VIST - YPF Sociedad: Curb Your Enthusiasm

2023-12-16 07:50:40 ET

Summary

- YPF has seen success in Vaca Muerta production growth but has faced lower margins due to price controls and currency devaluation in Argentina.

- The company's financial statements have been overstated due to the use of an artificial exchange rate, causing potential declines in results with the devaluation.

- YPF may struggle to raise pump prices in line with the devaluation, leading to a decline in EBITDA in 2024.

- Downgrade to Hold on to a tough transition year ahead.

Summary

YPF Sociedad Anónima ( YPF ) has had success and failure since my last update a year ago: YPF Sociedad Anónima Stock: Oil Exports And Growth On The Horizon

The company has delivered on Vaca Muerta production growth but has seen EBITDA decline on lower margins as it was not allowed to price oil in line with global markets to help control inflation in Argentina. While the new market-friendly government is changing this, the company may find it difficult to hike the prices at the pump at the same rate as the currency devaluation and this could produce a decline in USD results in 2024. I expect YPF will be able to recuperate pricing and margins in 2025 after a rough transition year.

Performance

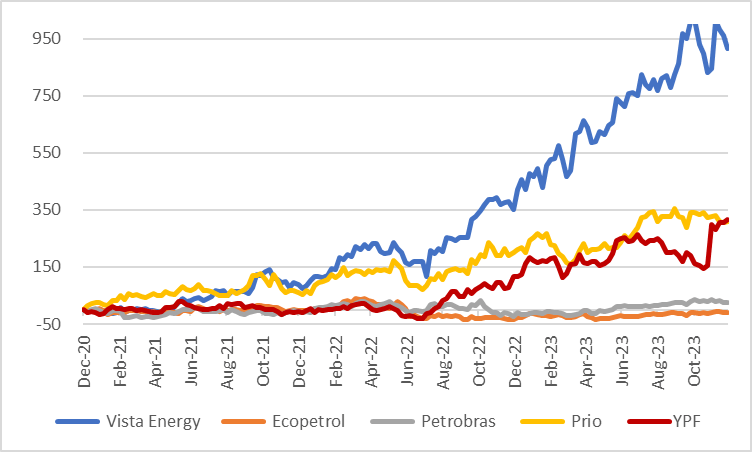

YPF is up 155% since my last article, despite the price controls and lower margins. YPF´s valuation grew as political change loomed. Similar to what occurred 8 years ago when another pro-business president took office. Vista Energy ( VIST ) is also a Vaca Muerta shale oil producer, that can export 50% of production, hence the far better performance.

{kind=link}

YPF Price Performance vs Peers (Created by author with data from Capital IQ)

The Nuances of Argentina

As an integrated oil and gas company, YPF´s price chain begins at the pump which is set in ARS (Argentinian Pesos). Thus, the companies' realized price in US$ BOE (Barrel Oil Equivalent) terms is primarily driven by local prices that are susceptible to the government's need to control inflation. At the same time, the FX (exchange rate for ARS to USD) has been set by the government (also in an attempt to control prices and inflation) and resulted in a severely overvalued currency. This is rapidly changing with the new market-oriented government.

Argentina's closed capital market, price, and FX controls created a parallel or black market (called Blue) for USDs with an exchange rate substantially higher than the official one. At the end of 3Q23, the official FX was $350 ARS for a USD and the Blue was $900.

The problem with having an artificial FX is that companies over-report USD results. YPF reports in USD, but its functional currency is the ARS and its financial statements, revenue, EBITDA, and cash flow, etc.. have been substantially overstated, since it uses the official FX, which was less than half the Blue. If the company had used the Blue FX in the 3Q23 results, EBITDA would be less than half the official rate. However, the debt is in USD and this represents another dilemma.

YPF 3Q23 Results (Created by author with data from YPF)

Devaluation Impact

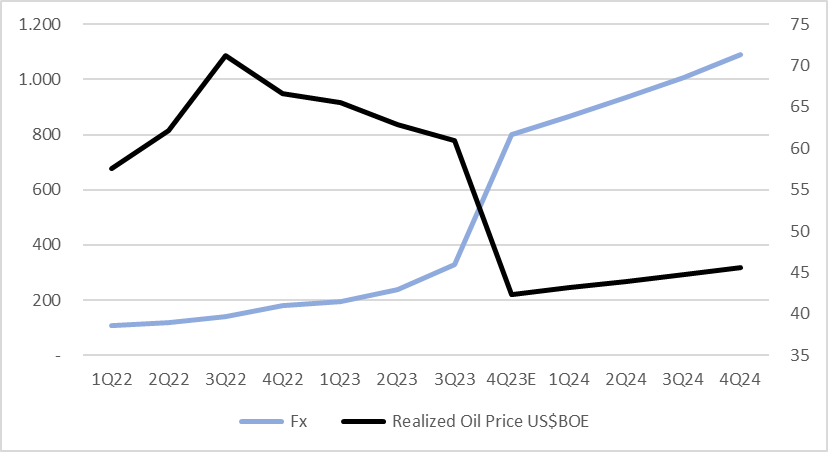

The new government has already devalued the official rate to $800 and should close the gap with the Blue in the medium term. This means that YPFs results could suffer significant declines in 4Q23 and into 2024 as financials are translated at a now far higher FX of $800.

The price charged at the pump, which drives consolidated revenue and EBITDA, needs to rise in line with the devaluation and inflation. This is going to be a problem since we are talking about an over 200% increase that will likely take most of 2024 to implement. The chart below shows my basic realized oil price assumption for YPF in this transition period.

