TSLA - 'A Brutal Space': Bad News For Tesla From Mercedes-Benz

2023-12-04 07:00:00 ET

Summary

- Tesla, Inc. faces challenges in the competitive EV market with decreasing margins, raising concerns about its high valuation and future sustainability.

- Industry competitors like Mercedes-Benz, Volkswagen, and Stellantis present tough competition, impacting Tesla's market share and pricing strategies.

- Despite Tesla's growth, its financial performance lags behind peers, leading to doubts about sustaining its premium valuation in the long term.

Introduction

"We dug our own grave with Cybertruck. Nobody -- generally, everybody digs a grave better than themselves."

With these words no more than a month ago, Elon Musk himself talked about the event everyone is focusing on the Cybertruck launch. Moreover, Mr. Musk admitted "there will be enormous challenges in reaching volume production with the Cybertruck, and then in making a Cybertruck cash flow positive."

In the meantime, I had finished going over most of the earnings reports of the main Western automakers, and I could not help but collect some piece of information to paint a picture of some hurdles across Tesla's bull case, in particular given its current valuation.

The mind frame to assess Tesla

How to value Tesla, Inc. ( TSLA ) springs directly from the answer to one question : is Tesla a tech company, or is it an automaker?

My perspective is the latter: Tesla belongs in its own unique way to the auto industry. This is supported by what Tesla writes about itself in its form 10-k.

We design, develop, manufacture, sell and lease high-performance fully electric vehicles and energy generation and storage systems, and offer services related to our products. We generally sell our products directly to customers, and continue to grow our customer-facing infrastructure through a global network of vehicle service centers, Mobile Service, body shops, Supercharger stations and Destination Chargers to accelerate the widespread adoption of our products. We emphasize performance, attractive styling and the safety of our users and workforce in the design and manufacture of our products and are continuing to develop full self-driving technology for improved safety. We also strive to lower the cost of ownership for our customers through continuous efforts to reduce manufacturing costs and by offering financial and other services tailored to our products.

Its current financials also support this thesis. Considering the last three fiscal years , we can see how automotive sales can't be really compared with energy generation and storage revenues.

| USD millions |

| FY 2020 |

| FY 2021 |

| FY 2022 |

| automotive and service revenue |

| 29,542 |

| 51,034 |

| 77,553 |

| energy and storage revenue |

| 1,994 |

| 2,789 |

| 3,909 |

So, as disruptive as Tesla may be, I can't help but consider it as currently part of a broader industry - auto manufacturing - whose valuation criteria are more or less given by the market. In particular, it is one of the industries trading at extremely low multiples, with most stocks trading between a 2 and a 6 P.E ratio.

This is why some news I collected from other automakers made me wonder if Tesla's future is currently so bright to justify "buy" and "strong buy" ratings, as I still see happening. But even if the company may indeed manage to be always on top of the industry, does its stock price reflect a correct valuation or even an undervalued opportunity?

In this case, it is even more important to know that a business may be wonderful, but its stock may not be as wonderful due to overvaluation.

Now, on the side of its organic business, Tesla might face some troubles moving forward. This is what I thought after I put together a few pieces of a puzzle.

Let me share them with you.

A brutal space

As I was going over Mercedes-Benz Group AG's ( MBGAF ) recent dip and the buying opportunity I think it is offering, I could not help but shudder as I read these words from its management during the last earnings call:

EV is a very competitive space. I mean, come on, with price discounts or some of the other guys, more than 30%, some of the traditional players selling best vehicles below the pricing level of ICE with variable costs probably sitting above, as you know. I would say this is a pretty brutal space.

After this, Mercedes' management spoke about price discipline and how the company won't sell any BEV (battery electric vehicle) at a loss. However, pointing out competition is important. There were already 40 BEV models available in the U.S. as of March 2023, with more that have been released in recent months. This increasingly will lead to a more fragmented market, where Tesla's 62% of 2022 BEV market share is forecasted to drop to around 18% by 2026. No matter what the forecast is, with such a growing availability of BEV models, a 62% market share is unsustainable.

Moreover, we should also consider Mercedes has higher FSD certifications than Tesla, since it is the first certified level-3 autonomous car in the U.S., beating Tesla at his own game.

