YYY - YYY: Fund Of Funds That Fails To Deliver

2023-10-27 10:04:40 ET

Summary

- Amplify High Income ETF is structured as an exchange-traded fund and serves as a "fund of funds" in the closed-end fund space.

- YYY aims to replicate the ISE High Income Index, which selects CEFs ranked highest overall by ISE via the following factors: yield, discount to net asset value and liquidity.

- The article argues why a rules-based methodology, like the one used by YYY, might not be suitable for the CEF space, with the fund's historic performance confirming this view.

- YYY's methodology fails to take advantage of special situations and corporate actions in the CEF space, and furthermore ignores the specificities of certain asset classes which function on an IRR basis rather than yield.

Thesis

We recently wrote an article about a closed end fund acting like a 'fund of funds' via its collateral, which is composed of CEFs, BDCs and other ETFs. That name was RiverNorth Opportunities Fund, Inc. ( RIV ), and we gave our opinion on what is the best approach to the fund.

Today we are going to have a look at a similar vehicle, namely the Amplify High Income ETF ( YYY ), which is also a fund of funds. YYY however is structured as an exchange traded fund, and thus has less complexities when compared to RIV. The first one to go out the window when using an ETF is the dilemma around distributions. ETFs can only distribute what they get from their collateral pool, thus there is no discussion to be had around return of capital usage here and NAV impact of overdistribution. We like this aspect because in this instance YYY acts like a pass-through, with the management team just clipping a fee for its services.

Secondly, as an ETF, YYY does not use any leverage, thus it is a clean portfolio aggregator. In fact YYY aims to replicate the ISE High Income Index , which selects CEFs ranked highest overall by ISE via the following factors: yield, discount to net asset value and liquidity. The number of constituents that comprise the Index was changed recently from 30 to 45.

Why we do not like the ISE High Income Index Methodology

Having covered CEFs for a while now, we can say with certainty that a methodology based on yield, discount to NAV and liquidity does not really work to generate outsized results in the CEF space.

Firstly, a CEF can have a high yield for a variety of reasons, but one has to remember that CEFs can set artificially high yields. The fact that a closed end fund declares a 15% distribution yield does not equate with the vehicle actually making that in cash disbursements from its underlying assets.

Secondly there are asset classes which do not have a base 'principal' per se, but work on an IRR basis. The best known asset class here is CLO equity, which as the name suggests is the lowest portion of a CLO structure. CLO equity does not have a traditional notional because it represents the residual interest in a CLO structure, and will not return a 'principal' amount to investors at a stated maturity. Thus, from a dividend standpoint CLO equity can look great, but it should be viewed from an IRR standpoint. Unsurprisingly YYY has CLO equity CEFs as its top holdings:

Top Holdings (Fund Website)

Oxford Lane Cap Corp ( OXLC ) and Eagle Point Credit Company ( ECC ) are CLO equity CEFs, and their NAV performance looks like this:

We are not asserting these two names do not generate attractive total returns, but just pointing out that structurally they will have a high dividend yield since they are IRR based instruments.

Secondly, looking at a discount to NAV as a factor is also not necessarily correct. Underperforming funds, or funds from fund families which are viewed poorly can have very high discounts to net asset value. These discounts are not going to close out if the underlying factor is not extinguished. Point in case with the consolidation going on in the CEF space which we have covered in the past, where fund families which were trading for years at large discounts to NAV were forced to sell (Delaware fund family for example).

There is also a correlation beta with underlying risk factors for discounts to NAV. For example a high yield CEF will tend to exhibit a higher discount to NAV during a recession when credit spreads are wide. The signal here is correct, because buying at these levels is going to work. Some asset classes though completely fall out of favor at times, and a high discount to NAV can just get wider. Point in case is the MLP CEF subsector, which saw a complete repricing in 2020, and is still trading at very wide levels to NAV.