{kind=link}

YPF Realized Oil Price vs FX ( Created by author with data from YPF)

4Q23 Should Hurt

YPF has raised prices several times in 4Q23, I calculate by 70%, but this will not be enough to offset the devaluation and EBITDA may drop 44% in USD terms. On the positive side, it is the government's hands-off approach and replacement of key executives that should provide support for the shares during the 2024 transition year.

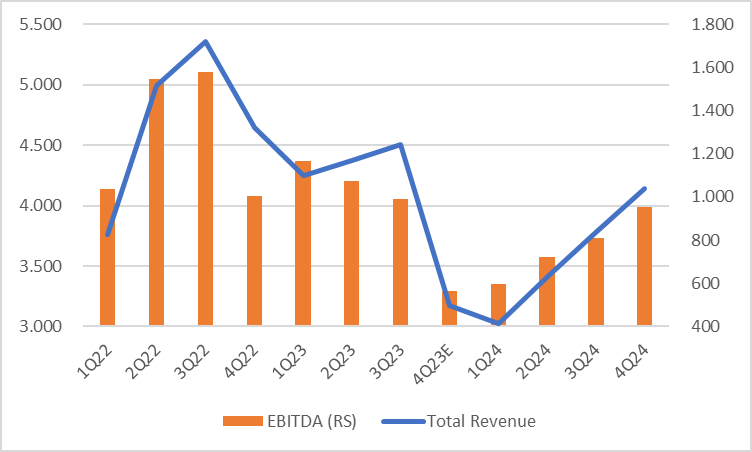

2024 Pain

With an official FX at $800 and likely to increase with inflation going forward, YPF will need to raise pump prices to “recuperate” cash flow to fund capex and pay debt, which is in USD. This means significant price increases that may lag behind the FX devaluation for the better part of 2024. I estimate YPF will see an 8% decline in EBITDA in YE24 while stressing its leverage and finding it difficult to fund capex. It may be forced to sell non-core assets, such as the electric generation subsidiary. One positive side effect of the likely decline in gasoline demand may be greater exports. Argentina is reaching an energy balance, with domestic supply meeting demand as Vaca Muerta Shale oil and gas increase production. This makes the future far brighter than the present for YPF and the Argentina oil and gas sector.

{kind=link}

YPF Revenue and EBITDA Estimates (Created by author with data from YPF)

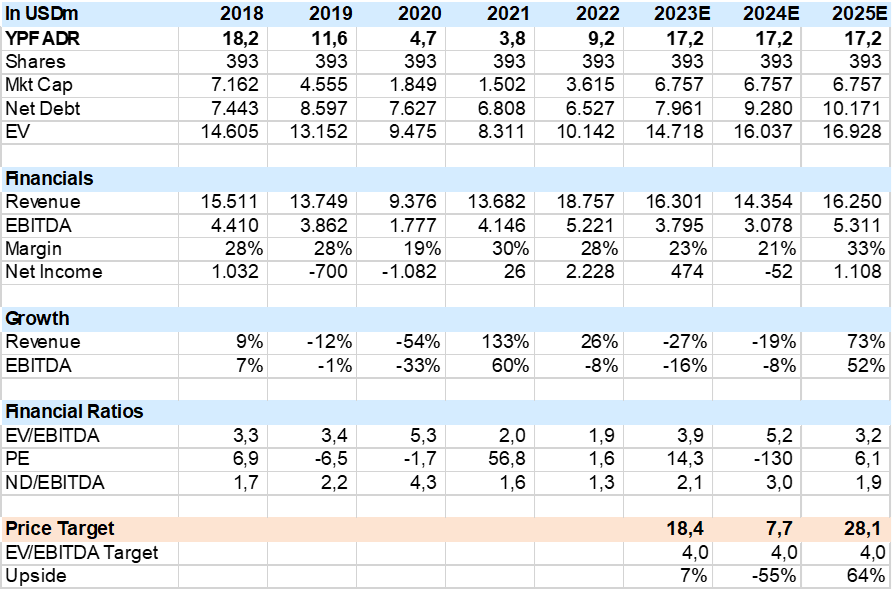

Valuation

On my estimates that assume an oil/fuel pricing lag during 2024, YPF may see a decline of 19% in revenue. Since most costs are in ARS the impact on operating margins may be lower, but the company's debt costs are in USD, and it may report a loss in 2024. At the same time, YPF has US$5bn in capex, needs to grow production and begin exporting. This funding may require additional debt, further stressing cash flow.

I assume domestic prices recuperate pre-devaluation USD oil price in 2025 which should produce a sharp recuperation in results that can support the share price during a difficult 2024. Thus, an investor should be aware that upside may be elusive in the medium term.

{kind=link}

YPF Financial Summary & Valuation (Created by author with data from YPF)

Consensus

Consensus has begun to move lower but, in my view, does not yet reflect the challenges that YPF is having to maintain revenue and margins during this devaluation. I suspect more downgrades to follow, especially post 4Q23 results.

YPF Consensus Forecast in USDm (Created by author with data from Capital IQ)

Conclusion

I am downgrading YPF from Buy to Hold, given the uncertainty in raising domestic fuel prices to offset the currency devaluation and inflation during the 2024 transition year. The result in 4Q23 may see EBITDA decline 44% and spark fear in investors. At the same time, it appears that consensus estimates do not yet incorporate this FX/Fuel price scenario which makes a downgrade more possible, and this does not support the share price.

For further details see:

YPF Sociedad: Curb Your Enthusiasm