YARIY - Yara: One Of The Safer Commodity Plays In This Environment

2023-03-20 12:51:37 ET

Summary

- Yara International is a solid fertilizer play with a massive potential upside from both geopolitical and economic macro. I'm very long the company.

- In this context, this company is a superb high-yielder with a continued upside to over 500 NOK/share.

- I'm still at a "BUY" for Yara, and here is why.

Dear readers/followers,

If you've followed my thesis for Yara International ( YARIY ), you'll know that I have been expanding my coverage of the company for years, buying more and more shares. At this point, over 5% of my overall portfolio and 4% of my corporate portfolio is made up of this Norwegian company.

Why?

Because Yara combines what I see as two very appealing facts. They reward shareholders while maintaining a conservative, and sector-leading set of operations. Yara has, over the course of the past few years, paid out massive amounts of dividends over the past few years, while also delivering impressive amounts of safety, if perhaps not stability.

Since my last article, the company has underperformed. What do I think about this? I don't really mind, given the safety of the company.

Let me update my thesis for you and give you my view of where the company is going.

Yara - Superb yield and superb upside for 2023.

Yara is a two-way play for me. I have a massive long position, I have long-term expiration put options running at strikes close to 340 NOK, and I have long-term dated calls , running at prices of 550-580 NOK/share.

Why do I have this, and maintain a long position valued at well over 5% of my overall portfolio?

Because I know where the company is, where it should be valued, and where it seems to be going.

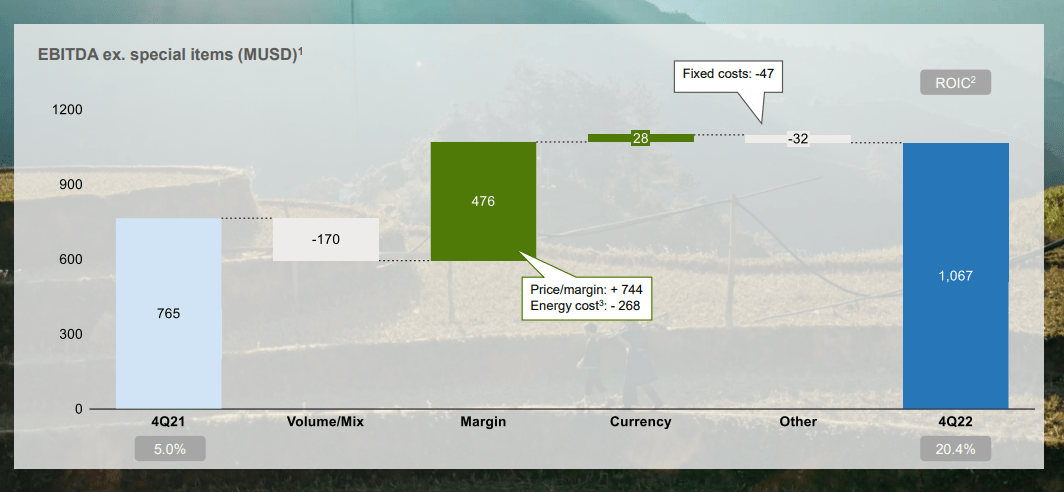

Yara delivered absolutely stellar levels of returns in 2022. Yara delivered solid cash flows and increased returns for all commercial segments , which is exactly what I was counting on. The improved company margins due to pricing offset the volume/mix issues the company saw in both 4Q and in full-year results.

{kind=link}

Now let's talk dividends because this is a big one. The company has announced 2022, to pay 2023 dividends of 55 NOK/share. That comes to a yield on the current share price of 12.2%, and it's a safe dividend. Not every day do you see something like this.

But that's not even all. Allow me a moment for an exercise here. Over the past 3 fiscals, including the company's dividends both regular and bonuses and including buybacks and redemptions (these are small), the company has paid out/returned 175 NOK per share to shareholders. If you exclude buybacks and redemptions, this still comes to a pure dividend payout over 3 years of 153 NOK/share. This is, based on an average share price of 430 NOK, a yield of 40.7% or 35.5% pure dividend yield over a 3-year time period.

Not only that, you could have bought the company at less than 380 at times, which means you'd add substantial amounts of capital appreciation to that.

