ZETA - Zeta Global Holdings: A Look At If It Can Maintain Momentum

2023-03-25 04:32:29 ET

Summary

- I see the company underestimating the impact of the macroeconomic conditions that will likely slow down its growth trajectory.

- Most of its growth metrics look solid, but it needs to be taken into consideration that a number of them are measured against a low baseline.

- If the company can execute, it has potentially lucrative long-term growth potential, but it still must cut costs a lot more before it turns a profit.

Since its 2021 IPO, Zeta Global Holdings Corp. ( ZETA ) has been trading very volatile. It predictably dropped not long after going public, falling from approximately $8.50 per share on June 28, 2021, to about $5.30 per share on August 9, 2021.

From there it began a nice run, soaring to its all-time high of $13.46 on April 4, 2022, before falling off the cliff from there, plunging to its all-time and 52-week low of $4.09 on July 4, 2022.

After that it has started a steady upward climb to around $11.25 on February 27, 2023, and dropping to under $10.00 per share in mid-March 2023. As I write it's trading at $10.20 per share.

ZETA has enjoyed some consistent momentum recently, and recent guidance from management for full year 2023, suggests that momentum could continue, assuming companies don't cut back on spending based upon macro-economic factors.

While management said in its conversations with leaders from its customer base and potential customers that they aren't considering cutting back on spend at this time, they did point out that there were still rumblings of concerns over potential economic headwinds that may change their minds.

I agree that spend is likely to remain solid in the near term, but in the second half of 2023 I'm not convinced it's going to remain as robust as it has been recently, and if companies start to cut back on expenditures, it's going to result in ZETA underperforming guidance, which would of course hit its share price hard.

In this article, we'll look at some of its recent numbers, the pros and cons of 2023, and whether or not its expected performance is already priced into the stock.

{kind=link}

Some of the numbers

Revenue in the fourth quarter of 2022 was $175.00 million, up 30 percent year-over-year. Revenue for full year 2022 was $591.00 million, compared to revenue of $458.00 million for full year 2021, a gain of 29 percent.

Adjusted EBITDA in the fourth quarter of 2022 was $32.4 million, compared to adjusted EBITDA of $22.9 million in the fourth quarter of 2021, up 42 percent.

Adjusted EBITDA margin in the fourth quarter was 18.5 percent, compared to adjusted EBITDA margin of 17.00 percent in the fourth quarter of 2021.

Net loss in the reporting period was -$(52.00) million or -$(0.36) per share, compared to a net loss of -$(61.00) million or -$(0.46) per share in the fourth quarter of 2021. Net loss for full year 2022 was -$(279.00) million or -$(2.01) per share, compared to a net loss of -$(250.00 million or -$(2.95) per share in full year 2021. On a quarterly and annual basis the net loss was attributed primarily to stock-based compensation.

Free cash flow in the fourth quarter of 2022 was $13.8 million, compared to free cash flow of $14.6 million in the fourth quarter of 2021.

Cash and cash equivalents at the end of calendar 2022 was $121.1 million, compared to cash and cash equivalents of $103.9 million at the end of calendar 2021.

The company had long-term debt of $184.00 million at the end of calendar 2022, compared to long-term debt of $106.00 million at the end of calendar 2021.

On the guidance side of things, management guided for 1Q 2023 revenue to be in a range of $149.00 to $151.00 million, which if attained, would be up 18 percent to 20 percent year-over-year. Revenue for full year 2023 was guided to be in a range of $686.00 million to $696.00 million, representing an increase of 16.00 percent to 18.00 percent.

Adjusted EBITDA in the first quarter of 2023 is projected to be in a range of $22.4 million to $22.7 million, which would be a year-over-year gain of 19 percent to 21 percent. Adjusted EBITDA for full year 2023 is projected to be in a range of $116.5 million to $118.3 million, representing a year-over-year jump of 26 percent to 28 percent.

Adjusted EBITDA margin for the first quarter of 2023 is guided to be in a range of 14.8 percent to 15.2 percent. Adjusted EBITDA margin for full year 2023 is projected to be in a range of 16.7 percent to 17.3 percent.

Concerning overall 2023 guidance, management said it was being conservative in its estimates, and suggested it's likely to be higher than the numbers above. It cited conversations with numerous management teams that resulted in optimistic expectations for 2023. I'm not as optimistic as ZETA and think there's an increasingly likely chance it's going to get tough economically in the second half of 2023, and if it plays out that way, companies are going to cut back on spending, and that would hit ZETA hard.

I've heard a lot of commentary concerning this across a variety of sectors, and the story is almost the same, which is more of a cautious optimism, rather than one of conviction.

At this time there are far too many potentially negative economic variables in play that could disrupt the performance of tech companies like ZETA, to justify what I consider to be unwarranted and overly optimistic outlooks for the next year or so.

