NYMTZ - 'Soft Landing' Hopes Revived

Summary

- U.S. equity markets extended a two-week rebound since hitting two-year lows earlier this month as a mixed slate of corporate earnings reports and lukewarm economic data revived "soft landing" hopes.

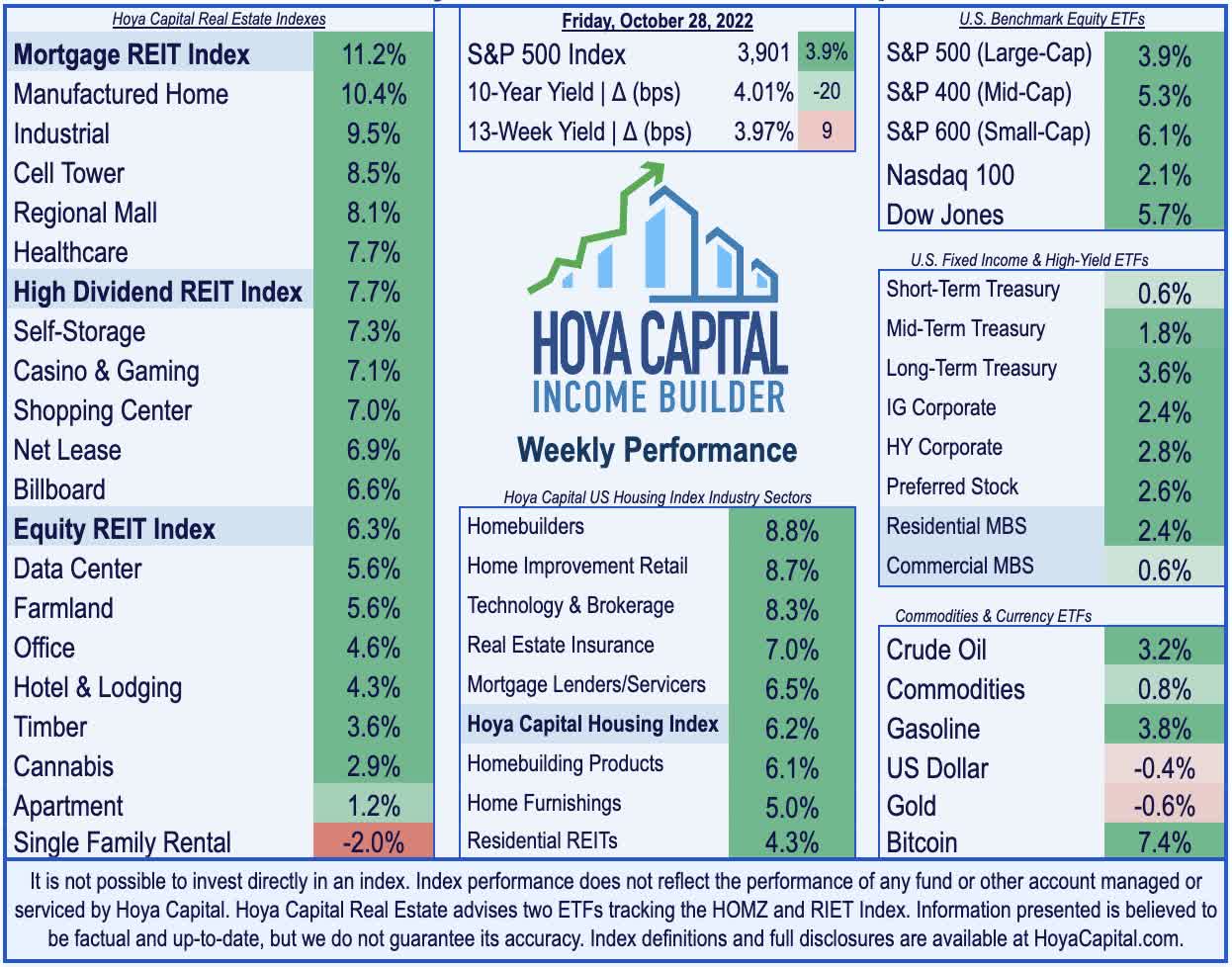

- Posting its strongest two-week advance since the initial COVID vaccine rollout in November 2020, the S&P 500 advanced 3.9% this week, pushing its rebound to over 9% since October 12th.

- Powered by a strong slate of earnings reports and another wave of dividend hikes, the Equity REIT Index rallied more than 6% on the week while Mortgage REITs soared 10%.

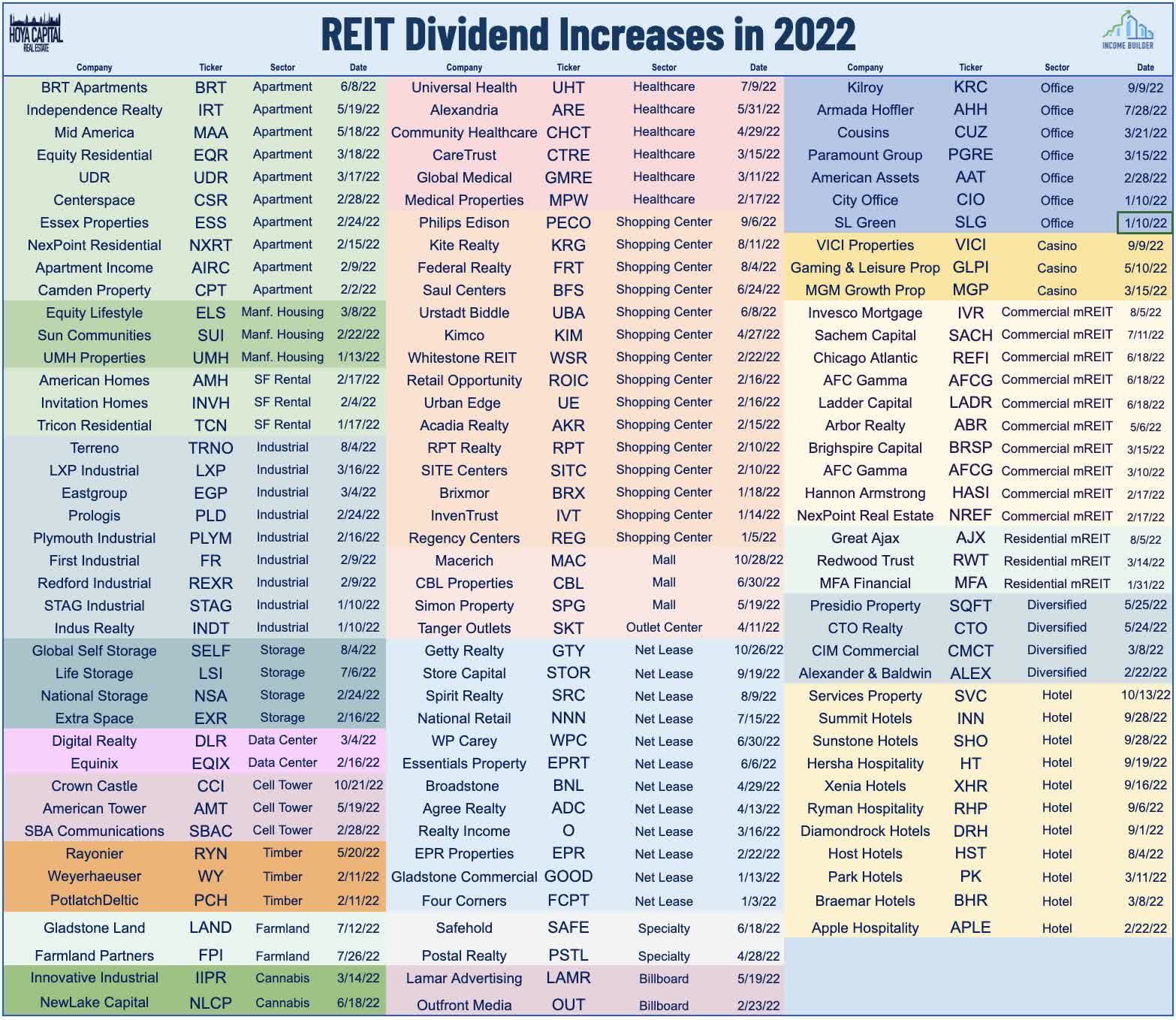

- Another week, another wave of REIT dividend hikes. A half-dozen REITs announced dividend increases this past week, pushing the full-year total to 120 - a new record-high quantity of REIT dividend hikes - including Kimco, Macerich, Getty, and NexPoint Residential.

- Hospital owner Medical Properties Trust - one of the most heavily-shorted REITs - rallied more than 13% on the week after raising its full-year FFO growth target. More than two-thirds of REITs have raised their outlook this quarter - well above the broader S&P 500 average of less than 50%.

Real Estate Weekly Outlook

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on October 28th.

