SPDN - 'Mild' Recession Is Code For 'Not Mild' Recession

2023-04-20 20:54:13 ET

Summary

- The Fed says we will have a mild recession.

- Credit conditions are tightening just when the U.S. consumer needs credit the most in a decade.

- Recessionary trends are hinting at something bigger than mild.

- The last time the Fed said the recession will be mild, it was the worst in 100 years.

The Federal Open Market Committee noted in their March meeting minutes that they now expect the U.S. to experience a "mild" recession later this year. This is what they stated (bold added):

Given their assessment of the potential economic effects of the recent banking-sector developments, the staff's projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.

This is the first time the Fed has openly stated that they expect recession since 2020. After the recent failure of SVB, Fed officials lowered their expectations for remaining rate hikes. Since then, inflation and employment data have remained strong, prompting some officials, including James Bullard , to predict the Fed Funds rate should be as high as 5.75%.

We believe that the Federal Reserve has a consistent history of underestimating bad news in an attempt to control market psychology. When we hear the Fed say that a "mild" recession is to be expected, we take confidence in our belief that the recession will be more than mild. We think the data supports this viewpoint.

Credit is Getting Tight

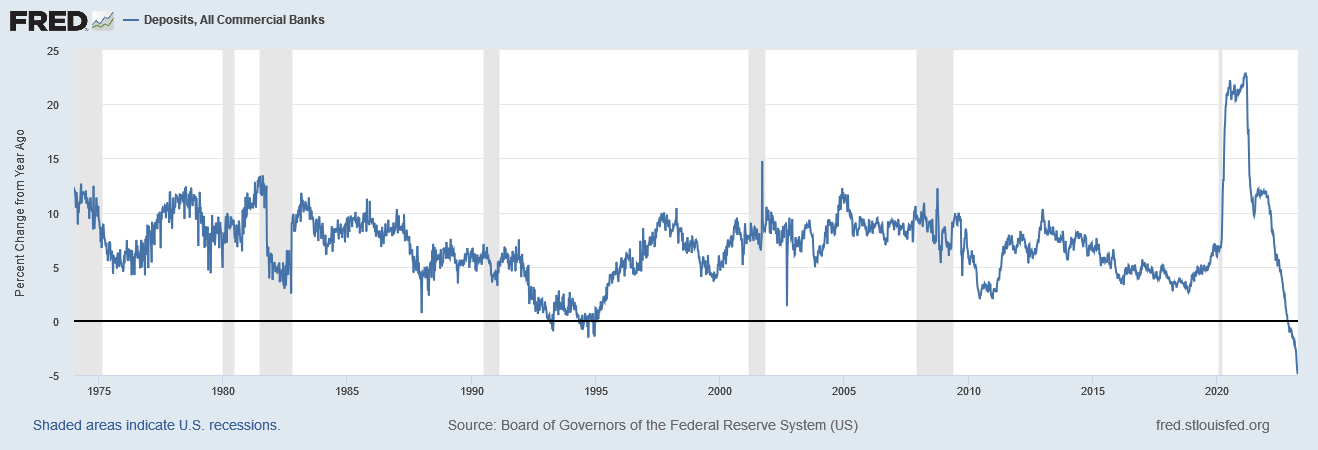

The banking crisis was accelerated by a flight of bank deposits. This is due to the fact that depositors can earn higher interest rates in money markets and treasury bills than in savings accounts. This flight of deposits is pressuring the banking system and causing issues with liquidity.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

