USX - Yellow Corporation: Cheap Price But Escaping The Pothole Remains Hard

2023-05-10 20:14:28 ET

Summary

- Yellow Corporation stays sluggish with its hammered revenues and margins.

- Its financial positioning is quite bothersome for a capital-intensive company.

- Near-term market prospects are mixed, given the potential recession and decreasing inflation.

- The stock price continues to decrease, making it very cheap.

The freight and logistics market saw disruptions as inflation peaked in 2022. The softening demand and clearing supply chain bottlenecks gave more headwinds. And even an industry trailblazer like Yellow Corporation (YELL) did not avert its adverse impact. This year, the company may experience another wave of disruptions as recession fears persist. It can become more challenging as it started the year with a lackluster performance.

Moreover, it must be careful as it heavily relies on borrowings. Interest rate hikes may continue and reduce its liquidity levels. Likewise, the stock price remains at its lowest point. It should not be surprising as its fundamentals are quite unappealing. Even so, the downtrend makes the stock very cheap despite its limited upside potential

Company Performance

It’s been almost a year since I last covered Yellow Corporation, and even today, market challenges are evident and hammering its performance. The freight and logistics industry must handle and get through these disruptive times. Even worse, The Fed expects a mild recession that may further lower aggregate demand. We can associate it with the skyrocketing interest rates, which attracted savings and discouraged borrowings and investments. As such, market volatility may remain evident and affect the capacity to stabilize growth and margins. The same applies to YELL, given its limited rebound potential.