Considering that, and the big move the stock has made since July 4, 2022, I see it prepped for a pullback. It appears to me everything is already priced in, and negative economic news would be a significant headwind going forward.

Growth and profitability

On a Quant basis, ZETA is somewhat contradictory, in that it has solid grades on growth and momentum, but a low grade on profitability. And based upon its valuation metrics, it seems to be the company may be slightly overvalued at this time, or close to in line with its value.

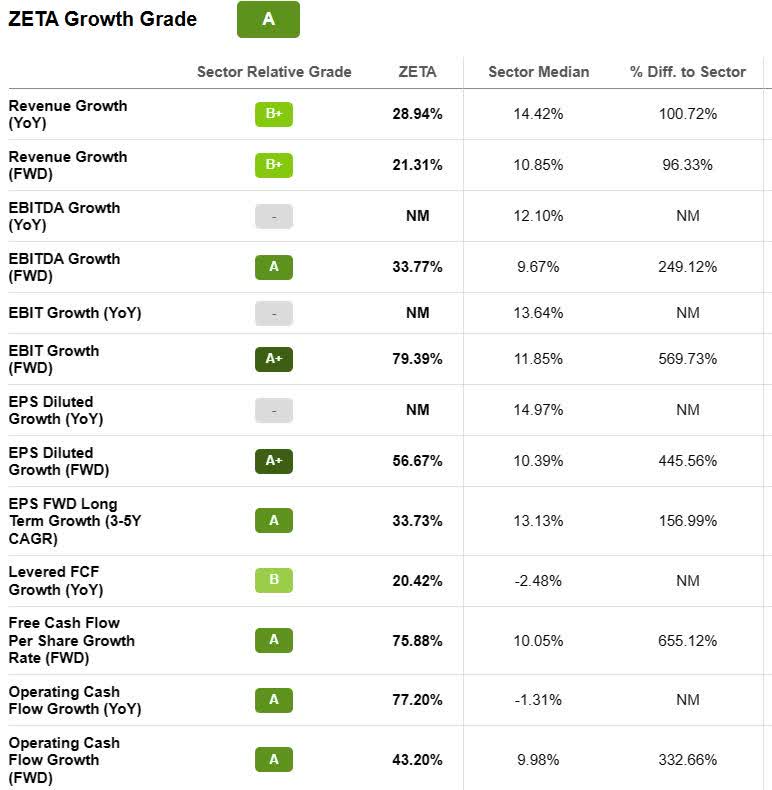

On the growth side, the company has excellent grades in many metrics, but at the same time it has to be taken into consideration that some of them are moving up from a low baseline.

For example, EPS for full year 2022 was -$(2.01), and even though on a ((FWD)) diluted basis it's projected to be at 56.67 percent - much higher than the sector median of 14.97 percent - it's not going to turn a profit anytime soon.

Other growth metrics are similar, and while they represent momentum, again, it's moving from a low baseline to start with. It's a positive for the company but must be taken in consideration with the overall performance of the company, and not on percentages alone.

{kind=link}

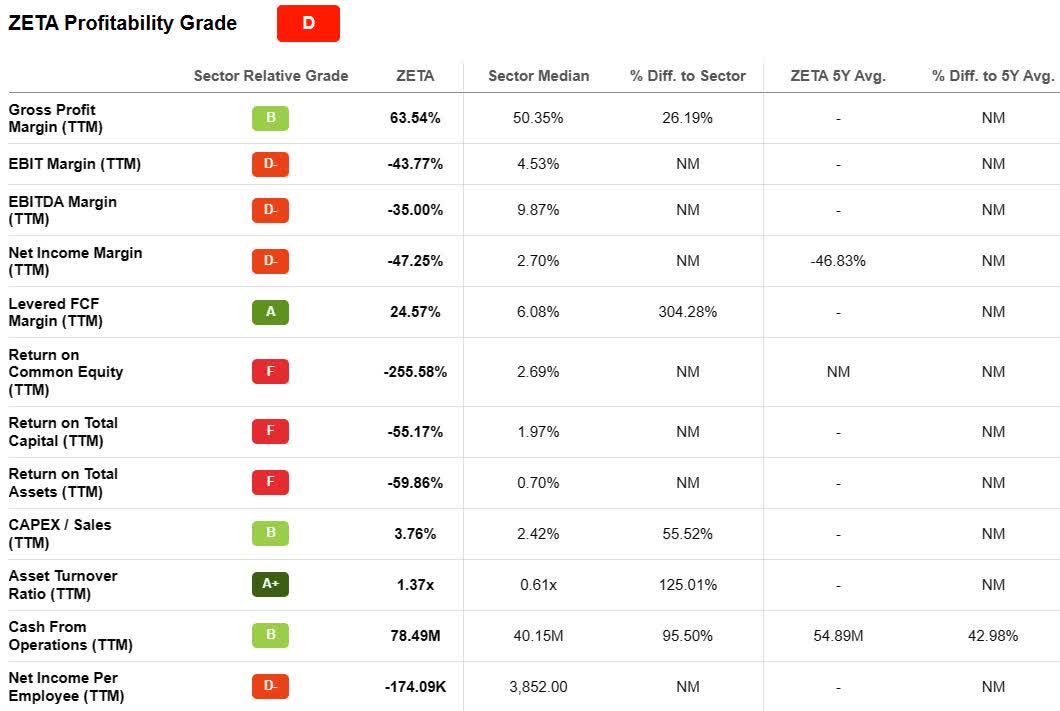

On the other hand, profitability remains challenging for ZETA. In most metrics it vastly underperforms the sector median.

