QVMS - 'Transitory Disinflation' Likely To Be Short Lived

Summary

- The Cleveland Fed forecasts inflation to start plateauing in January and February.

- The Fed will have to be more aggressive and hike above the currently expected 5.1%.

- Long-term nominal interest rates expected to rise, and the bear market in TLT expected to continue.

Transitory disinflation

Fed Chair Jay Powell warned that the current trend of "disinflation" will be transitory at the press conference after the FOMC meeting on Feb. 1:

If you take very short-term three months, say, measures of PCE - core PCE inflation, they're quite low right now. But that's because that's driven by, you know, significantly negative readings from goods inflation. Most forecasters and - would think that the significantly negative readings will be transitory and that goods inflation will move up fairly soon, back up to its longer run trend of something around zero, something like that.

Specifically, Powell has been consistent in explaining that the current inflation dynamics are function of:

- Goods disinflation, mostly based on improved supply-chains and shift from goods consumption to service consumption. However, as quoted above, this is likely to be transitory - goods prices will eventually stop coming down.

- Expected housing disinflation - based on the leading indicators on future rents, it is expected that the housing cost will also be disinflationary later this year.

- Service ex housing inflation is not showing any disinflation, and it's likely to remain elevated as long as the labor market stays tight.

In my humble opinion, the strong labor market will end the goods prices disinflation prematurely and possibly diminish the housing disinflation, while keeping services inflation elevated. People will buy TVs, get their own apartments, etc.

Taken all together, the current "transitory disinflation" is likely to be short lived. This is consistent with Ron Baron's just reported opinion, which sees long term inflation at 4%-5%.

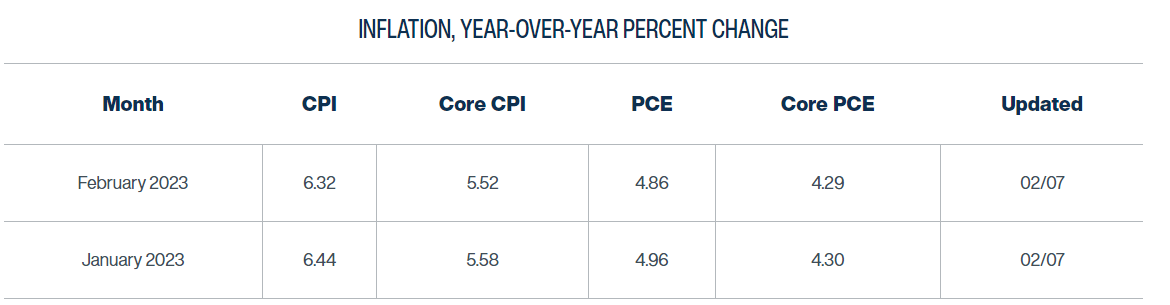

The expected inflation for January and February

In fact, the Cleveland Fed publishes the InflationNowcast and daily updates their inflation forecast, based on a very sophisticated model, which in their own words beats other forecasts over time. The Cleveland Fed is forecasting that the headline CPI inflation already is plateauing just above 6%, and the core CPI inflation is plateauing at 5.5%. This is their forecast for January and February:

{kind=link}

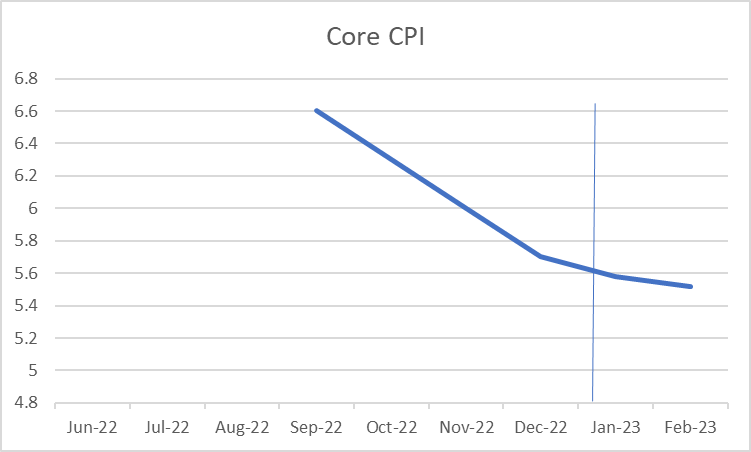

Core CPI peaked in September at 6.6% and based on the Nowcast prediction, the disinflationary downtrend is expected to significantly slow down. Here's the chart:

