ZIP - ZipRecruiter: Cash And Jobs From The AI Wave Imply Undervaluation

2023-11-14 03:23:45 ET

Summary

- ZipRecruiter has seen an increase in revenue per paid employer and continues to invest in R&D and net sales revenue.

- The company's growth potential lies in its ability to adapt to new job opportunities in AI and digital instruments.

- While there are risks from competitors and regulatory changes, ZIP stock appears undervalued.

ZipRecruiter ( ZIP ) recently delivered an increase in revenue per paid employer, and continues to increase its R&D/net sales revenue. Moreover, taking into account new solutions offered to cope with the new jobs available for artificial intelligence tools and digital instruments, ZIP could see business growth coming. I did identify many risks coming from failure of adapting to mobile devices, regulatory changes, and competitors, however the stock does seem quite undervalued.

ZipRecruiter

With the aim of achieving a competitive differential within the job talent search markets, ZipRecruiter is a North American company that offers a platform for the publication of professional profiles as well as job offers in a vast number of industries, along with the service of curatorship to bring the capabilities of the applicants closer to the needs of the contracting companies. This platform also has integrated artificial intelligence tools that allow the permanent capture of data and the optimization of its interpretations to offer a more efficient service in both directions for professionals as well as companies.

With more than more than 100 million active subscribers on the talent search side and more than 100 platforms managed by third parties to expand its reach to professionals, the business model is addressed through a single operating segment that represents all of the company's income. It also includes the international operation, which represented only 2% of the company's activity in recent years. Income comes largely from the payment of fixed fees for the use of the platform in monthly installments, offering a wide pricing opportunity for the subscription. To this fixed income are added the percentages that the company receives in the case of hiring talent within its platform or the management services derived in this regard.

Depending on the type of payment, subscribers will be able to access different functions within the platform, such as access to the talent list for talent searchers or the possibility of having verified profiles, participating in the rankings in the case of talent searchers employment.

Balance Sheet: The Company Has A Lot Of Cash

As of September 30, 2023, the company noted cash and cash equivalents close to $243 million, marketable securities of about $253 million, accounts receivable of $32 million, and prepaid expenses close to $11 million. Total current assets stand at about $546 million, more than five times the total amount of current liabilities. Thus, I believe that liquidity does not seem an issue here.

Most assets are current assets. With property and equipment of $6 million, operating lease right-of-use assets worth $9 million, and goodwill close to $1 million, total assets are equal to $643 million. The asset/liability ratio is close to 1x, however considering total amount of cash and marketable securities, most investors would appreciate the current financial situation.

Source: 10-Q

The list of liabilities includes accounts payable of close to $8 million, accrued expenses worth $41 million, accrued interest of $5 million, and total current liabilities of $90 million. The list of liabilities also includes operating lease liabilities of about $9 million and long-term borrowings close to $542 million.

Source: 10-Q

Debt

I studied a bit the interest rates being paid by ZipRecruiter, which was useful for making assumptions about the WACC in my DCF model. The company reached agreements with interest rates close to 5% and the LIBOR. With this in mind, I believe that assuming a cost of capital of about 7% and 11% makes sense.

The Company has a $250.0 million credit facility which matures in April 2026. On March 28, 2023, the Company entered into a Fourth Amendment to the Credit Agreement with the administrative agent to replace the London Interbank Offered Rate reference rate with the Secured Overnight Financing Rate reference rate (as defined therein). Source: 10-Q

On January 12, 2022, the Company issued an aggregate principal amount of $550.0 million senior unsecured notes in a private placement. The Notes will mature on January 15, 2030 and bear interest at a rate of 5% per year. Interest on the Notes is payable semi-annually in arrears on January 15 and July 15 of each year. Source: 10-Q

Market Expectations Include FCF Growth In 2024 And 2025

Most analysts out there are expecting sales growth in 2024 as well as net margin growth and FCF growth. I believe that it is worth having a look at their figures before checking my expectations.

2025 net sales are expected to be close to $709 million, with EBITDA of $193 million, EBIT of $207 million, 2025 net income of $58 million, 2025 free cash flow of about $198 million, and 2025 FCF growth of 35%.