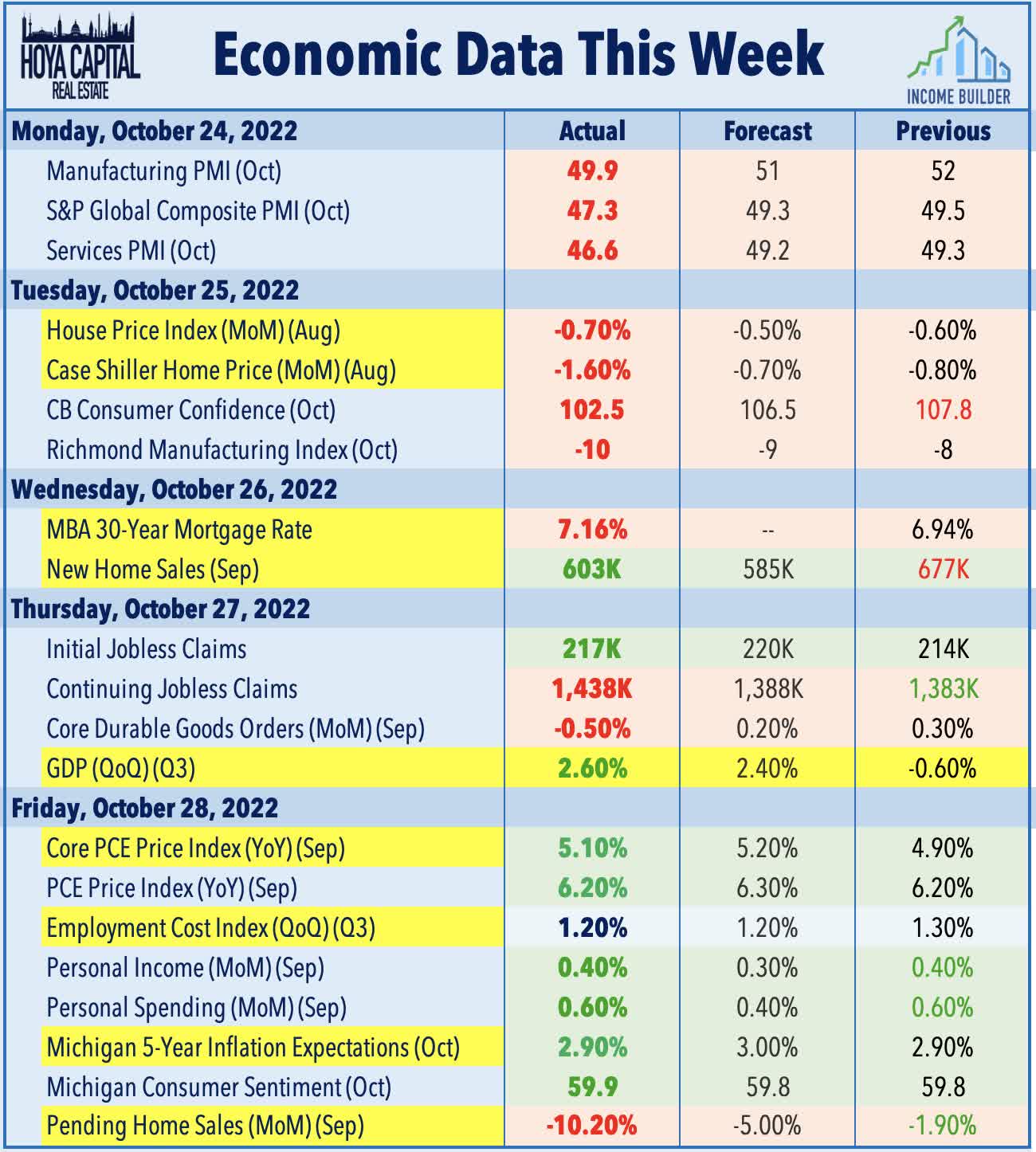

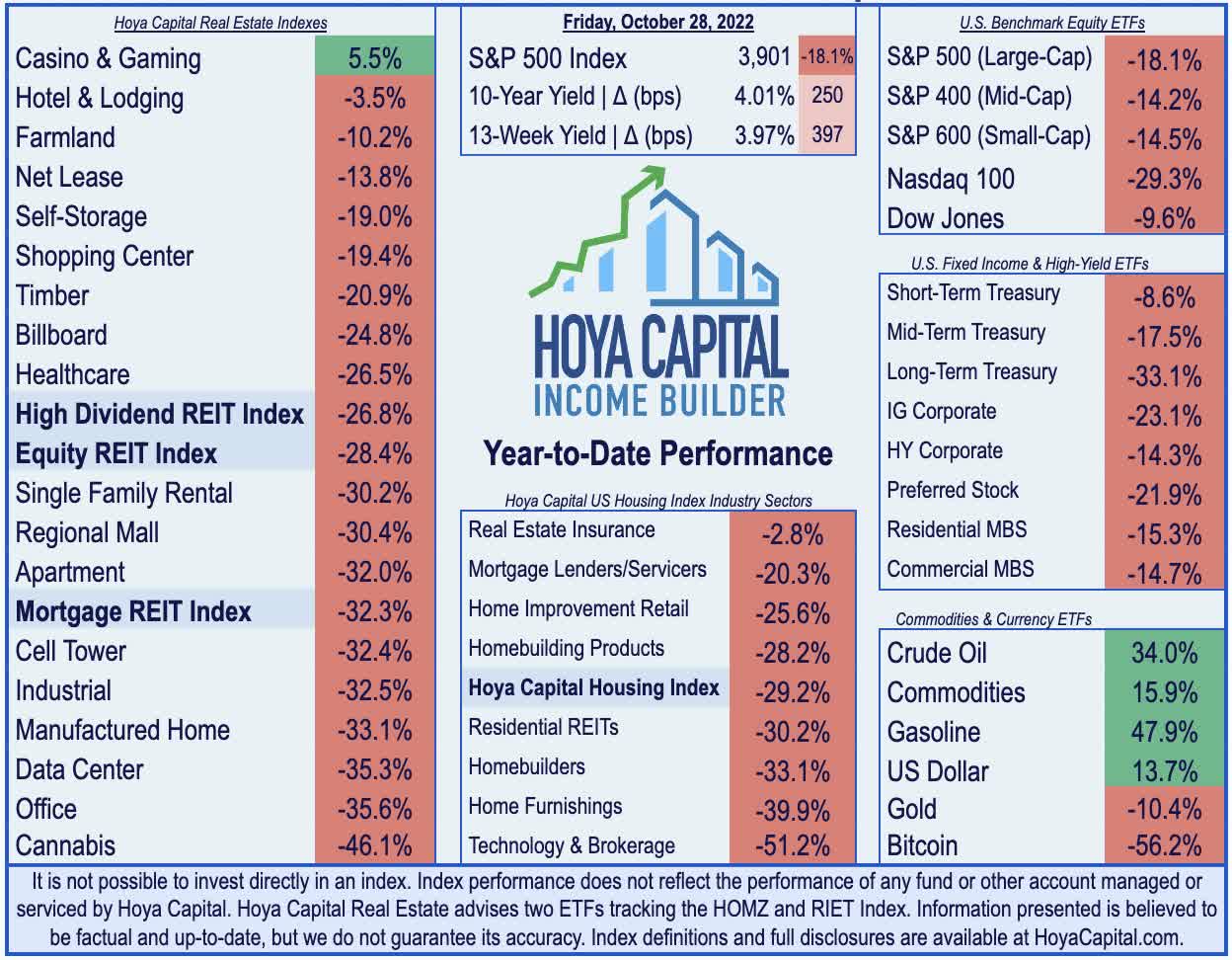

U.S. equity markets gained for a second-straight week - extending a rebound since hitting two-year lows earlier this month - as a mixed slate of corporate earnings reports, lukewarm economic data, and a weakening growth outlook in international markets raised hopes of a "soft landing" for the U.S. economy. Ahead of the FOMC rate decision in the week ahead, interest rates moderated from multi-decade highs on data showing the steepest one-month decline in home prices in over a decade while international political developments pointed towards a further downshift of growth and inflationary pressures.

{kind=link}

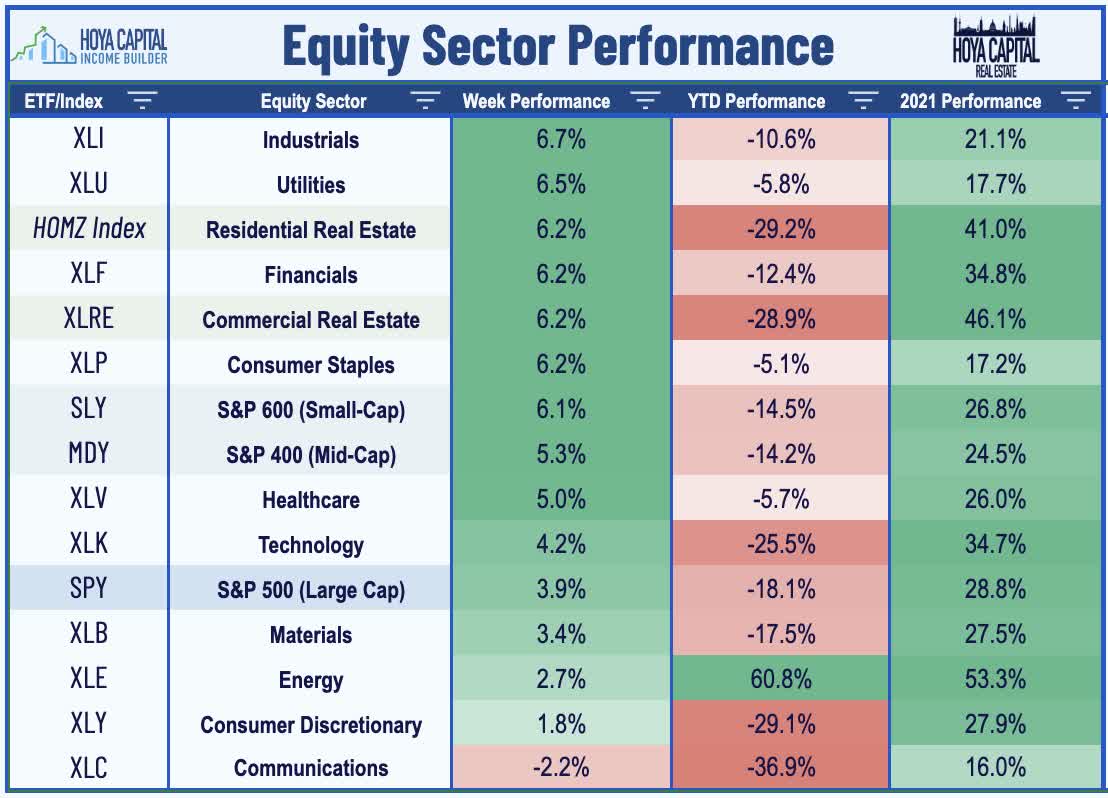

Posting its strongest two-week advance since the initial COVID vaccine rollout in November 2020, the S&P 500 advanced 3.9% on the week, pushing its rebound to over 9% since October 12. Perhaps even more impressive, the gains came despite a drag from mega-cap technology stocks with the Nasdaq 100 higher by just 2.1% on the week. The more domestic-focused Mid-Cap 400 and Small-Cap 600 led the charge this week with gains of over 5% and 6%, respectively. Powered by a strong slate of earnings reports and another wave of dividend hikes, the Equity REIT Index rallied more than 6% on the week with 17-of-18 property sectors in positive territory - the best week since November 2020 - while the Mortgage REIT Index soared more than 10%.