{kind=link}

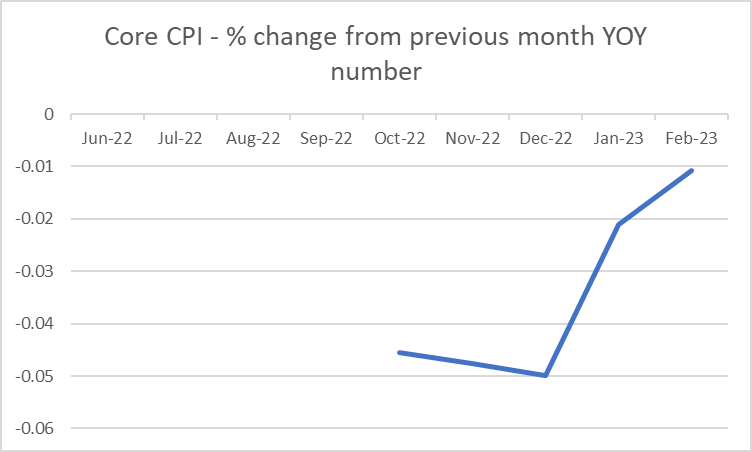

We can compute the percentage change in YOY core CPI number from the previous month, and see that the disinflation trend is approaching the end, with the monthly decrease in core inflation going from 5% (December) to expected 2% (January) and 1% in February.

{kind=link}

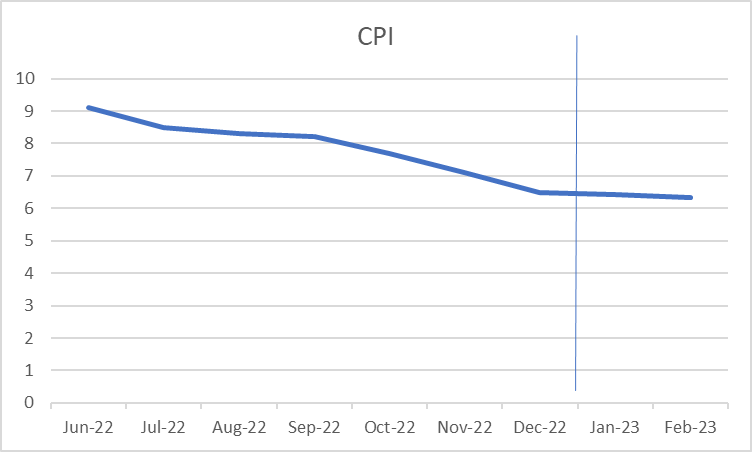

The headline CPI peaked in June at 9.1%, and since significantly fell to 6.5% in December. However, the Nowcast see the headline inflation plateauing just above 6% in January and February.

{kind=link}

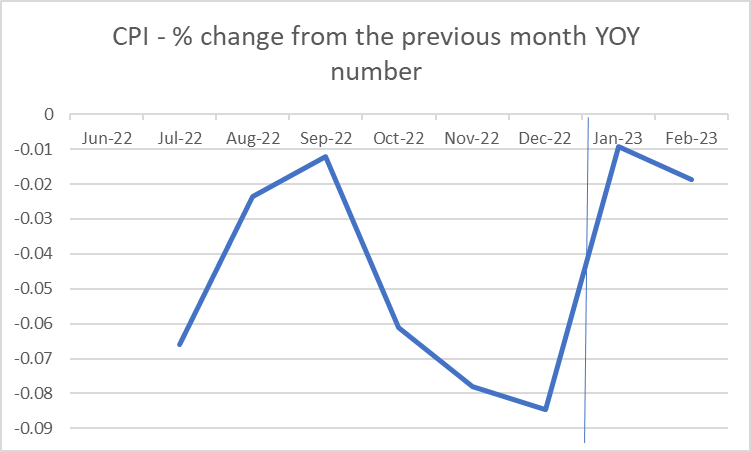

If we compute the percentage change from the previous month YOY number, we can see that in December CPI fell by 8% from November, but it's expected to fall by less than 1% in January and by 1.8% in February.

{kind=link}

The Fed must be more aggressive

The obvious implication of the "transitory disinflation" fading quickly is that the Fed will have to be more hawkish and possibly increase the interest rates above the currently expected 5.1% level. However, the Fed still refuses to explicitly acknowledge the need for a more aggressive stance on inflation.

The biggest news that came out of the Fed Chair Powell's interview/speech at the Washington Economic Club on Feb. 7 was that Jay is a guitar player. Welcome to the club and keep rocking.

But seriously, it was naive to expect that the Chair Powell would explicitly admit that the surprisingly strong January payroll report made the Fed more hawkish. He didn't have to - it's obvious. In fact, Powell clearly stated :

"The reality is we're going to react to the data, and if we continue to get strong labor market reports and higher inflation reports, it might well be the case we have to do more".

What more can you say? The Fed will likely have to be more aggressive than previously expected, with the Federal Funds rate going toward 5.5%. And this is not my opinion. The Federal Funds futures are already pricing the following:

- 4.84% FF rate in March, meaning 100% chance of 25bpt hike, and a small chance for a 50bpt hike.

