MLPS - 'Buy Income' - MPLX's 9.4% Yield Is A Good Place To Start

2023-11-06 00:41:57 ET

Summary

- MLPX LP is a top-tier income stock offering a dependable 9.4% yield.

- The company reported strong third-quarter earnings, achieving record figures for adjusted EBITDA and distributable cash flow.

- MPLX's resilient business model, uncorrelated with oil and gas prices, and strategic partnership with Marathon Petroleum contribute to its stability and growth potential.

(A Lengthy) Introduction

It's time to talk about MLPX LP ( MPLX ) , which is a Master Limited Partnership offering investors the opportunity to capitalize on midstream operations in the energy sector.

Based on that, please note that the company issues a K-1 form, which may have implications for your tax situation.

Also note that when dealing with MLPs, shares are called units. Dividends are called distributions. I tend to use both. It's not technically correct, but sometimes it avoids confusion.

On October 5, I wrote an article titled 9% Yield - MPLX Is A Top Pick For Low-Stress Energy Income.

In this article, I'm going to elaborate on that, as there are two important things we need to discuss.

- The company has recently reported its 3Q23 earnings, which confirmed every bullish thing I've ever said about this company. It remains a top-tier income vehicle capable of delivering both capital gains and juicy income.

- Even Goldman Sachs and Morgan Stanley seem to agree with me that we're likely stuck in a prolonged (volatile) sideways market, pressured by poor economic growth. In that scenario, having some juicy income plays is key!

The other day, I co-wrote an article with Brad Thomas. In that article, I highlighted the need for yield, using comments and findings from the two largest investment banks in the world.

As reported by Seeking Alpha, Morgan Stanley predicts that Wall Street will see volatile trading over the next six months. As a way to deal with these issues, it highlighted dividends as a potential area of investment.

In other words, the moment markets go sideways, we can boost our total return by focusing on income (the total return equals capital gains plus income).

The bottom line is that the more investors realize that rates might stay higher for longer, the tougher it becomes to sustain lofty multiples for equities," Morgan Stanley stated. "We expect markets to remain volatile and range-bound as earnings and valuations battle for dominance over the next six months." - Via Seeking Alpha.

While I'm not necessarily bearish, I have advocated since last year that we'll likely see a volatile sideways trend between the mid-4,000 and the mid-to-high 3,000 points range in the S&P 500.

So far, that's what's happening.

Although the U.S. is not in a recession, growth is slowing down rapidly, fueled by very poor consumer sentiment and the belief that the Fed will have to keep rates elevated to combat sticky inflation.