{kind=link}

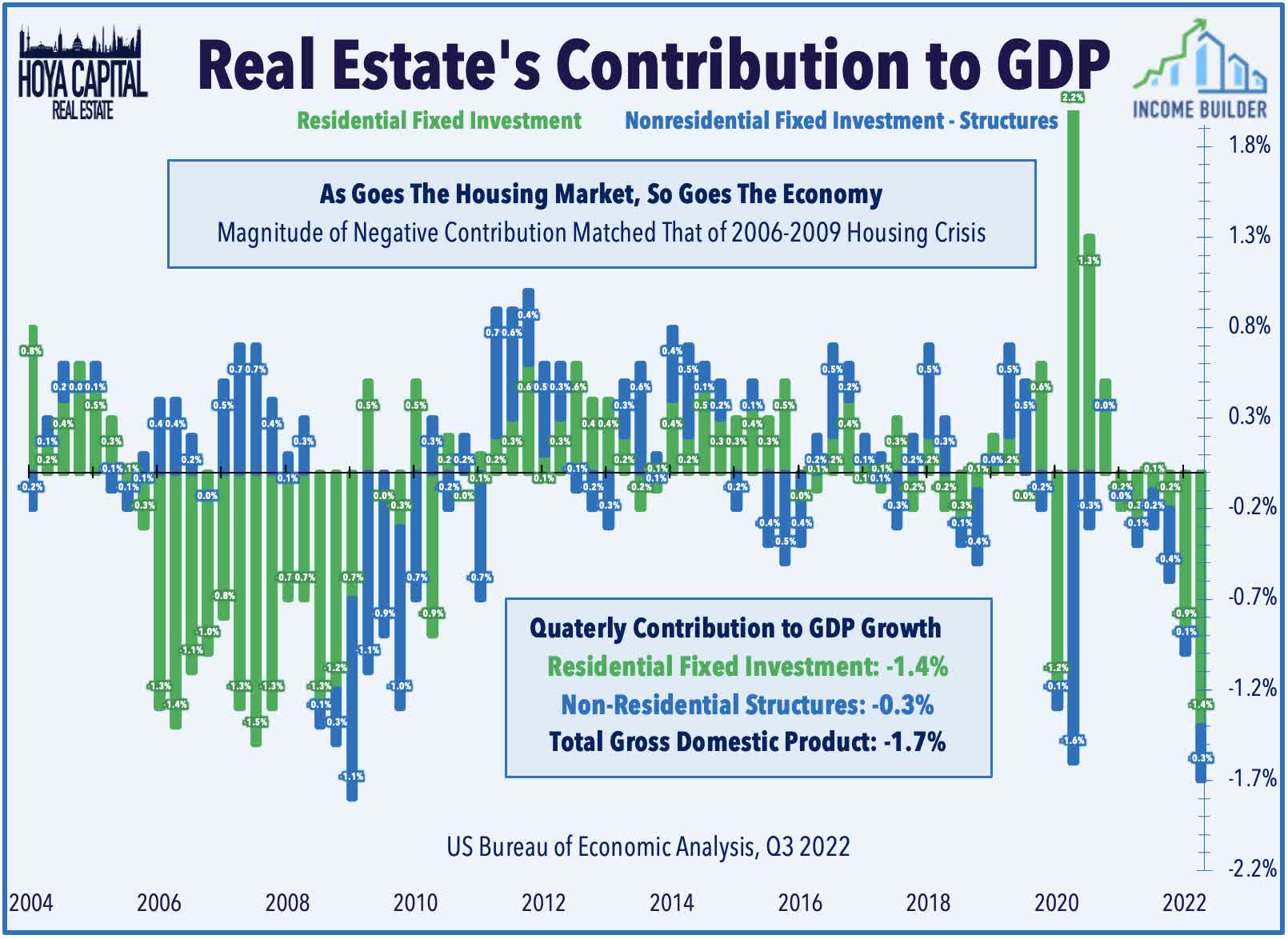

Expectations of cooling global inflationary pressure resulting from the power consolidation in China and the U.K. pivot towards tighter fiscal policy sparked a strong bid for bonds across the credit and maturity curve amid a historically brutal year for fixed-income securities. The 10-Year Treasury Yield pulled back sharply - closing the week at 4.01% - well below its recent intra-day highs of 4.30% in the prior week. Despite disappointing results from large-cap technology names with significant international exposure, domestic earnings results haven't been quite as weak as feared with 71% of S&P 500 companies beating EPS estimates, per FactSet , only slightly below the 10-year average. Homebuilders and the broader Hoya Capital Housing Index rebounded this week after reports indicated that homebuilders are capable of weathering the storm despite GDP data showing a steep contraction in residential fixed investment that matched that of the depths of the Great Financial Crisis.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

The U.S. housing sector continues to bear the brunt of the impact of extreme monetary tightening with the average rate on a 30-Year fixed-rate mortgage eclipsing 7% this week in the Freddie Mac Index for the first time since 2002. With monthly payments on new mortgages now nearly double that of just a year ago for the similarly-priced home, home sales activity and new home development have slowed dramatically over the past two quarters with New Home Sales and Pending Home Sales data this week posting sharp year-over-year declines of 17.6% and 31%, respectively. Remarkably, GDP data this week showed that Residential Fixed Investment - which took 14 years to recover to its pre-GFC level - subtracted 1.4 percentage points from GDP in the third quarter - a magnitude of negative contribution that was eclipsed only by two quarters in the past half-century: Q4 of 2007 and Q2 of 1980.

{kind=link}

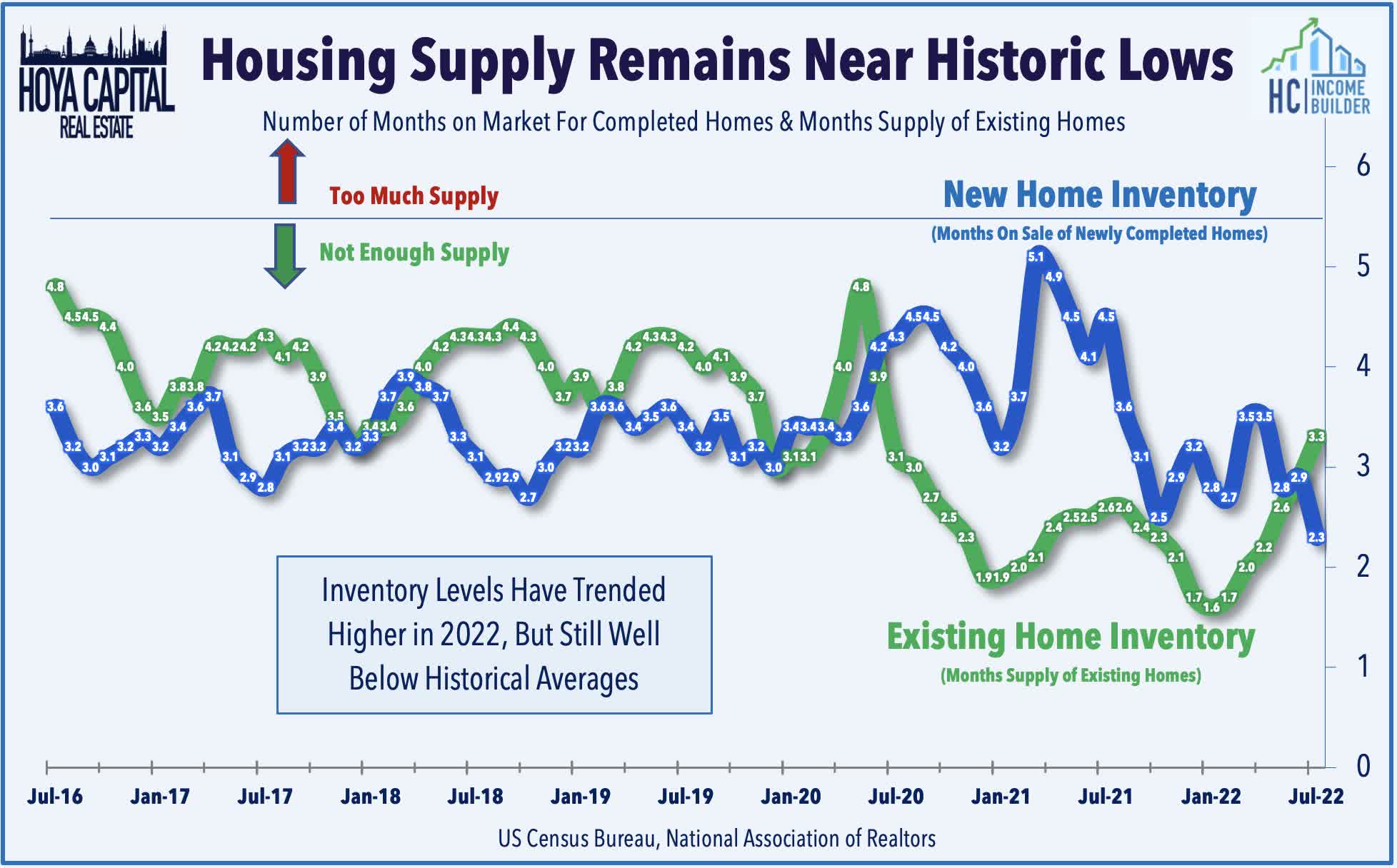

Exposing a paradox in the central bank approach, the attempt to tame housing cost inflation over the near term by targeting the demand side is likely contributing to a higher long-term level of housing inflation through its effects on the supply side. Home price and rent inflation has been driven primarily by a lack of housing supply resulting from a decade of historic underinvestment in new home development, and the higher rate environment has rapidly cooled the pace of new development - particularly in the single-family segment. Symptomatic of this dynamic, housing inventory levels have remained near historic lows despite the sharp drop-off in demand over the past several months. The New Home Sales report this week showed that in August, the Median Number of Months on the Sales Market for Newly Completed Homes stood at just 1.5 months - the lowest level on record.

