ICAP - XYLG: We See No Added Value For Covered Call Growth ETFs

2023-03-24 09:58:18 ET

Summary

- The upside potential of a covered call strategy is capped.

- Covered call growth ETFs like XYLG try to circumvent this “problem” by limiting the percentage of the portfolio on which they write calls.

- Covered call growth ETFs do not add value and should be avoided.

- A combination of a covered call ETF and a stock market index ETF offer you the same exposure, but at a lower cost.

Covered call ETFs like the Amplify CWP Enhanced Dividend Income ETF ( DIVO ) and the JPMorgan Equity Premium Income ETF ( JEPI ) are popular among income oriented investors. The upside potential of a covered call strategy is however capped. Covered call growth ETFs like the Global X S&P 500 Covered Call & Growth ETF ( XYLG ) try to solve this by limiting the percentage of the portfolio on which they write calls.

But, covered call growth ETFs do not add value and should be avoided. A simple combination of a covered call ETF like the Global X S&P 500 Covered Call ETF ( XYLD ) and a stock market index ETF offer you the same exposure, but at a lower cost.

Covered calls ETFs

Covered call writing is a conservative strategy with only two possible outcomes.

If the stock is sold at a higher price on the expiration date of the call option, the call writer keeps the option premium and also the appreciation of the underlying stock up to the strike price. The upside potential of a covered call strategy is capped.

On the other hand, if the stock never exceeds the strike price during the period up to expiration, the call writer keeps the option premium and also keeps the stock in portfolio. A negative total return cannot be excluded in this case. The received option premium offers some downside protection. When the markets are down, they are often also more volatile which results in higher option premiums and hence some extra downside protection.

In both cases, the collected option premium is a source of income.

Global X has several covered call ETFs that use a passive approach. XYLD e.g. buys the complete S&P 500 and writes calls every month on the index. Other ETFs like JEPI and DIVO are more active in their stock selection and tilt their portfolio to high dividend stocks.

Covered call growth ETFs

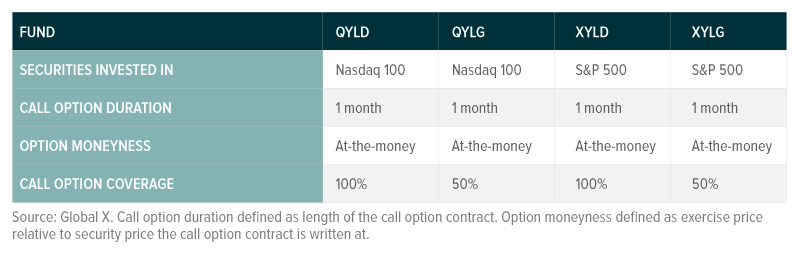

The upside potential of a covered call strategy is capped and covered call growth ETFs try to circumvent this "problem" by limiting the percentage of the portfolio on which they write calls. According to Global X "a 50% covered call approach is designed to balance growth potential with income, and therefore aligns best with investors seeking both outcomes". The Global X covered call growth ETFs the Global X Nasdaq 100 Covered Call & Growth ETF (QYLG) and XYLG write options that cover 50% of their stock holdings, whereas the Global X Nasdaq 100 Covered Call ETF (QYLD) and XYLD cover 100%.

Figure 1: Covered call growth ETFs vs. covered call ETFs (Global X)

{kind=link}

This means that QYLG and XYLG have exposure to approximately 50% of the upside of their underlying indexes, but should generate only half of the income of QYLD or XYLD.

QYLG and XYLG also use a passive approach for their stock selection. XYLG e.g. buys the complete S&P 500, just like XYLD does.

The InfraCap Equity Income Fund ETF ( ICAP ) is an example of a covered call growth ETF that uses an active stock selection approach. Just like JEPI and DIVO, ICAP invest in high yielding equities and uses a covered call strategy on top of that. But ICAP utilizes this option strategy on only 30% of its portfolio.

You can read our thoughts on ICAP here .