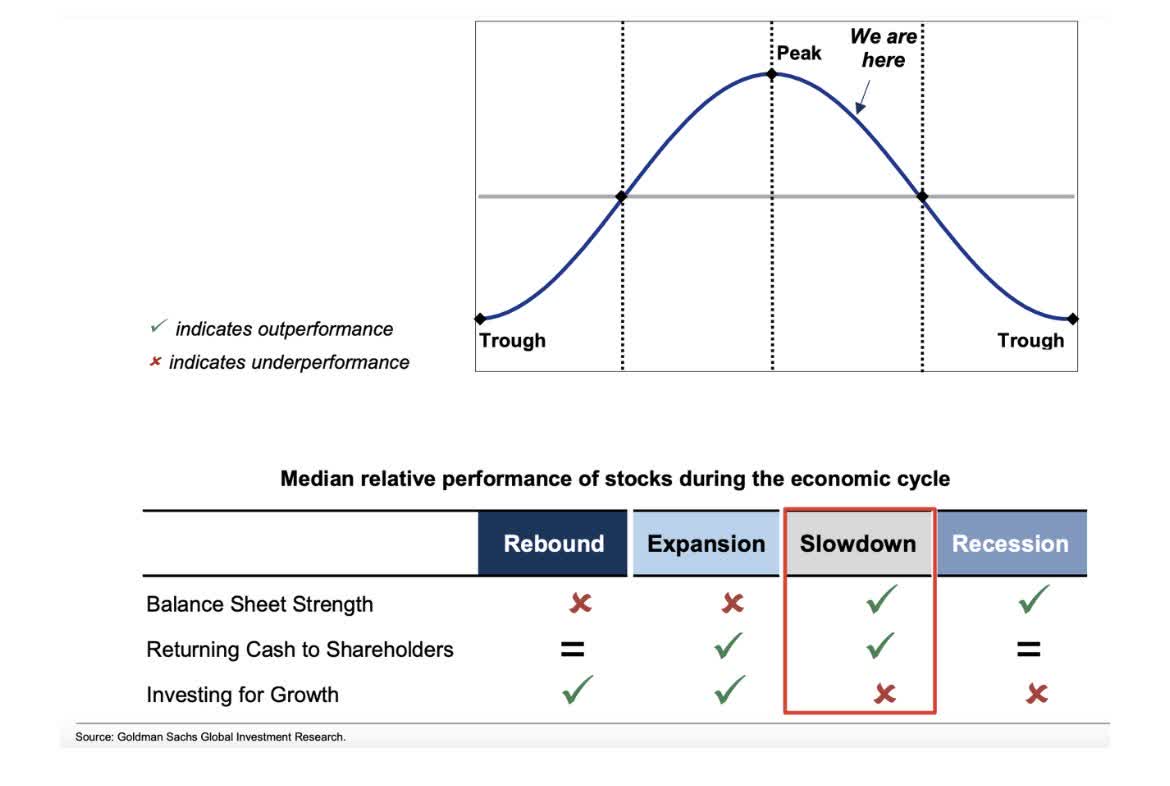

That's also what Goldman Sachs believes. Just like Morgan Stanley, it highlights the need for income using the chart below.

- It believes the economy is in a downtrend.

- This would warrant a focus on companies with healthy balance sheets (especially given elevated rates!).

- It also warrants a focus on companies that return cash to shareholders instead of companies that invest in growth. If the bank is right and we see weaker economic growth, companies may better hold off on massive CapEx projects. Needless to say, there are many exceptions. This is bigger-picture stuff.

{kind=link}

With this in mind, I do like midstream companies a lot.

Midstream companies are not correlated to the price of oil and gas. They do NOT produce oil and gas. They use pipelines and related infrastructure to store and move it from buyers to sellers. This includes by-products like gasoline, diesel, and so much more.

Since the pandemic, the industry has changed. Most companies are now free cash flow positive, meaning they have mature infrastructure and are able to somewhat dial down billions in annual spending.

While most midstream companies are more volatile than non-energy dividend stocks, the risks tied to buying elevated income have declined considerably, making some midstream companies great income tools - even in this environment.

That's where MPLX comes in, which just released its quarterly earnings.

MPLX Is A Top-Tier Income Stock

I like MLPX. In fact, I like all companies tied to Marathon Oil ( MRO ).

- Marathon Oil is a highly efficient driller that uses its free cash flow to buy back stock.

- Marathon Petroleum ( MPC ) is MLPX's largest customer. It's also its largest unitholder.

MPLX operates two major segments.

-

Logistics and Storage (L&S): This segment focuses on the gathering, transportation, storage, and distribution of hydrocarbon-based products. In 2022, roughly 88% of L&S segment revenues were generated from MPC.

-

Gathering and Processing (G&P): Operations in this segment involve gathering, processing, and transportation of natural gas, along with transportation, fractionation, storage, and marketing of NGLs.

Going back to MPC, the company not only accounts for 88% of L&S segment revenues, but it also accounts for 47% of MPLX's total revenues and owns 65% of the company and general partner shares.

MPLX LP

Having said that, according to MPLX, it is considered a strategic investment for MPC. MPC anticipates receiving $2.2 billion in annual cash flows through the distribution.

MPC does not plan to "roll up" MPLX, indicating that MPLX will continue to operate as a separate entity.