My RoR for Yara, inclusive of FX and dividends, is over 100%.

I say again, this is a great company - and it's one I love owning.

It produces nitrogen fertilizers, ammonia, urea, and nitrogen-based chemicals. Focal areas are, naturally, crops and farming. Historically speaking, the company was founded 115 years ago as Norsk Hydro ( NHYDY ) - yes, that's the same Norsk Hydro that I've written about for pretty much my entire career as a contributor, and had some massive, triple-digit successes with as well.

Norwegian companies should never be underestimated. I "play" with a lot of them both in the long as well in the options, with both calls, puts, and positions running.

What's more, Yara can essentially be considered an arm or part of the Norwegian government. Through a combined stake from the Ministry of Trade, Industry and Fisheries, and the pension fund of the nation of over 40% of the outstanding shares for the company.

Yara International has 17000+ employees, sales to 160 countries, and generates tens of billions in annual revenues. Out of its closest peers, very few are the size of Yara, and what's more, very few companies have the international footprint that Yara gives us. What's more, Yara is not dependent on Potash or similar trends, which can be considered legacy. I cover Potash as well, and I'm not negative about potash, but I consider Yara to be substantially better.

That is why my position in Yara makes my other fertilizer investments currently look like peanuts. It also has to do with the fact that not only am I familiar with the company to the degree that I've visited IR and their offices, but I've also been researching them for over 6 years.

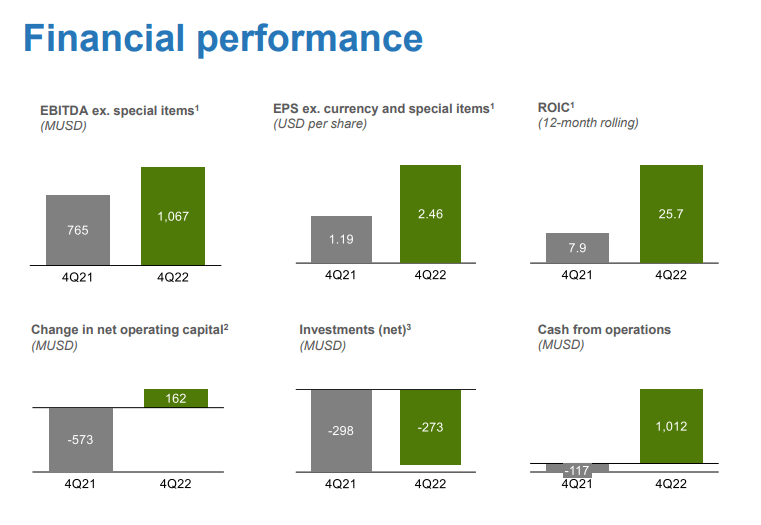

Financial performance in 2022 was, in a word, superb.

{kind=link}

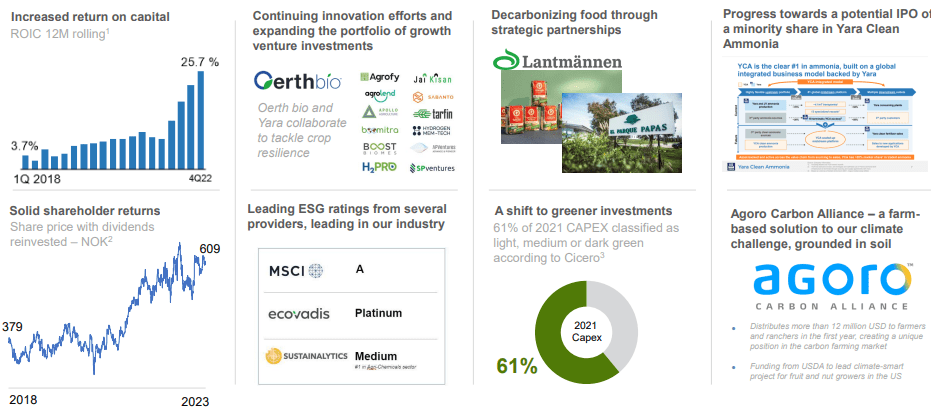

Between improved returns in every single commercial segment, the only negative we could see for this comes from the fact that sales volumes are actually down, given the pricing for the stuff. While pricing for fertilizer is down, much of the market is still seeing delayed purchasing trends from customers. Despite these trends, Yara still managed great progress on its objectives, both strategic and financial. ROIC is up to 25.7%, compared to around 3.7% back in early 2018. The company is further decarbonizing its production and its sales, and moving to greener investments, turning the company into an already-A-rated ESG leader with Platinum and A-rated scorecards.

