YARIY - Yara: 2023 Upsides And Targets Are Clear To Me

Summary

- I've been investing in Yara for years, and am currently sitting on a nearly 6% portfolio position in the company with a cost basis of native below 300 NOK.

- The current price is above that - and that does not yet include the substantial number of dividends and extraordinary dividends paid out, coming to a 63% RoR.

- The potential for Yara is to reach above 500 NOK once again driven by strong results for the year, and potential great 2023. I'll show you "BUY" and "TRIM" here.

Dear readers/followers,

Last time I wrote on Yara ( YARIY ) was in August of 2022. That's a few months back, and since that time, my stance has outperformed, and Yara has outperformed the S&P 500 by more than 10%.

Yara International Article (Seeking Alpha)

Without wishing to toot my own horn too much, I feel that I have a fairly good grip on this company's valuation range at appeal at certain points. It's why I have been so clear that above 500 NOK is when you consider to start trimming - below 400, or better yet, below 380 NOK, that's when you really back up the truck on Yara.

Why is that?

Well, let me show you.

Revisiting Yara

Think back to 2020, that's when I published my first article on this company. I stayed out of the company for years due to troubles, but since I went in, the company has generated total RoR of nearly 60%.

Yara International Article (Seeking Alpha)

By every measure, a very successful investment to have made.

Yara International is a Chemical Company. It produces nitrogen fertilizers, ammonia, urea, and nitrogen-based chemicals. Focal areas are, naturally, crops and farming. Historically speaking, the company was founded 115 years ago as Norsk Hydro ( OTCQX:NHYDY ) - yes, that's the same Norsk Hydro that I've written about for pretty much my entire career as a contributor, and had some massive, triple-digit successes with as well.

Yara was the world's first producer of mineral nitrogen fertilizers. Back in 2004, Norsk Hydro and Yara International de-merged as part of a strategy to clarify and specialize, forming the aluminum company and the fertilizer company we now know.

For those of you that don't know Norway that well, the Norwegian state has a close hand in most larger companies through direct share ownership. Yara, for instance, has a 36.2% ownership by The Norwegian Ministry of Trade, Industry and Fisheries, and another 6.3% by The Government Pension Fund of Norway, coming to a 40%+ government position for the company - and Yara is not alone in this among Norwegian businesses - there are plenty more that have this sort of allocation by the government.

Yara International has 17000+ employees, sales to 160 countries and generates tens of billions in annual revenues. Out of its closest peers, very few are the size of Yara, and what's more, very few companies have the international footprint that Yara gives us. Also, Yara is one of the most future-secured fertilizer businesses out there compared to Canadian Potash, German Potash, and Easter-European fertilizer, most of which is very "legacy".

The company's sales aren't focused on any particular geography, though the largest is the European continent and Latin/South America.

Portfolio is fertilizers, unsurprisingly, and a wide selection of them. The recent environment has been amazing for Yara shareholders, who have enjoyed dividends after dividends, complemented by extraordinary payouts on top of regular ones, the latest one in December of 2022 at 10 NOK per share, with the following wording.

{kind=link}

The dividend flow is currently looking like this.

{kind=link}

Note the absolutely massive amounts and increases in dividends since I bought in 2019-2020. The company now has an ordinary dividend level of 30 NOK/share and year, with 10 NOK for 2022 already being distributed a few weeks back. We can not only expect a full ordinary dividend given the company's results in 2022, I believe we can expect further extraordinary dividends.

Why?

Because gas prices are dropping due to the weather. That means ammonia and other curtailments that Yara has been doing/affected by for the past few months are likely to be lifted somewhat, which will lead to sales increases at currently elevated fertilizer prices. The gas prices don't solve the fertilizer shortage that's currently affecting the world.

Deliveries for the company are down, but margins are up due to massive price increases - and I expect volumes to stabilize and improve going forward.

{kind=link}

The company has all of the natural trends on its side. We're moving towards a circular economy; digital revenue streams are growing across the board for many businesses. The company is launching products frequently, and they even partnered with IBM ( IBM ) to launch a globally-leading digital farming data and services platform. Yara has long-proven expertise in agronomy, a global reach, and now includes the latest technologies.

The question becomes, why wouldn't you want to invest in Yara at the right price ? What could possibly be negative here? Aside from the relative cyclicality of the fertilizer space - which I admit is significant - there is really no fundamental worry to point to here. Yara is Baa2 rated, which makes sense given this fertilizer space, but a medium-grade credit with a Prime-2 credit risk, the ability to repay short term at a very high rating. Yara is investment grade, and should be treated as such.