{kind=link}

Low inventory levels should help to contain the potential downside in home values - particularly if mortgage rates moderate into year-end or if employment markets remain hearty - but an increasing number of housing markets in the U.S. are now seeing home price declines for the first time in a decade. The Case-Shiller 20-City Composite Home Price Index - which lags current market conditions by about 3 months - declined 1.3% in August from the prior month, which was the steepest month-over-month decline since March 2009. On a year-over-year basis, home values were still 13.1% higher than in August 2021, but notably, the slowdown from 16.0% in July was the steepest deceleration in the history of the S&P CoreLogic Case-Shiller Index. Data from Zillow ( Z ), meanwhile, showed that nearly half of the Top 60 markets recorded negative month-over-month growth in September with particularly sharp slowdowns in California and other West Coast markets.

{kind=link}

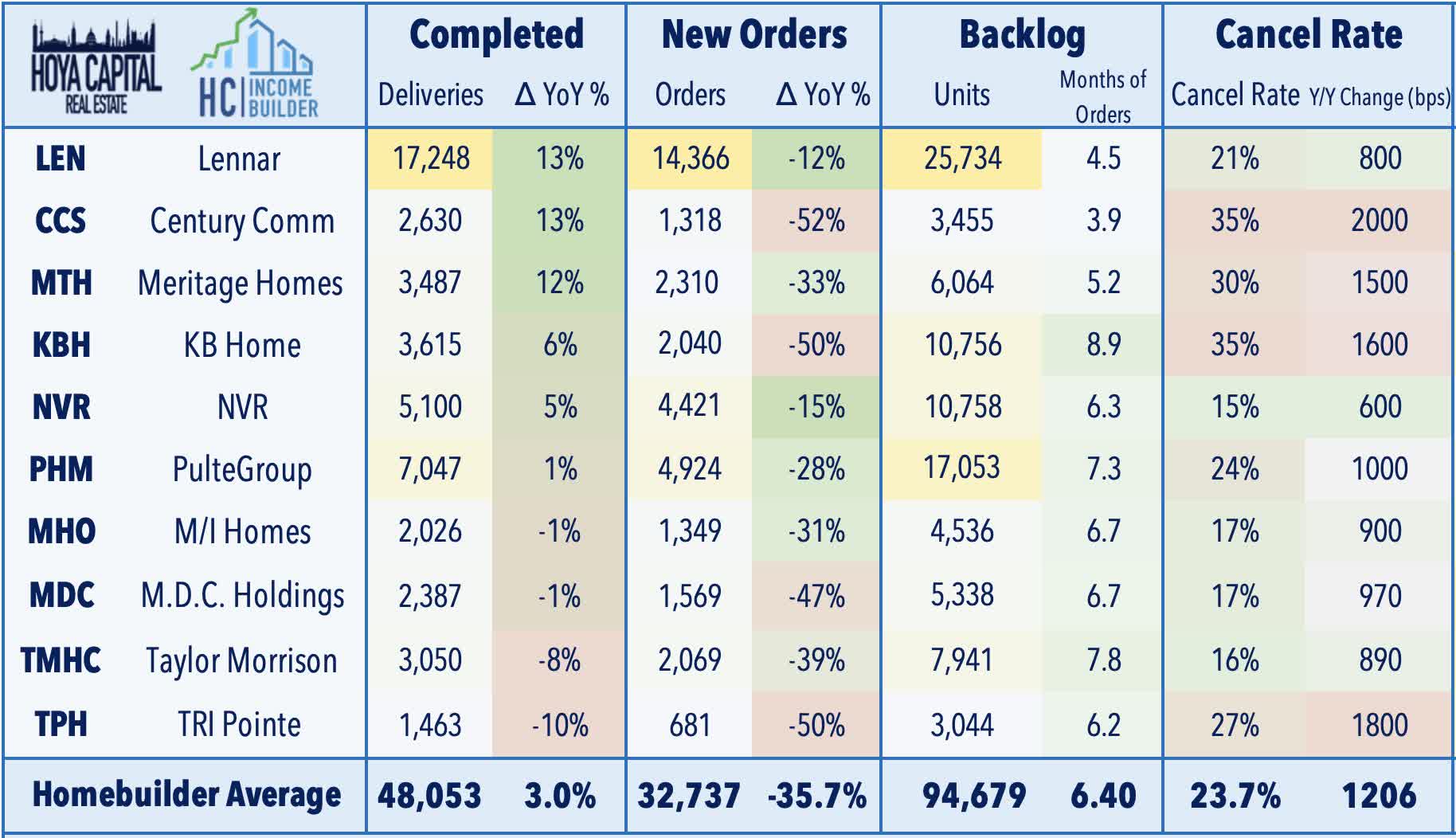

Results from the ten homebuilders that have reported results over the past month have shown that while the existing pipeline of previous orders has kept homebuilding revenues and EPS near record-high levels, the surge in mortgage rates has led to a sharp drop-off in new orders - lower by over 35% year-over-year in Q3 - and a surge in cancellation rates, which jumped to nearly 25% during the quarter. Positively, builders still have more than six months' worth of backlog to work through at the current sales pace - which should help to buffer the immediate downside pressure on revenues and earnings metrics - particularly if mortgage rates begin to finally moderate.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

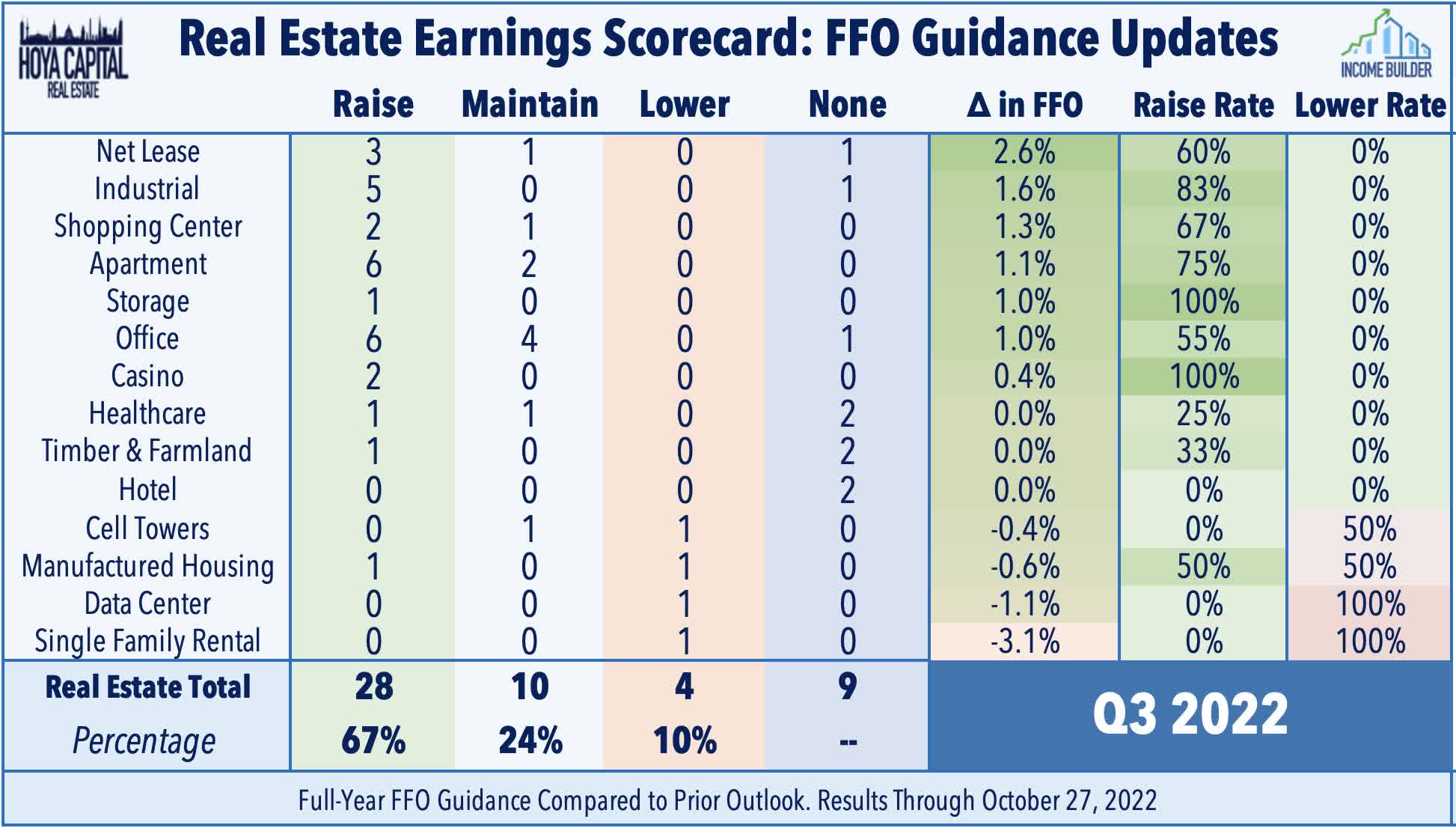

As analyzed in our REIT Earnings Halftime Report , we heard results from 45 equity REITs this week with the busiest slate coming in the week ahead with results from nearly 100 REITs. At the halfway point of earnings season, of the 41 REITs that have provided full-year Funds From Operations ("FFO") guidance, 28 REITs (67%) raised their outlook while just 4 REITs (10%) have lowered their outlook. Solid results from REITs come amid an otherwise disappointing earnings season for the broader equity market as, per FactSet, just 48% of S&P 500 companies have boosted their outlook. Upside standouts thus far have been Industrial, Shopping Center, and Apartment REITs. Sunbelt-focused office REITs have also surprised to the upside while the initial batch of results from Hotel and Healthcare REITs have been solid.

