FLO - 'Buy' 2 Undervalued Food And Drink Companies

2023-10-28 01:56:32 ET

Summary

- Diageo and Flowers Foods are two superb companies in the consumer goods sector - one in bread and one in spirits/alcohol.

- I own both of these businesses, and I'm currently adding more shares to the businesses due to continued undervaluation.

- DEO and FLO are currently both at "BUY" ratings - and consider the company to have upsides of over 20%, both of them, over the next 3 years.

Dear readers/followers,

With the market currently in shambles in terms of valuations, I believe it's time to highlight undervalued quality businesses currently available on the market. And obviously, one of the very first things that I look at is actually consumer goods companies.

Why do I look at consumer goods companies above others?

Because they offer the advantages of being resilient, must-have businesses and products without having the regulation of utility-type businesses, provided you're okay with safety above a triple-digit short-term RoR, these companies offer some of the best investment potential around. None of them have superb or massively high yields - but they come with unparalleled safety which is something you want in the current market - if not for your own sleeping well at night, then for wealth preservation.

All of these companies I'm going to present to you are companies I have invested money into. All of these companies I'm presenting to you are companies that I'm going to invest more money into.

All of them are at least investment-grade rated, and all of them have a significant upside to consider here.

Let's look at 3 consumer goods companies you can buy at undervaluation

So, you might expect me to talk about Altria ( MO ) or British American Tobacco ( BTI ) here.

You would be wrong. Those are not the companies I will be looking at here. I'm not talking tobacco - I'm talking food and spirits. I view those businesses as safer than I do tobacco. I'm not avoiding tobacco as such - I have exposure to both of those businesses - but I'm favoring others here.

Oh, and all of these businesses are companies I've written about at one point or another.

We'll begin with Diageo ( DEO )