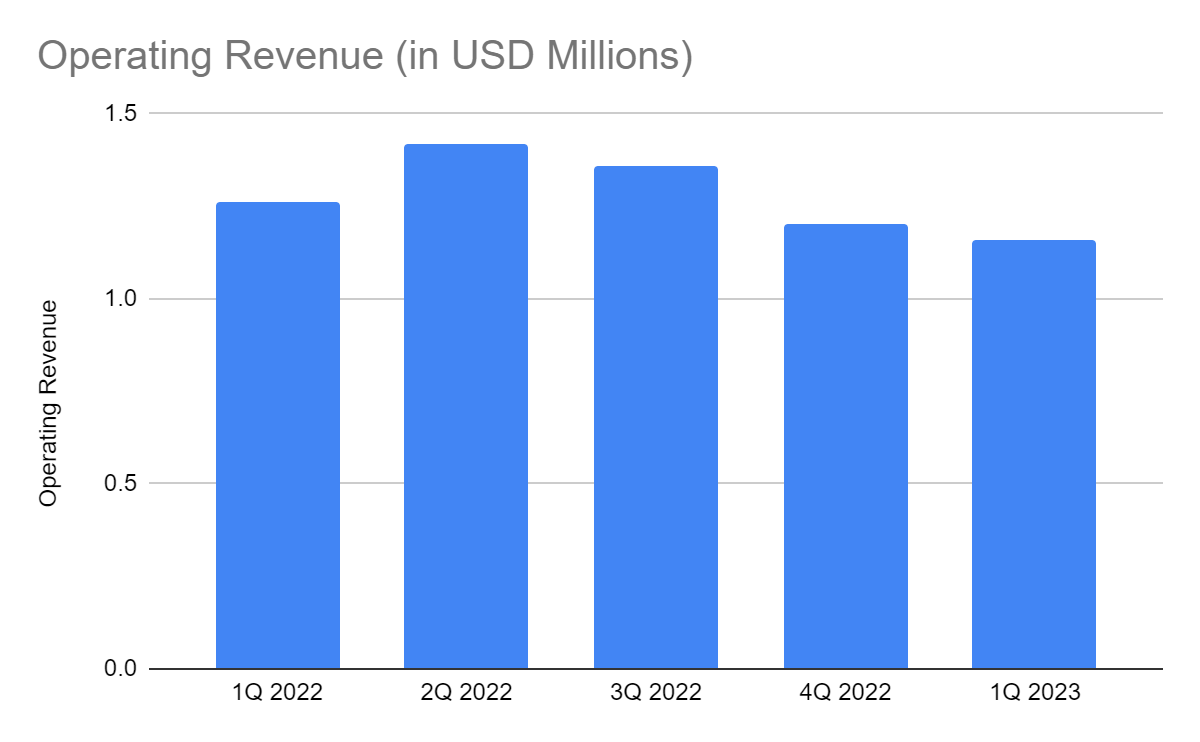

Its operating revenue amounted to $1.16 billion , a -8% year-over-year decrease. We can also see the consistent revenue decrease since 2Q 2022, which we can attribute to inflation. Although the management expressed its positive view, we know it was relatively weaker. It was quite disappointing, given the continued decrease in inflation since 4Q 2022. On a lighter note, we can attribute the softer demand environment to seasonality.

Note that holidays are also vital to its performance. In essence, holidays are at their peak during the second half of every year. However, we can’t deny the fact that Yellow can hardly cushion the blow of macroeconomic disruptions. By 2Q 2022, we already saw the softening demand across industries. The continued downtrend helped slow down inflation. But cost-of-living adjustments could take more time due to supply inelasticity in some industries.

Moreover, its effort to counter the decreasing demand through pricing remained futile. It attempted to set more strategic pricing to stabilize demand and shipment rates. LTL revenue per hundredweight and shipment across its business segments rose by 4.4% on average. Yet, LTL shipments per workday dropped by 12%. With that, it is logical to assume that the company had limited pricing flexibility. Despite its size and domestic market presence, it had a hard time rebounding from its 2022 troughs.

{kind=link}

Operating Revenue (MarketWatch)