{kind=link}

Another week, another wave of REIT dividend hikes. A half-dozen REITs announced dividend increases this past week including mall REIT Macerich ( MAC ), which surged nearly 17% after hiking its quarterly dividend by 13% to $0.17/share . Getty Realty ( GTY ) gained 10% on the week after reporting better-than-expected, raising its full-year FFO outlook, and boosting its quarterly dividend by 4.9%. Kimco Realty ( KIM ) advanced 7% on the week after it raised its full-year FFO growth outlook to 14.5% and hiked its quarterly dividend by another 4.5% to $0.23/share - its second dividend hike this year. Community Healthcare ( CHCT ) advanced nearly 3% after raising its quarterly dividend by another 1%. We've now seen 120 REITs raise their dividend this year - matching the full-year record-high total from 2021.

{kind=link}

Healthcare : Hospital owner Medical Properties Trust ( MPW ) - one of the most heavily-shorted REITs - rallied more than 13% on the week after reporting better-than-expected results and raising its full-year FFO growth target. Citing improvement in operating performance at its hospital facilities and forecasted escalations in its CPI-linked leases, MPW raised its full-year FFO growth target to 3.4% - up 50 basis points from last quarter. Universal Health ( UHT ) gained nearly 10% on the week after its external manager reported better-than-expected results, commenting that "staffing vacancies and corresponding premium pay expenditures continue to sequentially decline," consistent with our conclusions in Healthcare REITs: Staffing Shortage Stumble , which noted that recent data suggests that the worst of the staffing shortage headwinds may be easing. Lab space-focused Alexandria Real Estate ( ARE ) also rallied more than 10% on the week after reporting another strong quarter while maintaining its full-year outlook calling for FFO growth of 8.4% and same-store NOI growth of 7.8%.

{kind=link}

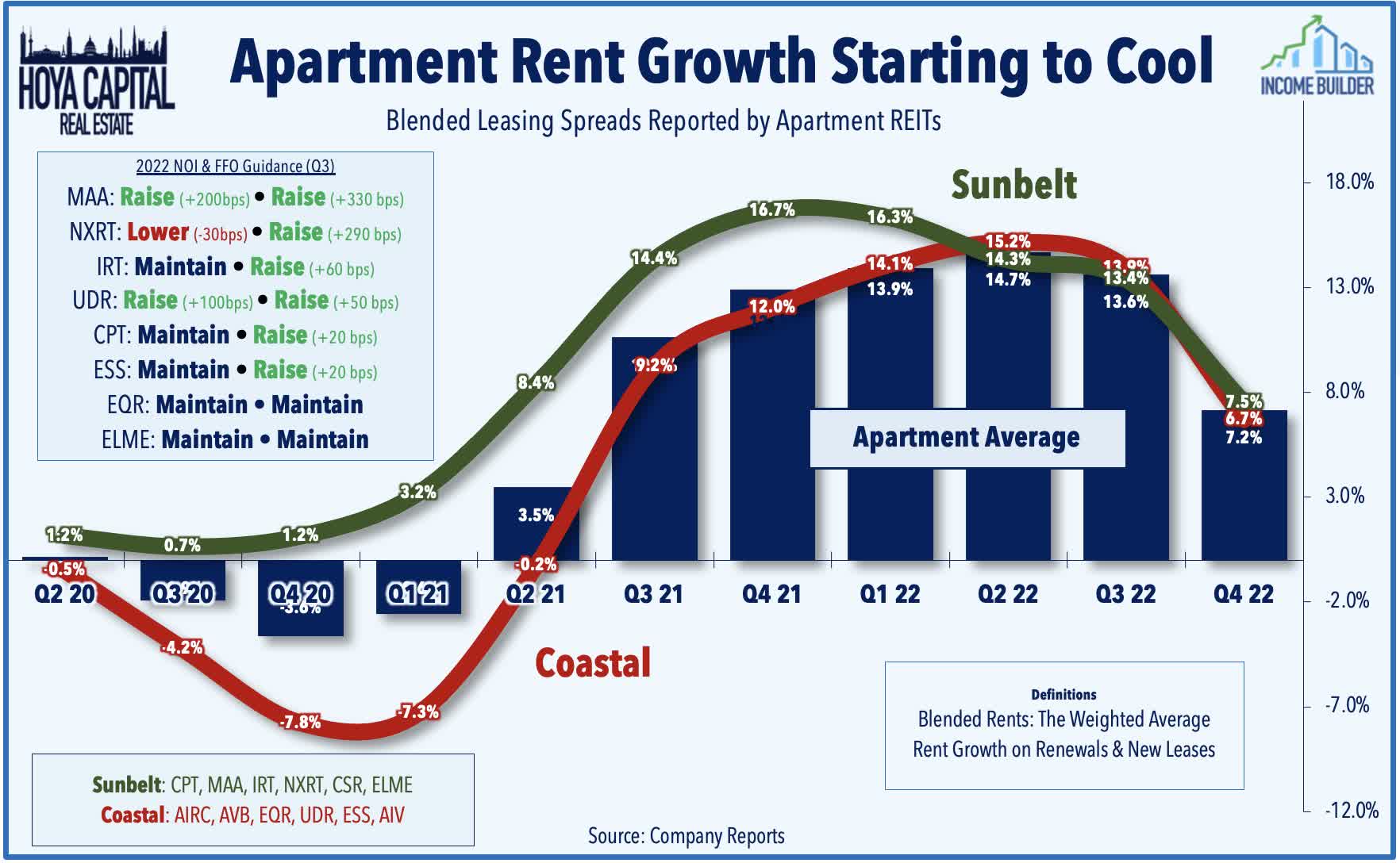

Apartments : Amid a busy slate of eight apartment REIT reports, Sunbelt-focused NexPoint Residential ( NXRT ) was the upside standout with gains of nearly 14% after raising its full-year FFO growth outlook, hiking its dividend by 10.5%, and increasing the share repurchase authorization to $100M. Driven by another quarter of double-digit rent growth with blended spreads of over 13%, NXRT now expects full-year FFO growth of 26.7% - up 290 basis points from its prior outlook. Independence Realty ( IRT ) rallied more than 6% after reporting similarly strong results and boosting its full-year FFO target by 30 basis points to a sector-high 28.0%. Mid-America ( MAA ) rallied nearly 5% this week after reporting impressive results and raising its full-year FFO growth target higher by 330 basis points to 21.4%. Coastal-focused REITs, however, have delivered a more challenging quarter thus far with rent growth showing a more material deceleration. West Coast-focused Essex Property ( ESS ) was a laggard after noting that blended spreads slowed to just 4.7% in October - down from 15.4% in Q2.

{kind=link}

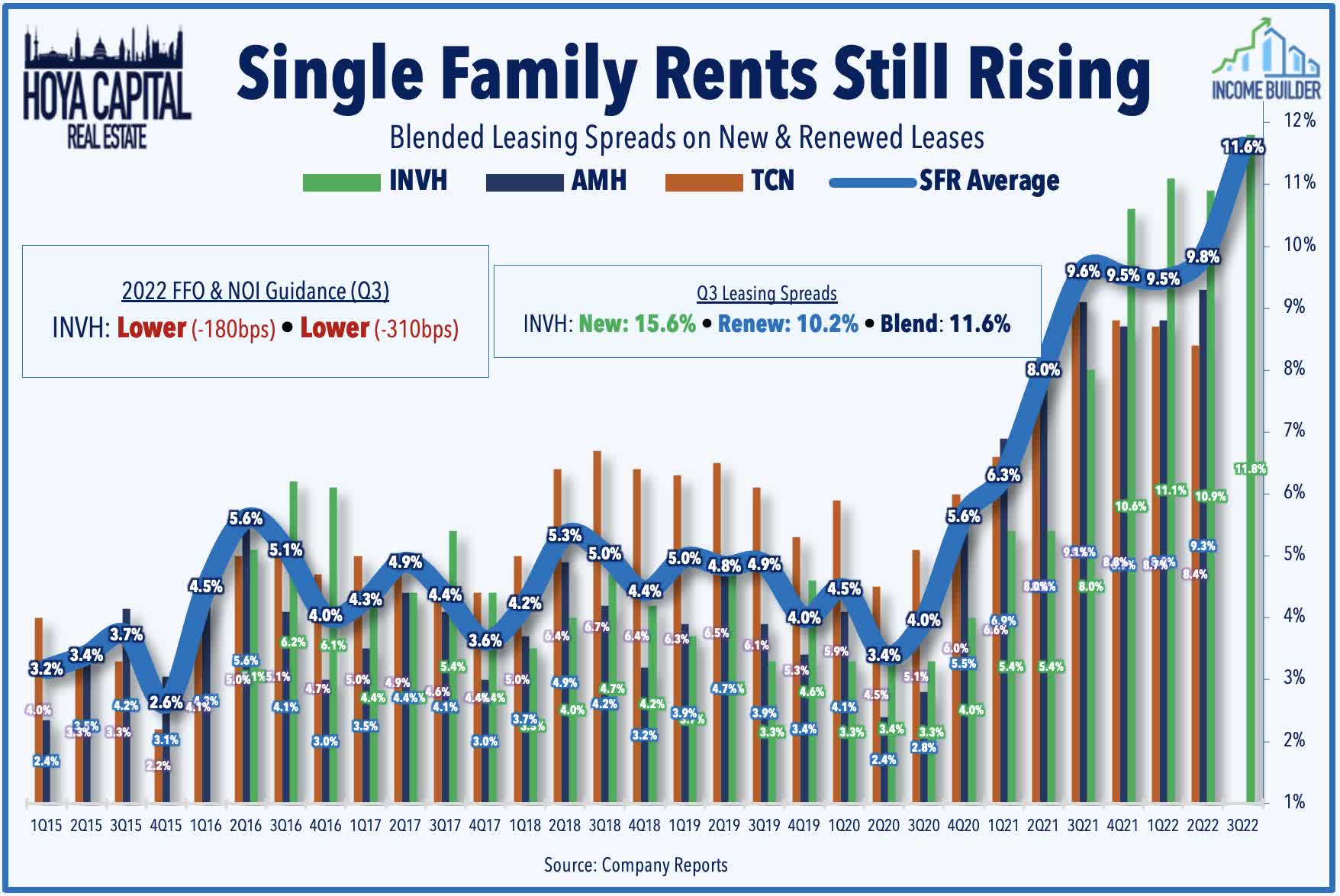

Single-Family Rental : Invitation Homes ( INVH ) - which also has a large West Coast presence - was also a laggard on the week, slumping more than 3% after reporting mixed results and trimming its full-year outlook, citing a hit from higher-than-expected property taxes and higher bad debt expense from renters who have fallen behind on their rent. While INVH reported impressive leasing spreads of nearly 12% in Q3, its rent collection rate dipped to 97% in Q3 - down 200 basis points from last quarter and its pre-COVID average of 99% - consistent with signs of stress across the broader economy amid historically high levels of inflation. We'll see results from American Homes ( AMH ) this Thursday and Tricon Residential ( TCN ) the following week.

