GLPI - 'Winter Chill' Dims Holiday Cheer

Summary

- U.S. equity markets declined for a third-straight week as benchmark interest rates surged after the advance of a $1.7 trillion federal spending package overshadowed another slate of encouraging inflation data.

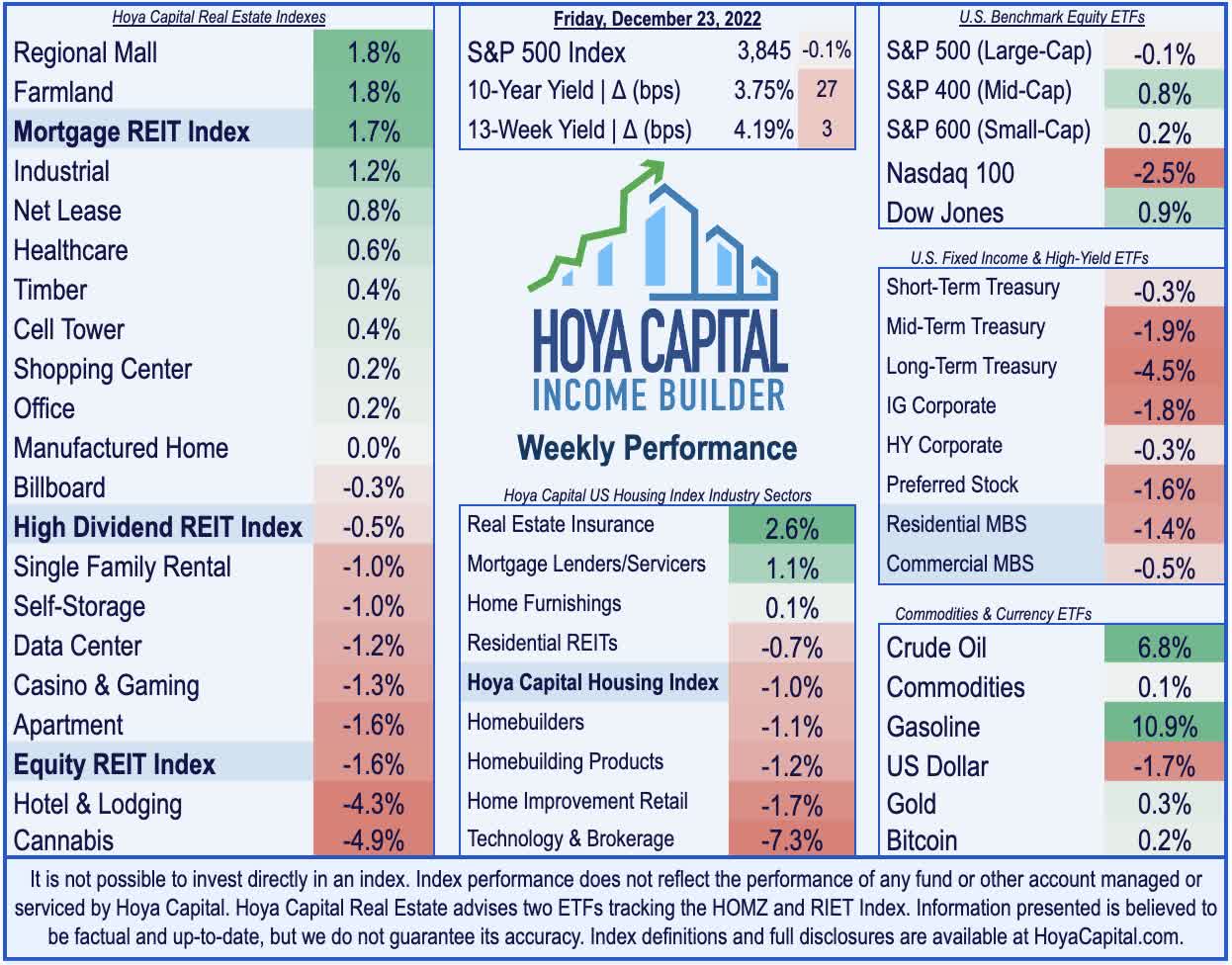

- Declining for a third-straight week and finishing back on the cusp of the "bear market" threshold, the S&P 500 slipped 0.1% this week while the tech-heavy Nasdaq 100 dipped 2.5%.