1. Diageo

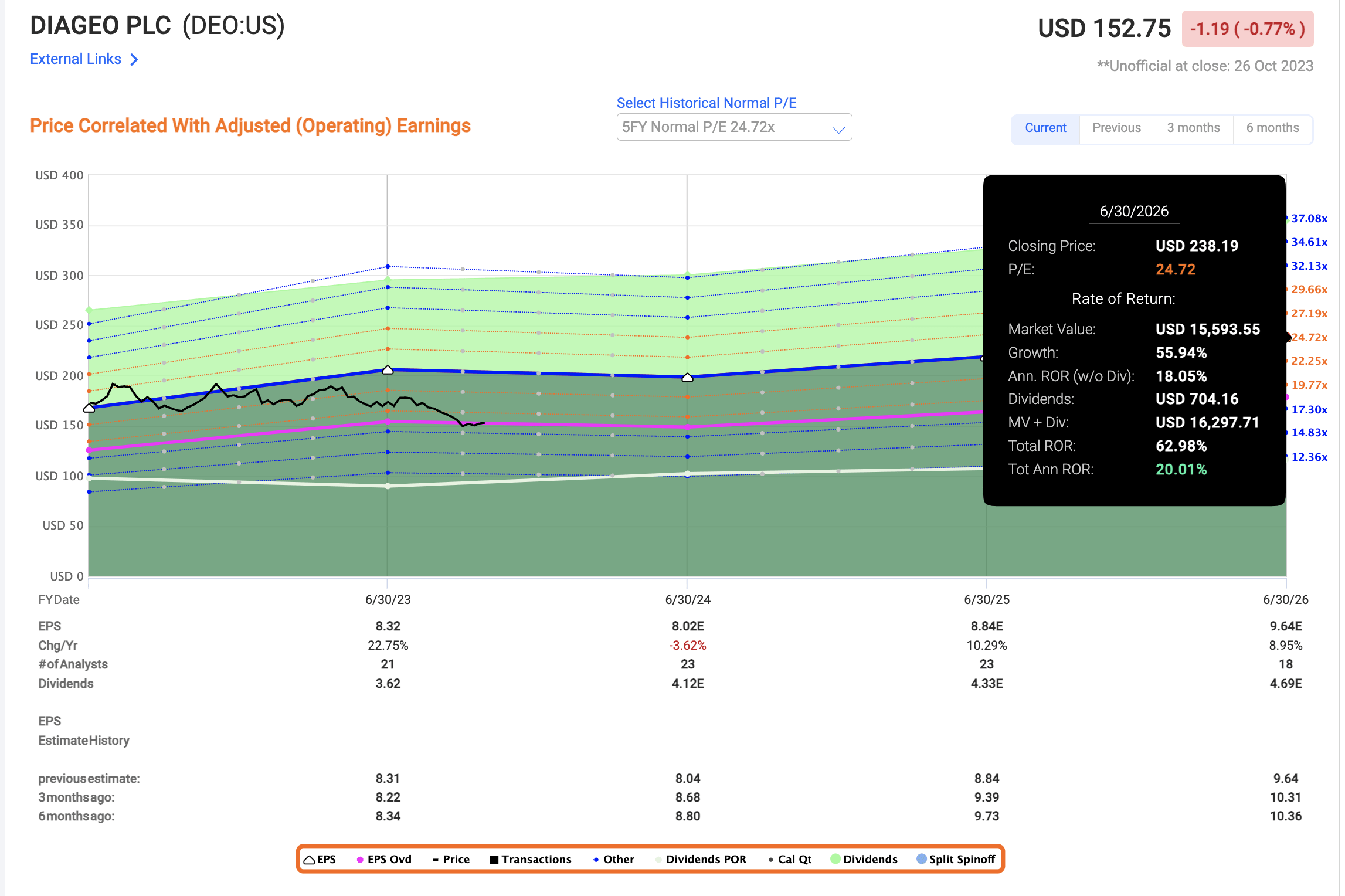

My last article on DEO was back in September, several years ago. The company has actually performed pretty well - 18.5% RoR since then, though somewhat less than the market. But the company has actually trended down somewhat since and now stands at what I believe to be a significant undervaluation.

It was formed back in 1997 when the Guinness Brewery and Grand Metropolitan merged. It owns some of the most famous, and best spirits on earth.

{kind=link}

The company's share price evolution is a product of margin and macro changes. DEO has not seen a crash in EPS, rather improving its adjusted earnings by double digits in the 2023A fiscal, going into 2024, and is expected to continue to grow at an average rate of 6%+ year in terms of EPS until 2026E.

Diageo is an A-rated giant , with a current multiple of 18.5x to earnings, which might sound high but really isn't when you consider that DEO typically trades somewhere at 25-29x P/E. (Source: FactSet)

We'll of course see some lack of premiumization given the changes in macro and interest rates. That's only natural. The question becomes where we should value this company on a forward basis. My answer to this is that it should be valued at least higher than 16-18x P/E. This is because the company's portfolio includes global giants, which together have a combined retail value of nearly £16B per year. Smaller, local brands are still strong and are complemented by the company's reserve brands.

Diageo is truly a global company, with a reach into nearly every nation of the world. While the main markets are clear, the company has sales virtually everywhere. Product sales happen in 180 countries and consist of large shares of vodka and Scotch as well as beer - most other products are at sub-10% of company sales.

Alcohol consumption does, of course, differ from nation to nation. Yet, investors need to consider that when investing in Diageo, you're essentially investing in the human desire to drink alcohol - and a company's ability to capitalize on that desire. Diageo's history, brands, and trends show that the company is quite apt at doing just that.

The company reported 2023A results around 2 months ago. The company saw trends not dissimilar to other consumer goods companies, meaning increased net sales and increased operating profit in the low-mid single digits, while actual volume went down. Earnings were up over 17% though, and over 20% on an adjusted basis. Given the broad uncertainty across the planet, I believe it fair to say that the performance that was reported was a good one in context.

There are many analysts that would give the company a massive premium or potential increased upside, resulting in a triple-digit upside. I am not one of those analysts. I believe Diageo has an upside, but I believe that any quality consumer goods company is more likely to be a slow grower and so too this one.

The reason why I believe you should look closer at Diageo is simple.

