RVLV - Zalando: A Top Pick In A Struggling Industry

2023-12-20 04:13:58 ET

Summary

- Investors have never been more pessimistic about Zalando's prospects, indicated by a near all-time low P/S ratio.

- The company is a market leader with approximately 12% of the European market share, benefiting from economies of scale.

- Zalando's dominant position in the market enables it to function as a comprehensive one-stop shop, offering a unified inventory pool for international companies seeking to enter the European market.

- The current sharp decline in Zalando and similar online fashion retailers is seen as temporary, with the potential to strengthen Zalando's future profit generation.

- Zalando's healthy financial position and continuous investment increase the potential to gain market share from struggling competitors in Europe.

The market currently values online fashion companies at significantly depressed levels. The challenges confronting the British online fashion retail companies ASOS ( ASOMY ) and boohoo ( BHOOY ), the American high-fashion brand Revolve ( RVLV ), and European market leader Zalando ( ZLNDY ) are substantial and undeniable. Nevertheless, my research indicates that the market's selloff is overly aggressive, presenting astute investors with an exceptional opportunity to capitalize on select online fashion retail companies.

In the current difficult climate, most companies are prioritizing profitability and cash flow at the expense of their revenue growth and market share. However, there are exceptions. The German e-commerce success story, Zalando, appears uniquely positioned to achieve both — effectively having its cake and eating it too.

Investment Thesis

Zalando is trading at a historically cheap valuation, around 79% away from its 2021 peak and 55% below its pre-pandemic levels. Investors are more pessimistic than ever about the German online fashion retailer as evidenced by the all-time-low PS (Price-to-Sales) multiple.

With a solid balance sheet to weather the storm, cash-flow positive on a trailing 12-month basis, a leading market share in Europe with 50 million active users across 25 countries, and a decisive focus on serving and elevating its partners through its ecosystem and beyond, Zalando is one of the most appealing buy-and-hold growth stories in Europe at the moment.

By utilizing a fundamental FCFE valuation and relatively conservative estimates (Vs. analyst expectations), I demonstrate that the stock exhibits a 280% upside potential. The thesis is further solidified by a comparative employee review with industry peers and a company ownership structure breakdown.

From a top-down perspective, the online fashion retail market has far from peaked, with promising growth lying ahead for companies that solidify their market share.

The Appeal

A Historically Low Valuation

Zalando shareholders have endured a roller coaster ride over the last years witnessing substantial gains during the COVID-19 stay-at-home mandates, followed by a precipitous drop—around 55% from their pre-pandemic levels and a maximum drawdown of 81% . Zalando hasn't seen such valuations in around four years (2019), apart from a brief, all-time-low drawdown in 2022.

Zalando Market Capitalization in USD Over The Last 10 Years (YCharts)

Caught In An Industry-Wide Downfall

Zalando's British fast-fashion competitors ASOS, Boohoo, and the American premium-offering Revolve are currently trading market capitalizations not seen since 2010, 2016, and 2020 respectively. Online fashion retail companies have underperformed significantly, even against the consumer discretionary sector.

Zalando Market Capitalization in USD Over The Last 10 Years (YCharts) S&P 500 Vs S&P Consumer Discretionary Vs ASOS Vs Boohoo Vs Revolve Vs Zalando, from 01/2020 to 11/2023 (YCharts)

Investors Have Never Been More Pessimistic

From the Price-to-Sales perspective, it's apparent that the market's outlook on online fashion companies is deeply pessimistic, with these stocks trading at, or near, all-time-low multiples.

Price-to-Sales Ratio Over Time: ASOS, Boohoo, Revolve, Zalando (YCharts)

Such a significant downturn usually follows from excessively high valuations, a significant and permanent setback in profit generation, or are on the brink of bankruptcy. However, Zalando has clearly demonstrated its ability to manage tough environments deliver on its promises and continuously invest in its growth.

The Online Fashion Industry Downfall

In a nutshell, this downturn is attributable to a confluence of factors including:

- Skyrocketing costs (freight, labour, outbound delivery costs, etc.) due to supply chain disruptions

- Stronger-than-expected return to physical stores

- Waning consumer demand due to the cost-of-living crisis

- A steep increase in cost-of-borrowing due to aggressive rate hikes

The bigger picture starts with the e-commerce demand surge during the stay-at-home mandates over 2020 and 2021. The first half of 2022 was pivotal in assessing the sustainability of e-commerce growth as economies reopened. However, e-commerce demand was weaker than expected, evidenced by a notable shift of customers back to in-store shopping and weak e-commerce revenue.

Simultaneously, online fashion retailers who were anticipating a continuation of the high demand experienced in 2021, faced over-stocked inventories. This, coupled with weaker demand, and rising inflation resulted in a significant supply-demand imbalance. Their already low-profit margins were further squeezed as online fashion retailers were compelled to clear their excess inventory through deep discounts.

Comparative Performance

Comparative Financial Performance

The figure below illustrates that the majority of the decline in market valuations since early 2020 can be attributed to a decline in profitability (Earnings Per Share, EPS) and a shift in investor sentiment (Price-to-Sales Ratio, P/S).