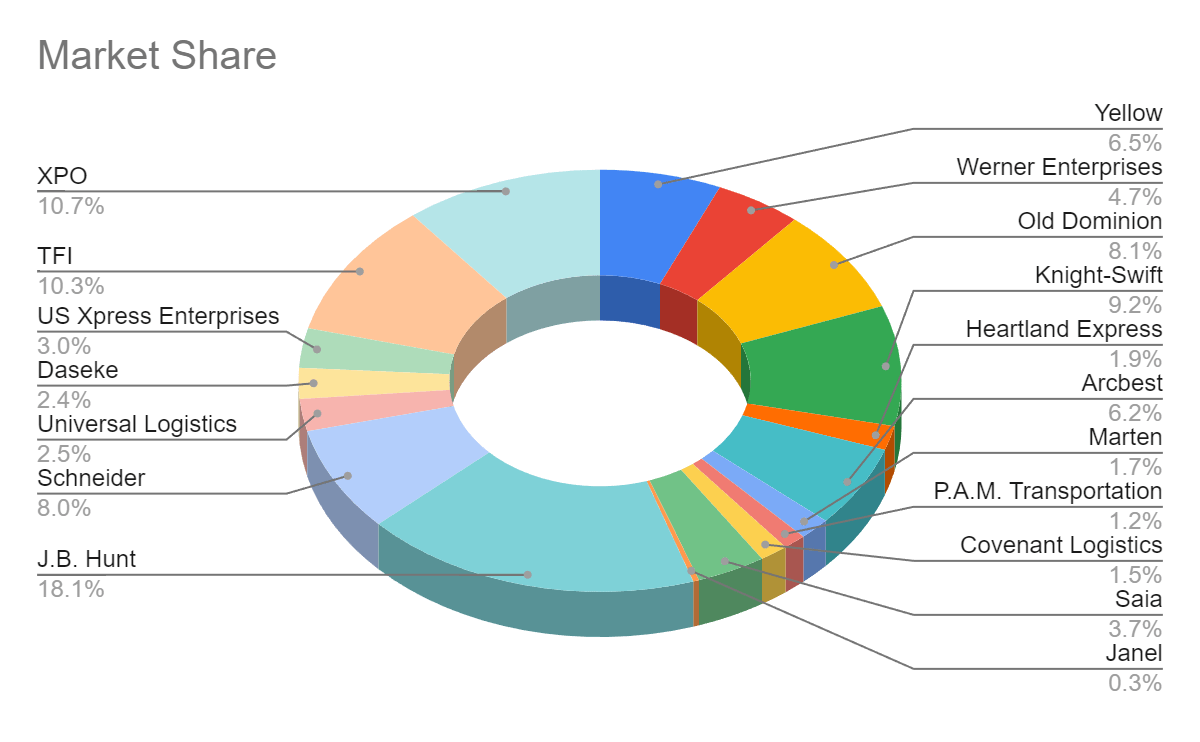

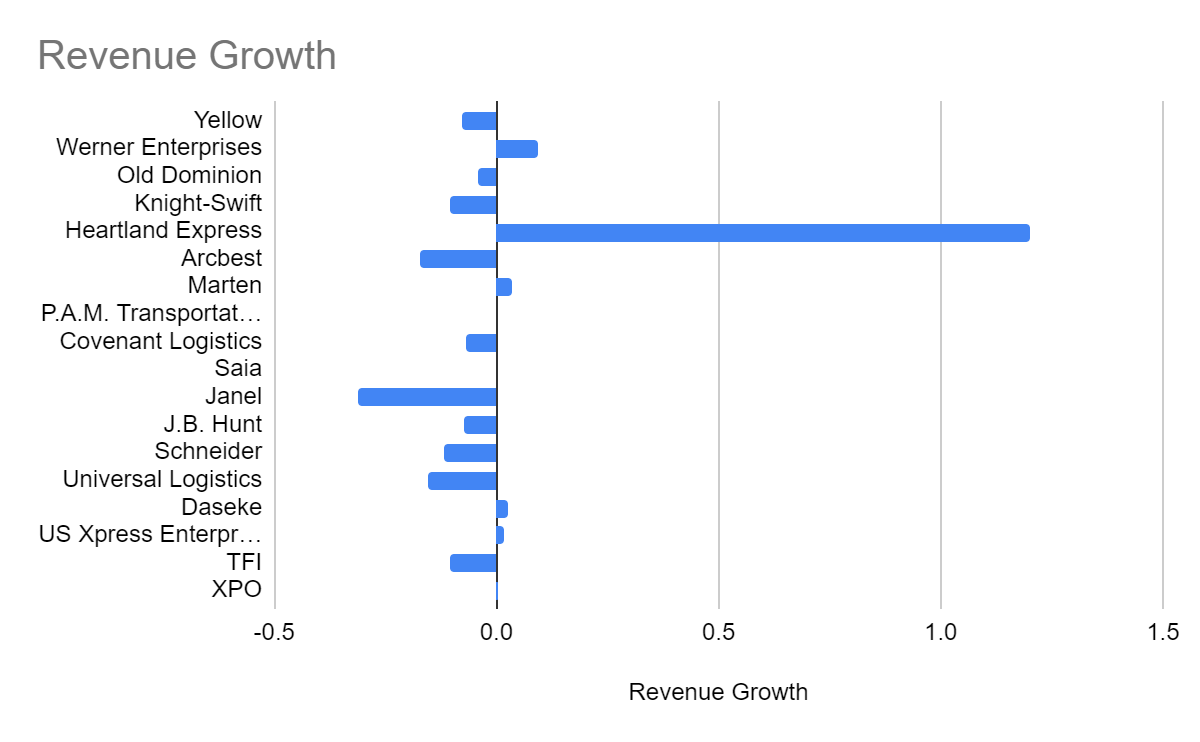

Relative to its peers, YELL remains an essential figure with a market share of 6.5%. It was higher than in my previous coverage with 5.6%. But it was still lower than 1Q 2022 with 6.8%. We can attribute it to its revenue decrease, which is opposite to the average market revenue growth of 0.80%. Also, it remains weaker than its peers like Old Dominion ( ODFL ) with -4% and Werner ( WERN ) with 9.2%.