{kind=link}

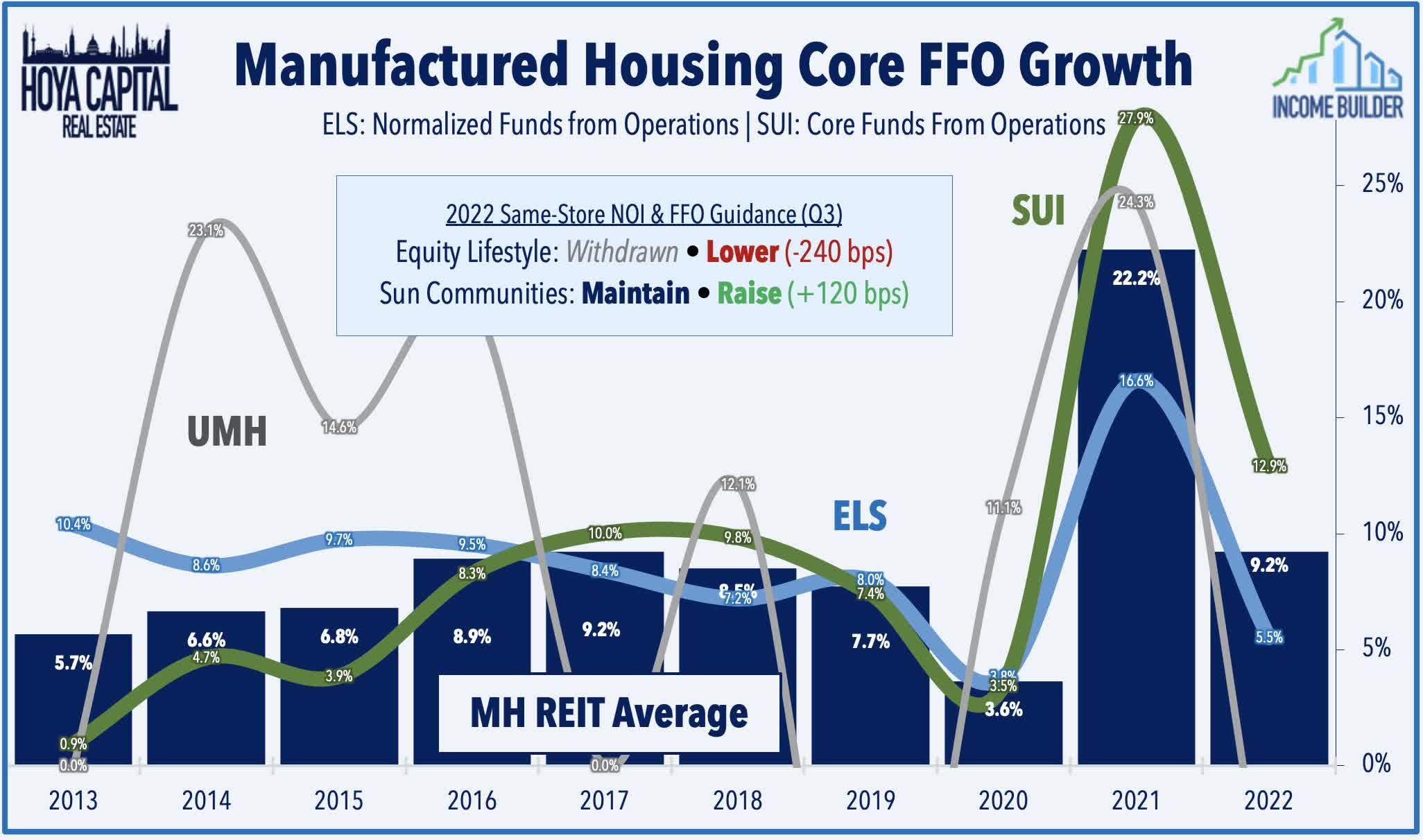

Manufactured Housing : Sun Communities ( SUI ) soared more than 12% this week after reporting better-than-expected results and raising its full-year outlook driven by better-than-expected results in its RV and marina division and expectations of accelerating rent growth in its core manufactured housing communities for the 2023 renewal season. SUI now expects its full-year FFO to rise 12.9% this year - up 120 basis points from last quarter - which is particularly impressive in light of last week's earnings miss from its MH peer, Equity LifeStyle ( ELS ). On the Hurricane Ian impact, SUI noted that the major storm damage was limited to four properties in the Fort Myers area - three RV properties and one marina. SUI recognized $29.9M for impaired assets with insurance expected to cover $17.7M. The $12.2M in estimated net losses represents less than 1% of its expected 2022 revenues.

{kind=link}

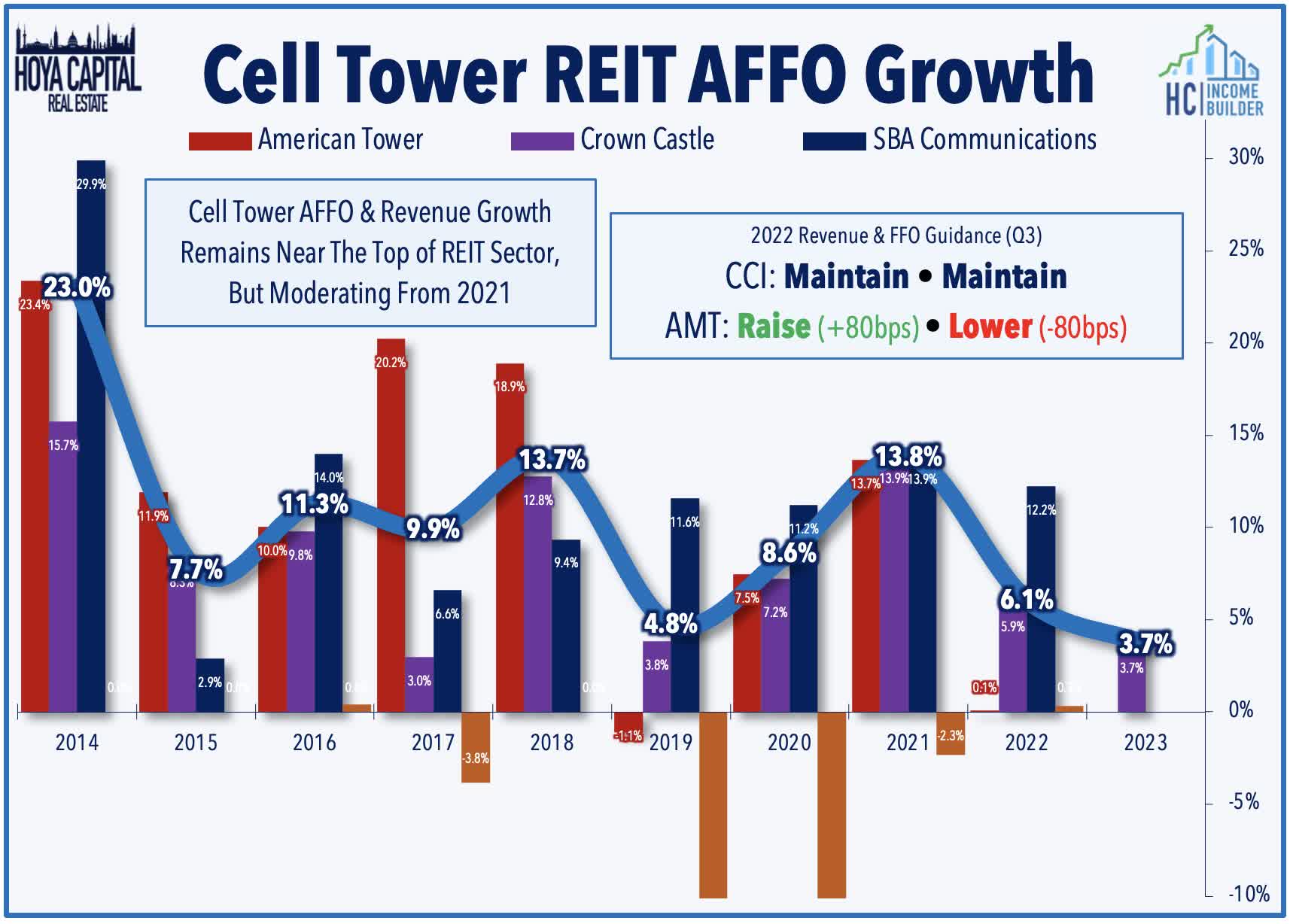

Cell Tower : American Tower ( AMT ) advanced 9% on the week after reporting decent results and raising its full-year revenue guidance, but revising down its full-year FFO target, citing negative FX effects and a drag from deferred rent payments from Vodafone India - which is undergoing a government-backed restructuring. AMT noted that it expects Vodafone to "revert back to 100% payment at the start of 2023 and repay outstanding pass-through balances." AMT did revise its full-year revenue growth target higher by 80 basis points, however, driven by strong "organic" rent growth in the U.S. and in its Latin America and Africa markets. Of note, AMT did not provide 2023 guidance but did comment that it expects 2023 to be a "challenging year" given the headwind from rising interest rates which will "certainly will take us off of our target AFFO growth" but noted that property-level fundamentals - rent growth and leasing volumes - should continue to "accelerate" into 2024.

