ZIP - ZipRecruiter Q4 Results: Downgrading To Hold

Summary

- The results for Q4 and FY2022 for ZipRecruiter were close to what was expected, but guidance was extremely weak.

- After a significant share price increase year to date, and the weak outlook, shares no longer look meaningfully undervalued.

- While the company continues to look promising, based on the less attractive valuation and the weak outlook, we are adjusting our rating to 'Hold' from 'Buy' previously.

If there is one thing that ZipRecruiter's ( ZIP ) Q4 results showed is that headwinds are getting increasingly bad. We found the Q1 and FY2023 guidance particularly concerning. This, combined with a share price that had been moving up year to date, leads us to believe the valuation is no longer that attractive, and we are re-adjusting our rating to 'Hold'. Still, we have to give the company credit, as it has shown that it can be quite flexible and resilient, adjusting its sales & marketing spend to protect profitability.

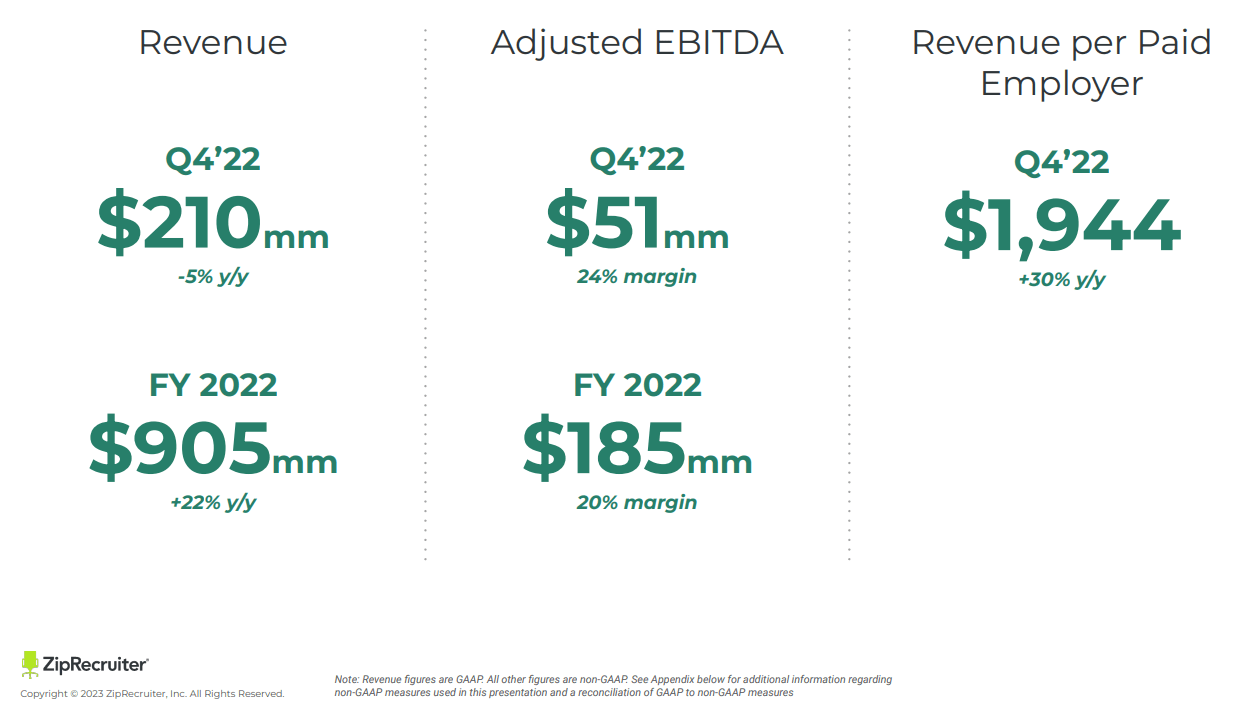

The results appear to reflect a continuation of a trend that started in June 2022, when the company reported that it began to see employers reduce the number of jobs posted. This continued for the rest of the year, and into 2023. ZipRecruiter finished the year with 108,000 paid employers in Q4, a decrease of 26% y/y, and a 20% decrease versus Q3. Needless to say, this is a very significant decline in paid employers on the platform. At least revenue per paid employer continued growing, reaching $1,944 in Q4, an increase of 30% y/y. This softened the impact of having fewer employers on the platform.

Looking at the whole year, 2022 was not too bad for ZipRecruiter. Its revenue grew ~22% to $905 million, and the company delivered a ~20% adjusted EBITDA margin, up from ~15% in 2021. The company also saw a big increase in active jobseekers on its platform, growing to 42 million in 2022, a ~20% increase from 2021. It appears, however, that 2023 will be a very tough year for the company, with revenue expected to go down ~14%. On the positive side, the company believes it can maintain strong EBITDA margins, guiding to an increase to ~24% or ~400 bps of margin expansion.