Performance

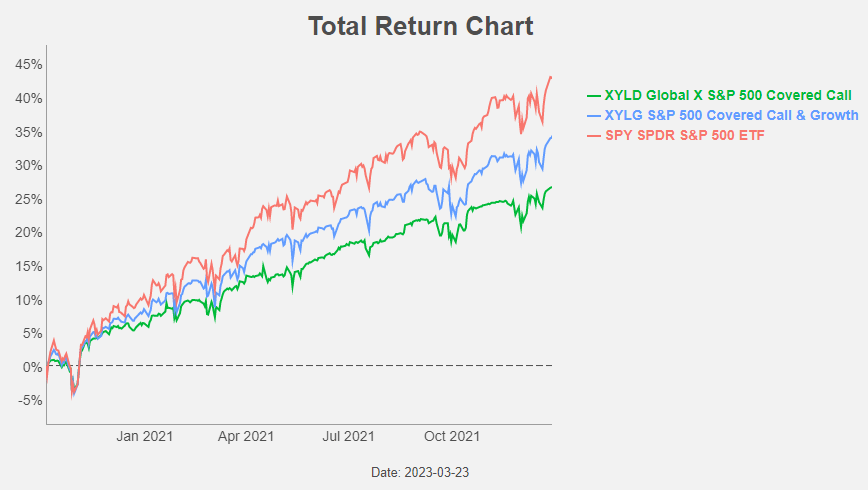

Let's see how the (passive) covered call growth ETFs perform in a rising stock market. They do indeed perform better than traditional covered call ETFs. Of course, they underperform the S&P 500 given covered calls cover 50% of the portfolio.

Figure 2: Total Return Chart (Yahoo! Finance, Author)

{kind=link}

There is also no active stock selection that could deliver alpha and limit the underperformance compared to the S&P 500.

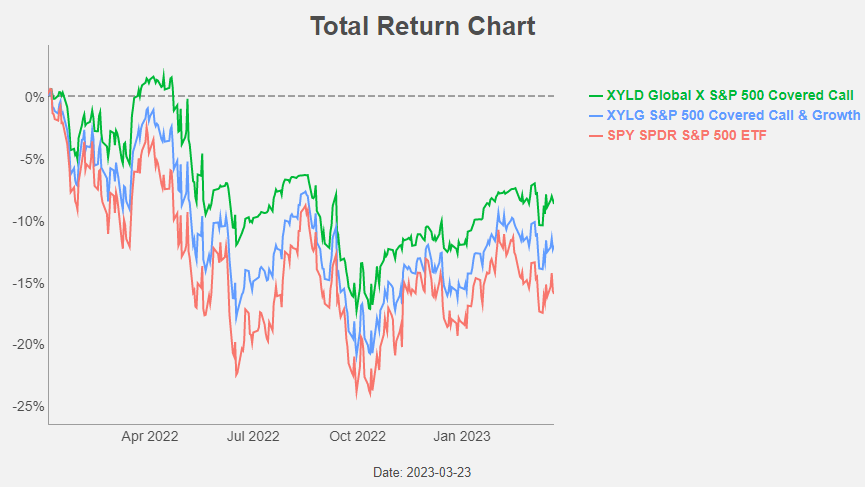

In a down-market we get the mirror image. Covered call ETFs receive more option income and offer more downside protection.

Figure 3: Total Return Chart (Yahoo! Finance, Author)

{kind=link}

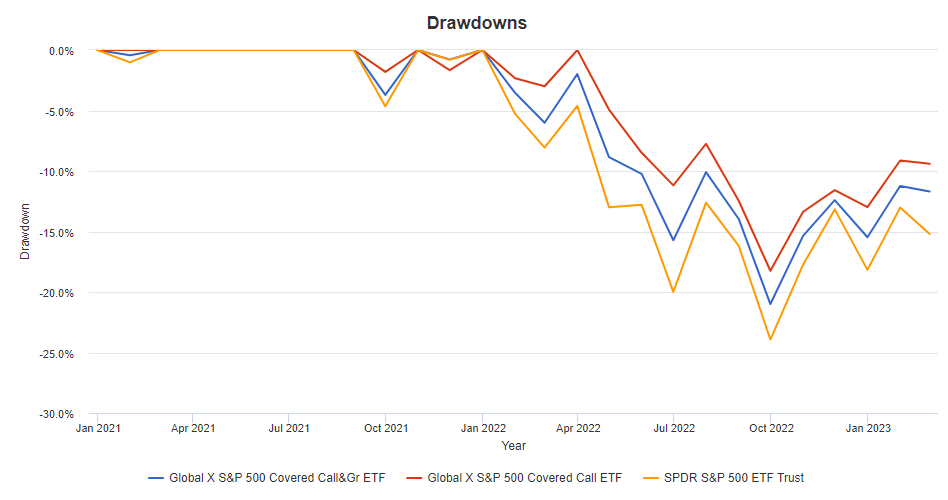

The drawdowns confirm this downside protection.