{kind=link}

Again, plenty to like. The nitrate and NPK premiums which dictate much of the company's returns are still seeing good trends - but expect Yara's earnings in terms of its pricing tart to drop here going forward, requiring a recovery in the volume/mix part of the business.

Aside from this, a few things we should keep an eye on include the demand situation and the nitrogen value chain. The company is already confirming to me, both with the presentation and my contact with IR, lower activity on the purchase side. It's not unusual, but I interpret this as the beginning of a trend, and because we're heading into/are currently in the main product application season (with respect to planting and the like), it will pay off to look at both the 1Q23 and 2Q23 trends with regards to this, because this is likely what will be driving share price development.

What's basically on everyone's mind at this time is how the demand situation is going to be developing. Second is European capacity curtailment, and when or if this is going to be changing. Yara is still not, as of 4Q22, producing at anything close to the normal levels, and once this normalizes in line with the natgas/energy price, this too will change things. A lot of how things look when you look at Yara today is what specific geography you're looking at. Europe is still troubled - the rest is going fairly well.

What you want to look at when it comes to Yara is the balance between the various commodity pricing levels and the demand-side development from the customer side. I see that for the foreseeable future, and even with a demand decline, the company will be in a better position to push pricing and trends than they have been for many years, and this forms the continued positive thesis that I have for Yara International.

Yara International - The valuation

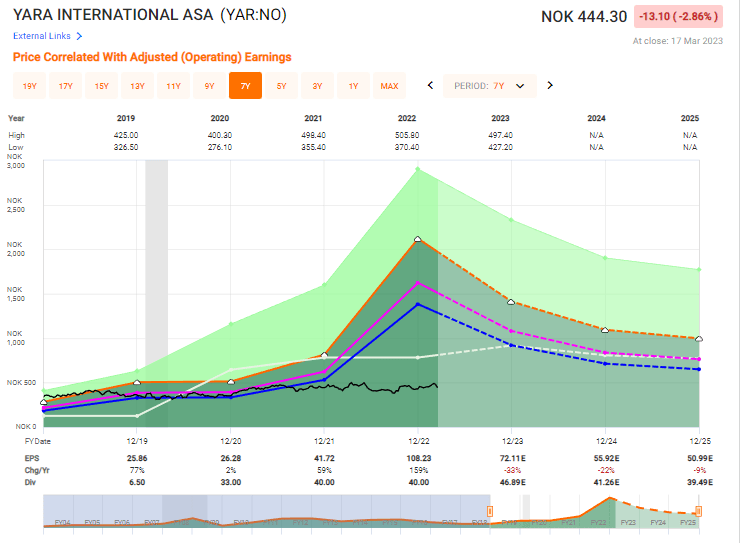

My price target for Yara has long been around 420-450 NOK, and that remains. I'm not shifting that one for this article - but I do want to point out, and clearly emphasize, that's as high as I would go. And above 450 NOK is really stretching it. This is especially true when we consider the current overall trends in demand, which seem at this point to be inching in the other direction.

1Q and 2Q numbers will provide some more clarity on these points, but I'm emphasizing here that you might be careful not to buy at too far above that 450 NOK mark. I understand that the yield, safe as it is, is very enticing here, but there's still a potential downside risk.

That's the reason I run both puts and calls options on this company. I could try and forecast a 10-15% EPS growth and try to guesswork energy pricing trends, but given how much volatility is in the market today, that's not something I'll do either. Instead, I'll give you my assumptions for where I see the company realistically going, with a conservative touch, in the next 12-24 months - and even that is stretching credibility.

Yara has long traded between the 300-450 mark, only to occasionally go above 500. The fact that I managed to sell relatively attractively-priced Calls at 560-580 strikes tells you where I believe the company won't go, not even in a positive situation as we've seen in 2022.