Volkswagen ( VWAGY ), the BEV market leader in Europe, in its last earnings call also had some concerning news regarding BEVs.

our order intake is below our ambitious targets due to the lower-than-expected overall market trend. [...] The order bank of BEVs went down 150,000, but we have a very strong order bank in Western Europe. [...] We currently face a general reluctance in the European market to buy battery-powered vehicles. [...] As a consequence, we are currently investing in both BEVs and ICE technologies in parallel, a situation that we expect to continue over the next 2 years.

Moreover, Volkswagen spoke, too, about a "very competitive pricing environment" in BEVs. Tesla is part of this environment because this year, it has been aggressive in targeting volume growth. This means it was willing to sacrifice its margins to reach better scale. Therefore, we saw several price cuts

Although Tesla has made progress in bringing its cost per vehicle lower over the past four quarters, the average selling price of its cars went down at a quicker rate due to price cuts .

On the other side, BMW ( BMWYY ), in its last earnings call , saw strong BEV momentum, with increasing orders and profitable sales, although the company is not present in the under EUR 25k segment.

Another company that seems to fare better in BEVs is Stellantis (STLA), as it announced in its last earnings call that

At EUR 23,300 we are the first major carmaker to offer a BEV in Europe, which is manufactured in Europe at a price below EUR 25,000. And towards 2025, we’ll break the next price threshold with our urban variant, calibrated for lower range needs at just under EUR 20,000. The launch reception has convinced us that there will be strong demand for this product and [...] these vehicles are going to be profitable from day one at Stellantis.

The picture seems mixed, with a few struggling manufacturers while others appear to be doing well. Electric-car inventory has been piling up, and with market penetration rate " slightly lower than prediction [...] because EV uptake has weakened in North America".

After all, with high interest rates, most goods requiring financing to be purchased see demand deterioration. Tesla's CFO addressed exactly this issue in the last earnings call.

As regards our pricing strategy, in addition to what we have shared before, I want to elaborate that most car buying happens with one or other form of financing, and hence we also view pricing in terms of monthly costs for the customer. And therefore, as interest costs in the U.S. have risen substantially, it has required us to adjust the price of our vehicles to keep the monthly cost in parity. We’ve tried to offset such adjustments via focus on reducing costs. However, there is an inherent lag in cost reductions, which in turn impacts margins. To that extent, we recently announced a partner vehicle leasing program in the U.S. whereby you can get a standard Model Y for as low as $399 a month.

And Mr. Musk added:

So, if interest rates remain high or if they go even higher, it’s that much harder for people to buy the car, they simply cannot afford it. [...] I know people want to us advertising, we are advertising. I think there’s something to be gained on the advertising front. I don’t think it’s nothing. But informing people of a car that is great, but they cannot afford doesn’t really help. So that is really the thing that must be solved is to make the car affordable or the average person cannot buy it for any amount of money or they can’t afford it. So, this is big deal.

The Cybertruck

With a delay of two years, the Cybertruck launch has caused many reactions . Needless to say, not all of them were enthusiastic. In particular, there were some disappointments regarding the range which goes from 250 miles for the rear-wheel drive to 340 miles for the all-wheel drive.

{kind=link}

Moreover, part of the disappointment came from pricing, which ranges from $49,890 to $96,390. At first, Tesla had guided for an entry price below $40,000. Of course, inflation needs to be blamed, at least in part. But the entry price is 25% more than what had been previously hinted, and this hike far outpaces the hot inflation we have had in the past two years. Of course, Tesla may indeed be engineering and manufacturing a built-from-the-ground and disruptive pick-up. But the challenge of making it affordable hasn't been fully overcome.

This leads me to another consideration. Tesla guides for 250,000 units sold in 2025. Consider Ford's (F) F-150 Lightning, which starts at $51,990 and can thus be considered similarly priced to the Cybertruck, and which has sold approximately 16,000 units year to date. I personally find it very difficult for Tesla to create so much demand starting almost from scratch.

