YARIY - Yara: A Buy Following A 55 NOK Ex-Dividend Correction

2023-06-16 02:31:34 ET

Summary

- Yara International is a solid fertilizer play with a massive potential upside from both geopolitical and economic macro. I'm long on the company.

- Yara has had a superb 2022 with some of the best results in the company's history. However, 2023 is going to see some different overall trends.

- The company recently dropped over 55 NOK, in part due to the ex-div. Here's my updated thesis for the business, and I maintain "Buy".

Dear readers/followers,

Yara ( YARIY ) is a fertilizer company that I've been reviewing for several years. It also happens to be one of the largest overall positions in my entire portfolio, accounting for both commercial and private investment portfolios. My stake here is representative of my conviction in the company's long-term viability, which in this case is very high.

That being said, this is a very volatile business because it's tied to commodities pricing levels. So expect this to go up and down, and be sure to buy it at a "cheap" valuation, which is actually something we have here at this time.

What do I mean when I say that we're at a cheap valuation because, after all, the company is down almost 17% since my last article.

Yara International RoR (Seeking Alpha)

There are reasons for this development, obviously. The company is, despite this, an investment with a potential upside to the native 500 NOK level before I would entertain the possibility of starting to rotate shares.

Let's review the latest results and why this is such an amazing business to, in my opinion, invest heavily in.

Yara - Investing in food production

An investment in Yara, dear readers, is an investment in food production itself because Yara is one of the world-leading providers of quality fertilizer. The company is a global player in agriculture and the production of food, which thanks to current demographic trends, are bound to continue to grow both in demand and in scope going forward.

The company is, as I see it, a two-way sort of play. I run long-dated covered calls for my large positions, with Yara being over 5% of my portfolio. The strikes for those calls are at 550-580 NOK, and I recently sold a very attractive one in the low 500s.

At the same time, I run cash-secured puts, because I'm always willing to "BUY" Yara if the company were to drop below 320-340 NOK/share.

Why is this such a high-conviction case for me then, you might wonder.

Because I know where the company is, where it should be valued, and where it seems to be going.