{kind=link}

Essentially, it's downhill from here. The company's earnings have been an absolute outlier, and it's doubtful that they'll be repeating anytime soon. Now, the downward trajectory might be less sudden or slower than we see in forecasts here, including that 33% drop in 2023, but I believe the overall trajectory is correct.

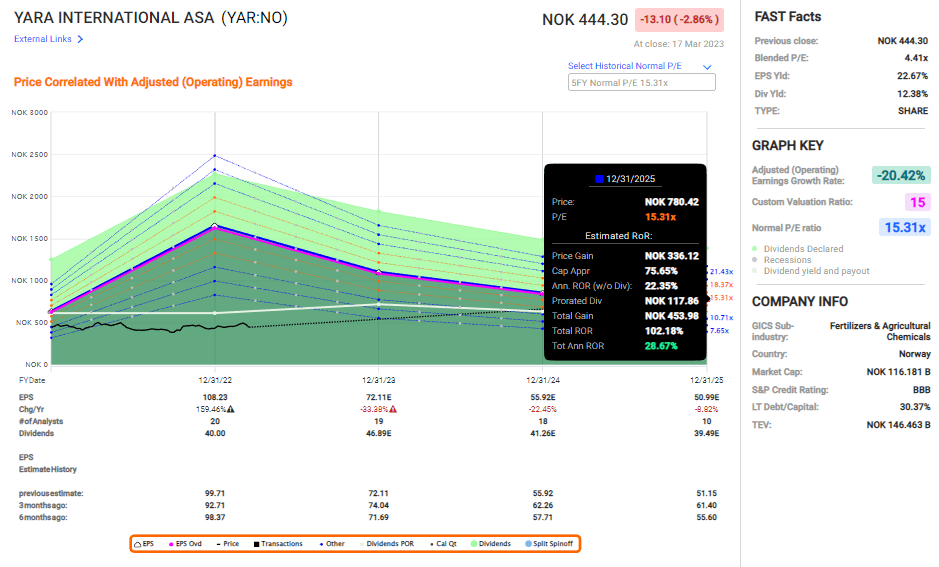

However, because Yara hasn't really moved outside of the share price range where it typically trades, this means that while it could affect the short to medium-term, the appeal is still very much there. About 3 years ago, a 444 NOK share price represented a P/E of 17.16x. Today, it represents a P/E of just north of 4x.

I can tell you that I believe 17x is more "correct" than 4x in the long run, even if the company might see foundational increased EPS levels in the next few years, perhaps more commonly seeing 30-40 NOK EPS.

The upside to normalized P/E levels, which currently are forecasted to be around 40-50 NOK in 2025E, is still 28.67% per year, or 100% RoR in a few years. Given the company's generous dividend policy, confirmed by the fact that the Norwegian government is very adamant about wanting its continuous pay-outs from its investments, this is not an unrealistic prospect.

{kind=link}

S&P Global looks at Yara and averages 18 analysts with upsides to a PT of 480 NOK/share - surprisingly reasonable, all things considered, given where the company's earnings have gone last year.

This is from a range of 360 NOK to 560 NOK - again, surprisingly reasonable, and it shows you why I've placed my options at the strike prices I've targeted. However, despite the company being below this target, most of these analysts are currently at conservative ratings of either "HOLD" or "Underperform". Only 6 out of 18 are at positive ratings.

I believe this to be wrong. At a sub-450 NOK price target, I believe the combination of yield and still-present upside in this macro and given the foundational nature of the company's products in our current world, to still be enough to warrant a "BUY".

For that reason, I present you with my refreshed thesis for Yara International.

Thesis

- Yara is one of the best/most appealing fertilizer businesses on earth and by far the most attractive with a combination of quality/fundamentals and upside that I see. The company combines legacy appeal with future-proofing, and I see only limited downside at any sort of conservative valuation.

- That is why Yara is my biggest single position in my entire portfolio.

- Yara is a "BUY" here, though every investor, of course, needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this.

- I give the company a PT of 435 NOK for the common.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Yara cannot rightly be called "cheap" at 444 NOK, but it's nonetheless an appealing stock here. If you have access to the Oslo options market, then that is another avenue you might go.

For further details see:

Yara: One Of The Safer Commodity Plays In This Environment