YCharts

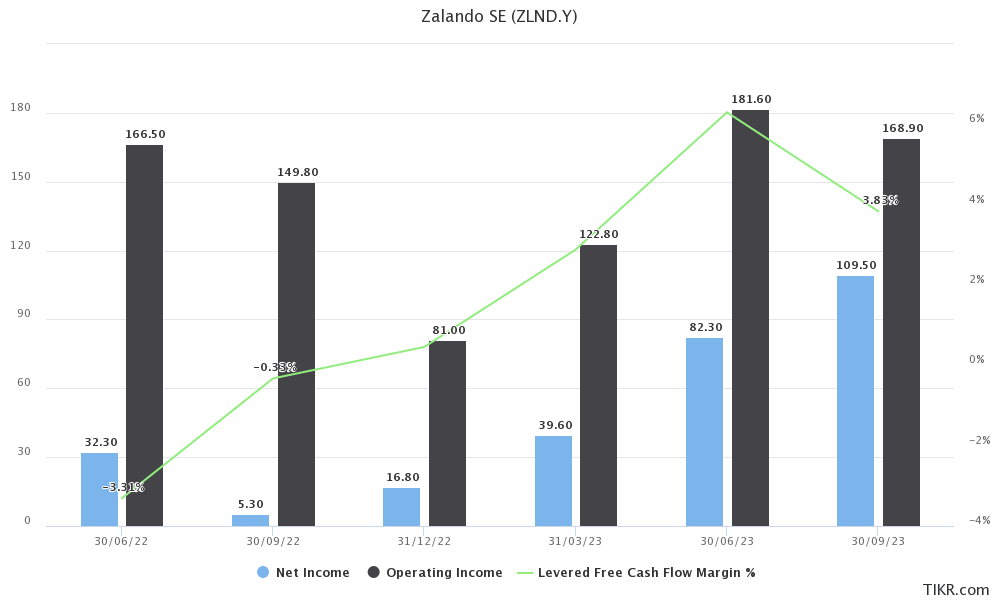

Among these companies, Zalando is the only one to have bounced back from the late 2022 lows with a positive trajectory going forward. Zooming into the company's Net Income, Operating Income, and Free Cash Flow Margin during that time it is apparent that Zalando managed the downturn exceptionally well.

Zalando's Profitability And Cash Generation Over The Last 18 Months (TIKR.com)

{kind=link}

Revolve, with its higher-margin, premium offerings, has managed to maintain profitability in an exceptionally challenging environment for the online fashion retail industry. This is evidenced by the fact that 85% of their net sales in FY22 were sold at full price. In contrast, ASOS and Boohoo resorted to steep discounts to clear their overstocked inventories as well as the closure of distribution centres to manage costs.

GPM, EBIT Margin and Profit Margin Graphs for ASOS, Boohoo, Revolve and Zalando (YCharts)

Zalando, although it exhibits the lowest Gross Profit Margin among the group, is the only one to show an upward trajectory in EBIT margin and resilient Profit Margin over the past five years, possibly due to economies of scale.

Overall, the American company Revolve and the German firm Zalando have navigated the post-pandemic environment more successfully. Revolve benefited from the premium offering market's resilience while Zalando's story is centered around execution and continued investment in growth. Their British counterparts, ASOS and Boohoo, have seen their profitability peak in 2021 and turned negative thereafter, a trend reflected in their stock prices.

It is worth noting that, when the online fashion retail market recovers I would expect Revolve to experience less growth than its counterparts due to its premium offering market not being hit particularly hard during the cost-of-living crisis.

Table 1: Summary of the companies' latest results, guidance, and key metrics. Data is fetched through the companies' latest statements or through SimplyWallSt and TIKR. Figures in millions except if specified otherwise. YoY change in parenthesis.

| Latest Financial Results |

| ASOS, FY23 |

| Boohoo, 1H24 TTM |

| Revolve, 3Q23 TTM |

| Zalando, 3Q23 TTM |

| Revenue |

| £3,538 (-11%) |

| £1,615 (-15%) |

| $1,070 (-1%) |

| €10,254.9 (-0.2%) |

| Gross Margin |

| 44% (+60 bps) |

| 51% (+20 bps) |

| 51.7% (-290 bps) |

| 38.4% (-210 bps) |

| Operating Margin |

| -0.8% (-190 bps) |

| -3% (-250 bps) |

| 3.6% (-590 bps) |

| 1.6% (+10 bps) |

| Current Ratio |

| 1.7 |

| 1.5 |

| 2.8 |

| 1.5 |

| Debt-to-Equity |

| 77.6% |

| 85.6% |

| 0.0% |

| 40.7% |

| Active Customers |

| 23.3 (-9%) |

| 17.0 (-12%) |

| 2.5 (+12%) |

| 50.1 (-0.2%) |

| Revenue Guidance |

| -5% to 15% (FY24) |

| -12% to -17% (FY24) |

| -4% (FY23) |

| -1.4% (FY23) |

Comparative Financial Position

As online fashion retail companies emerge through the toughest macroeconomic environment they have encountered in years, examining their Balance Sheets to assess their liquidity is crucial.

Table 2: Financial health data fetched from SimplyWallSt and TIKR

| Debt-to-Equity Ratio |

| Debt (millions) |

| Cash (millions) |

| Total Assets (millions) |

| Total Liabilities (millions) |

| Equity (millions) |

| ASOS |

| 77.6% |

| £673 ($838) |

| £353 ($440) |

| £2,630 ($3,276) |

| £1,760 ($2,192) |

| £867 ($1080) |

| Boohoo |

| 85.6% |

| £325 ($394) |

| £290 ($352) |

| £1,180 ($1,431) |

| £802 ($973) |

| £380 ($461) |

| Revolve |

| 0% |

| $0 |

| $266 |

| $630 |

| $233 |

| $397 |

| Zalando |

| 40.7% |

| €938 ($907) |

| €1,902 ($2,011) |

| €7,379 ($7,801) |

| €5,091 ($5,382) |

| €2,289 ($2,419) |

Due to the total liabilities, Zalando's balance sheet appears less strong than it actually is. With $1,104 million in net cash and an FCF (Free Cash Flow) of €553.7 million, Zalando's use of debt does not seem problematic at all.

On the other hand, ASOS's and Boohoo's financial situation appears concerning. ASOS was forced to raise capital through an equity and debt offering in 2023 at a significantly low valuation, diluting its already beaten shareholders. While Boohoo carries a considerable amount of debt, its cash flow-positive status mitigates immediate concerns.