- 5.1% FF rate in May, meaning 100% chance of another 25bpt, and also matching the Fed's dotplot target for 2023.

- 5.16% FF rate in June, meaning the market is already starting to price the third 25% hike, which is likely to continue with the incoming data.

- the first cut in December 2023

Thus, the bond market has started to price a more hawkish Fed after the January payroll report, which in my opinion has been confirmed by the Chair Pöwell at his Feb. 7 speech.

At the end of the video around 1:16 mark Powell also says "we have a significant road ahead to get inflation down to 2%". The "significant road" has a different meaning from the "long road" as previously used when referring to inflation. The meaning of significant is: "Suggesting a meaning or message that is not explicitly stated." This was a more hawkish message.

Market implications

However, the stock market ( SPY ) is still focused on the "beginning of disinflation" narrative, rather the "transitory disinflation" reality. The implications for stock market are obvious - the bear market continues as the probability of a much deeper and longer recession increases with each additional Fed hike.

However, the implications for the longer-term bond market are less obvious ( TLT ). Here's the TLT chart, which shows the downtrend (higher interest rates) since 2020, with the recent "disinflationary" bounce since October, right to the 200-dma resistance.

If the current disinflation is in fact transitory, and inflation settles at a much higher level, the downtrend in TLT is likely to resume - meaning higher interest rates.

The 10Y Treasury Bond nominal yield is the sum of the Real interest rate and the Inflation expectations. The 10Y BE inflation expectations have peaked at 3% in April 2022 and since fallen to around 2.2%. Powell calls this "anchored inflation expectations" near the target rate of 2%, which is positive.

However, if the market sniffs that longer term inflation will be 4-5% as Baron sees, the 10Y BE inflation would rise back to, and above 3%.

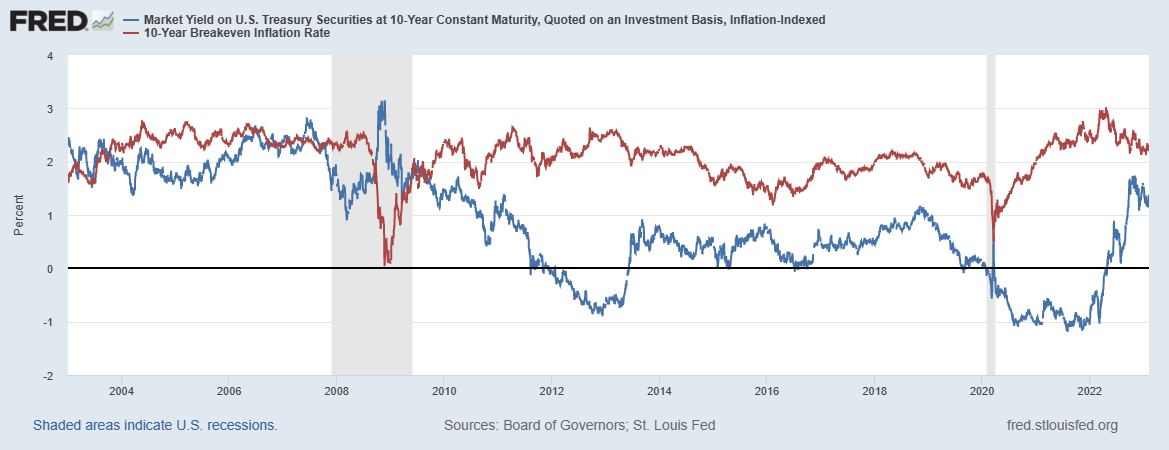

Further, the real interests are function of the financial condition, whereby a stimulative monetary policy pushes the real rates to zero and below (via QE), and tightening monetary policy pushes the real rates closer to the inflation expectations (via QT). Here's the chart of inflation expectations (red) and real interest rates (blue):

{kind=link}

The real rates at 1.3% are still too low, based on the restrictive monetary policy and QT. Thus, real rates should be closer to 2%, given the current level of inflation expectations around 2.2%. That would suggest that the nominal interest rate on 10Y Treasury should be above 4% (currently 3.68%).

But if inflation settles at 4-5% level, and inflation expectations rise to above 3%, the real interest rate would also have to rise closer to 3%, which suggests the nominal interest rate on 10Y Treasury Bond should rise close to 6%.

The alternative view is that the Fed will be much more aggressive and will not allow inflation to settle above 2%, which would cause a much deeper recession and bring the 10Y nominal yield back below 3%.

Given the current reluctance of the Fed to explicitly acknowledge the inflationary reality, the nominal long term interest rates are likely to rise, and the bear market in TLT to continue.

For further details see:

'Transitory Disinflation' Likely To Be Short Lived