Figure 4: Drawdowns (Portfolio Visualizer)

{kind=link}

Covered call strategies do indeed offer superior risk-adjusted returns with lower volatility. In the period from January 2021 to February 2023 XYLD delivered a Sharpe ratio of 0.31 compared to a Sharpe ratio of 0.24 for the S&P 500. The beta of 0.56 proves it's a low-beta strategy.

Figure 5: Performance metrics (Portfolio Visualizer)

{kind=link}

XYLG's beta lies right in the middle between XYLD and the S&P 500.

No added value

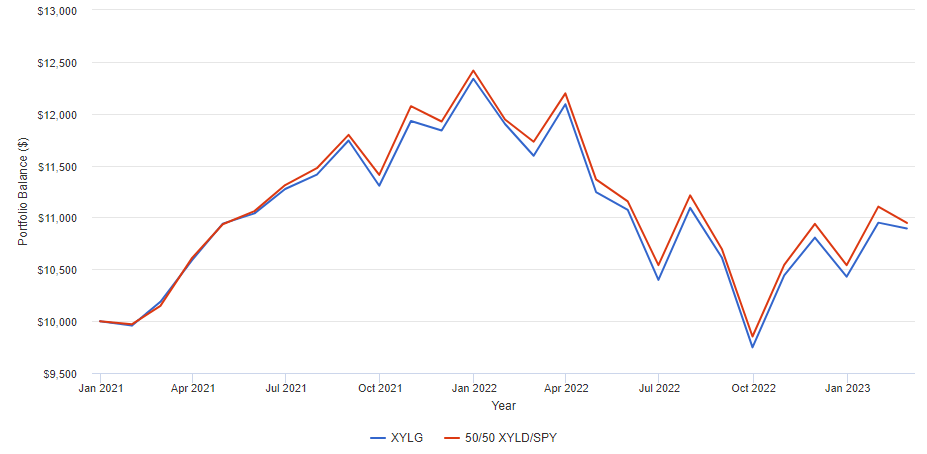

For most metrics XYLG is right in the middle between XYLD and SPY. This makes us wonder how a portfolio with 50% in both XYLD and SPY would perform compared to XYLG?

Figure 6: Performance (Portfolio Visualizer)

{kind=link}

The 50/50 portfolio is outperforming XYLG in the period from January 2021 to February 2023.

The expense ratio might be the main reason for this difference. Both XYLG and XYLD have an expense ratio of 0.60%, while SPY has an expense ratio of 0.09%.

The conclusion is that we see no added value for buying a covered call growth ETF like XYLG (and ICAP).

Outlook for covered call ETFs

To be really positive about covered call ETFs we look at two features: high volatility and stock markets that are not in a downtrend.

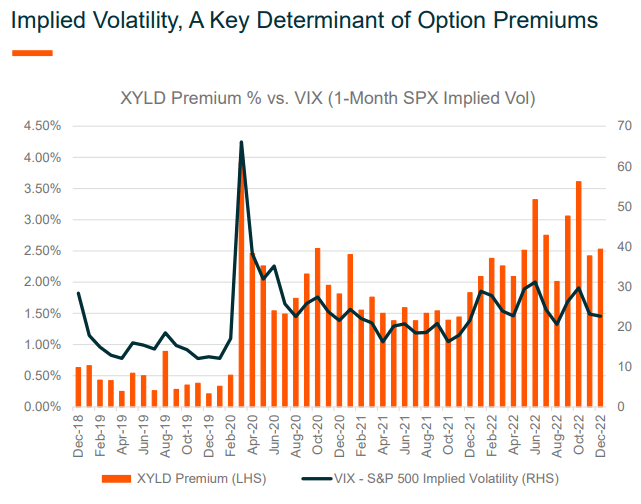

When the markets are more volatile this results in higher option premiums.

Figure 7: Implied volatility and option premiums (Global X)

{kind=link}

The banking crisis has a silver lining for covered calls ETFs: the higher volatility as a result of the crisis translates into higher option premiums and hence higher option income.

Figure 8: VIX Index (CBOE)

DIVO e.g. uses a rules-based set of triggers to identify the best covered call opportunities on the stocks in their portfolio. They look for opportunities to write covered calls when the VIX is at 15 or higher.