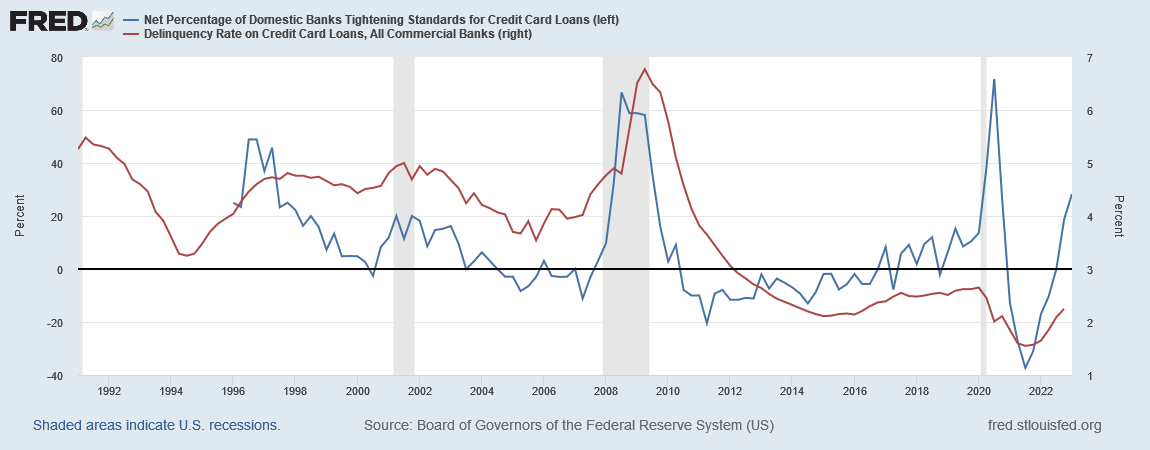

As a result, banks are expected to tighten lending standards even further. Prior to the crisis, lending standards had already been tightening. The extent of lending tightening is now at levels on par with those experienced during previous serious recessions. Credit card delinquency rates remain historically low at 2.25%, however, the trend is concerning. Lending standards tend to correlate with delinquency rates. Current lending standards suggest that higher delinquency rates are expected, perhaps as high as 4% in the coming quarters.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

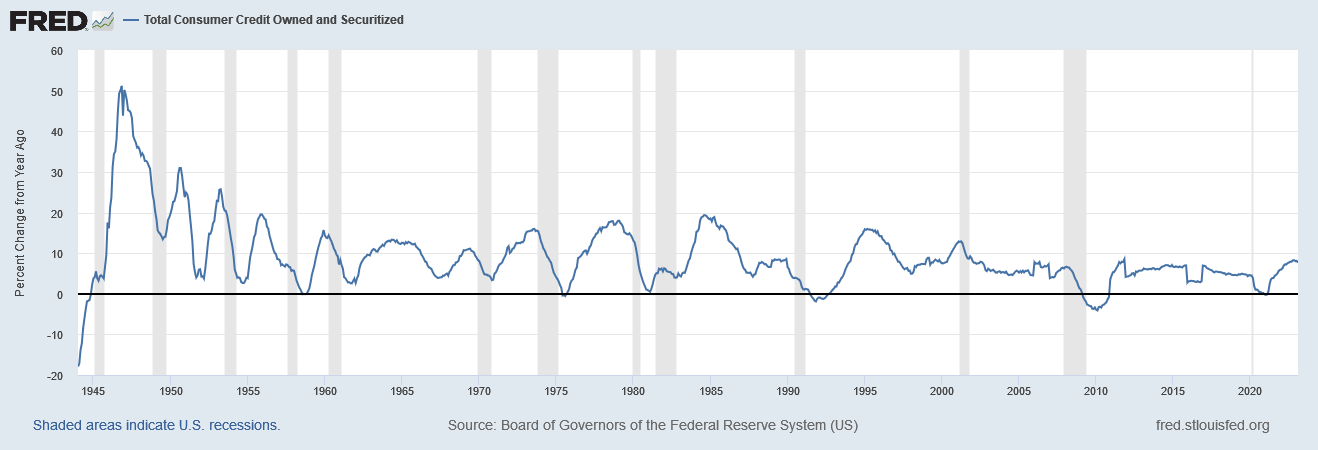

The overall trend in consumer credit is concerning. The YoY change in consumer credit has risen quickly in 2022-2023 to the highest level since 2011. Consumer credit outstanding tends to rise in advance of recession and the momentum of credit growth slows before the onset of recession. Current credit momentum growth is slowing considerably and could turn lower in the immediate future.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