The current lower ammonia production in 3Q22 which we saw is likely to reverse somewhat in 4Q22 with the mild winter...

{kind=link}

...which will be beneficial for Yara sales, and its long-term portfolio growth. Remember, this company has some of the more solid current trends and future plans in the industry.

{kind=link}

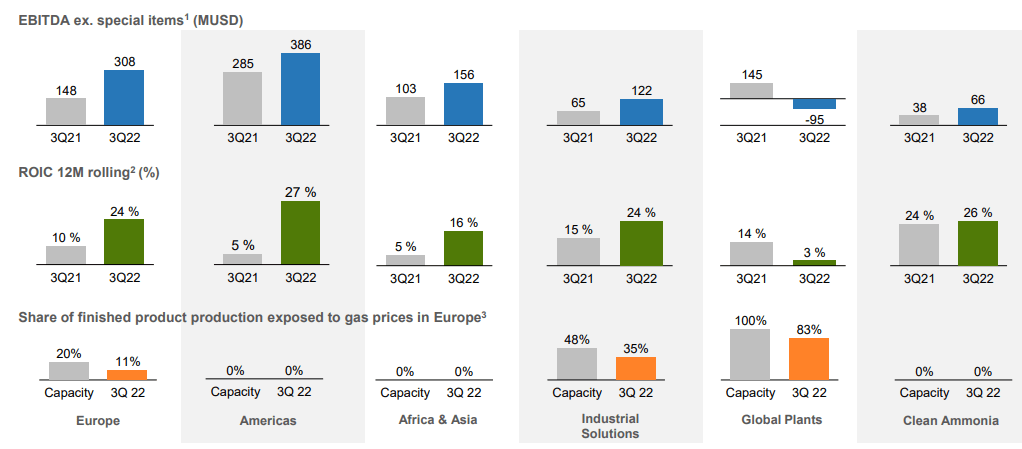

The company has improved its YoY results significantly - with EBITDA up nearly 30% in the last quarter, EPS closer to 40%, RoIC from 8.3% to over 20% and operational cash flow from negative to $103M positive.

Returns have improved across all regions, and these results are offsetting any and all losses from ammonia production.

{kind=link}

The company's earnings, propped up by significantly positive pricing, is making possible planned investments for the company without the need to draw down any debt or other worries. And let's not forget that these trends are extremely unlikely to disappear in the near term.

Why?

Because everyone in Europe is calling for reduced dependence on Russia, a major fertilizer producer. There aren't many companies outside of Eastern Europe in Europe that do fertilizers - more importantly, there aren't many larger ones that do modern, ammonia/nitrogen-based fertilizers as opposed to potash. The reduction of dependence on Russia is a first-order positive for Yara - and even if the war stops tomorrow, I don't see Russian fertilizer shipments resuming all that quickly.

{kind=link}

The fundamental appeal of Yara remains after 3Q22 and going into 2023 here. It's the #1 premium crop nutrition leader, and it's transitioning in full toward more sustainable solutions.

What's more, it's one of the most shareholder-rewarding companies in its sector on earth, while maintaining a strict capital discipline, but also paying out windfalls in cash to shareholders that have made possible triple-digit returns over the past 5-6 years. It's my largest position , and while I do have covered calls opened on about 25% of it, those CCs are targeting strike prices of 520-560 - which is higher than Yara has ever traded , so they're just a way for me to boost my income. If I do get to sell at that price, I'll be happy as well, and I'll probably be writing more contracts as we move toward 500 NOK, and the premiums for the 600-650 Strikes start improving.

But, this is about the common share - so here's my valuation for that one.

Yara's current valuation and upside

My price target for Yara has long been around 420-450 NOK, and that remains. I'm not shifting that one for this article - but I do want to point out, and clearly emphasize, that's as high as I would go. And above 450 NOK is really stretching it.

Yara at below 420-450 NOK is attractive in part because of the high dividend. And because of current macro trends and the way the business in which they operate works, Yara remains attractive here.

From a valuation perspective, it doesn't matter how you view or choose to look at Yara. You can model DCF, NAV, yield, or book value - however you go for it, you'd have to severely discount this great, Norwegian business to find a downside at 430-440 NOK. It's not the best price , but it's a damn decent one.

While peers trade closer to 5-10X and Yara now still trades above 10x P/E, this company has yield and price upsides that the peers don't have - especially BASF ( OTCQX:BASFY ).