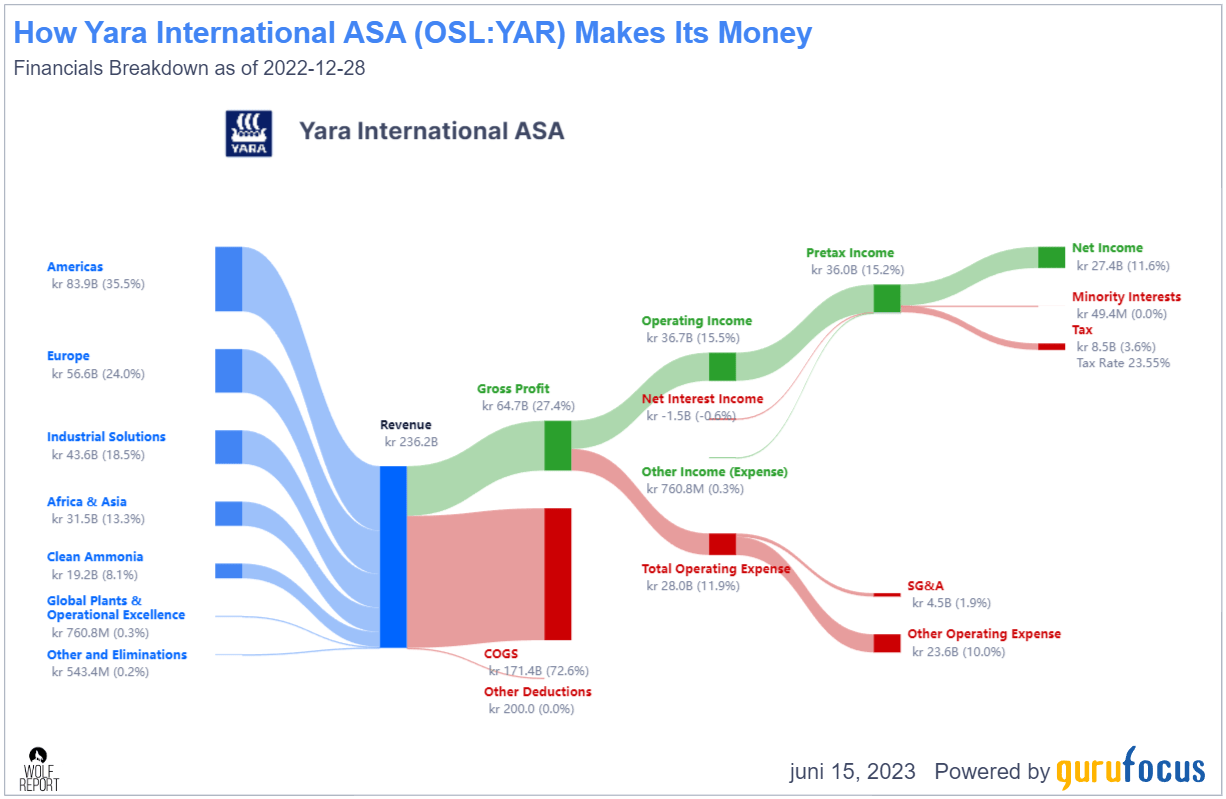

2022 was one of the best years in the company's history, managing to improve returns for every single commercial segment. That we're on a comparative basis isn't going as high as this seems like a given to me, and the 1Q23 results give confirmation of this.

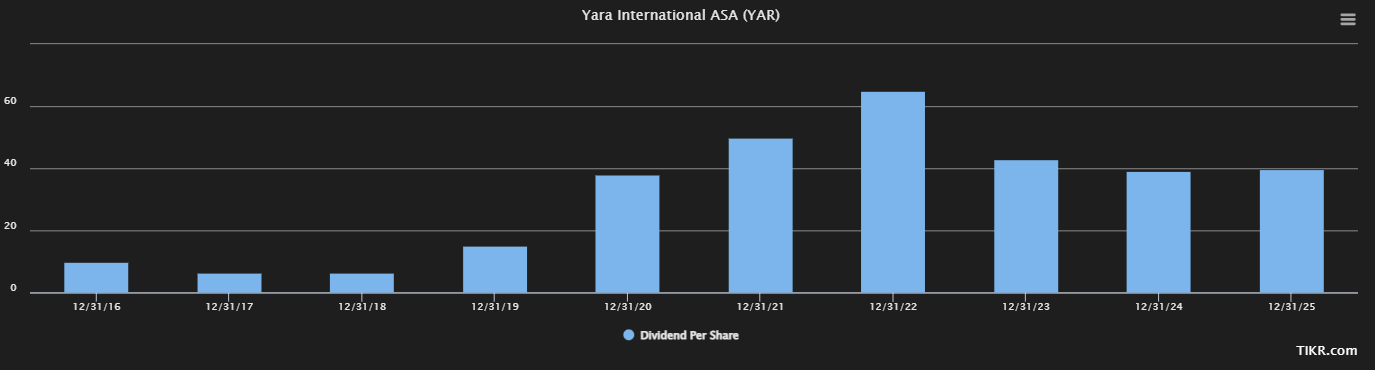

First and foremost, however, why did Yara drop the equivalent of 60 NOK native in 2 days? Well, it's climbing today, but 55 NOK of that drop was due to going ex-div. Because Yara's dividend at this time is so massive - over 16% YoC for me - that's going to take a big chunk out of the share price whenever it goes ex-div.

Even based on the current share price, it's well over 13% if it'll even be close to maintain, which I, unfortunately, do not believe that it will - nor am I alone in this belief - it's an actual S&P Global forecast. Here are the forecasts as they are expected for 2023 and the coming few years.