Valuation

Diageo trades at a current 18.5x P/E and a share price of close to $150/share. At a 5-year average P/E, the current implied 24.7x share price is closer to $200/share, and in the longer term to 2026E, it's implied with the current EPS growth rate at around $240/share.

This is not a massive yielding company. 2.56% is less than the going risk-free rate, far less in fact.

But find me another consumer goods company with an A-rating that gets a 20% annualized RoR or 63% in 3 years based on trading at its historical premium.

{kind=link}

You won't find many.

DEO fulfills my current demands for a conservative consumer investment.

- Investment-grade or above, preferably BBB+

- A well-covered yield.

- A strong moat and strong earnings prospects regardless of the coming macro

Even if the company were to stick to this historical discount, the company would still annualize over 8% returns per year. For you to lose money on DEO, including dividends, the company would have to drop below 14.5x P/E in the long term, which for 2026E implies a share price of $140/share, meaning it would not move from now, only decline.

I consider that scenario to be very unlikely.

Diageo is a "BUY" to me here. I have a position in the company, and I'm expanding my position. It's a company where I buy slowly, and I buy for the very long term.

So, that's #1.

Let's look at #2.

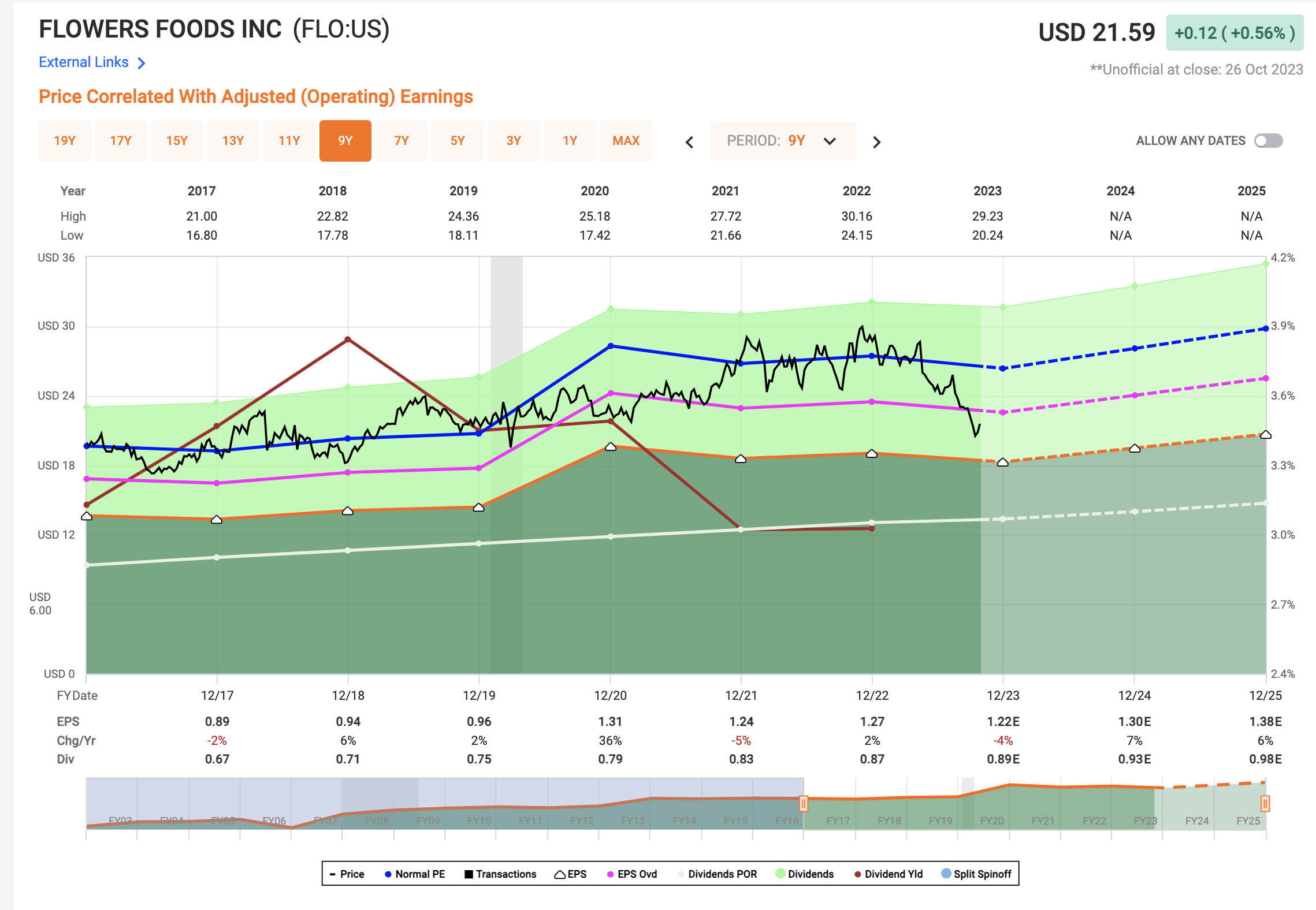

2. Flowers Foods ( FLO )

At this time I am kicking myself for not pushing this article earlier - because Flowers Foods has already started reversing. I bought the company close to $20.5, the company is now above $21.5. It might seem like a small change, but valuation matters.

Why is Flowers Foods a company I "BUY"?

Because it's a great business. It's bread. People are going to keep eating bread, and FLO is $4B+ worth of market cap in bread and baked goods. I've actually been neutral on this company for some time, and this recommendation has turned out to be exactly right since my last piece because the company has declined over 20% excluding dividends.

Seeking Alpha FLO article (Seeking Alpha)

So, I consider myself an apt investor in FLO - because I sold at a profit of over 20%.

Now I'm back in.

Why am I back in?

Because Flowers Foods represents one of the best brands in bread. it's the #1 loaf, organic, and gluten-free bread brand, gaining market share in stable categories of products that are and will continue to be bought for the foreseeable future.

{kind=link}

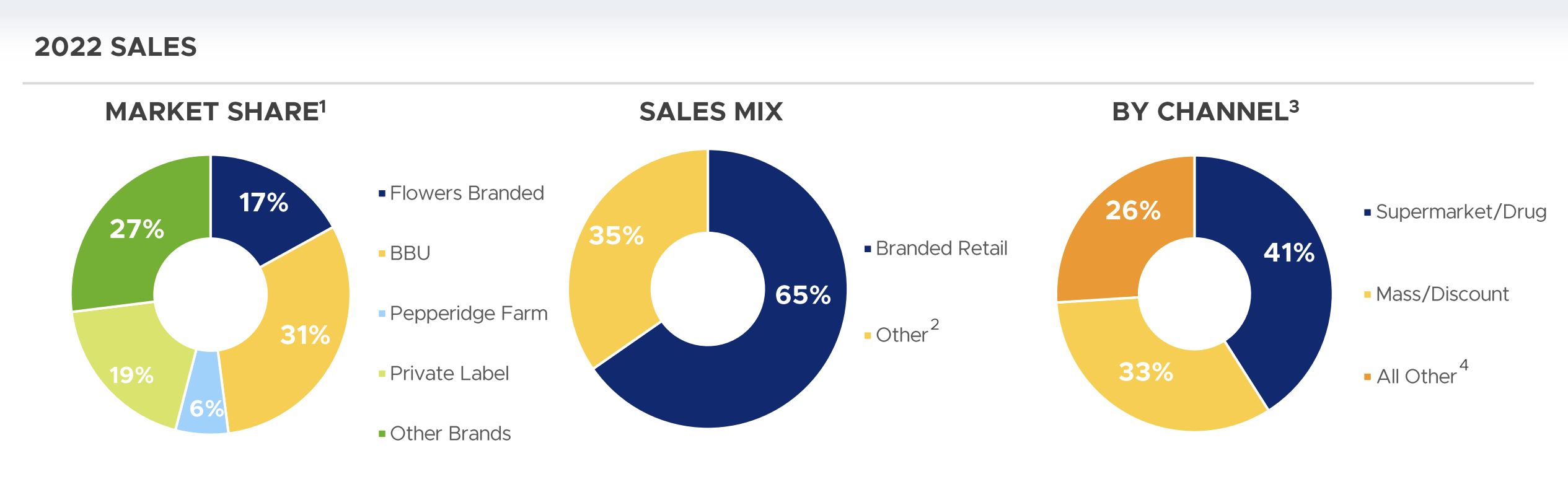

The US fresh bakery market is a retail market with $24B of annual sales. It's also one of the most profitable categories for retailers, where consumers are historically willing to pay premiums.