Revolve sits at a notably healthy financial position with zero debt and $266 million in cash.

Understanding Zalando

Zalando is active in a variety of business fields - from multi-brand online shopping (including their brands), the shopping club Lounge by Zalando, outlets, as well as logistics and marketing offers for retailers.

Zalando's strategy revolves around a 3-part proposition:

- Create deep customer relationships at scale

- Transition into a true platform business for Partners

- Sustainability

In this section, I will discuss further number two, i.e. Zalando's partner ecosystem, which I believe is the key differentiator from its peer companies.

Partner Proposition

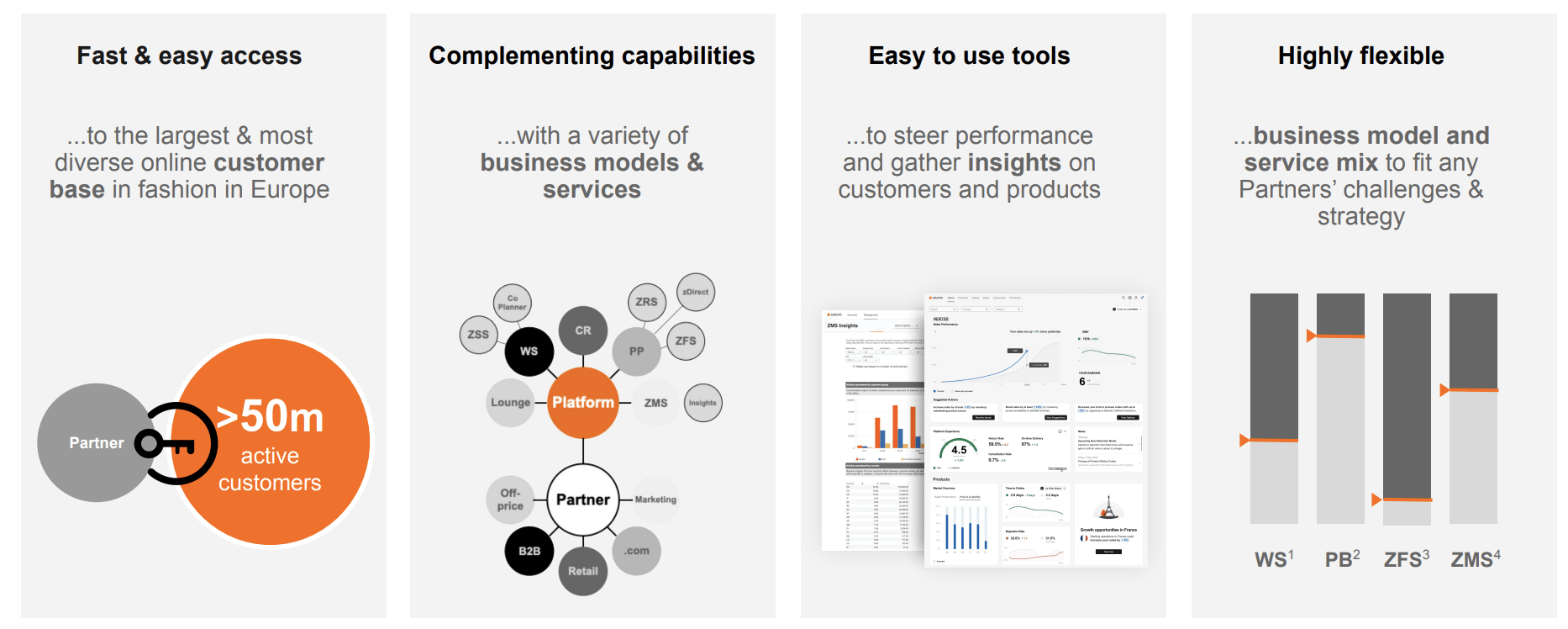

Unlike most of its peers, Zalando is not a pure B2C online fashion retailer, but also a B2B all-around logistics, marketing, and digital shopping platform connecting sellers to European consumers.

Zalando Partner Solutions ( Zalando, FY22 )

Over the last years, the company has leveraged its 50 million active user base across 25 European markets, its high market penetration, and comprehensive logistics and marketing solutions to connect fashion brands' inventory with European digital consumers essentially incorporating B2B services in their business model.

Every quarter, Zalando is a stronger and more appealing platform for brands that want to access the European market with a single inventory pool and reliable logistics through its ZFS offering (Zalando Fulfillment Solutions), evidenced by the 900 brands that used the during 2022 to ship 120m items and most recently of Partners signing up for the ZFS, up +6pp to 39% fueled by a record-high number adoption of Zalando Fulfillment Solutions up +4pp to 64% in 3Q23 .

Complementing the fulfilment solutions, Zalando offers marketing solutions to its partners through ZMS (Zalando Marketing Services) making Zalando a one-stop shop for companies that want to access the European market.

{kind=link}

The company does not limit its B2B services to partner companies selling on the Zalando platform. Companies can benefit from Zalando's extensive logistics, distribution, and marketing services while selling directly to consumers.

Sources Of Revenue

Zalando's business relies on three revenue sources:

- Fashion Store (81.5% of Revenue)

- Offprice (14.9% of Revenue)

- Other Segments (3.6% of Revenue)

The Fashion Store segment offers a wide range of fashion products from various brands and private labels. It operates in two regions: DACH (Germany, Austria, and Switzerland) and the Rest of Europe. It includes the ZFS (Zalando Fulfillment Solutions) revenues.

The Offprice segment sells discounted fashion items through the Zalando Lounge and Zalando Outlet channels.

All Other Segments include Highsnobiety , a media and commerce platform for streetwear and luxury fashion, and other services such as Zalando Marketing Services and Zalando Gift Cards .