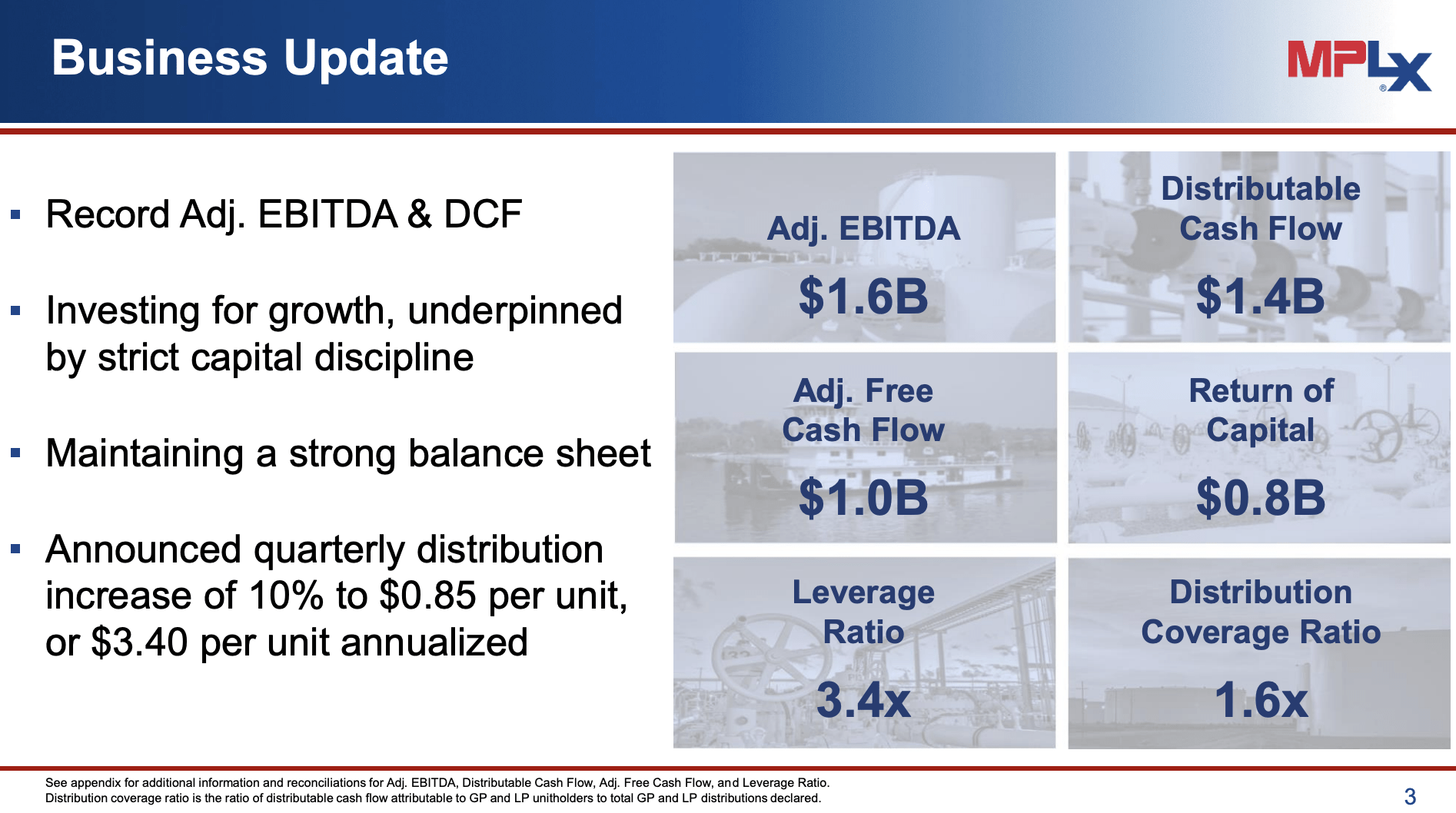

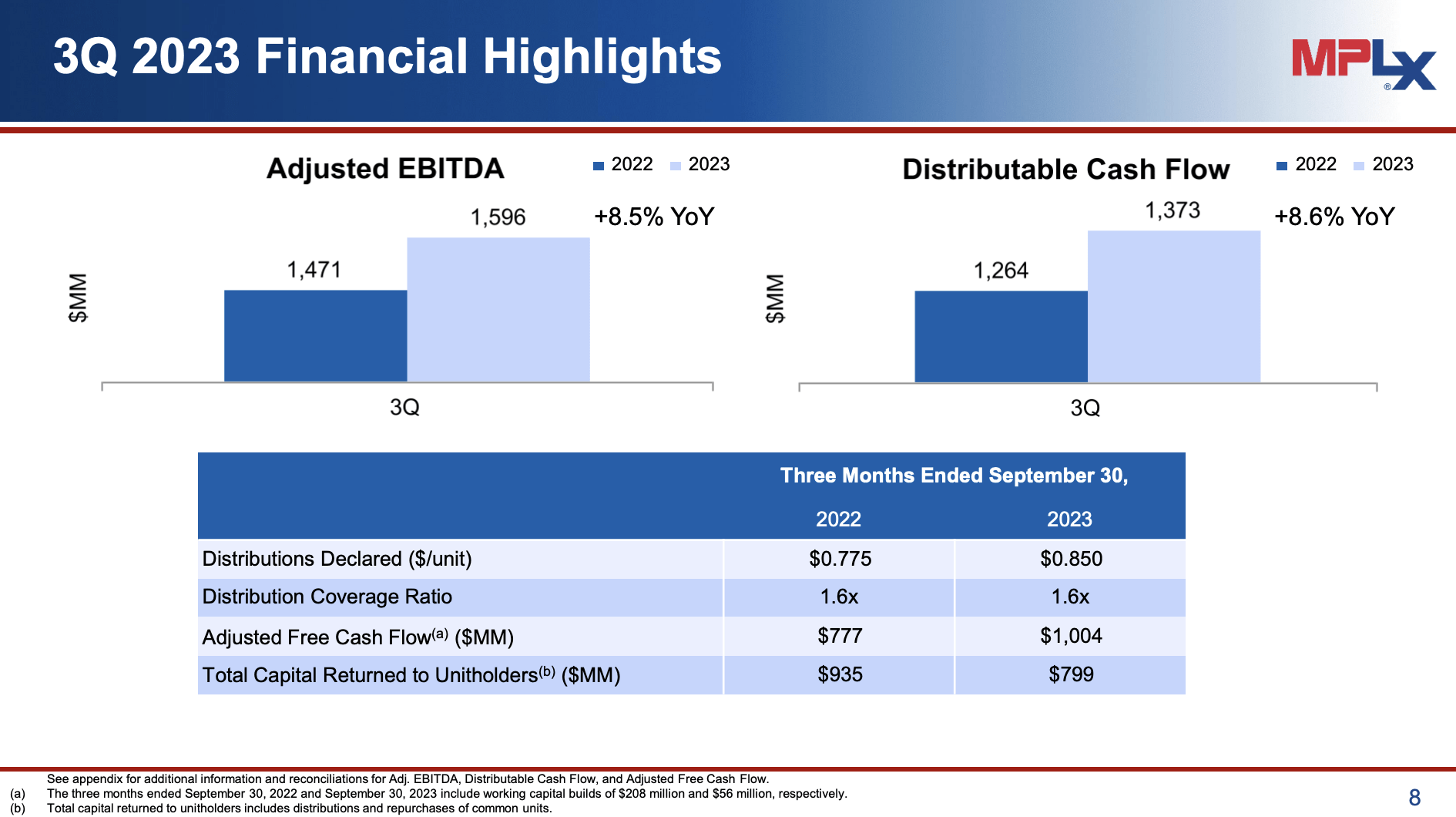

With that in mind, the company just reported its third-quarter earnings, which tells us a lot about the state of this midstream giant.

They achieved an adjusted EBITDA of $1.6 billion and distributable cash flow of $1.4 billion, both of which set new quarterly records.

{kind=link}

These figures represent an impressive year-over-year increase of over 8%.