{kind=link}

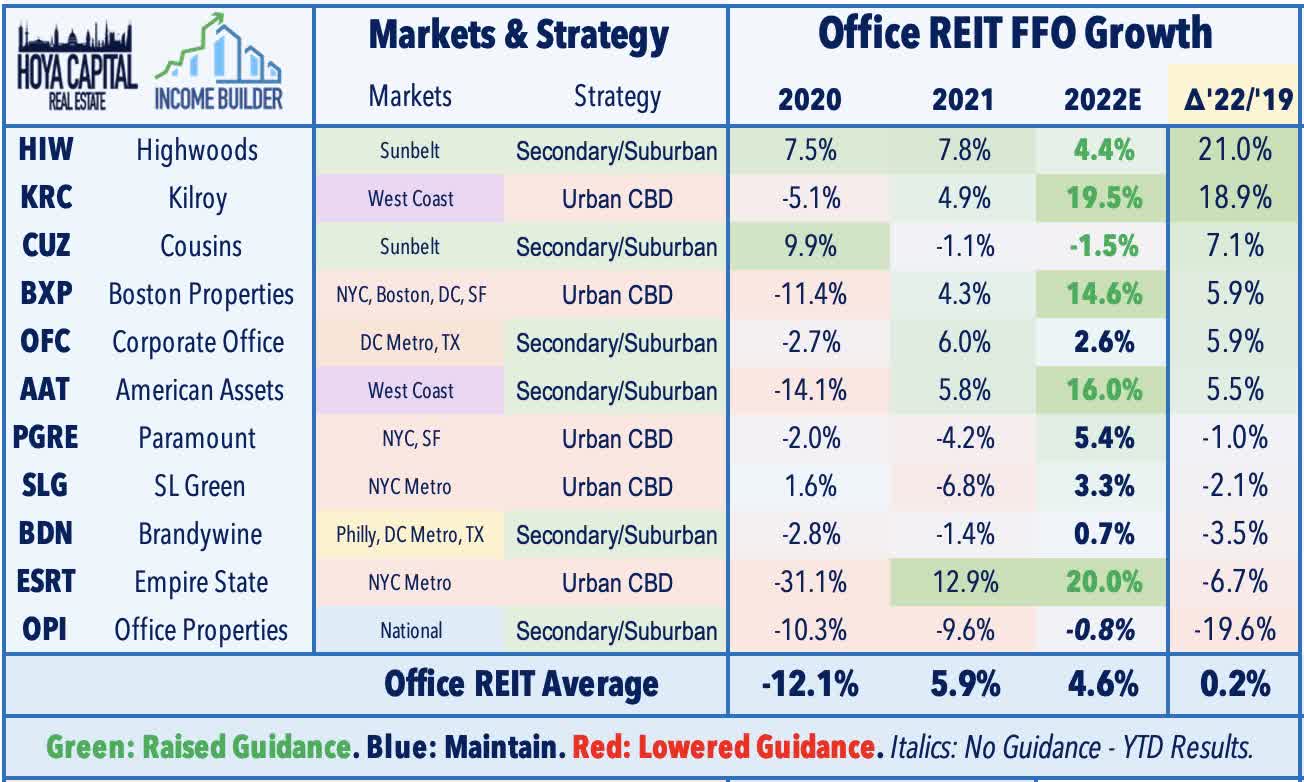

Office : Sunbelt-focused Highwoods ( HIW ) was the standout in the sector this week, rallying nearly 9% after reporting better-than-expected results and raising its full-year outlook. HIW - which has been an upside standout in the office REIT sector given the relative strength of demand in its Sunbelt markets - raised its full-year FFO growth target to 4.4% - up 180 basis points from its prior outlook while noting that it leased 518k SF of space in Q3 - its highest volume of new leases since 2014 with net effective rents that were more than 20% above its prior five-quarter average. Results from coastal-focused Boston Properties ( BXP ) were less impressive, however, as BXP finished flat on the week after maintaining its full-year outlook, but noting that it expects its FFO to be about 4% lower in 2023 at the midpoint of its range.