Yara Dividend (TIKR.com/S&P Global)

{kind=link}

I believe, based on macro and earnings trends, for these forecasts to be fairly accurate. However, even if that were to materialize and 40 NOK is the "best" we can expect from the company at this time in the next few years, that 40 NOK is still a 10.8% yield based on a current share price of 370 NOK.

And based on forecasted earnings, that yield is quite well-covered despite the implication of a double-digit yield when it comes to risk.

So, even in the case of several small dividend reductions, there's still a yield attraction to this investment. Now let's talk about fundamental attraction - because there is a lot to be said about that as well.

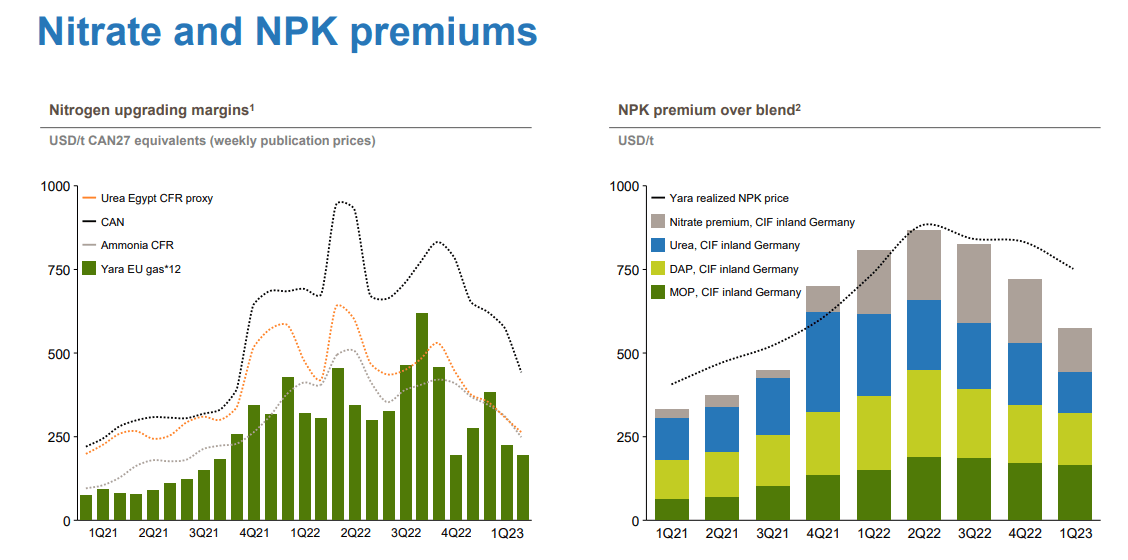

So, as things are now, we're already seeing indications of these trends turning around in a way that will impact company earnings negatively. Results for 1Q are weak, but this is again compared to 2022, which was strong. Steep market price declines are impacting both volumes as well as margins and earnings.

There are also still production curtailments at around 0.6 mt, and 1.3 mt finished fertilizer for the quarter. Negative volume effects have over $360M worth of effects, with inventory write-downs due to trends, which are more than offsetting the positives from lower natural gas prices in terms of feedstock.

Operating cash flow is up, however, due to capital releases. And some feedstock markets - like nitrogen - are even tighter than before, due to strong EU demands with resulting strong pricing.

Commodity pricing is down.

Yara IR (Yara IR)

Purchasing in Europe has been delayed. Imports are replacing some of the curtailed capacity, which in turn improves some of the comps going into 2Q. The negatives are really lower deliveries because farmers are purchasing at later dates. Current EU production curtailment is at 1/3rd of the full capacity, and only partially replaced by ongoing Urea imports.

