ZIP - ZipRecruiter: Still Expensive

2023-05-06 11:34:39 ET

Summary

- ZipRecruiter is facing a lot of tough competition. It needs to differentiate itself somehow.

- The management is very excited about its AI assistant in the future.

- The softness in the economic environment will weigh further on the company.

- The balance sheet is decent; however, the company is still quite expensive.

Investment Thesis

With Q1'23 earnings just around the corner, I wanted to take a look at ZipRecruiter Inc. ( ZIP ) in more detail to see if such a high P/E ratio is justifiable, even after a huge drop when it reported FY22 results. In short, the company is still a little expensive in my opinion, and with further softening in the economy, fewer job postings, and overall negative sentiment, I could see the company go further down as volatility lives on throughout the whole of '23 and probably beyond.

I will look at the hiring sector in broad terms, and also what could be good catalysts that could propel the company’s revenues in the future.

About the company

Zip Recruiter is an online employment marketplace that connects quite a big user base of employers to employees in the US and Canada via their website and their mobile app. The company is in a very competitive sector, where its biggest competitors are Microsoft's ( MSFT ) LinkedIn, Indeed, Glassdoor, and Monster to name a few.

Needs to Stand Out - Revenue Catalyst

So, the company needs to stand out somehow to attract more people to its platform. The focus on employers and an easy-to-follow format, while the ability to apply to a job with one click is a good feature to have for employees, as I know myself when I was applying for jobs before, after uploading the CV to the employer's platform, I would then need to put in the same information manually. In the end, I would only look for jobs on LinkedIn that have one click feature. This feature is available on many websites like LinkedIn and ZIP, so what could be a great feature that competitors don't have? The answer is Phil, the smiling, cartoony AI assistant that helps employees improve their profile, scans for better matching jobs as it learns from how the person interacts with each posted job, and cheers you on until you get a job.

This is not all new, to be fair. Other companies have been using AI assistants for a while too, like InstaHyre or Tarta.ai , however, with the new boom in generative AI over the last few months, I do believe that the company will mention Phil a lot more in the coming months. The management already mentioned Phil quite a bit in the earnings transcript .

The advancement of AI in recent months and every company going up with a mere mention of the two letters pop up. Surprised it didn't during the FY22 earnings call, but I do think that was overshadowed by the weak guidance the company gave for '23. I would venture a guess that in the next report, the company will go even harder on the AI assistant, as it has been working quite well for them in the past. Phil has been very well received by candidates, as mentioned in the same transcript above. People are taking Phil's advice to heart and making adjustments to their profile, CV, or other parts of the recruitment process.

Volatility Ahead

The company dropped over 20% on FY23 guidance in February. The management guided for a very weak year ahead, which is predicted to decline by around 14% by the end of '23. It’s no surprise that many companies are scaling back on hiring new staff, which doesn’t necessarily mean that they’re firing people, as the unemployment rate still ticked further down in April to 3.4% .

If the company already is seeing such softening in the markets, once the unemployment rate starts to tick up in the next 6-12 months, I would expect the company to see a lot more revenue declines, and investors did not like such weak guidance, and I don't blame them.

Slowly but surely, the job openings to jobseekers ratio will fall back down to what the Fed is looking for, which is 1:1. As of February of this year, that ratio stood at around 1.67 , which is well down from 2.0 we saw in 2022. This will surely affect the company's revenue negatively, and we will see a lot of volatility this year and probably going into ’24.

Financials

Let’s look at how the company will be able to weather the economic downturn.

At the end of '22, the company had a very decent cash position of $227m and $342m in short-term investments, so around $570m in liquidity, compared to long-term debt of $540m, and we can see that the company is positioned well in terms of liquidity.

The interest coverage ratio has been fluctuating quite a bit in the last 4 years, however, the EBIT number as of the end of '22 covers the interest expenses over 3 times. The debt the company took on is quite new, but eventually, I would like to see it paid off.

The company’s current ratio is very healthy too and has improved quite considerably over the last 2 years or so. I wouldn’t mind seeing the ratio come down to around 2.0 again, as we saw in ’21. ZIP has no liquidity issues.

{kind=link}

In terms of efficiency and profitability, there isn’t a lot of consistency from the company as it is still a relatively new one, so it is very hard to judge these metrics. ROA and ROE do not show a good trend yet. One year of being quite profitable and efficient does not mean it will be again.

{kind=link}

Same story with ROIC, it seems like the company may have some sort of competitive advantage, however, I would need to see this being more consistent in later years.

ROC (Own Calculations)