With EBIT margin ((TTM)), EBITDA margin ((TTM)), and the important net income margin, it doesn't come close the rest of the sector.

That's also true with return on equity, return on capital, and return on assets, which were even worse than margin metrics in comparison with the sector median.

{kind=link}

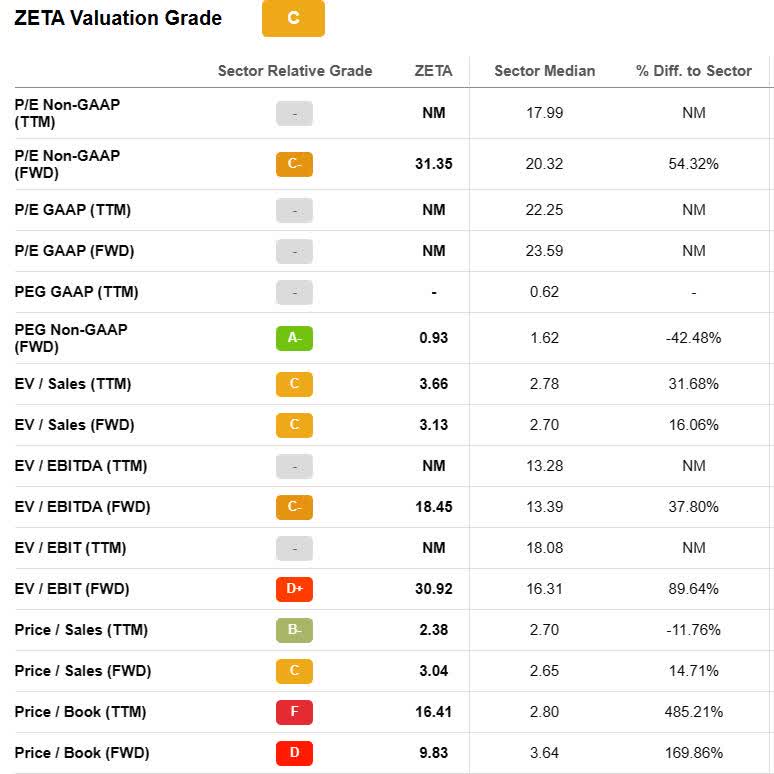

As for valuation, a couple of concerns I have are in regard to Price/Sales ((FWD)) and Price/Book ((FWD)). In Price/Sales it's expected to increase from 2.38 ((TTM)) to 3.04 ((FWD)). With Price/Book it's expected to move from 16.41 ((TTM)) to 9.83 ((FWD)). While it's moving in the right direction, it's still far below the sector median.

{kind=link}

Taking into account profitability versus growth, I see it as a mixed bag, and taking into consideration the company's valuation, I think the stock reflects its value, or is slightly above it.

Conclusion

A high-tech company like ZETA can't escape the impact of the policies of the Federal Reserve and the accompanying high interest rates. Tech companies like ZETA have historically been hit harder than most sectors under those economic circumstances, and I expect that to continue in the latter part of 2023, because I don't think there's going to be the economic soft landing that much of the market is looking for.

The argument could be made that ZETA has already taken the brunt of the impact of Fed policies when it dropped to almost $4.00 per share, and that, in general, would be true. But the overall market is, in my opinion, bidding up stocks under the assumption that the worse is over. I think the market is wrong, which is why the combination of a rapid boost in share price, a weakening economy, and what I see as elevated interest rates that are going to remain stubbornly high for longer than is being priced in now, will push the share price of ZETA down in the quarters ahead.

At this time, I can't see companies continuing to spend at levels expected by ZETA's management if the economy continues to weaken, in accordance with my thesis.

With management guidance and current economic visibility, along with Quant metrics, I see ZETA either being fully priced, or slightly overvalued. The price point it's trading at now isn't a highly favorable one when considering guidance is probably fully priced in.

I think the company has a solid chance at performing well over the long term, especially if it takes share from legacy cloud platform companies. But in the near term I think it's due for a pullback that aligns with current economic realities, and that would be the time to scoop up some shares at an attractive entry point.

For further details see:

Zeta Global Holdings: A Look At If It Can Maintain Momentum