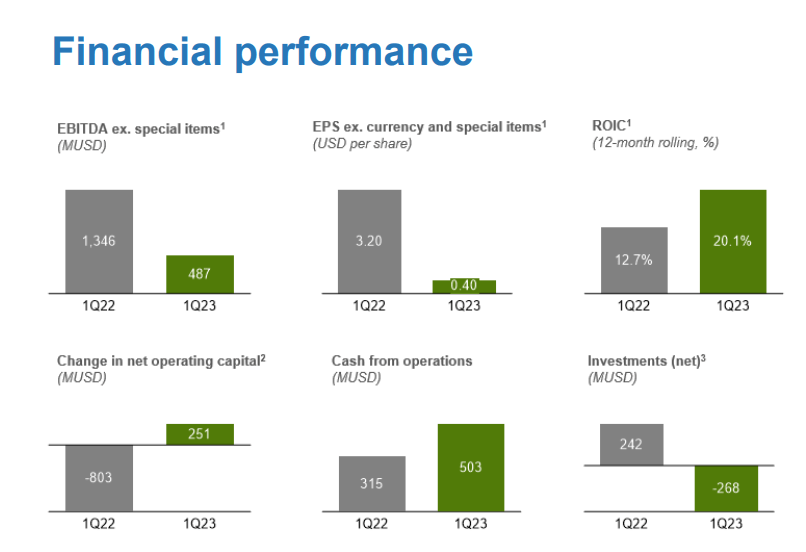

The financial performance tells the story of this quarter.

{kind=link}

It's important to clear up that this was expected. This company was bound to decline. I'm actually considering it a positive that ROIC levels are not declining in any one segment/geography except with global plants. America's ROIC is up 1000 bps, Africa and Asia 1000 bps as well, and Europe is almost flat. Deliveries are down double-digits, but that really is from high levels.

Net debt is actually down, as is close to going below $3B. The company has also initiated a partnership with Enbridge (ENB) for carbon capture, with service expected in 2027E.

And the major argument for investing in Yara really still involves fundamental demographics and overall macro trends. It's an investment in food, and it's one of the best-managed fertilizer businesses on the planet.

{kind=link}

So if you invest in Yara, you should do so with the mindset of a long-term shareholder. Selling the company is acceptable, if it were to spike to relative heights, which at current earnings numbers and fundamentals would be above 500 NOK. At that point, even I would start to consider selling shares. Here though, the company is cheaper than it has been in some, even considering that you won't (likely) get a dividend for this year, and you can expect the next payout to come in 2024. I don't think this year's results will allow for a fall-paid bonus dividend, as we've seen in the past few years - or if there is one, I consider that dividend to be relatively small.

Yara remains a play on premiums and pricing. During 2022, we had some of the highest pricings for commodities, but also for fertilizers in history. That naturally translated into high costs, but even better margins and earnings for Yara.

Yara International IR (Yara International IR)

{kind=link}

But this positive is now winding down, and we need to be prepared for the effects this will have on the share price.

The company's FCF has significantly turned around from the consistently negative levels we saw several years ago in 2018-2019. But now it's time for the cycle to normalize - though I don't expect, based on macro, for this to happen to a negative FCF level.

It's important to consider that when premiums and pricing normalize, input pricing and energy costs tend to do so as well. So the trip down isn't going to be as volatile as you might fear.

Let's see what this does to company valuation.

Yara International - The valuation remains a compelling part of the story

Yara is a massively attractive, as I see it, business, even looking beyond 2022. Most standardized models and analysts consider the company significantly undervalued and for a good reason. Many of the services or analysts give the company price targets which even I would consider excessive or "too positive", with some GF-valuation targets based on projected FCF, tangibles, PS values, and graham numbers, going as high as 750 NOK/share. That is, as I see it, bordering on ridiculous.

Yara remains a fertilizer company, and it does remain volatile. Its debt to EBITDA is 1.17x, making it one of the best-leveraged fertilizer companies in the world. It's margins are solid, and even if these were impacted by about 30% across the board, the results would still come out relatively positive.