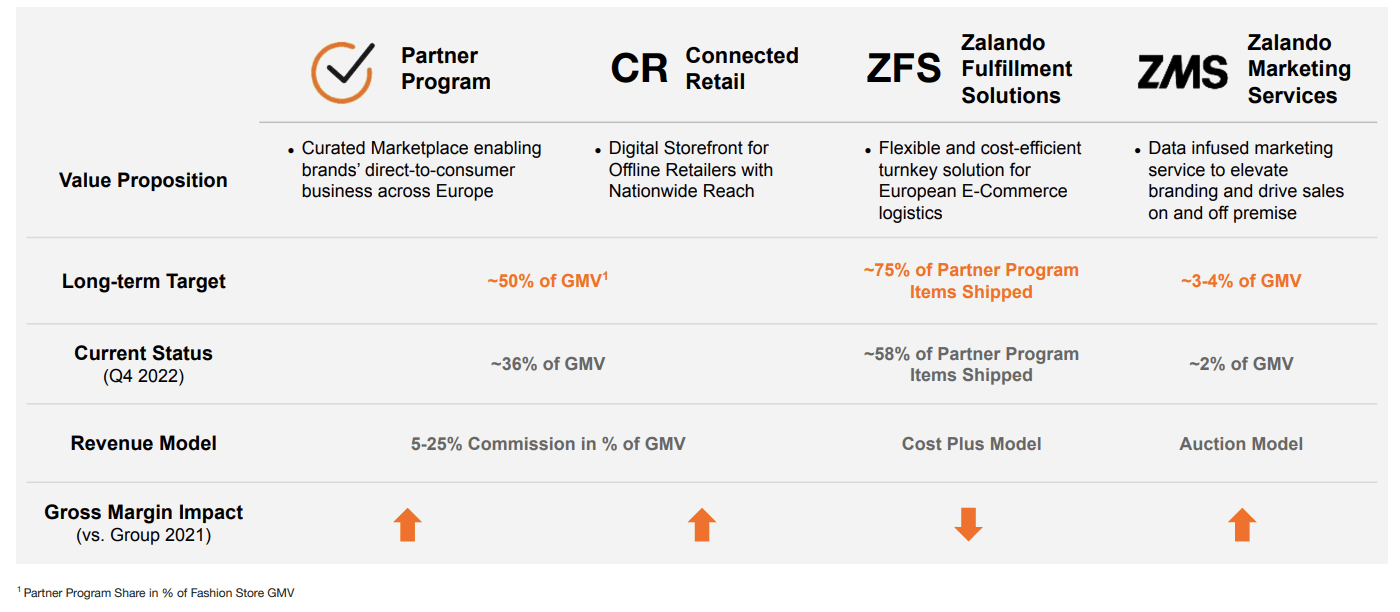

The following table from Zalando's investor presentation in December 2023 shows how the company earns revenue from Partner-related solutions.

{kind=link}

Zalando has set a long-term goal at the group level to achieve an adjusted EBIT margin between 10% and 13% . This target is a combination of expected margins from different business segments: a 6% to 8% margin in the wholesale business and a higher margin of 20% to 25% in the Partner Business, which includes associated services like Zalando Fulfillment Solutions and Zalando Marketing Services.

A Top Pick For 2024 And Beyond

As consumer sentiment strengthens, driven by a reversion of inflation rates to equilibrium and an easing of monetary policy, Zalando, with its hybrid B2B and B2C model, is well-positioned to gain substantially. This advantage comes from an anticipated increase in consumer demand and the inevitable demand from fashion brands for market access in Europe.

Moreover, Zalando's potential extends beyond serving clothing, footwear, and accessory brands on its digital platform. Its openness to a diverse range of retailers and companies that sell directly to consumers positions it to benefit significantly more than traditional online fashion retailers.

However, investors should be mindful of the key assumptions underlying this thesis:

Firstly, the market is currently expecting four to five 25 basis point cuts by the Federal Reserve in 2024, which would facilitate easier access to capital. Should inflation surge again, additional rate hikes may be implemented by the Federal Reserve, further constraining consumer and investor spending—a scenario that would likely be unfavourable for consumer discretionary companies like Zalando.

Secondly, the market is currently betting on a soft landing, which implies a cyclical slowdown in economic growth that avoids a recession. If a significant recession were to occur, consumer and corporate strength would likely be weaker than assumed in the initial part of this analysis, potentially delaying the anticipated recovery in demand.