{kind=link}

Market Share (MarketWatch)

{kind=link}

Revenue Growth (MarketWatch)

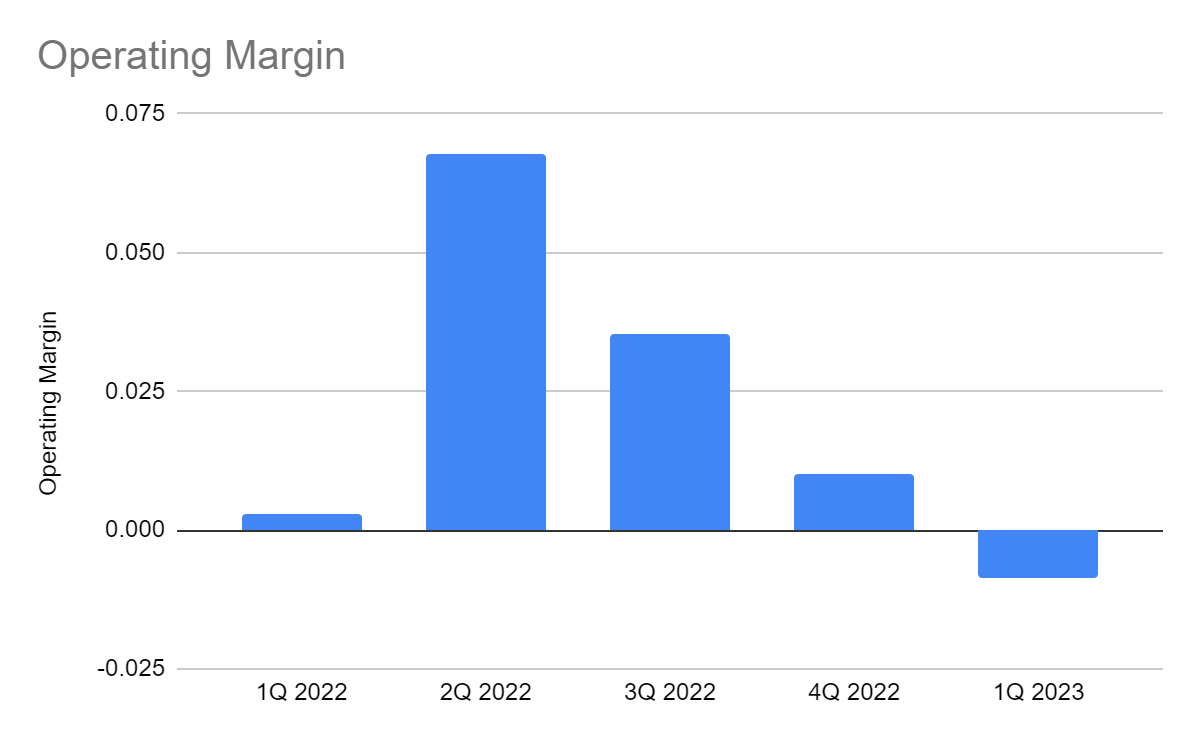

Meanwhile, the company improved its operational efficiency to deal with inflation. Its operating costs and expenses were $1.17 billion, a 7% year-over-year increase. The only problem was that the impact on revenue was higher. Its effort to stabilize costs and expenses did not offset the decrease in revenue. Also, costs and expenses were higher than revenues, leading to an operating loss. The operating margin dropped to -0.84% versus 0.29% in 1Q 2022. It was also the lowest margin in five quarters. Relative to the market, YELL continued to underperform versus the average margin of 8%. It was also the lowest among the companies in the chart. Most of them had positive margins, and only Yellow and US Xpress ( USX ) had negative margins.