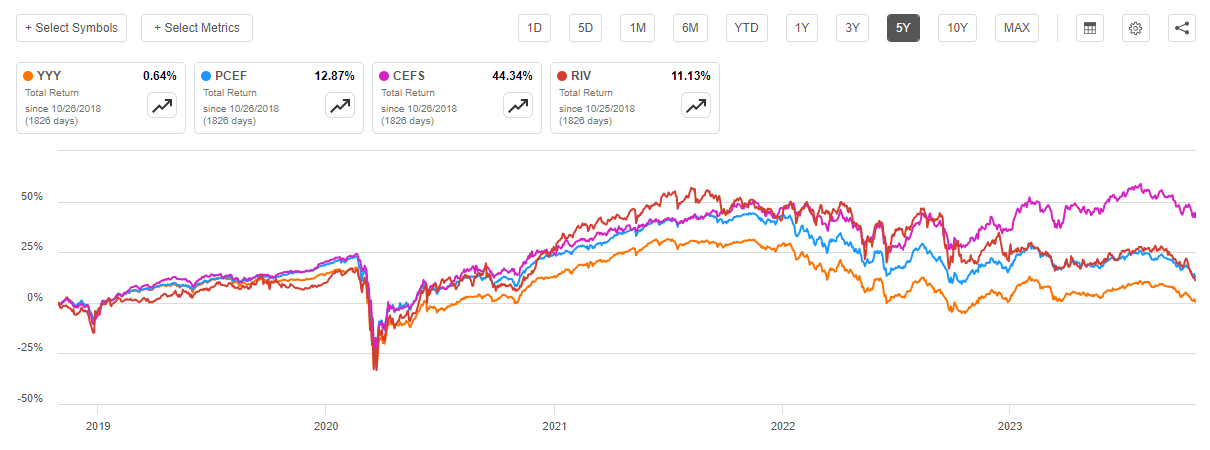

How has YYY performed? Not that great is the answer

In the above section we described the reasons for which we did not view very favorably the way YYY is built. Its historic performance when compared to similar funds confirms that view:

{kind=link}

On a 5-year lookback period, YYY is the clear underperformer on a total return basis. In fact, YYY has failed to generate any return for said period, being flat. Moreover, it has always been the lagging fund in terms of total return in the respective time span. It did not have periods of outperformance versus the cohort. Just always lagging.

Why an index methodology is not the appropriate one for the CEF space

We do not believe setting up a rules based methodology works in the space. The best example is the PIMCO Energy & Tactical Credit Opportunities ( NRGX ) CEF which we covered with a 'Strong Buy' here and is up over 7% since while the overall market has tanked:

NRGX Rating (Author)

The reason for our rating was a change in mandate, and the fact that PIMCO credit funds have historically traded flat to NAV or at a premium to NAV. We also looked at the holders of the vehicle and made an assumption regarding the reasons for the corporate action. None of these metrics would show up in the screening process that YYY does.

However, the best in breed in the space, namely Saba moved to purchase NRGX:

On September 29, 2023, Saba Capital Management, L.P. a New York-based investment firm, added 6,887,083 shares of PIMCO Energy & Tactical Credit Opportunities (NYSE:NRGX) to its portfolio. This article provides an in-depth analysis of the transaction, the profiles of both the guru and the traded company, and the potential implications of this acquisition.

Source: Yahoo Finance

We would like to think they read our article, but in fact Saba has done very well in the space, with their CEFS ETF a leader from a total return perspective. They are doing what needs to be done here, and that is active management. Understanding a corporate action, judging it and making a decision is the appropriate way to trade the CEF space outside the underlying risk factors.

If a CEF is an equity one from a good manager, it will have the underlying equity risk factor as its main driver, and little else to offer in terms of opportunities. Special situations or corporate actions need to be judged actively by a person. YYY does not do that, and its returns will always lag in the space in our view.

Conclusion

YYY is an exchange traded fund. The vehicle acts as an aggregator, or a 'fund of funds'. YYY aims to replicate the ISE High Income Index, which selects CEFs based on yield, discount to net asset value and liquidity.

The article presents the reasons for which we do not think the ISE methodology will produce robust long term results, and YYY's historic performance agrees with our view. YYY is flat on a 5-year basis and has always trailed its peers. YYY will never be able to correctly capture special situations or corporate actions in the CEF space, and a 'blind' yield methodology that does not take into account the asset class is set to produce mediocre results.

We are of the opinion that a retail investor looking for a fund of funds should sell out of YYY and consider CEFS or RIV instead.

For further details see:

YYY: Fund Of Funds That Fails To Deliver