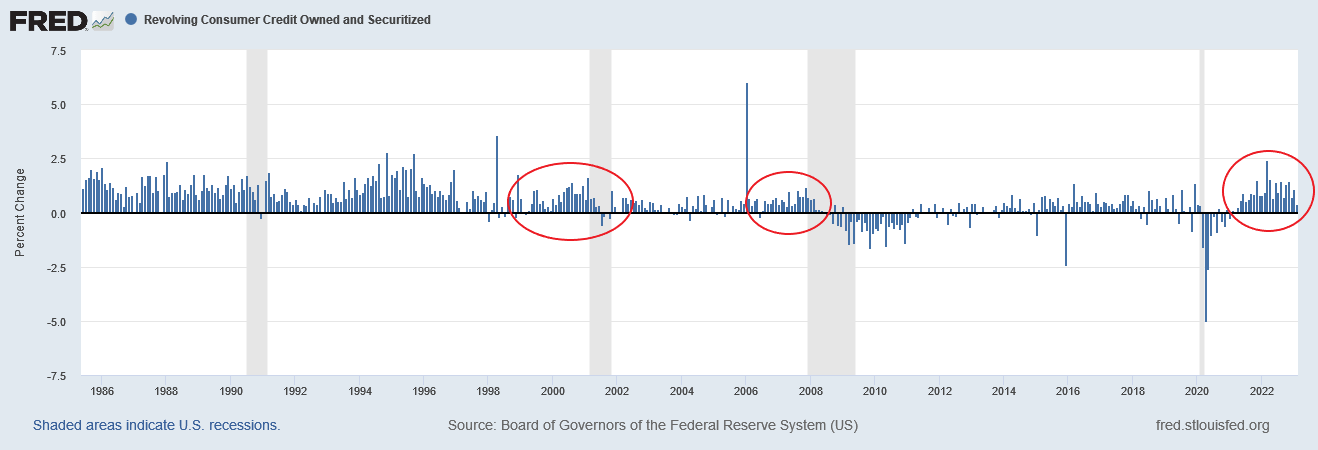

Similarly, consumer revolving credit surged higher prior to the last two major recessions of 2001 and 2008. Nominal revolving credit has surged significantly higher in 2022-23.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

Credit card debt as a ratio of median income is in-line with the last decade. Many interpret this as simply a return to trend. While that could be the case, we often witness that a return to trend from a strong deviation, such as the one we experienced in 2020, often results in the "slingshot" move past the trend in the opposite direction before reaching equilibrium. What is more significant, by our assessment, is the rate of change for credit card debt. The current rate of growth of credit card debt in the U.S. is among the highest since 2000. This consumer behavior is not a sign of financial health.