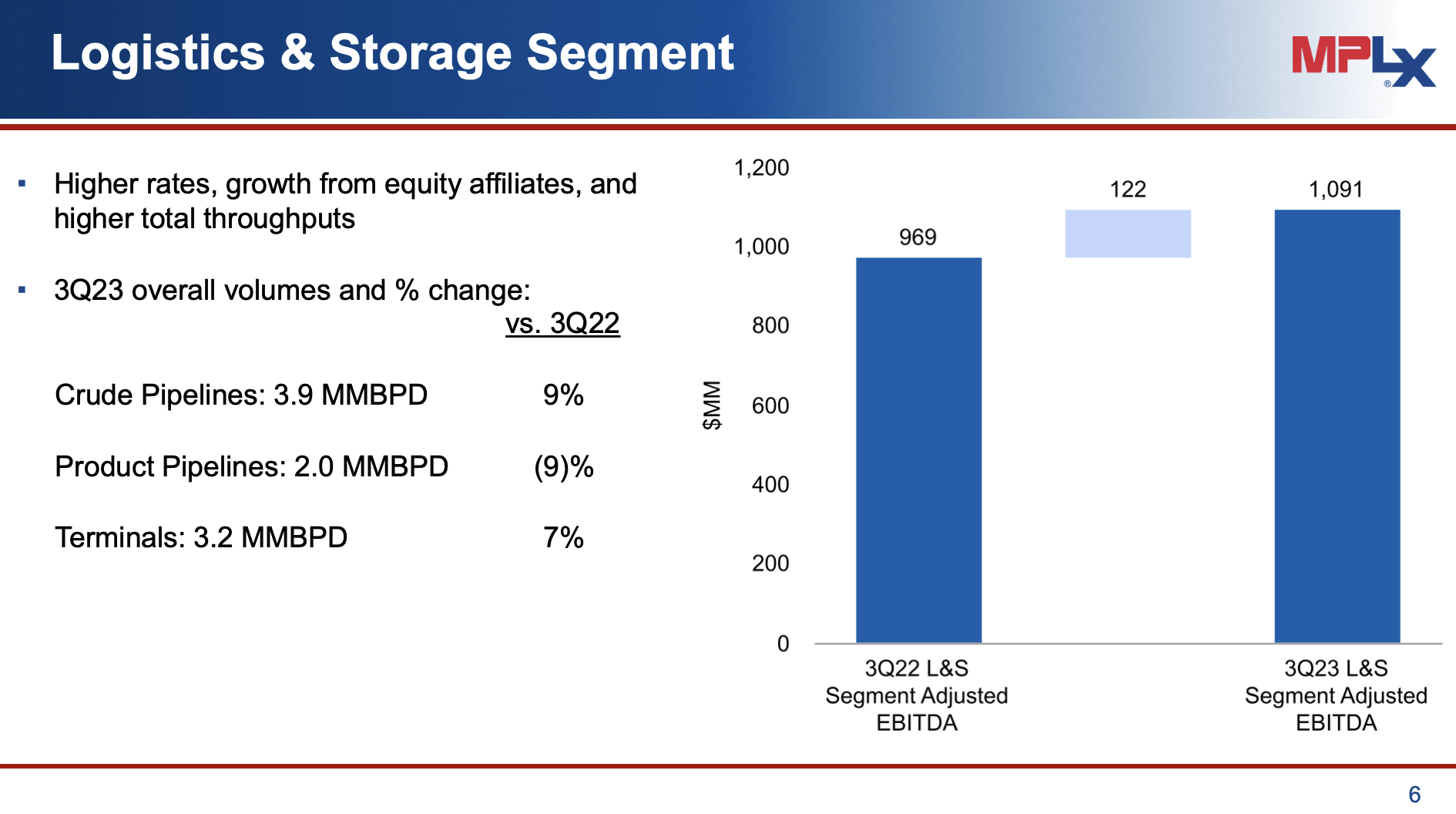

In the L&S segment , MPLX is involved in several projects. For example, the expansion of the Whistler natural gas pipeline to 2.5 billion cubic feet per day was successfully completed in the third quarter of 2023.

According to the company, there is significant demand for this pipeline.

Additionally, construction is progressing on the Agua Dulce to Corpus Christi pipeline lateral, expected to be operational in the third quarter of 2024.

The company is also actively participating in the NGL value chain by expanding the BANGL pipeline to accommodate 200,000 barrels per day, with completion expected in the first half of 2025.

{kind=link}

Furthermore, as we can see in the chart above:

- Crude pipeline volumes reached a new quarterly record, increasing by 9%, with growth driven by expansion and debottlenecking activities.

- Product pipeline volumes decreased by 9%, influenced by market dynamics and the effects of Marathon's refinery downtime.

- Terminal volumes increased by 7% due to higher customer demand. However, MPLX anticipates some headwinds in the fourth quarter, with lower throughput volumes resulting from MPC's planned turnaround activity and higher operating expenses due to the timing of maintenance projects.