Q4 and 2022 Results

Fourth quarter revenue of $210 million represents a ~5% decline y/y. GAAP net income was $19.4 million in Q4 of 2022 compared to net income of $21 million in Q4 of 2021. Fourth quarter adjusted EBITDA was $50.6 million, reflecting a margin of ~24%. The biggest positive in our opinion was the ~30% y/y increase in revenue per paid employer on the platform. We believe that, given the macroeconomic environment, the results are not bad, but what likely scared the market was the incredibly weak guidance for 2023.

ZipRecruiter Investor Presentation

{kind=link}

Growth

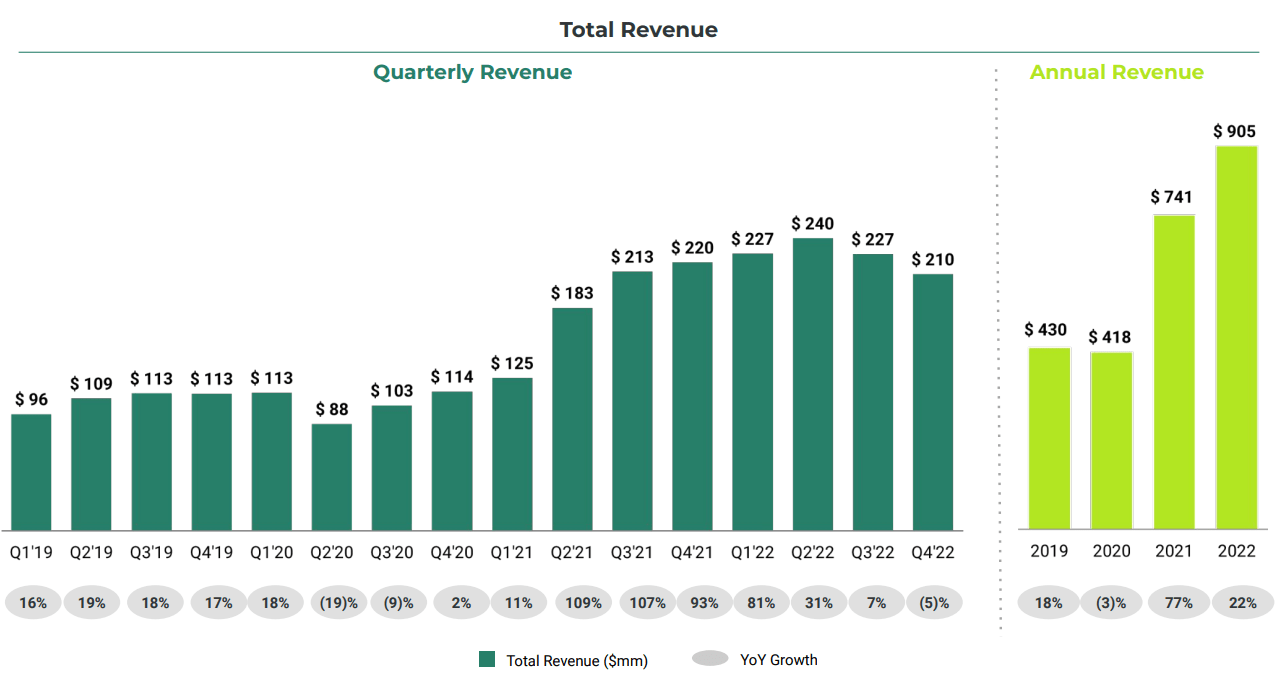

We believe ZipRecruiter is a growth company with significant embedded cyclicality. It is not rare for the company to post negative y/y growth in some quarters, like it did in Q2 and Q3 of 2020. There have been other quarters where its growth rate exceeded 100%. Still, revenue clearly grew significantly between 2019 and 2022.