Recession Warnings are Getting Louder

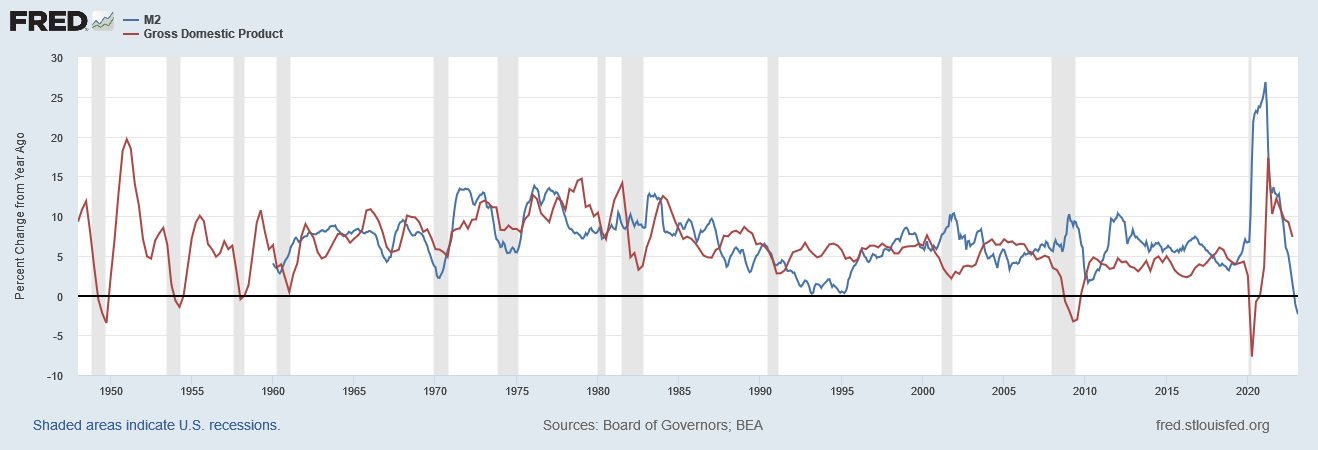

In rare form, M2 money stock growth in the U.S. has become negative. It is the most negative since 1960. This is not surprising, given the dramatic rise in M2 money stock in 2020-2021. Again, it aligns with our expectation that significant deviations from trend often result in over-correction. Changes in M2 have a moderate correlation with GDP. Through the 1970s, changes in M2 were closely mirrored by changes in GDP. During the significant recessions of 2001, 2008, and 2020, M2 and GDP diverged as monetary stimulus was used to turn the business cycle. The surge in M2 after the 2020 recession is reflected in GDP growth with 6-12 months of delay. M2 money stock growth became negative in December 2022. If this correlation holds, we expect that GDP may reach 1-2% by the end of 2023.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

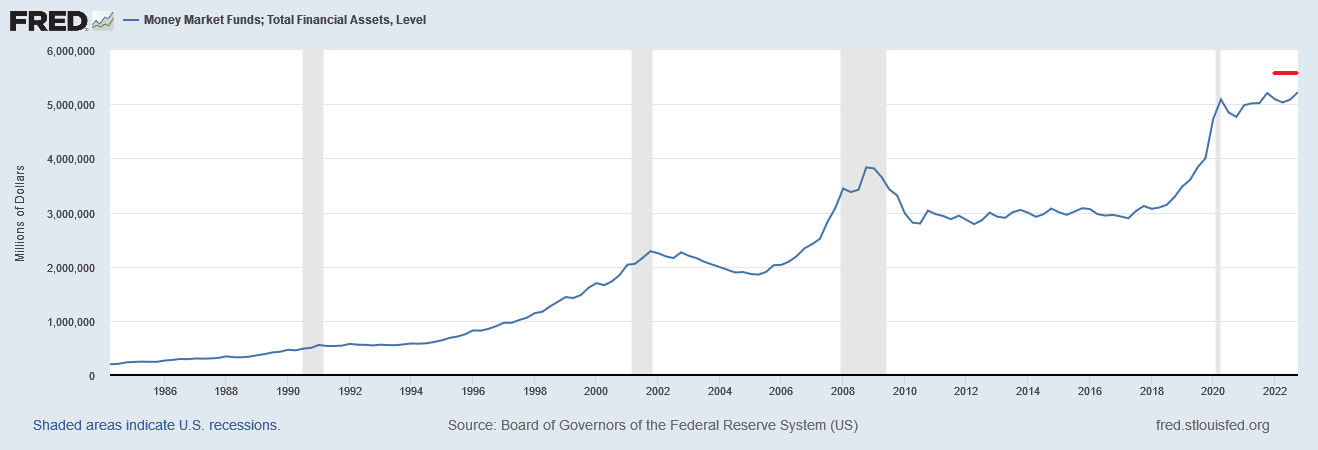

Money market funds have increased dramatically in the wake of the banking crisis. By the end of March 2023, money market funds were expected to reach $5.5 trillion as symbolized by the red line on the chart below.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