{kind=link}

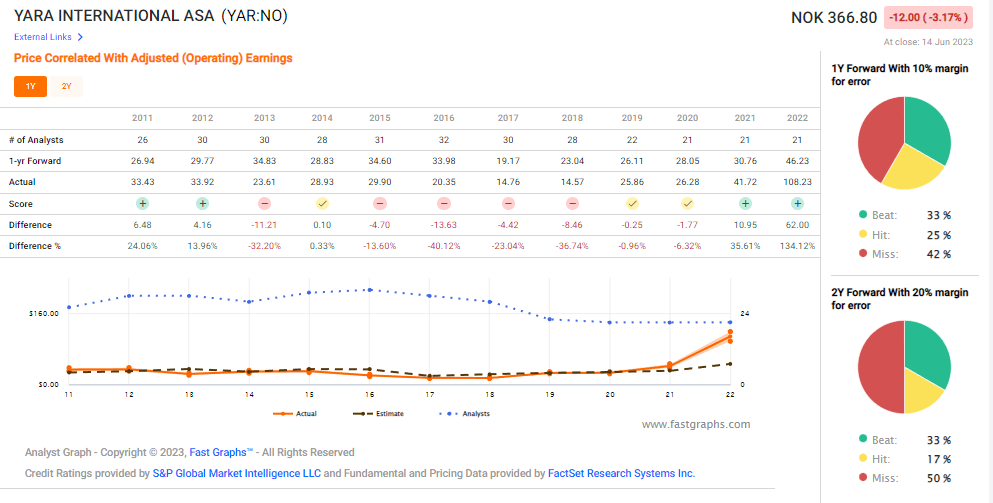

Exact forecasts here are not easy. This is easy to confirm - forecast accuracy here is close to zero, if we consider both negative and positive misses on a 1-2 year forward basis. The suitable takeaway here is that analysts cannot accurately forecast this company.

Yara Forecast Accuracy (F.A.S.T graphs)

{kind=link}

The difficulty here is that there is a consensus that Yara prices and valuations are either moving down due to current macro trends, or they're certainly not moving up further from here. Compared to the 108 adjusted EPS in NOK, the forecast for 2023E is 42 NOK, followed by 42.6, and then 44.8 NOK. And based on current trends, I consider this to be fairly accurate - meaning almost zero growth for the next few years. FactSet and S&P Global analysts are also pretty consistent in their forecasts here, and I would say it's the "best we have".

S&P Global analysts consider the company an attractive "BUY" with a range of 350 NOK to 525 NOK, averaging out at 440 NOK. That's around 30 lower than my last article, with 18 analysts still following the company with 6 of the 18 at a "BUY", and most at a "HOLD". This mirrors my assumption quite well that many investors are currently waiting to see where Yara may go.

I'm not doing that. When the company dropped, I actually went ahead and added some shares to my commercial account, in addition to adding some cash-secured puts at the low 300's with a 45-day expiration. Easy money - or great prices on Yara, as I see it.

At a sub-450 NOK price target, I believe the combination of yield and still-present upside in this macro and given the foundational nature of the company's products in our current world, to still be enough to warrant a "BUY". I'm not shifting my price target for this company at this time. The decline in earnings was something I already took into consideration. If 2Q comes in worse than expected, I may lower it further, but for now I'm considering my target to be valid - and for the 55 NOK drop to only add to the appeal of the long-term investment in Yara International.

Because of that, my thesis for the company is as follows

Thesis

- Yara is one of the best/most appealing fertilizer businesses on earth and by far the most attractive with a combination of quality/fundamentals and upside that I see. The company combines legacy appeal with future-proofing, and I see only limited downside at any sort of conservative valuation.

- That is why Yara re mains the biggest single position in my entire portfolio.

- This goes for both my private investment account, as well as my commercial/corporate account where I invest proceeds and profits from my business dealings.

- Yara is a "BUY" here, though every investor, of course, needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this.

- I give the company a PT of 450 NOK for the common.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Yara cannot rightly be called "cheap" at 444 NOK, but it's nonetheless an appealing stock here. If you have access to the Oslo options market, then that is another avenue you might go.

For further details see:

Yara: A Buy, Following A 55 NOK Ex-Dividend Correction