Covered call writing is a defensive, low(er) beta, strategy. When the markets rise, you get a nice return. That return will probably be lower than the return of the equity markets itself, but that's something you know in advance.

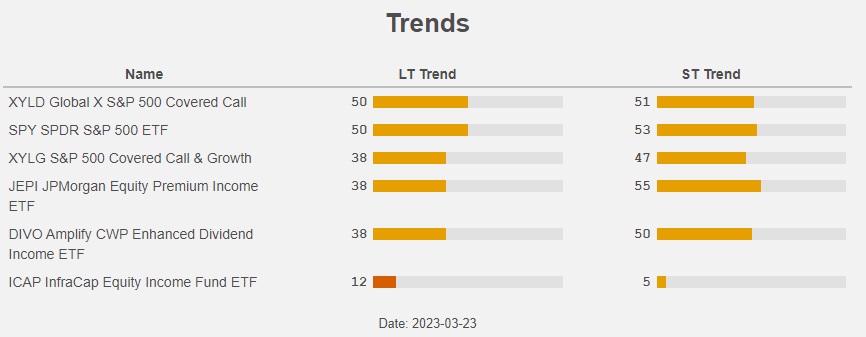

When the equity markets fall, you usually outperform thanks to the collected option premiums. Of course, when the market really tanks, you will still have a negative return. That's why we prefer not to invest in such a strategy when the equity market is in a long term down trend.

Figure 9: Trends (Yahoo! Finance, Author)

{kind=link}

This is currently not the case. The S&P 500 is in a neutral long term trend, as is the case for both XYLG and XYLD (and JEPI and DIVO). ICAP on the other hand is in a long term down trend.

The current environment with stocks not in a long term downtrend and high volatility is a good backdrop for (genuine) covered call ETFs.

Figure 10: Total Return Chart (Yahoo! Finance, Author)

{kind=link}

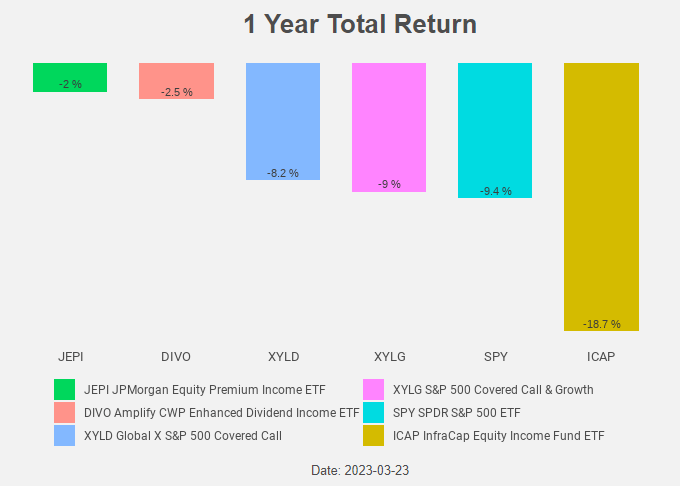

Figure 10 is a great summary:

- The performance of a passively managed covered call growth ETF (like XYLG) lies in the middle between a passively managed covered call ETF (like XYLD) and their underlying index.

- Covered call ETFs outperform when stocks markets are down.

- Actively managed ETFs covered call ETFs (like JEPI and DIVO) can deliver alpha.

- Covered call growth ETFs do not add value.

- Covered call growth ETFs that use leverage (like ICAP) certainly do not add value.

The actively managed ETFs can of course deliver negative alpha. If you want to exclude this possibility XYLD is a viable option.

Covered call growth ETFs do not add value and should be avoided. A combination of a covered call ETF and a stock market index ETF offer you the same exposure, but at a lower cost.

JEPI is exposed to counterparty risk through the use of ELNs. The counterparties mentioned in its prospectus are diversified and well-known names like Barclays, BNP Paribas, Citigroup, Credit Suisse, Goldman Sachs and Royal Bank of Canada. We don't know if JEPI currently has any ELNs outstanding with Credit Suisse as a counterparty. We do know that the counterparty risk is higher than it was say two weeks ago.

That's why we have a preference for DIVO.

Conclusion

Covered call growth ETFs like XYLG do not add value and should be avoided.

A combination of a covered call ETF like XYLD and a stock market index ETF offer you the same exposure, but at a lower cost.

For further details see:

XYLG: We See No Added Value For Covered Call Growth ETFs