Tesla's financials

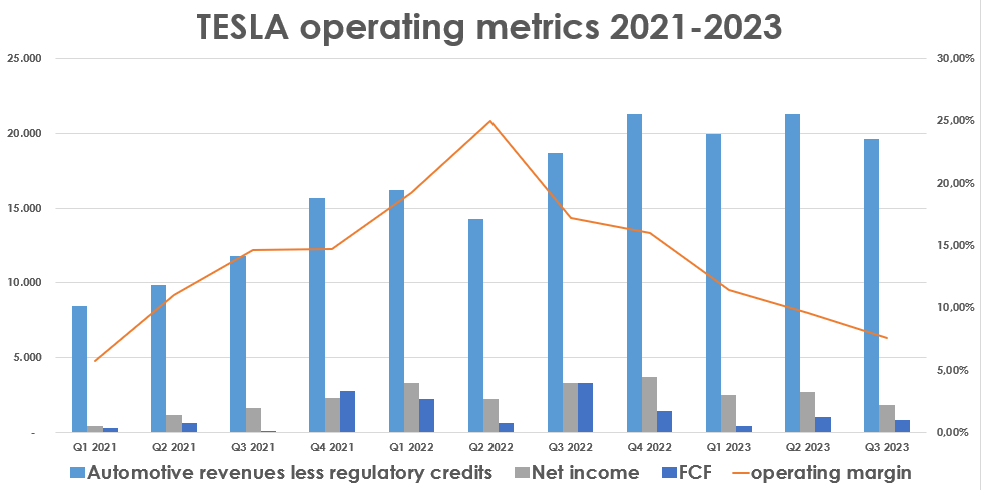

In any case, the pressure of this environment is impacting Tesla rather harshly. On one side, its automotive revenues have grown thanks to volume growth. On the other, the company's profitability is taking a hit: net income is decreasing as is free cash flow. Most importantly, the operating margin has plunged for 5 consecutive quarters by now, moving from 25% to 7.6% in Q3 2023 .

Author, with data from Tesla's quarterly reports

{kind=link}

Well, some may say this is a general problem for the industry as a whole.

But if we compare how Tesla's competitors are doing, we see that Tesla is performing worse than its competitors.

It is still among the top 4 automakers, considering the TTM. Yet, its margins are normalizing. For the TTM, we see Tesla still in the top tier. On a side note, while it may not be surprising to find Mercedes and BMW (BMWYY) among the most profitable automakers, we should highlight the extremely good performance of Stellantis, led by a management team worldwide known for its ability to turn unprofitable businesses into cash cows. But a 7.6% operating margin, such as the one recently reported, sets Tesla way lower among its peers.

I actually think Tesla's margins will move north once again and could be in the low double-digits. Yet, I would be extremely surprised to see them climbing up again at 20-25%. It's nearly impossible in the auto industry, at least until it is so highly competitive.

Valuation

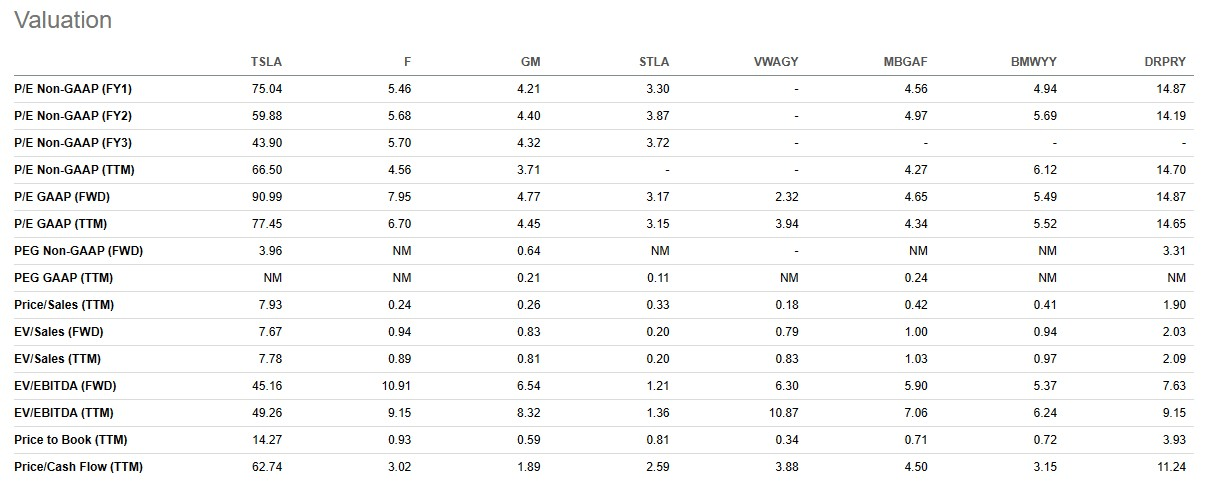

Currently, Tesla's TTM EPS amounts to $3.11. This gives a TTM P/E of 77.2. Of course, we need to be forward-looking. Current consensus sees Tesla's earnings at $4.01 for FY 2024 and $5.47 for FY 2025. This is a fwd P/E of 60 and 44 respectively. Not even Ferrari (RACE) trades at these multiples, though it is one of the safest, most predictable, and most profitable companies in the industry. Even if move further ahead, the current forward P/E for 2032 is 13, which is way above most of its peers . By then, I bet the industry will have consolidated and several BEV winners will be operating. As far as I can see, Tesla trades at an immense premium, very difficult to protect, and is very dangerous for long-term investors. There are many well-insulated companies with safer growth prospects trading at more interesting and fair valuations.