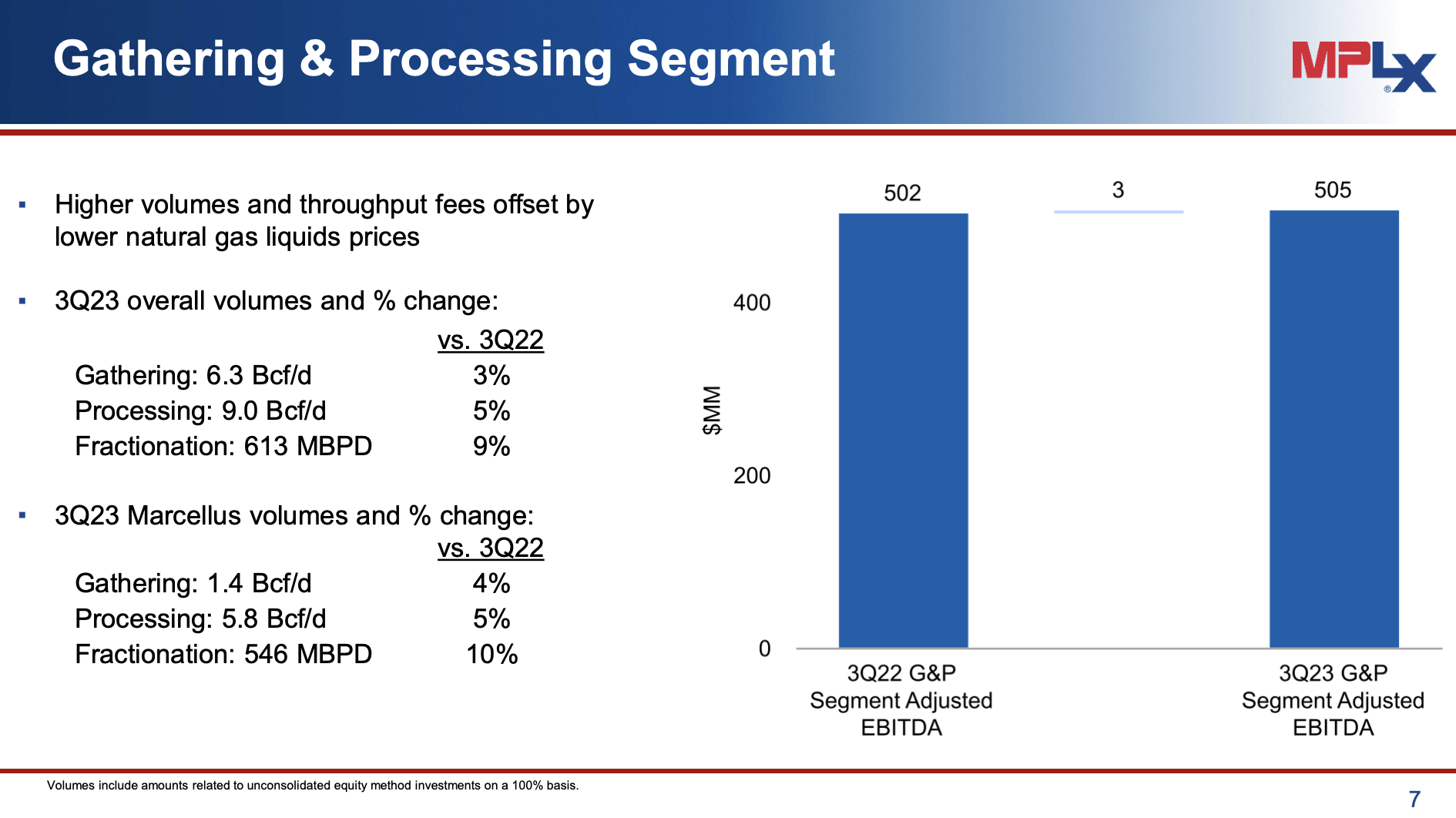

In the G&P segment , MPLX continues to invest in the Permian and Marcellus basins to meet producer demand.

New gas processing plants are being brought online in the Permian Delaware Basin, with the Preakness II plant expected to be operational in the first half of 2024.

Additionally, the company announced the construction of a seventh gas processing plant, Secretariat, anticipated to be online in the second half of 2025.

These plants will increase the total processing capacity in the Delaware Basin to 1.4 billion cubic feet per day.

{kind=link}

Thanks to a strong performance in the third quarter, MPLX announced a 10% increase in its distribution - for the second year in a row!