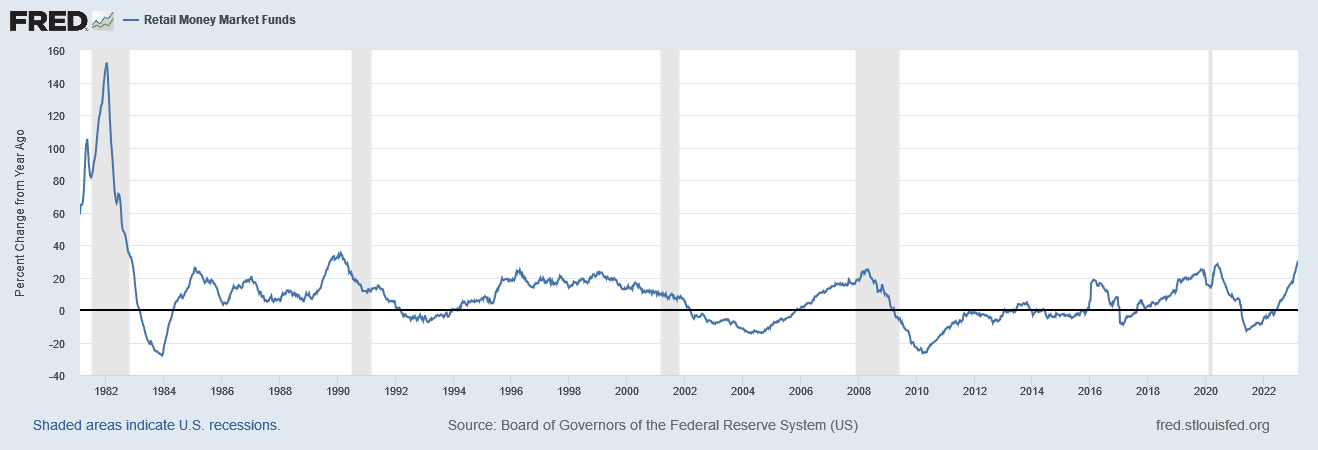

Likewise, retail money market funds have been growing rapidly. The year over year rate of increase is the highest since 2008. Institutions and individuals tend to raise their money market allocations during periods of uncertainty. This also correlates with the business and rate hiking cycle which incentivizes fixed income assets. Together, these trends indicate that the effectiveness of rate hikes and fear by market participants is nearly on par with the circumstances that precede serious recessions of the past.

{kind=link}

Federal Reserve Economic Data | FRED | St. Louis Fed

The Conference Board Leading Economic Index ((LEI)) considers significant leading economic indicators to create an aggregate measure of economic cycle activity. The LEI is expected to lead changes in the business cycle by about 7 months. The LEI reached a 6-month annualized growth rate of -9.0% in March 2023. The last three times the LEI was this weak was during the recessions of 2001, 2008, and 2020.

Summary

The Fed has finally admitted that recession is probable, only after economic data is convincing. We have been on recession watch for the last 12 months based on our research. For now, the Fed is calling the potential recession "mild." Interestingly, Fed officials continue to talk about further rate hikes. If recession is expected, it would likely be prudent to pause hiking rates given the prolonged lag that policy changes endure before their effects are fully experienced.

The data speaks for itself. If we are headed toward recession (and it appears we are) this recession is not on the "mild" trajectory. Moreover, a continuation of monetary tightening into a "mild" recession will have increasing odds of pushing into the "serious" category. Our concluding thought is that of the last "mild" recession experienced in the U.S. This recession was so characterized by Fed Chairman Bernanke in April 2008, mere months after the start of the "Great" Recession. By September 2008, Bernanke upgraded his assessment to "deep and extensive."

They say mild.

We say not.

What do you think? Leave a comment.

For further details see:

'Mild' Recession Is Code For 'Not Mild' Recession