You need to consider that this is a category where people buy fresh bread every 12 days on average, and 98% of US households eat bread. It's also one of the few categories of products where store brands have yet to even come close to overtaking branded. As a matter of fact, the trends show the exact opposite development.

FLO IR (FLO IR)

The company has over 100 years of history under its belt, starting as a family-owned bakery in Georgia, with a public listing in 1968. It has M&A'ed, successfully, over 100 brands since that listing and now operates the second-largest baked foods company in the entire country. FLO has a proven business model with good economics, and manages over 47% gross margins in bread, with a 4-6% net margin and EBIT in the 6-9% range. These margins have declined over the past few years due to input cost increases - we can note the impact of commodity pricing shifts even in Europe, and baked goods is one of the things that has really gone up in price.

However, FLO manages a very attractive mix that I believe will manage through this crisis as well.

{kind=link}

Much like with Diageo, the company's goals are fairly modest. FLO wants a 1-2% sales growth, with a 4-6% growth in adjusted EBITDA and 7-9% in EPS. I believe this to still be on the high side for what the company may realistically achieve - but the next few years will tell.

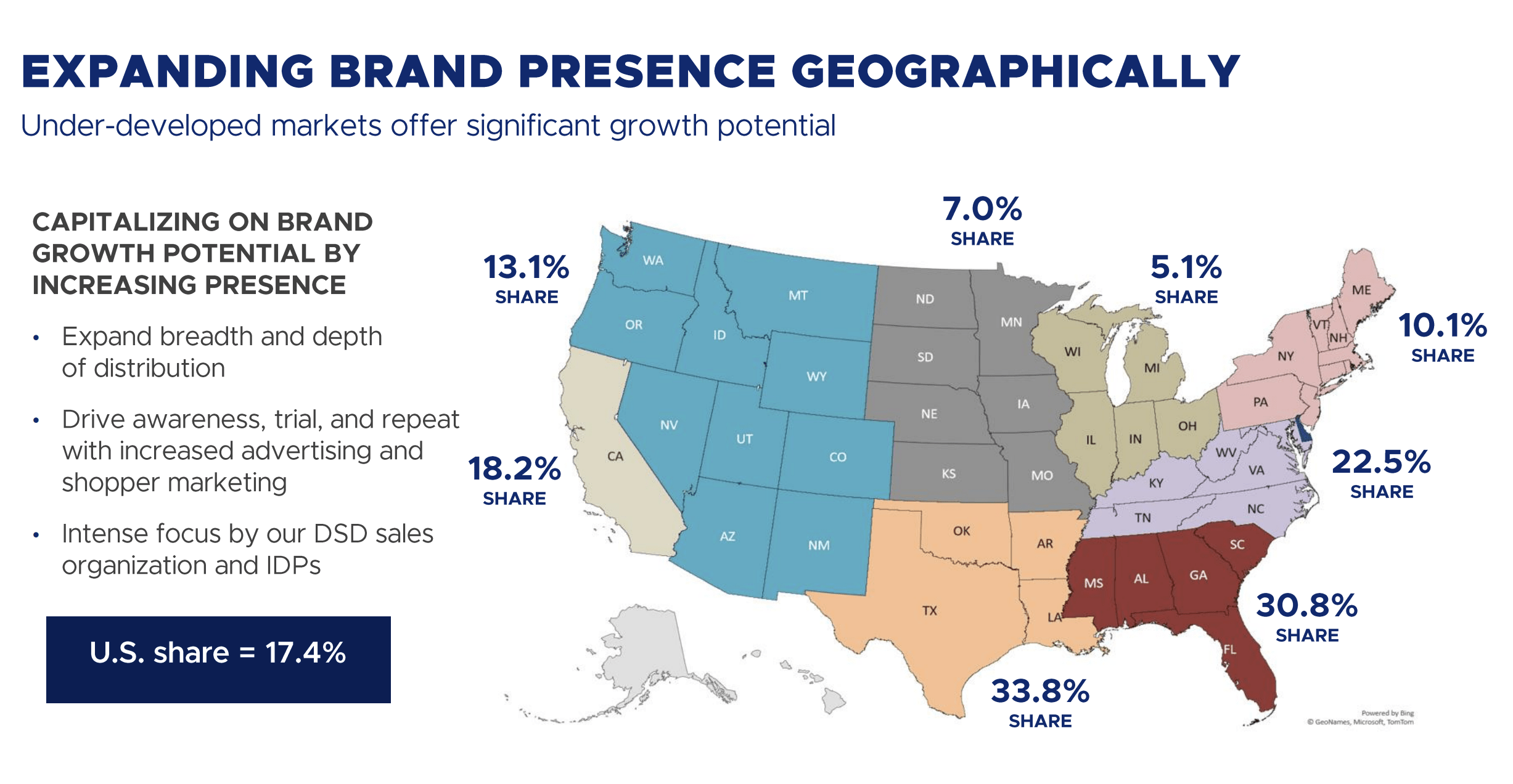

However, I personally don't forecast FLO higher than a 4-6% EPS growth rate - I believe I know the economics of this industry, and I don't foresee the commodity side of the business, namely input, improving materially to a state where a 7-9% EPS growth is possible, even for a market leader. And by the market leader, I mean that the company has 17.4% of the US market share, making it, de facto, among the market-leading companies across the nation, with over 30% in its "home states" or regions.

{kind=link}

The problem with Flowers Foods has been valuation - as you might expect. FLO typically commands a premium, and it should. A company growing at 12% per year over the past 20 should do just that. The interesting time to buy the company, on a statistical basis is below an 18.5x P/E.

That's where we currently are.

{kind=link}

This company offers you the prospect of single-digit growth from bread, in a very conservative segment, at an attractive 4.2%+ yield. The company is low in debt - under 45% of long-term to cap, has BBB, and tends to hit its targets over 80% of the time (or beat them) (Source: FactSet)