The annualized distribution now stands at $3.40 per unit, which, according to the company, reflects its commitment to returning capital to unitholders.

This payout translates to a 9.4% yield!

Furthermore, the distribution is expected to be the primary tool for returning capital to investors, supplemented with opportunistic repurchases.

Adding to that, thanks to its strong financials, the dividend is protected by a 1.6x coverage ratio!

So, even more severe economic headwinds won't likely result in a dividend cut. The company has never cut its dividend in the past.

{kind=link}

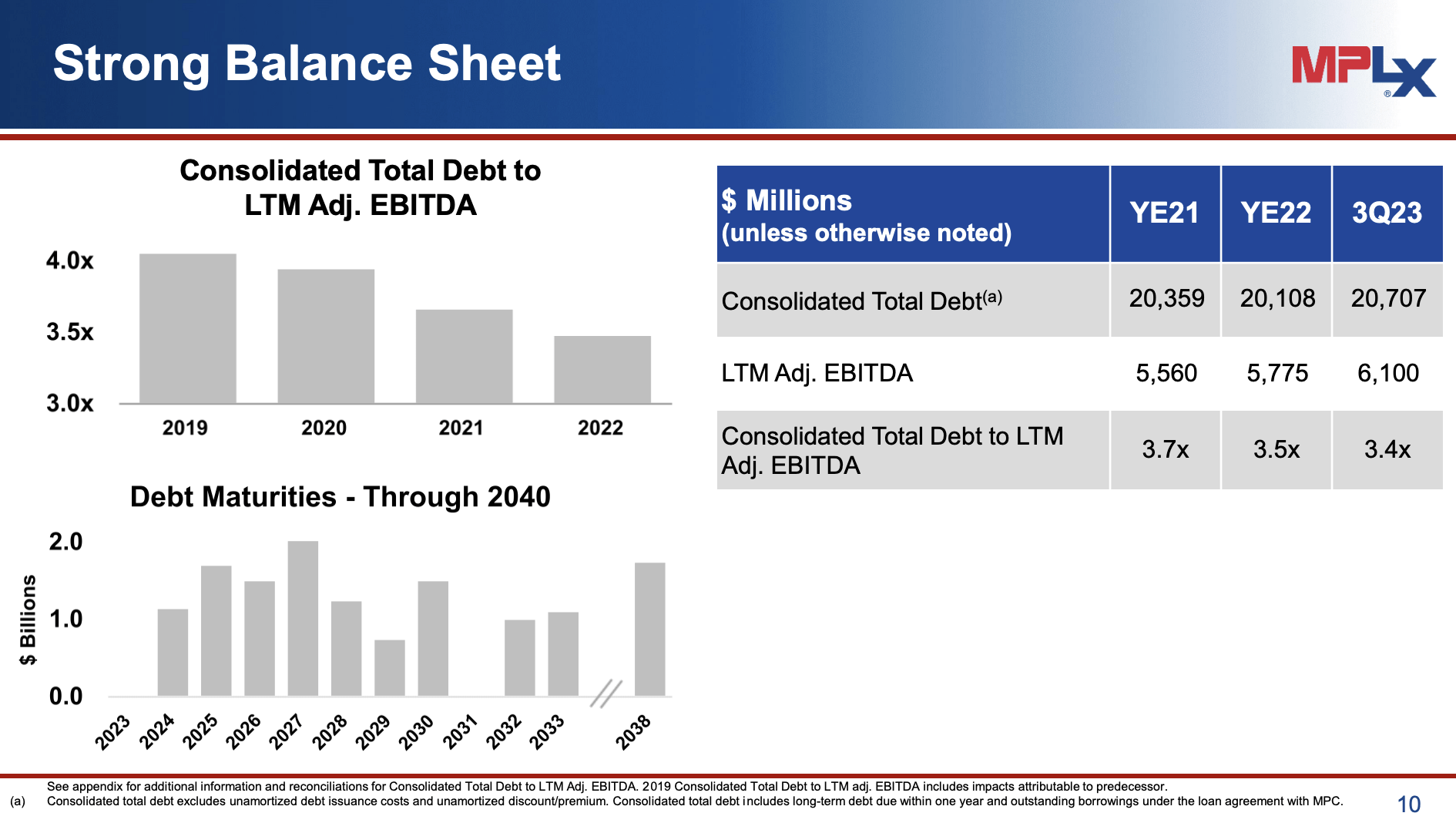

It also comes with a healthy balance sheet, which is just as important when it comes to dividend safety.