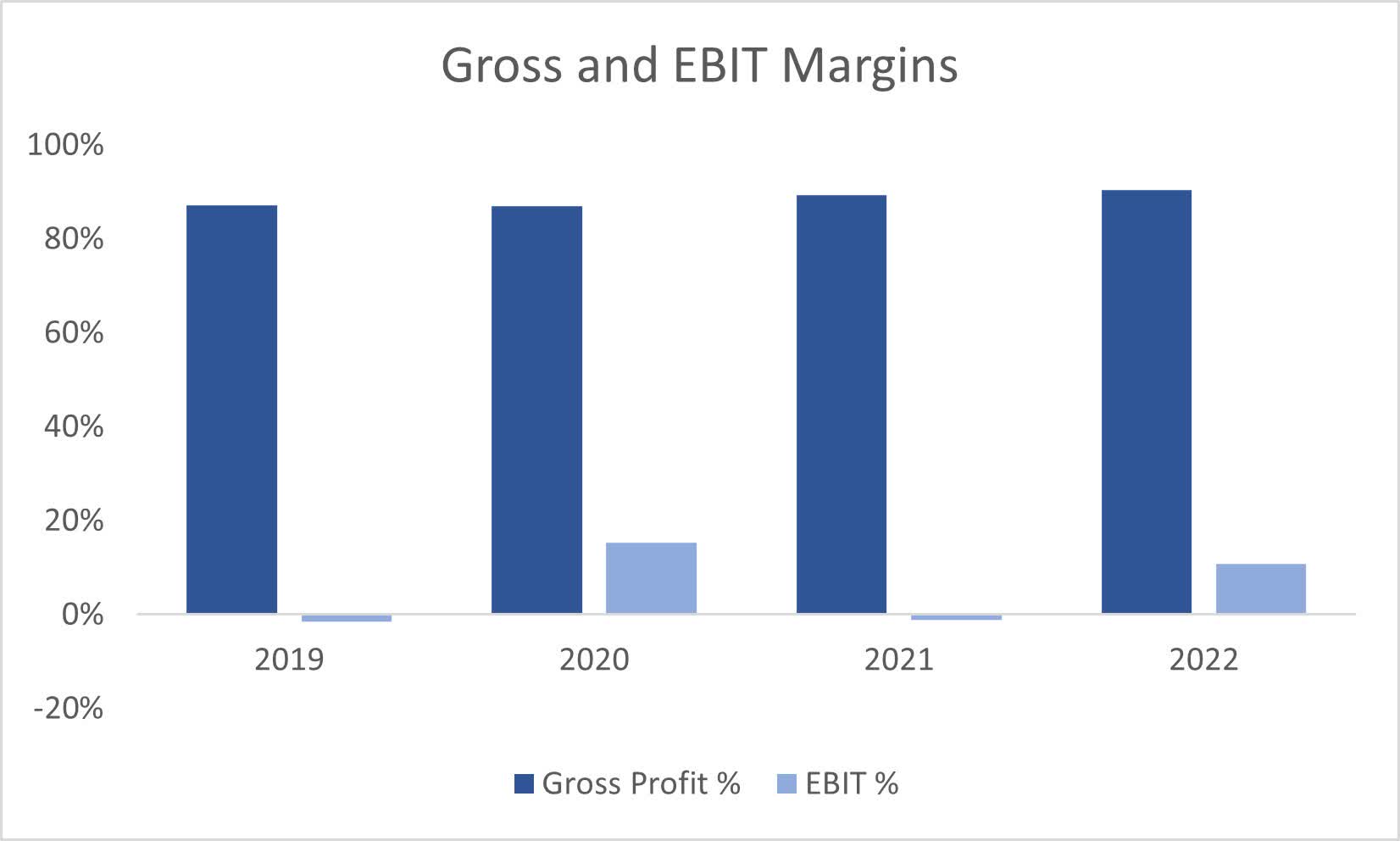

Gross margins have been fairly consistent; however, EBIT margins have seen a lot of fluctuations.

{kind=link}

In terms of liquidity, the company seems to be geared well for a downturn, however, in terms of efficiency and profitability, the returns jump around too much y-o-y, and the company is very volatile when it comes to bottom-line consistency.

Valuation

It’s not going to be easy to come up with decent revenue growth for the next 10 years, but I’ll try to be on the conservative side and see what kind of valuation I would get for a company like that.

For ’23 for the base case, I will go with -a 14% decline in revenues just as the management has guided, they would know better than me that's for sure. For the next years, I decided to go with a 25% bump in '24 and linearly decrease the growth to 5% by '32, giving me a 12.1% average annual increase. I think these are quite reasonable, the company saw -3% one year, then 77% the next year, and 22.1% in '22. The company is still quite young and has some pretty good prospects of succeeding.

For the conservative case, I went with a 10% average over the next decade, while for the optimistic case, I went with 14%.

In terms of margins, as I mentioned before, these have been quite volatile over the last 4 years. With time, however, digital companies like ZIP will figure out a way to be more consistent and efficiency will come. I went with a 200bps improvement in margins over the next decade, just to be on the conservative side, as I believe the company can achieve much better margins.

On top of these estimates, I will add a 25% margin of safety. The balance sheet is decent enough to warrant my lowest margin of safety requirement.

With that said, the company's intrinsic value is $12.59, which implies a 27.5% downside from current valuations.

{kind=link}

Closing Comments

The company has a good future ahead, however, with the volatility on the horizon, I cannot recommend buying it right now, even after the 20% drop. It’s just a bit too expensive still. If the company manages to grow at around 12% a year, the current P/E ratio is unjustified. The company would have to grow at 15.5% a year to justify the current valuation, which is not impossible, but I’d like to keep it on the safe side, as I’d like to get a better risk/reward ratio with a more conservative estimate.

There is a possibility that the company might even ride the AI wave a bit, but in the long run, if the company doesn’t manage to improve its profitability and efficiency, there are better companies to invest in for the long haul. I’ll keep an eye on this one when the earnings come out, as I want to see what the management thinks about the short-term future, and if they see improvements or further deterioration that could last well into ’24.

For further details see:

ZipRecruiter: Still Expensive