A Qualitative Look

Company Ownership Structure And Management

{kind=link}

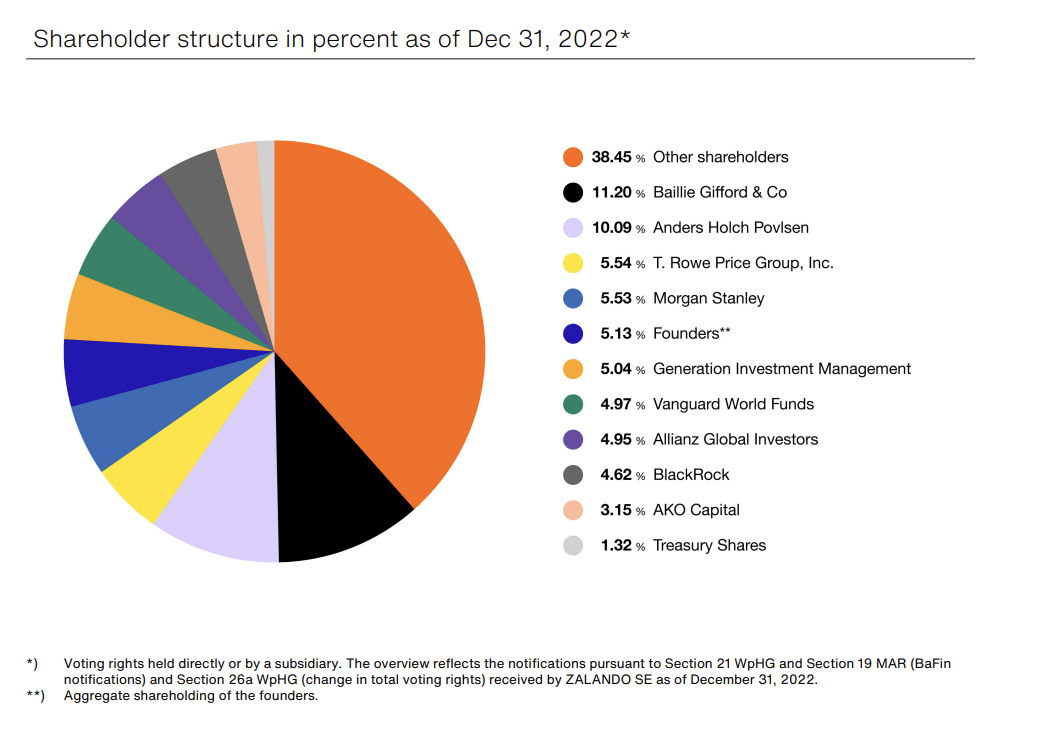

One of the most compelling aspects of Zalando is its management, led by the two co-founders, Robert Gentz and David Schneider. It's evident that Zalando's rise as a European e-commerce success story is not mere chance. Having a proven, competent, and founder-led management team is a crucial component in the formula for a successful and enduring company.

As of FY22, the two co-founders and co-CEOs hold any part of the 5.13% of their company. Simultaneously, the co-CEOs receive a modest fixed salary of $85,460 and are primarily compensated through stock-based compensation. This approach is designed to align management's incentives with the company's success, though it could potentially lead to the dilution of shareholder value. A further 10.09% is held by Anders Povlsen, a board member of the company.

Comparative Employee Reviews

Investors often utilize platforms like Glassdoor to gauge employee sentiment within companies, which can reveal potential issues or advantages not apparent externally. However, it’s important to note that the companies might influence these metrics to present a more favourable image.

Table 3: Employee company reviews fetched from Glassdoor.com

| Company |

| Overall Score |

| Recommend to a Friend |

| Approve CEO |

| Frequently Reported Pros |

| Frequently Reported Cons |

| ASOS |

| 3.5/5 |

| 57% |

| 69% |

|

|

| Boohoo |

| 3.2/5 |

| 52% |

| 54% |

|

|

| Revolve |

| 2.8/5 |

| 41% |

| 60% |

|

|

| Zalando |

| 3.6/5 |

| 69% |

| 69% |

|

|

Among the four, Zalando is viewed more favourably by its employees, evident from its fairly high CEO approval rating and "Recommend to a friend" statistic. In contrast, Boohoo CEO John Lyttle is the least favoured. Revolve seems to be the company with the most dissatisfied employees. Common concerns across all companies include low salaries, poor work-life balance, and inadequate management.

A Top-Down Perspective

The Current State Of Online Fashion Retail

Online fashion companies are currently clearing their overstocked inventories through significant discounts, a consequence of the demand surge during COVID-19. This situation is compounded by high (albeit decreasing) costs and reduced consumer spending on clothing and footwear.

The post-COVID-19 era has exposed the inelastic nature of the online fashion business model, with companies struggling to maintain cash flow and profitability. As a result, there's a marked shift in strategy: moving away from the high-volume/high-growth approach, characterized by generous discounts and free return policies, towards a model focused on targeted, profitable growth and cautious expansion.

Temporarily Unfavourable Macro Trends and Business Economics

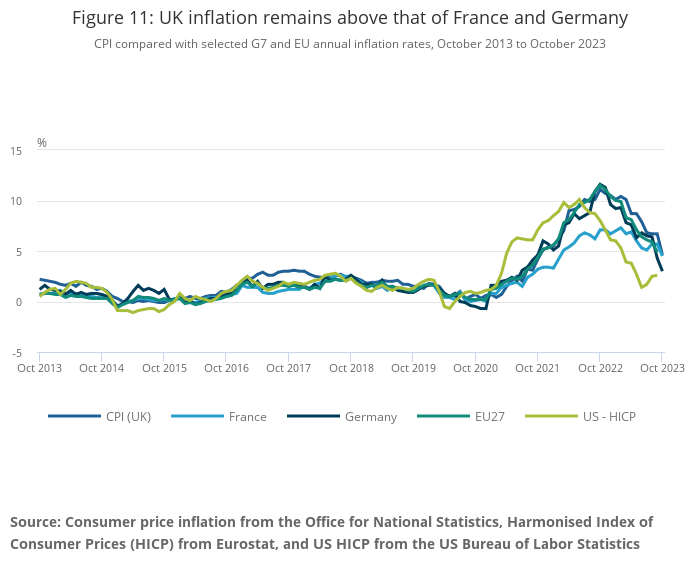

Following the COVID-19 reopening, the UK—ASOS and Boohoo's primary market—experienced persistently high inflation, more so than the US (home to Revolve) and Germany (Zalando's base).

CPI of G7 countries annual inflation rates, August 2013 to August 2023 (Home - Office for National Statistics)

{kind=link}

In February 2022, during the reopening phase, the Clothing and Footwear segment recorded a low contribution to inflation at -0.46% . This indicates that despite soaring costs in sourcing and distribution, prices paid by customers for clothing and footwear remained relatively stable or even decreased, adversely impacting the profit margins and bottom lines of online retailers.

Home - Office for National Statistics

On the other hand, the inflation rate for Clothing and Footwear rebounded during 2022 and 2023, standing at 0.43% in the latest report from August 2023.