The upside here, in the case of full premiumization of FLO, is very significant. We're talking at least 20% to a P/E of 21.5x, much like DEO - but at a lower valuation and with a greater yield.

Also, there is more downside protection. The company would have to decline to below 14x P/E to really give you negative RoR here, and I don't see this happening given what the company does and the long-term profitability of the business.

FLO may not warrant full premiumization, not under the current macro. I would be hard-pressed to argue that FLO should trade at 21x P/E, even with bread, given the margin challenges the company presents.

But as a long-term investment, and forecasting the company at 18-19x?

I have no issue with that - and at 19.4x the company's upside is 15% annually. That's what I am looking for when I invest money.

Flowers Foods is a company best bought at most a fair valuation. That valuation, if you really push it, is 19-20X P/E.

I'm completely unwilling to pay more, and even if we average out future earnings until 2024E, that indicates a price of no more than $26.5/share - and that's the higher end. I'd personally prefer no more than $25/share. That's what I wrote in one of my last articles, and it's the targets that I am sticking to here.

The company is a "BUY" here.

Wrapping up

These two companies are solid businesses that I am currently buying. My focus is on undervalued, quality businesses that are likely to outperform over the next few years. I tend to take a perspective of at least 3-5 years to ensure that I'm being somewhat long-term enough for companies to develop their valuation-related upsides.

They are far from the entirety of my "BUYs" at this time, but they are companies that I myself have been adding to over the past 2 weeks, and have frequently bought shares in as they have dropped/declined.

So when someone is asking me, what he/she should be buying - I would say to take a look at these companies, specifically if they want safe consumer stocks, and see if any of them meet your requirements or pique your interest.

Because if you're anything resembling a valuation-conscious investor, then they should at the very least interest you.

Questions?

Let me know.

For further details see:

'Buy' 2 Undervalued Food And Drink Companies