{kind=link}

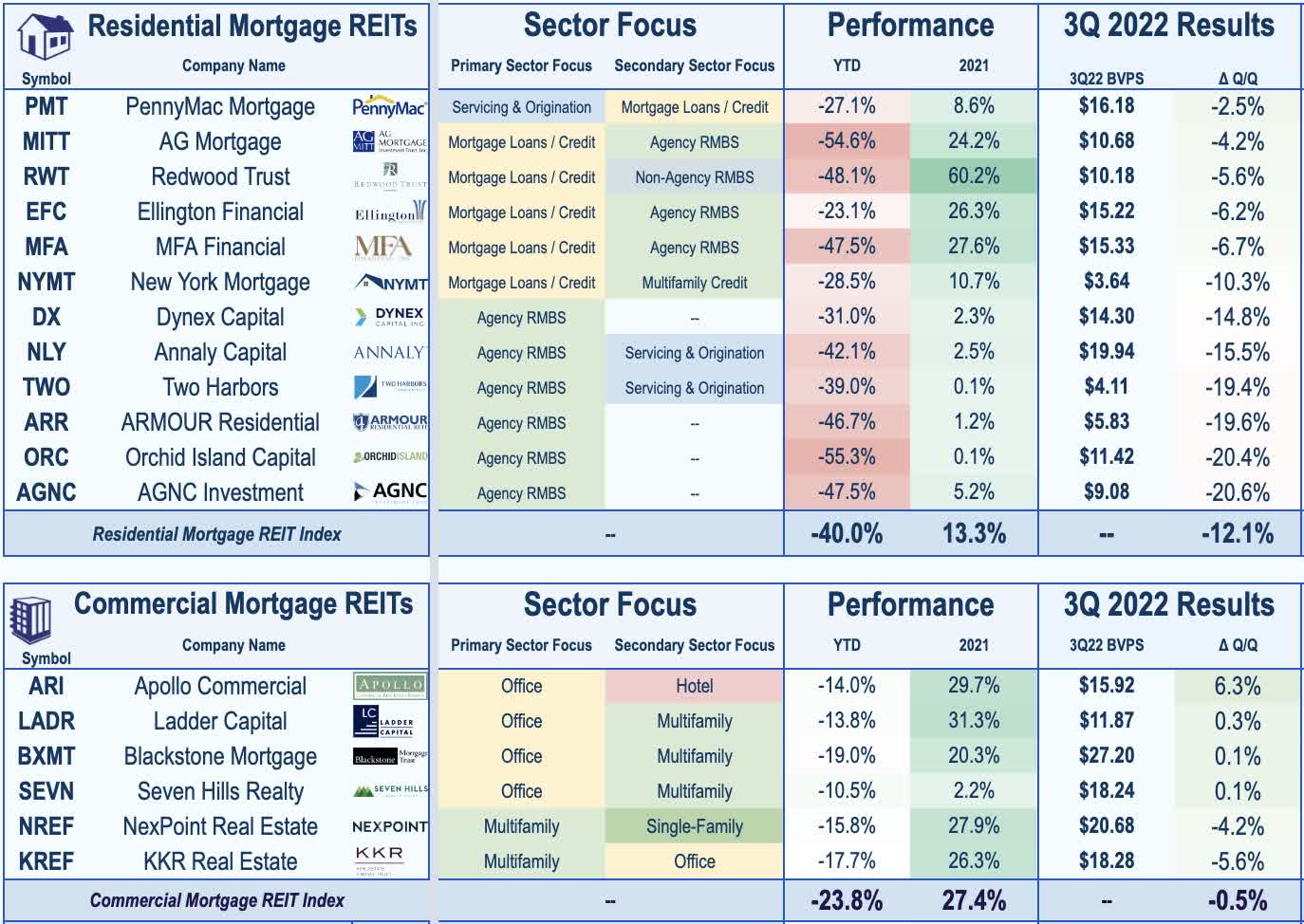

Mortgage REIT Week In Review

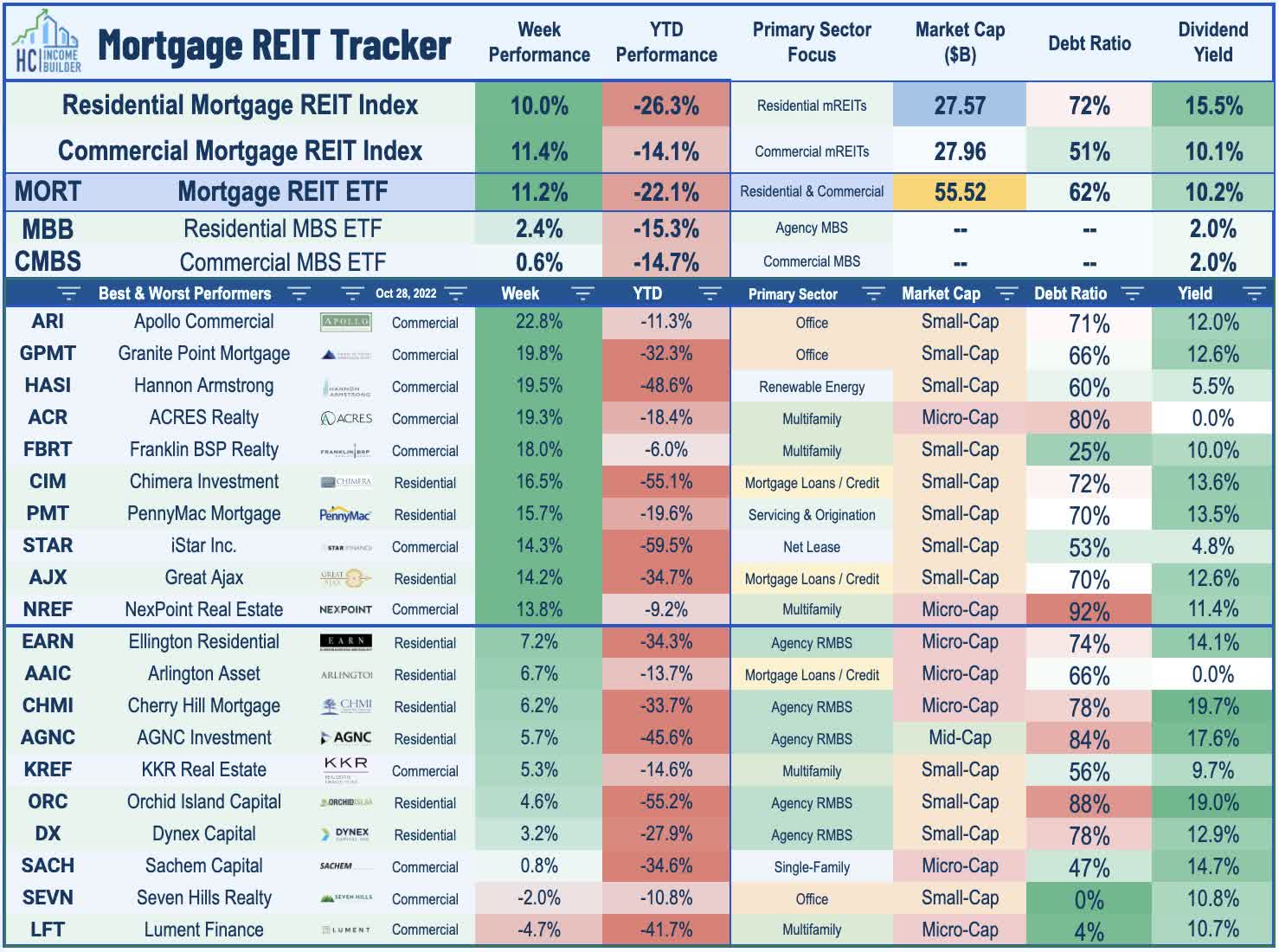

The significant rebound continued this week for Mortgage REITs as earnings results thus far have been significantly better than expected despite the historically brutal quarter for lending markets. We heard results from 13 mREITs this week with some of the strongest results coming from commercial mREITs that focus on floating-rate lending. Apollo Commercial ( ARI ) soared more than 20% this week after reporting that its Book Value Per Share ("BVPS") rose 6% in the quarter to $16.12. Blackstone Mortgage ( BXMT ) rallied 12% after reporting a 1% rise in its BVPS to $27.20, noting that its average loan rates increased 100 basis points in Q3 alone. Residential mREIT PennyMac ( PMT ) surged more than 15% on the week after reporting that its BVPS was lower by just 2.5% in the third quarter - the most muted decline among residential mREITs to report results thus far. Redwood Trust ( RWT ) advanced more than 6% after reporting a similarly better-than-expected report with a BVPS decline of just 5.6% in Q3.

{kind=link}

As expected, Book Value declines have been more significant for pure-play agency-focused mREITs but conditions are far less grim than feared several weeks ago. Annaly Capital ( NLY ) - the largest mortgage REIT focused primarily on government agency-backed lending - rallied nearly 10% after reporting better-than-expected EPS results while confirming that its BVPS declined 15% in the quarter - consistent with its update in early October. AGNC Mortgage ( AGNC ) gained 6% after reporting that its BVPS dipped 21% in Q3 to $9.08 - also consistent with the preliminary estimate provided earlier this month. Armour Residential ( ARR ) surged more than 11% after reporting a similar beat on the bottom line with adjusted EPS of $0.32 - covering its $0.30 quarterly dividend - while confirming that its BVPS dipped 19% in Q3. Orchid Island ( ORC ) and Dynex Capital ( DX ) - each agency-focused lenders - were each slightly higher after reporting in-line results that confirmed earlier preliminary updates.

{kind=link}

While earnings commentary was generally upbeat with most mREITs seeing stronger future earnings potential in the higher-rate environment and noting that dividend payouts are still covered, KKR Real Estate ( KREF ) has been a laggard on the commercial mREIT side after providing cautious commentary, noting that the "macro environment has continued to deteriorate...real estate values are declining in real-time as the market digests the higher cost of capital." We'll hear results from 18 mortgage REITs next week including New York Mortgage Trust ( NYMT ) and Chimera ( CIM ) on Tuesday, Rithm Capital ( RITM ) and Ares Commercial ( ACRE ) on Wednesday, Hannon Armstrong ( HASI ) and Invesco Mortgage ( IVR ) on Thursday, and Arbor Realty ( ABR ) on Friday.

{kind=link}

2022 Performance Check-Up

With ten months of 2022 now in the books, Equity REITs are now lower by 28.4% on a price return basis for the year - their second-worst YTD performance for the REIT Index on record through this date behind 2008 - while Mortgage REITs are lower by 32.3%. This compares with the 18.1% decline on the S&P 500 and the 15.2% decline on the S&P Mid-Cap 400 . Within the real estate sector, just one property sector is in positive territory on the year - Casino REITs - while nine property sectors are lower by more than 30%. At 4.01%, the 10-Year Treasury Yield has surged 250 basis points since the start of the year, but is below its 2022 highs of 4.30%. As a result, the US bond market is on pace for its worst year in history with a loss of 15.3% on the Bloomberg US Aggregate Bond Index , which is 5x larger than the previous worst year back in 1994 (-2.9%).

{kind=link}

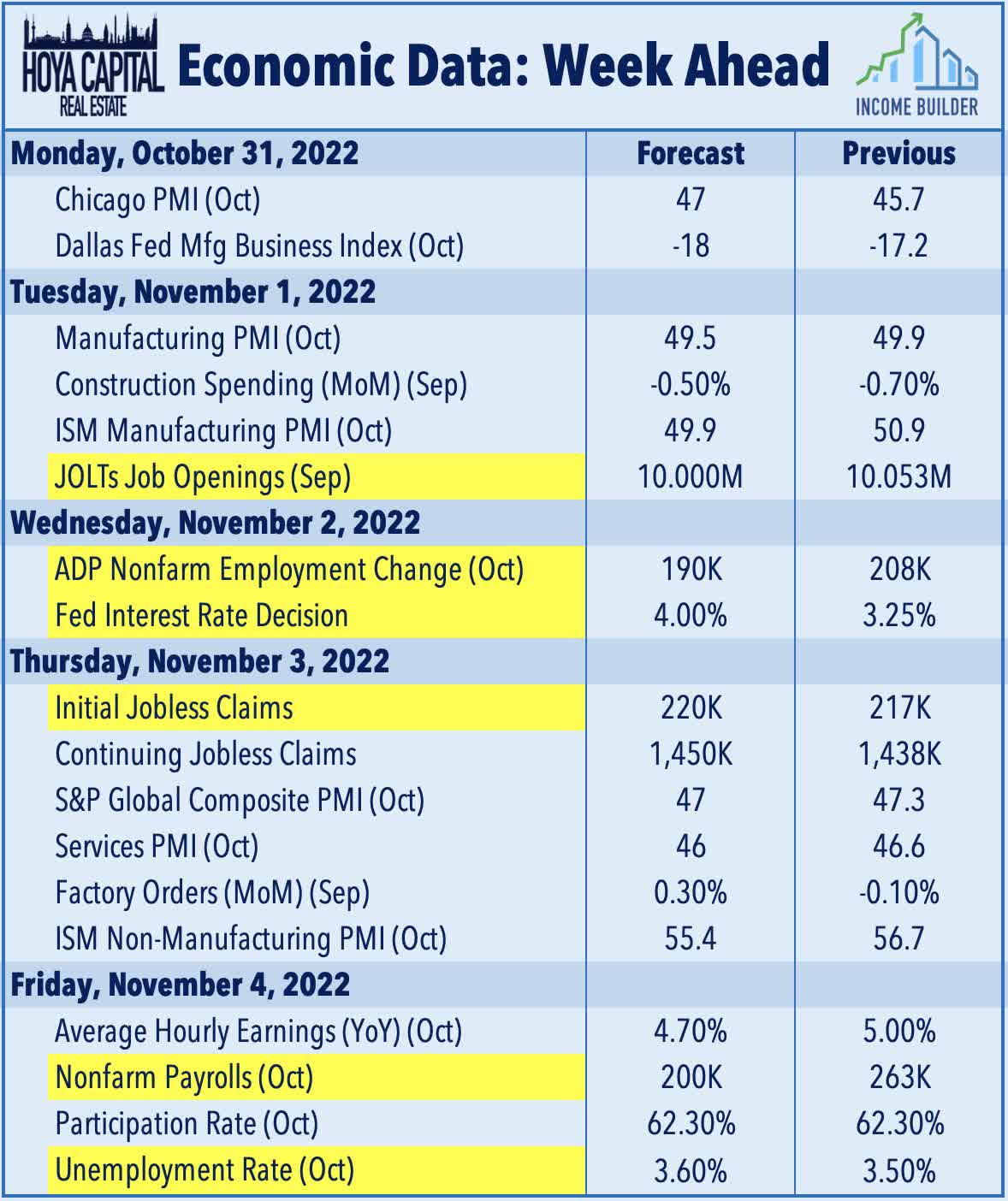

Economic Calendar In The Week Ahead

It'll be another jam-packed week of economic data and corporate earnings results with the main event coming on Wednesday with the FOMC Interest Rate Decision on Wednesday, in which the Fed is widely expected to raise rates by 75 basis points to bring the Fed Funds rate to a 4.0% upper-bound. Jobs data highlights the busy economic data slate with JOLTS data on Tuesday, ADP Payrolls on Wednesday, Jobless Claims data on Thursday and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 200k in October - which would be the smallest gain since December 2020 - and for the unemployment rate to tick higher to 3.60%. 'Good news is bad news' will likely be the theme of these reports as investors and the Fed look for signs of the long-awaited cooldown in job growth which has yet to fully materialize. Purchasing Managers' Index ("PMI") data will continue to be a major market focus - particularly in Europe and Asia - as recent reports have dipped below the breakeven 50-level.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

'Soft Landing' Hopes Revived