{kind=link}

Operating Margin (MarketWatch)

This year, YELL may stay slow-moving since it may face similar challenges. We must also consider interest rate hikes that may continue to affect consumer spending. Despite this, decreasing inflation may help stabilize costs and expenses. It is more crucial today, given its lower demand and large operating capacity. We will discuss it further in the following section.

Potential Threats And Opportunities For Yellow Corporation

Yellow Corporation operates in a highly cyclical and volatile market. It may take more time before the company can heave a sigh of relief. Market risks are still evident as demand remains soft. Also, supply chain bottlenecks have eased, so there is a lower need for shipments. Interest rate hikes continue to aggravate the situation as it makes borrowings costlier and investments less enticing. With more people and businesses choosing to save rather than invest, production and consumption may be affected. As such, a mild recession may take place this year.

Yet, hope floats as gradual improvements become evident. It may not materialize anytime soon, but the positive spillovers may help the company in the long run. Inflation is a potential rebound driver as it continues to decrease. It started in 3Q 2022 and accelerated earlier this year before landing at 5% . Today, it is 45% lower than the 9.1% peak in 2022. The inflation downtrend may be instrumental in increasing the purchasing power of customers and business owners.

So, pricing flexibility may increase and drive revenue rebound. It can also help stabilize costs and expenses. It may be evident in fuel surcharges and expenses as fuel expenses. Fuel prices remain quite high at $3.711 per gallon, but it was already way lower than the 2022 peak of $5.032 per gallon. Overall, the freight and logistics market, including Yellow may still bounce back. It is vital in driving macroeconomic recovery and growth. Movement of goods and services play a vital role, whether in established or emerging economies.

