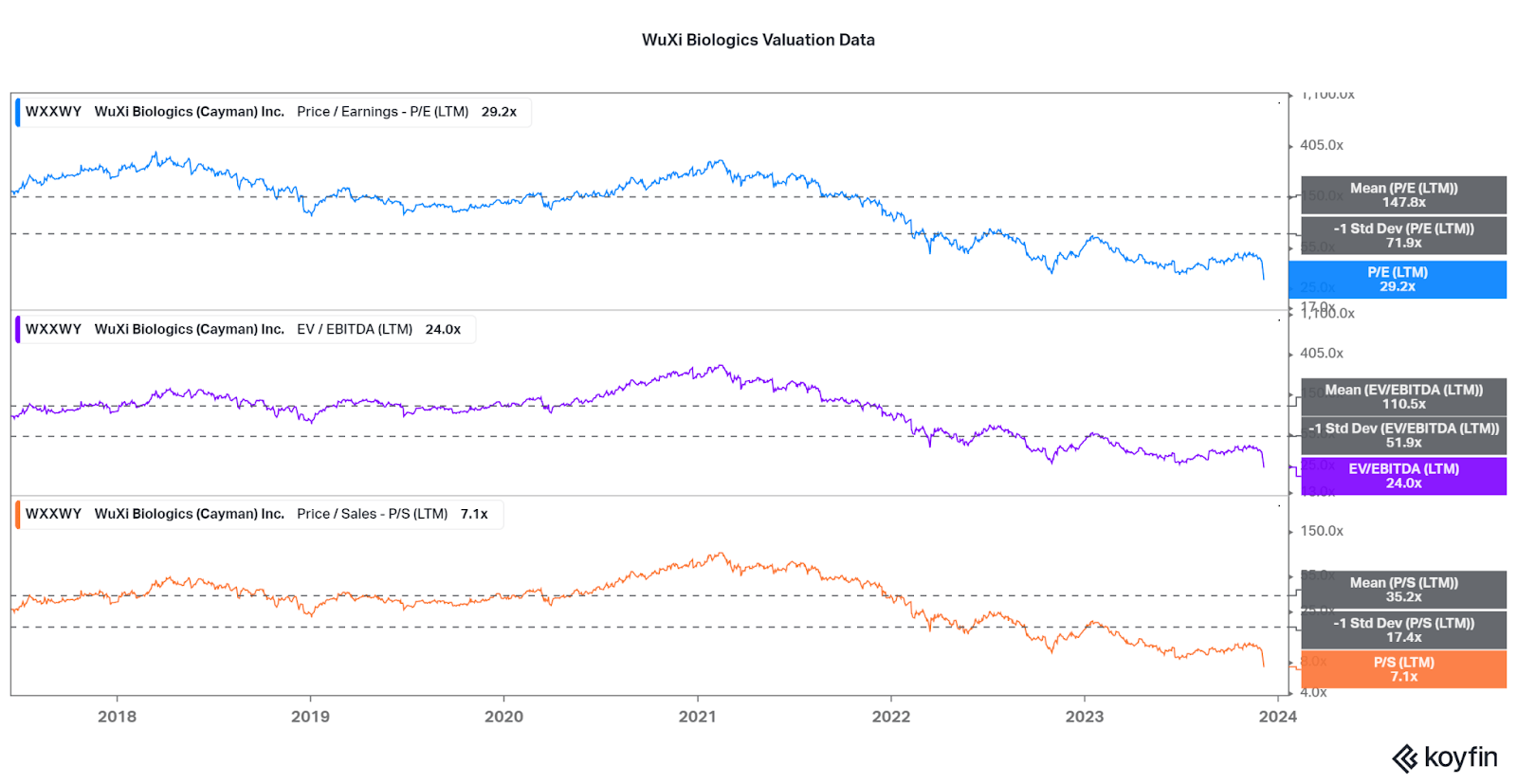

Valuation and Buy Point

I never invested in WuXi prior to now due to the high valuation. In fact, the valuation was very high even before the pandemic led to an earning boom. The share price did go up though, at least until 2021. Now with the decline, I see a more favorable valuation closer to reality. These values will change with the next earnings report, and if the price remains flat, then the valuation will fall further. This is to be expected with the market downturn, but I do expect a rebound under a return to normal conditions in the coming years. I believe it is best if we compare to peers.

The best example would be Lonza AG, a pure-play CDMO with global reach. Profit margins are fairly similar, although WuXi is growing far faster (almost 10x the earnings growth over the past 5 years). However, as WuXi growth slows, a slight growth premium is justified only. At current valuations, WuXi is priced approximately 1.5-2.0 times higher than Lonza. All else equal, bottom-line growth at WuXi is more than double that of Lonza.

Therefore the valuation is bordering on a deal, although the main factor is that both companies are trading far below historical averages (adjusted with performance). This is also why WuXi looks more enticing in my eyes than peers. I will try to pick up shares of WXXWY anywhere below $7.80, and reevaluate after earnings are released. However, the bear case exists and I would suggest investors look at Catalent ( CTLT ) for an example of what can go wrong if a facility inspection comes back with a warning and revenues decline excessively.

{kind=link}

Conclusion

While WuXi is certainly a key example of boom and bust cycles, I do believe there is long-term opportunity. The biologics market is in a secular growth phase thanks to cell therapies, antibody therapies, vaccines, and more. I have discussed these features in depth in many of my prior articles. I believe that WuXi is also worth a deeper look in future articles, especially when considering the risk of foreign listing, complex business structure, and strong peers. In time I will provide an update doing just that.

For now, I will take advantage of this sale period by initializing a position. However, I will not make the position a major part of my portfolio, and instead allow WuXi to grow into a major holding if the thesis turns out correct. I already have plenty of exposure to the CDMO industry with Avid Bioservices (CDMO), which is also underperforming, so the overlap risk is high for me. And, to reduce risk it may be better to wait for the earnings to come out to see the full financial impact of the poor business update. So be sure to consider your investment goals and capabilities, and invest accordingly.

Thanks for reading. Feel free to share your thoughts in the comments.

For further details see:

WuXi Biologics: Holiday Fire Sale For Leading CRDMO