Assessing The Future of Online Fashion

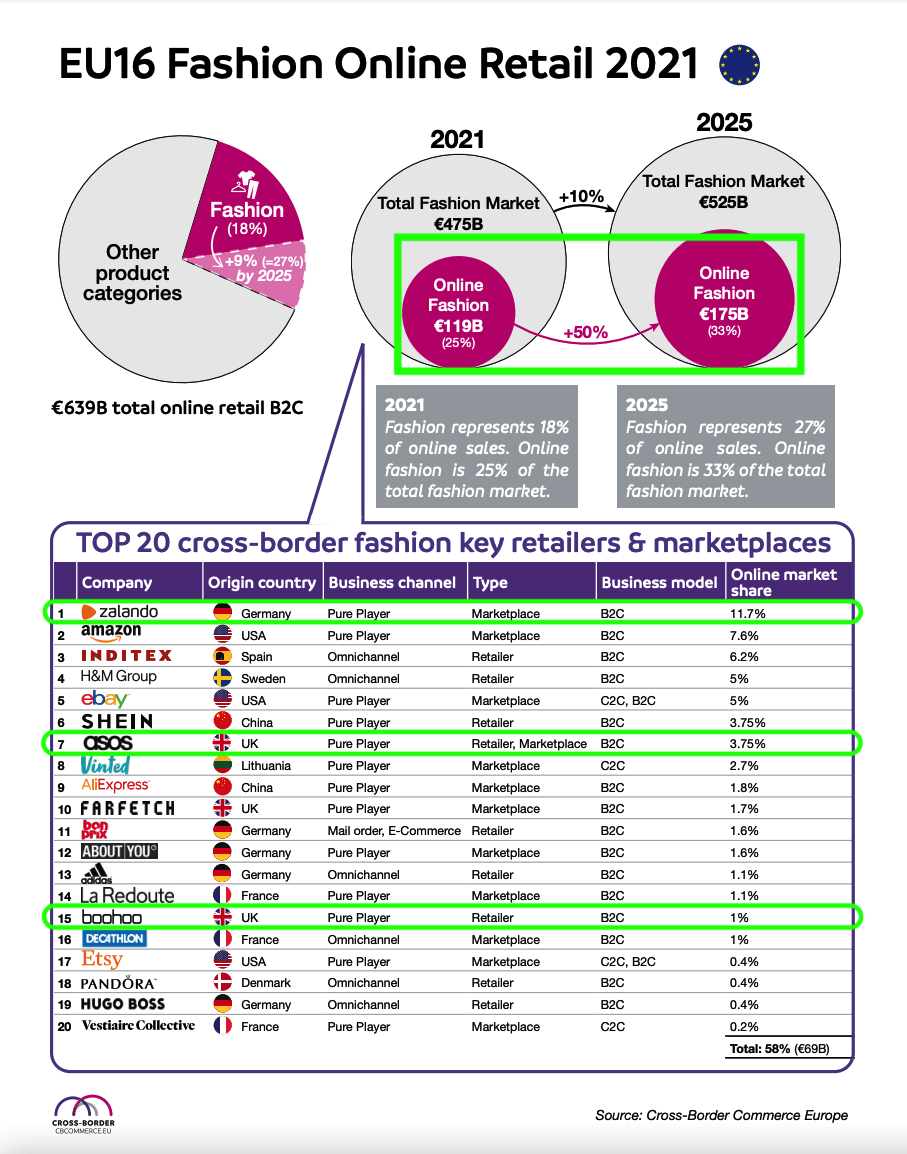

Recent studies present an optimistic outlook for the online fashion industry. According to a study by Cross-Border Commerce Europe, the online fashion sector is expected to experience significant growth in the coming years, capturing a larger market share of the total fashion industry. In this burgeoning landscape, Zalando leads the way in Europe, with ASOS and Boohoo ranking in the top 7 and top 15, respectively.

Fashion Online Retail 2021 In Europe ( Cross-Border Commerce Europe | EU Retail Network/Accelerator )