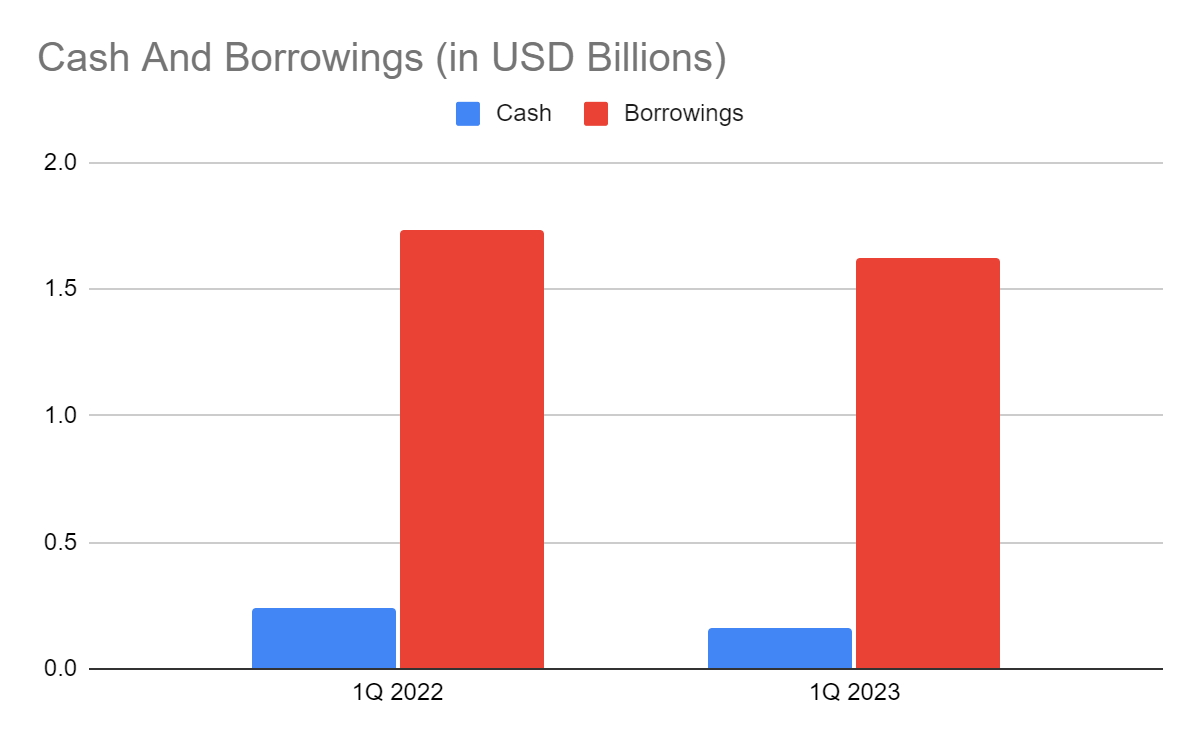

But before we conclude, we must check Yellow’s capacity to sustain its operations amidst market headwinds. If we check the Balance Sheet, we can see that cash decreased by 33% in only a year. Accounts receivables are almost unchanged, proving the slow-moving performance of the company. Another concern is its borrowings of over $1 billion. The only consolation is that cash remains high at $155 million and was used to pay 90% of its current maturities. Even so, liquidity remains unappealing, given the Net Debt/EBITDA Ratio of 5x.

It is higher than the maximum ideal ratio of 3.5-4.5x. Yellow must be more cautious since it is a capital-intensive company. It must do better to generate higher core earnings to limit cash burns and cover borrowings. We can confirm it using the Cash Flow Statement. After adding back non-cash transactions, its cash flow from operations increased to $12.6 million. But it was still lower than the CapEx of $29.6 million. It proved that the company had to burn massive cash to sustain its operating capacity. The company must improve its growth potential and viability to ensure sustainability.

{kind=link}

Cash And Equivalents And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Yellow Corporation has decreased substantially. But it is now at its lowest point after a series of sharp plummets in 2021 and 2022. At $1.42, the stock price is 37% lower than last year’s value. Its fundamentals agree with the continued downtrend, given the negative EPS estimates and book value. Meanwhile, the EV/EBITDA Ratio shows that the stock price decrease is becoming excessive, given the target price of (1.54 B EV - $1.46 B Net Debt) / 51,955,000 shares = $1.54.

Moreover, YELL stock does not pay dividends, making it more unappealing. It distributes capital returns through share repurchases, but it only seems to cover dilution. On a lighter note, the company still seems to dedicate itself to shareholders. We can compare the trend of its EPS and the stock price. From 2019-2022, the company had a cumulative EPS of -$7.82. Meanwhile, the stock price had an average decrease of -$2.83. It shows that for every $1 decrease in EPS, the stock price only decreased by $0.36. However, it didn’t help to improve shareholder value. To assess the stock price better, we will use the DCF Model.

FCFF $68,090,000

Cash $155,000,000

Borrowings $1,620,000,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 51,955,000

Stock Price $1.42

Derived Value $2.14

The derived value also shows that the stock price is already below the intrinsic value of the company. There may be a 50% upside in the next 12-18 months. Even so, their actual gap of $0.72 remains limited.

Bottom line

Yellow Corporation remains hammered as market conditions remain unfavorable. It must also be careful with its liquidity as cash burns and borrowings remain high. The only consolation we have now is that the freight and logistics industry is crucial to the economic rebound. As such, the company may still bounce back, given its current size and domestic market presence. It may also improve its viability and liquidity by selling some of its non-performing assets. But it may be difficult since it already has a negative book value.

Meanwhile, the stock price keeps decreasing. Despite this, price metrics show it is already fairly valued, although upside potential remains limited. Investors may still keep an eye on the company as it becomes cheaper, but there are many better alternatives in the market. The recommendation, for now, is that Yellow Corporation stock is still a hold.

For further details see:

Yellow Corporation: Cheap Price, But Escaping The Pothole Remains Hard