ZipRecruiter Investor Presentation

{kind=link}

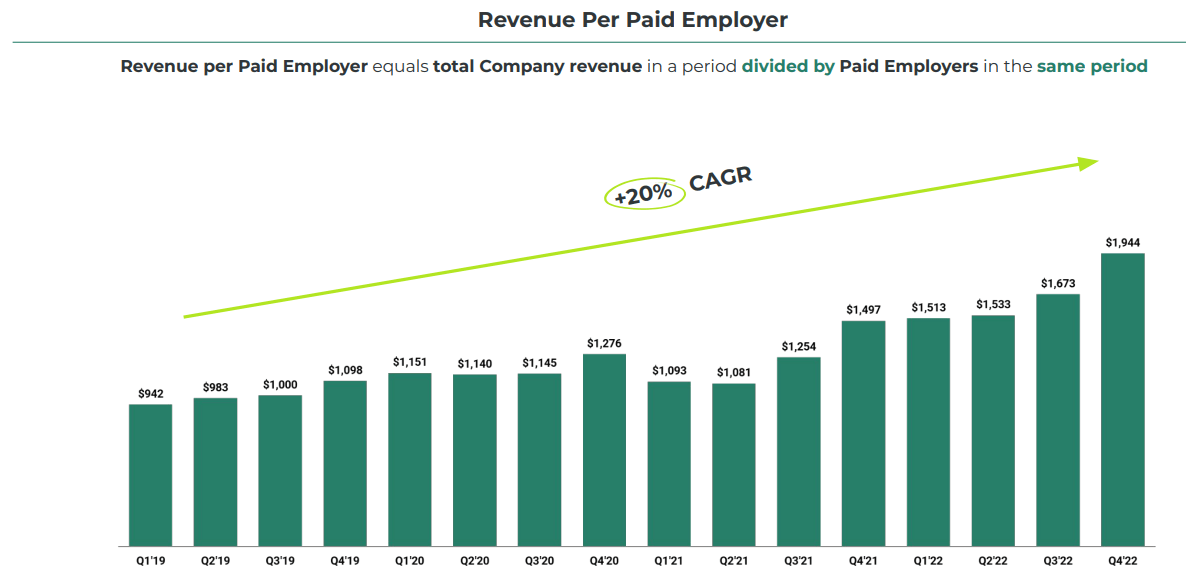

One of the key metrics to follow is revenue per paid employer. Being able to generate more revenue from each company posting jobs on its platform will be critical to sustain revenue growth over time. Here, growth has been a little more consistent. This metric has grown at a ~20% CAGR, which is a nice tailwind for overall revenue growth.

ZipRecruiter Investor Presentation

{kind=link}

Balance Sheet

ZipRecruiter continues to have a very strong balance sheet, ending the year with ~$570 million in cash and short-term investments. This was despite the company spending ~$140 million repurchasing shares during the quarter. ZipRecruiter has been aggressively buying back shares, and in 2022 it bought more than 18 million of its shares, reducing shares outstanding to ~119 million. It reported paying an average price of a little over $18. In addition to a solid balance sheet, ZipRecruiter is generating operating cash flow, roughly $44 million in Q4 alone. One thing to note, however, is that the company is also showing significant long-term borrowings on its balance sheet of ~$541 million.

Guidance

The big surprise from the earnings results was the extremely weak guidance. The company attributed this to the increasingly complicated macro-economic environment. The company shared that revenue in January 2023 declined ~15%, and during the Q&A session of the earnings call , it hinted that February looks even worse. This is CFO Tim Yarbrough's reply to a question from an analyst asking if February was already declining more than January:

So on the shape of Q1, yes, so the 15% we've already noted in the call, 15% down year-over-year. When we kind of zoom out and look at the quarter overall, we think that [Technical Difficulty] provided for Q1 is appropriate given everything that we've seen to-date.

The company's guidance assumes that the negative trend will persist throughout the year. ZipRecruiter currently expects Q1 2023 revenue of $179 million at the midpoint, representing a ~21% decrease y/y. For the full year 2023 it expects $780 million at the midpoint, which means a ~14% decline compared to 2022. Profitability is expected to prove resilient, with Q1 2023 adjusted EBITDA guided at $25 million or a ~14% adjusted EBITDA margin at the midpoint. For the full year 2023 the company expects adjusted EBITDA to be ~$185 million, for a margin of ~24% at the midpoint, roughly 400 bps higher than the 2022 margin, helping offset the impact of lower revenues on earnings.

Valuation

The company has an enterprise value of ~$2.4 billion, which means that based on 2023 guidance, it is trading roughly at a forward EV/Adj. EBITDA multiple of ~13x. While this might sound cheap, the company looks a lot more expensive when using GAAP results. Full year net income for ZipRecruiter was $61.5 million, which means that the company is trading with a trailing twelve months price/earnings ratio of ~39x. Whether this is cheap or expensive will depend on the growth the company delivers in the coming years. Based on the weak guidance for 2023, and shares trading higher compared to our last article, we are adjusting our rating to 'Hold'. Interestingly, the run-up in the share price year to date brought the EV/Revenues multiple close to the historical average of ~3.3x, but that is before the significant drop that shares are seeing in afterhours.

Looking forward, analysts estimate earnings per share for 2024 of ~$0.77. Based on the afterhours prices of ~$19.5 per share, that would represent a FY24 forward p/e of ~25x, although it is likely that analysts will adjust their models after the company's weak guidance. Overall, we believe shares are now closer to fair value, especially when considering the significant short to medium term headwinds.

Seeking Alpha

Risks

In the short to medium term, the biggest risk we see for ZipRecruiter investors is a continued deterioration of the economy. This would mean more companies going from hiring to laying off employees, significantly reducing the need for ZipRecruiter services. In the long-term we believe the biggest risk is Microsoft's ( MSFT ) LinkedIn, if they optimize and improve their platform, especially if they succeed in adding powerful AI capabilities as ZipRecruiter is also doing.

Conclusion

The results for Q4 and 2022 for ZipRecruiter were close to what was expected, but guidance was extremely weak. As a result, shares are dropping in afterhours, and we believe this price adjustment to be reasonable. After a significant price increase year to date, and the weak outlook, shares no longer look undervalued. We are therefore adjusting our rating to 'Hold' from 'Buy' previously. We continue to like the company and believe there is an interesting long-term opportunity, but there might be better entry points given the extremely weak outlook for 2023.

For further details see:

ZipRecruiter Q4 Results: Downgrading To Hold