{kind=link}

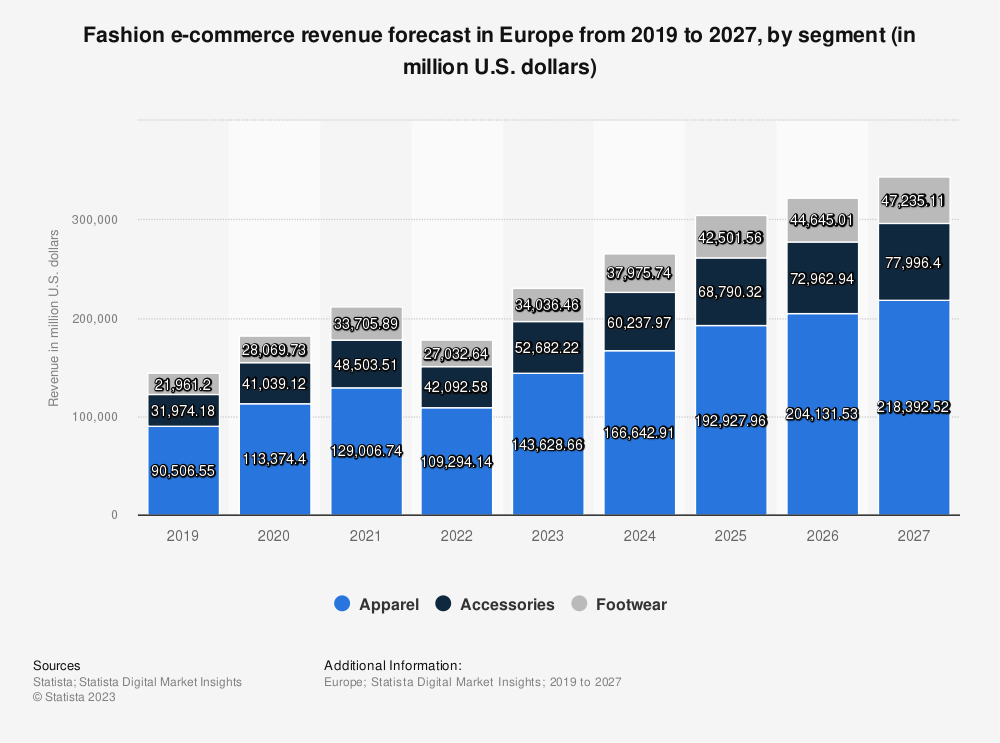

Complementing this, Statista's research highlights a contraction in fashion e-commerce revenue in Europe during 2022 but predicts a notable resurgence in the medium term.

{kind=link}

While there are discrepancies in the historical data reported by these two sources, likely due to varying methodologies in measuring industry revenues and differences in their publication times (such as the companies and countries included), the general consensus is similar. Both sources project growth estimates that are in the same ballpark, indicating a broadly aligned, optimistic view of the industry’s future trajectory.

Risks

Systemic Risks

Systemic risks impact companies broadly or within specific industries, such as online fashion retail. While not directly stemming from Zalando's operations, it's crucial for investors to be cognizant of systemic risks that surround the company.

Business Model Shift for Improved Margins: For heightened profitability, a shift in business models is critical. This involves more effective inventory management, reducing discounted sales, and concentrating on profitable customers, thereby mitigating the influence of unprofitable ones.

Macroeconomic Challenges: Although there's been a swifter-than-anticipated reduction in inflation, it remains a concern in the US, Germany, and the UK. The swift pace of interest rate hikes presents another challenge, with its full impact still unfolding. A recession or resurgence in inflation could adversely affect consumer demand, Zalando's partner companies, and investors.

Sensitivity to Economic Cycles: As a consumer discretionary entity, Zalando is expected to be particularly susceptible to economic fluctuations. With a 'soft landing' anticipated in 2024, the market's current optimism may be overly positive.

Idiosyncratic Risks

Company Ownership Structure: The absence of equity ownership by the two co-CEOs is concerning. Given their status as co-founders, one would expect them to hold some equity in the company if they are confident in its direction.

Targeted By European Legislation: Recently, Zalando, alongside Meta ( META ) and Google ( GOOG ), has been placed on a scrutiny list, classified as a "Very Large Online Platform" due to its user base exceeding 45 million. Strict European regulations could hinder Zalando's progress as a leader in European fashion e-commerce.

Market Share Vs Profitability: The primary determinant of Zalando's market value is its ability to generate cash through its dominant position in the European market. If Zalando must continually operate with low margins to maintain or increase market share, investors might only see linear share appreciation relative to the company's Gross Merchandise Volume ((GMV)).

Share Dilution: Zalando's stock has experienced a cumulative 5-year share dilution of 4.7% due to Stock-Based Compensation ((SBC)). A continuation or increase in stock dilution in the upcoming year could potentially erode returns from the stock.