It might not be widely known, but in the last 3 years, Stellantis returned 106% against Tesla's 26%, and in the last year Stellantis has returned 54% against Tesla's 23%. This shows how Tesla's valuation has been stretched, and the stock has thus had some difficulties in giving once again the incredible performance it returned until the end of the post-Covid bull market.

If we compare Tesla's multiples to its peers, we see it trading at P/E ratios between 44 and 91, depending on the time frame. Its peers, aside from Porsche ( DRPRY ) all trade in the low- to mid-single digit P/Es.

I ask myself and my readers: is this reasonable? Is there so much of a premium to be paid for a company whose cars may have been disruptive but whose margins are now below 10%? I believe not.

{kind=link}

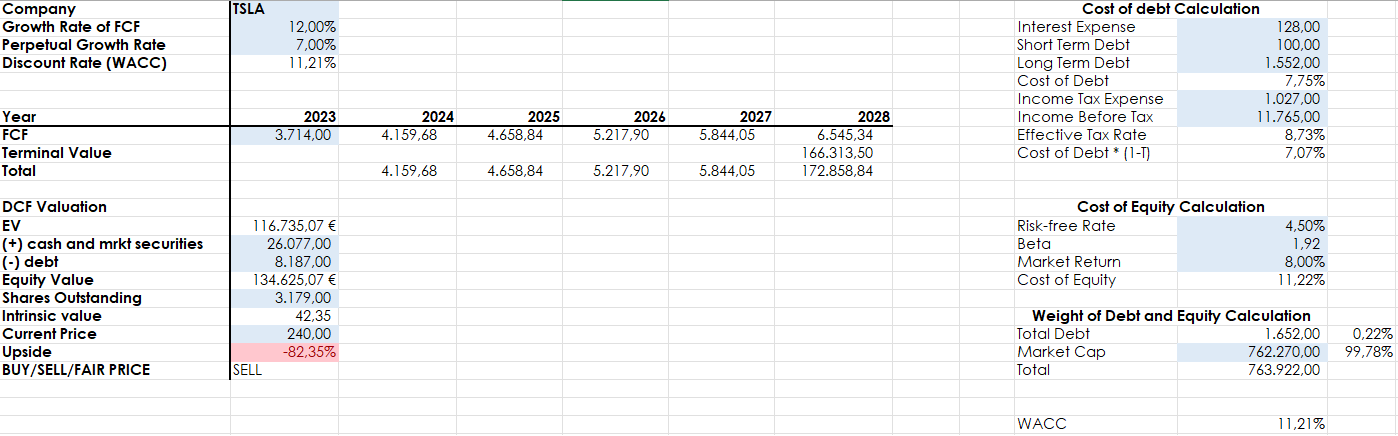

To show why I don't think so, let's run a discounted cash flow with some bullish assumptions for Tesla.

Author, using TTM financial data

{kind=link}

On one side, I use the TTM financials. On the other, I assume 12% FCF growth for the next 5 years with a perpetual growth rate of 7%. These are high rates. Still, the result is that Tesla should trade at $42.35 instead of $240. At this price, we would still be using a 13.6 earning multiple for this year, which already reflects quite a premium compared to other depressingly valued automakers and would position Tesla at the same level as Porsche. As much as one can like a Tesla, it is hard to say Teslas are in the same car category as Porsches.

Conclusion

I am no short-side investor and very rarely I short stocks or sell put options. Nonetheless, the reasons shown above make me think Tesla is not likely to sustain its valuation for much longer. Therefore, I suggest moving out of this stock, where hype and volatility seem to determine its price much more than its fundamentals. At the moment, probably many investors are in the green on Tesla, and it would be wise to lock in some gains and move them to safer and higher-quality compounding machines.

For further details see:

'A Brutal Space': Bad News For Tesla From Mercedes-Benz