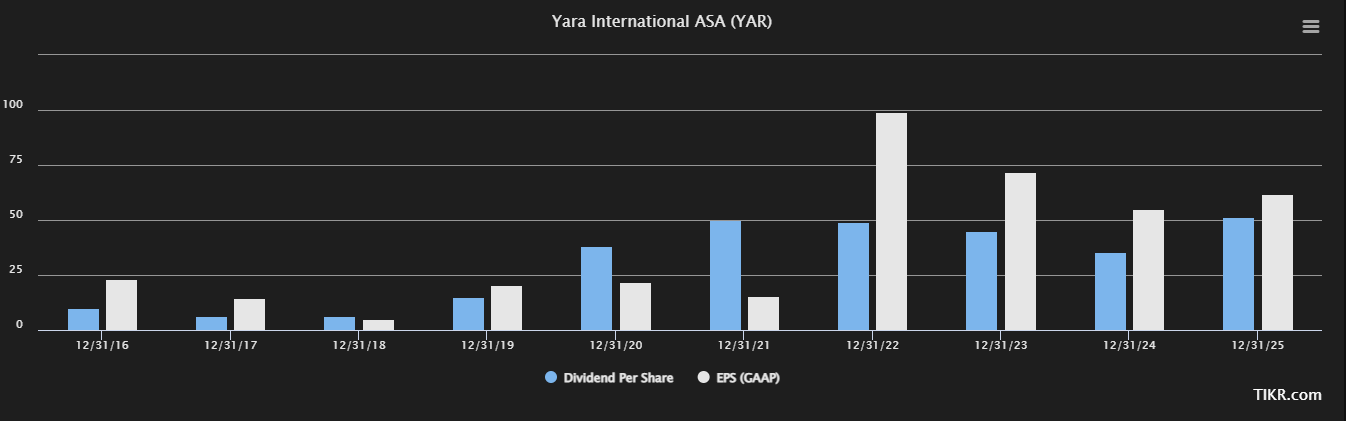

As I've said before, crisis modeling is rough - that's especially true when we're talking about something cyclical like fertilizer. I could try and forecast a 10-15% EPS growth and try to guesswork energy pricing trends, but given how much volatility is in the market today, that's not something I'll do either. Conservative NAV gives us 425-430/share, but that really discounts some of the improvements that the company has been doing.

Yara EPS/Dividend Forecast (TIKR.com)

{kind=link}

When I last wrote about Yara, it was at 415 NOK - so 430 isn't as attractive - but it's still a decent "BUY" if you want fertilizer exposure.

For these reasons, I call this company a "BUY" here. I'm holding my large position in Yara, and I'm not divesting it at this time, at least not unless you count the covered calls I'm writing which technically opens me up to the potential of a sale.

I'm very interested in seeing what 4Q22 and the year-end bring us.

S&P Global looks at Yara and averages 17 analysts with upsides to a PT of 475 NOK/share - surprisingly reasonable, all things considered. This is from a range of 380 NOK to 560 NOK - again, surprisingly reasonable. I believe some of those 17 analysts must be valuation investors because I can see my way very clearly to reaching either way of that range by discounting or allowing for various realistic impacts and upsides.

Only 5 out of 17 analysts are at a "BUY" here, despite the company trading significantly under the PT - and upside of close to 10%.

My, I'm somewhat more conservative. 420 NOK was my latest PT - I'm not going neutral, but sticking to my range of 420-450, and going to 435 NOK, a good midpoint, and calling this a "BUY" here.

However, I won't be adding due to my position at this time. It's already above 6%, and that's as high as I want to go.

I believe Yara for 2023 can go as high as over 500 - at which point some of the calls I wrote will be ITM and I'll be happy to start bonsaiing slowly - or it could stick to a 380-450 level for the year - also acceptable given the dividend, but I don't see it disconnecting massively below those levels at the current macro.

Thesis

- Yara is one of the best/most appealing fertilizer businesses on earth and by far the most attractive with a combination of quality/fundamentals and upside that I see. The company combines legacy appeal with future-proofing, and I see only limited downside at any sort of conservative valuation. That is why Yara is my biggest single position.

- Yara has a potential longer-term upside at these fertilizer prices. The headwinds for Yara are very real, but none of them have, as I see it, the potential to seriously de-rail this company in the near term.

- Yara is a "BUY" here, though every investor, of course, needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this.

- I give the company a PT of 435 NOK for the common.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Yara cannot rightly be called "cheap" at 430 NOK, but it's nonetheless attractive here.

For further details see:

Yara: 2023 Upsides And Targets Are Clear To Me