Fundamental Stock Valuation

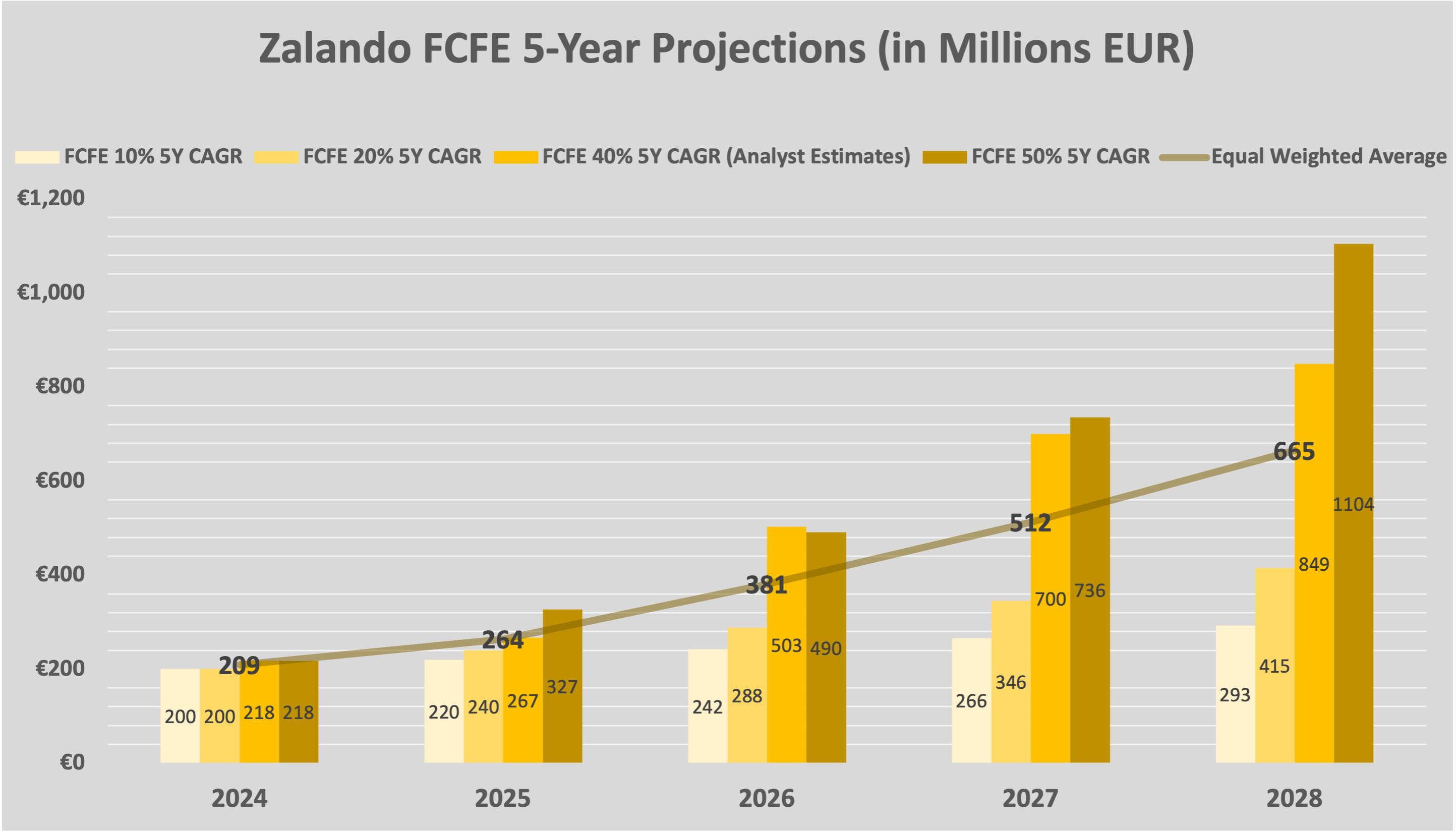

The stock valuation methodology is centred around analyst expectations, which see the FCFE (Free-Cash-Flow to Equity) grow at an impressive 40% average CAGR over the next 5 years. The valuation was balanced by equally weighting a bearish 10% and 20% average CAGR and a bullish 50% CAGR. The weighted average projection is conservative compared to analyst expectations as seen by the weighted average line below.

Zalando 5Y FCFE Valuation (Author's Representation)

{kind=link}

Using a 5-Year Average German Government Bond Rate of 2.5% , an ERP (Equity Risk Premium) of 5% , and a Specialty Retail Unlevered Beta of 0.97, I concluded at a discount rate of 8.25%.

Based on the FCFE and discount rate figures given above and a 4% perpetual growth rate after 2028, I concluded a fair market value for Zalando of around €22.8 billion or €88 per share, equivalent to $24.9 billion or $48 per share for the ZLNDY stock, about 280% upside from the current prices.

For reference, the current Market Cap of $5.8 billion assumes Zalando grows its FCF at a modest 10% average CAGR for the next 5 years with a discount rate of 8.25%.

Zalando Stock Correlation

From a portfolio management point-of-view, Zalando's attractiveness is neutral, neither particularly appealing nor unappealing. The 3-year correlation seems to have a moderate connection with the S&P 500.

3-Year Daily Pearson Correlation Of Online Fashion Retail Companies (Author)

Summary

I contend that the sharp decline in Zalando and other online fashion retail companies, while understandable, is likely to be temporary. Specifically for Zalando, this downturn could paradoxically strengthen its prospects for future profit generation. To summarize, the key factors driving this sharp decline are:

- Deteriorating Margins: Triggered by supply chain disruptions and cost inflation.

- Waning Consumer Demand: Stemming from the cost-of-living crisis and an unexpectedly robust return to brick-and-mortar stores post-COVID.

- Expensive Borrowing Rates: Resulting from significant interest rate hikes and falling share prices.

Despite these challenges, Zalando stands out as an especially appealing investment opportunity due to several factors:

-

Valuation Metrics: Currently, the company's price-to-sales (P/S) ratio and market capitalization are near all-time lows, indicating a high level of market pessimism about Zalando and the online fashion retail sector in general.

-

Solid Financial Position: Zalando has a healthy positive Free Cash Flow ((FCF)), positioning it well to capitalize on industry-wide weaknesses and expand its market share.

-

Market Leadership: Holding approximately 12% of the European market share, Zalando benefits significantly from economies of scale, a critical factor in e-commerce success.

-

Strong Partner Value Proposition: Zalando's commitment to adding value for partner brands sets it up for dual benefits: from its established dominance in customer service and its rapidly expanding B2B segment.

-

Proven And Aligned Management: The founder-led, co-CEO management team at Zalando holding a 5% stake, has a track record of successful navigation through past challenges, positioning the company well for future online fashion trends.

-

Innovation and Adaptability: The company's innovative approaches, such as the Shopping Club, demonstrate its ability to navigate difficult periods by clearing excess inventory while enhancing customer engagement.

Contrary to many online fashion retailers that primarily focus on customer service, Zalando also addresses the needs and aligns with the interests of clothing brands. This dual focus makes Zalando a comprehensive one-stop shop in Europe, benefiting from a unified inventory pool.

Bottom Line

The German market leader Zalando appears to be an exceptionally attractive investment opportunity at its current market valuation. This assessment is supported by the FCFE valuation, which suggests a 280% upside potential. A Glassdoor employee review study indicates that Zalando's employees are relatively satisfied compared to their peers. Individual insiders hold 15% of the company's shares, creating an alignment between management's interests and those of the investors. However, this alignment is somewhat counterbalanced by the dilutive effect of their stock-based compensation packages.

Zalando's strategy to offer an all-encompassing gateway into the European market for international retail brands through its digital marketplace—and for companies serving their customers directly—positions it well for a strong performance once market conditions improve in its favour.

The company's consistent investment in growth positions it to potentially increase its market share in Europe, especially as smaller online retailers face challenges. Economies of scale, a seasoned co-founder-led management team, and a proven ability to perform in tough times are key ingredients for exceptional returns.

Considering the factors discussed in this article, I am initiating a 'Strong Buy' rating for Zalando at the current price levels.

Readers need to know that, following my own analysis and advice, I have recently added Zalando stock to my investment portfolio with all the inherent biases this might be accompanied by.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Zalando: A Top Pick In A Struggling Industry