MPLX maintains a strong balance sheet, including a quarter-end cash balance of $960 million and a leverage ratio of 3.4x (EBITDA).

It has no debt maturities this year.

According to its management, this financial strength provides the company with the flexibility to optimize its capital allocation and support its growth initiatives. I cannot disagree with that.

{kind=link}

So, what about the valuation?

Valuation

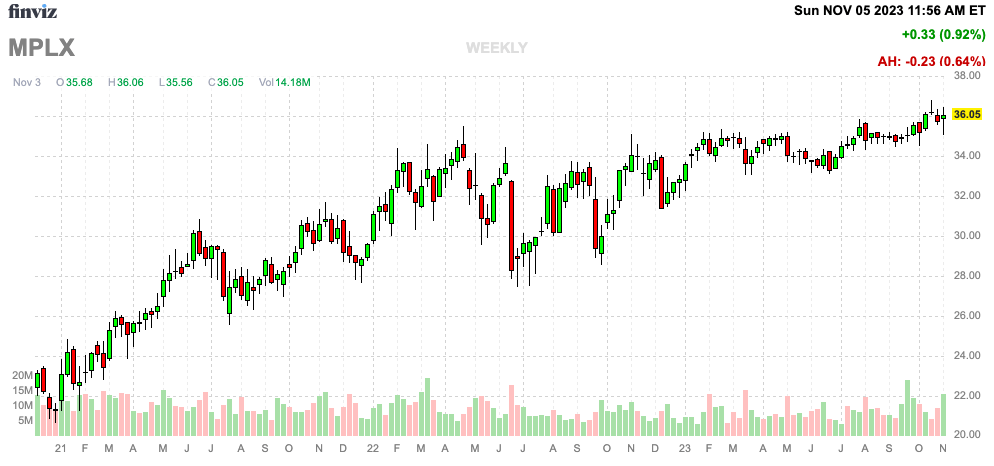

So far, MPLX has done a stellar job ignoring market weakness. The stock is trading just 2% below its 52-week high. MPLX is up 10% year-to-date.

{kind=link}

Yet, it still has a great valuation.

Using the chart below, we see a number of important things that indicate an attractive risk/reward.

- MPLX is trading at a blended price-to-operating cash flow ratio of 6.9x.

- The long-term normalized multiple is 8.2x OCF.

- After potentially growing OCF by 6% this year, analysts expect 3% growth in 2024, followed by 9% contraction in 2025 (I think that number will be much better than expected).

- Based on these expectations, the company could, technically speaking, return 15.4% through 2025. This includes a return to its normalized valuation, expected growth rates, and its dividend. After all, its dividend is a big part of the total return.

{kind=link}

As I always say, this is a theoretical return. While economic challenges could result in lower returns, it does show that the risk/reward is attractive.

Hence, my rating remains a Buy rating.

I believe MPLX is a fantastic income stock for long-term investors - especially if the capital gains component of the S&P 500's total return turns out to be disappointing.

MPLX has a strong business, growth opportunities, a healthy balance sheet, and a well-covered dividend with a yield close to 10%.

Takeaway

In a market characterized by volatility and uncertainty, MPLX shines as a top-tier income stock. The recent third-quarter earnings report confirms its robust position as a lucrative investment.

With economic challenges looming and the need for income becoming increasingly essential, MPLX offers a dependable 9.4% yield.

Moreover, the company's dividend is well-protected, backed by a 1.6x coverage ratio and a track record of no previous cuts.

MPLX's strength lies not only in its attractive yield but also in its resilient business model.

As a midstream operator, it remains uncorrelated with oil and gas prices, focusing on the transportation and storage of energy products. The company's strategic partnership with Marathon Petroleum adds further stability to its income potential.

With impressive 3Q23 numbers, ongoing projects, and financial strength, MPLX is poised for sustainable growth. Its valuation and potential return on investment make it an appealing choice for long-term investors, especially in a sideways market.

For further details see:

'Buy Income' - MPLX's 9.4% Yield Is A Good Place To Start