Source: Market Screener

Expansion Of Its Job Offers, Further Hiring, Artificial Intelligence Tools, And Digital Instruments Will Most Likely Lead To Net Sales Growth

The company's strategy at present is growth, mainly through expanding subscribers within its platform and its related services. In this sense, in my view, future acquisitions or mergers with companies with similar structures or companies that allow ZipRecruiter to expand its job offer in a specific niche are not ruled out.

The company seeks to exploit growth to achieve the hiring of suitable talents to lead the company's operations. In addition, in my opinion, the company is making an effort for future outreach strategies and an active marketing campaign to grow brand recognition.

It is good to keep in mind that although this type of platform has existed for two decades, in recent years, with the globalization of labor markets, their use has grown exponentially, and the forecasts are positive, especially regarding jobs within the IT industry, application of artificial intelligence tools, and digital instruments.

Further Growth In Revenue Per Paid Employer Could Bring FCF Margin Growth

Given the recent increase in the revenue per paid employer, some investors out there may expect similar behavior in the coming years. As a result, I believe that we would also see an increase in the FCF margins. In my opinion, if the company offers better technologies in the near future, revenue per paid employer will most likely grow again.

We believe our products and services continued to improve and offered more value for employers of all sizes including offering solutions with the best matching technology to help employers identify and recruit standout candidates. Source: 10-Q

{kind=link}

Further Research And Development And Product Development Will Most Likely Lead To Net Sales Growth

In the last quarter, we saw how the R&D/revenue increased as compared to the same quarter in 2022. We also identified growth in the nine months ended September 30, 2023. According to management, increases in R&D lead to expansion of services, product development, and improvements in the marketplace. As a result of these efforts, I believe that we can expect net sales growth.

{kind=link}

This expense may vary as a percentage of total revenue for the foreseeable future as we continue to invest in research and development activities related to ongoing improvements to, and maintenance of, our marketplace, expansion of our services, as well as other research and development programs, including the hiring of engineering, product development, and design employees to support these efforts. Source: 10-Q

The Share Repurchase Program Could Bring Demand For The Stock

ZipRecruiter purchased once again shares of its class A common stock. The company has an ongoing plan to repurchase up to $450.0 million of stock, so I believe that we can expect further repurchases. As a result, I think that demand for the stock and decrease in the total amount of shares outstanding could push the price up.

During the year ended December 31, 2022, our board of directors authorized us to repurchase up to $450.0 million of our outstanding common stock, with no fixed expiration. In May 2023, our board of directors authorized an increase to the share repurchase program of $100.0 million. During the nine months ended September 30, 2023, we repurchased 8.9 million shares of our Class A common stock for $138.9 million under our share repurchase program. Source: 10-Q

Source: Ycharts

Cash Flow Model Based On Previous Assumptions

My cash flow statement projections include small net income growth from 2023 to 2033 and FCF growth. I believe that my numbers are quite conservative, but I will try to offer all the numbers used so that investors can judge themselves.

{kind=link}

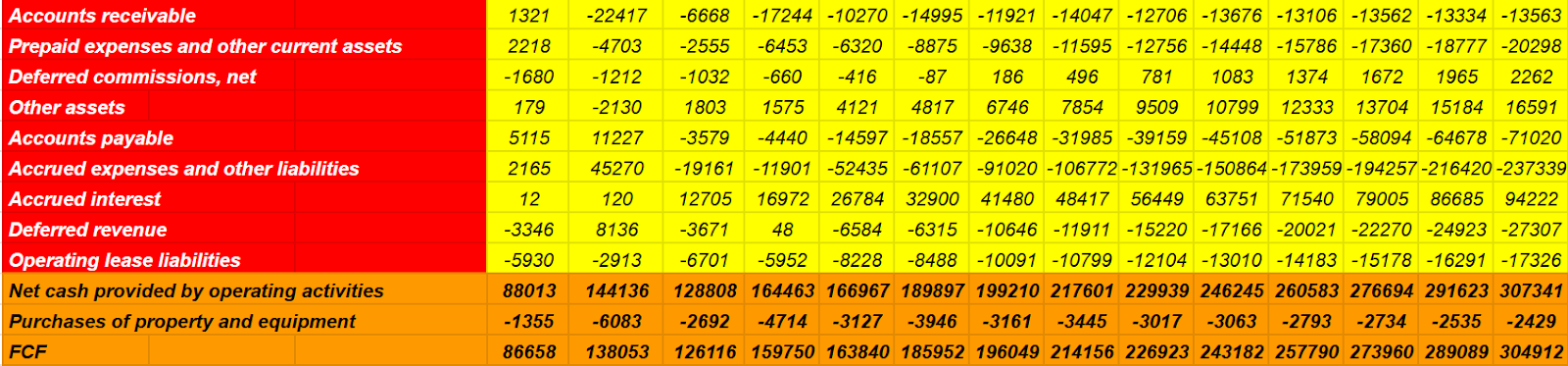

More in particular, I included 2033 net income close to $58 million, with stock-based compensation expense of about $344 million, depreciation and amortization worth $16 million, and provision for bad debts of $10 million.

{kind=link}

Additionally, with changes in accounts receivable of close to -$14 million, prepaid expenses and other current assets worth -$21 million, and deferred commissions of about $2 million, I also included changes in accounts payable of -$72 million.

In addition, with accrued expenses and other liabilities of -$238 million, accrued interest of $94 million, and changes in deferred revenue of -$28 million, 2033 net cash provided by operating activities would be $307 million. Finally, taking into account purchases of property and equipment worth -$3 million, 2033 FCF would be $304 million.

{kind=link}

With FCF expectations ranging from $160 million to $305 million between 2023 and 2033, a WACC of 7%-11%, and FCF multiple of 4x-7x, the equity valuation would be close to $1.7 billion and $2.6 billion.

Source: CW

Note that the sector median price/cash flow stands at 7.6x, and the EV/EBITDA is close to 8x, so I believe that my exit multiple appears reasonable.

Source: SA

The price forecast would stand at close to $17 and $27 per share with a median of about $22 per share. In addition, I obtained an IRR of close to 4% and 12%, with a median IRR of 7%-8%.

Source: CW Source: CW

Competitors, And Risks

CareerBuilder, Craigslist, Glassdoor ( GDOOR ), Indeed, LinkedIn, and Monster are some of the competitors that stand out within a market of high competition and a large number of participants, where there are also companies that offer platforms for hiring specific niches or talents for specific industries. Along with this, we must consider that competition occurs based on participation within the platforms, therefore its optimization plays a fundamental role in this sense.

On the one hand, competition comprises a large number of risk factors, especially considering that there are companies with greater access to resources, brand recognition, and historical relaxation with important international clients.

On the other hand, the company depends on third-party services for the reach of its platform, internet search engines for its outreach campaigns, and its own technology for collecting and interpreting artificial intelligence data. Any significant changes in search engines and disruption in outsourced systems or your own technologies would mean big risks for the company. In this sense, any legal change that includes the possible restriction on the collection of user data or its use for private purposes could generate complications in the current structure of the company.

The ability to adapt its platform to mobile devices and make correct readings of a market in profound transformation due to the emergence of new job opportunities linked to technology and the digital world will also be key elements for the company to contain its growth and remain competitive in the short and long term.

Conclusion

ZipRecruiter recently delivered a significant increase in revenue per paid employer. I think that further investments in R&D will most likely bring expansion in the services offered. At the same time, an increase in the number of jobs available for artificial intelligence tools and digital instruments could bring further net sales growth for ZipRecruiter. Additionally, I believe that sufficient collection of data and data optimization will most likely bring more understanding about clients' needs, which may bring new job solutions and business growth. I do see risks from competitors, failure of adapting to mobile devices, or regulatory changes, however ZipRecruiter does look undervalued.

For further details see:

ZipRecruiter: Cash And Jobs From The AI Wave Imply Undervaluation