- Pressured by the surge in interest rates, real estate equities were under renewed pressure this week with the Equity REIT Index slipping by 1.6%, but Mortgage REITs advanced 1.7%.

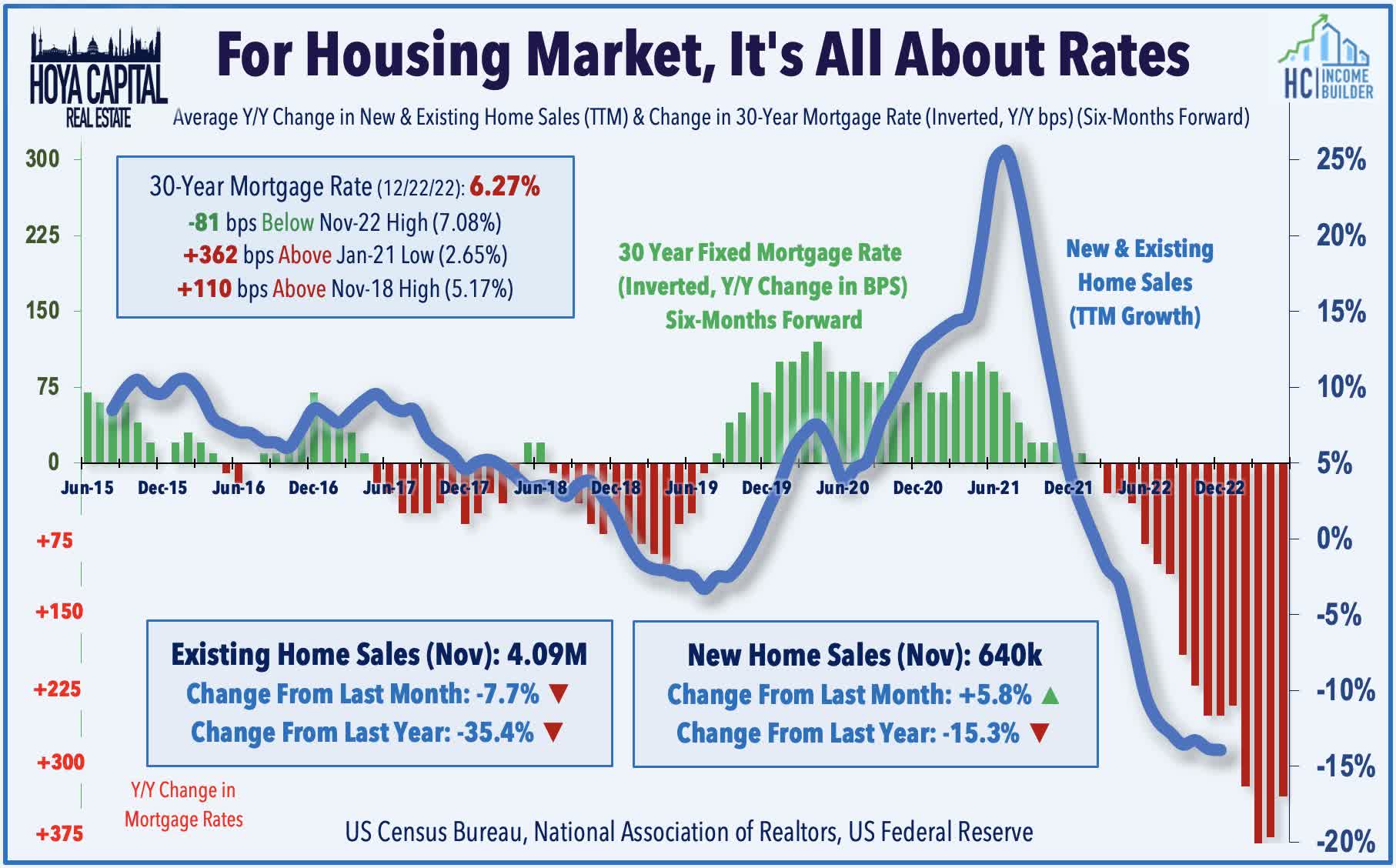

- Homebuilders remained under pressure after a busy slate of housing market data showed a deepening "winter chill" in home buying and building activity - but also some reasons for optimism heading into the new year.

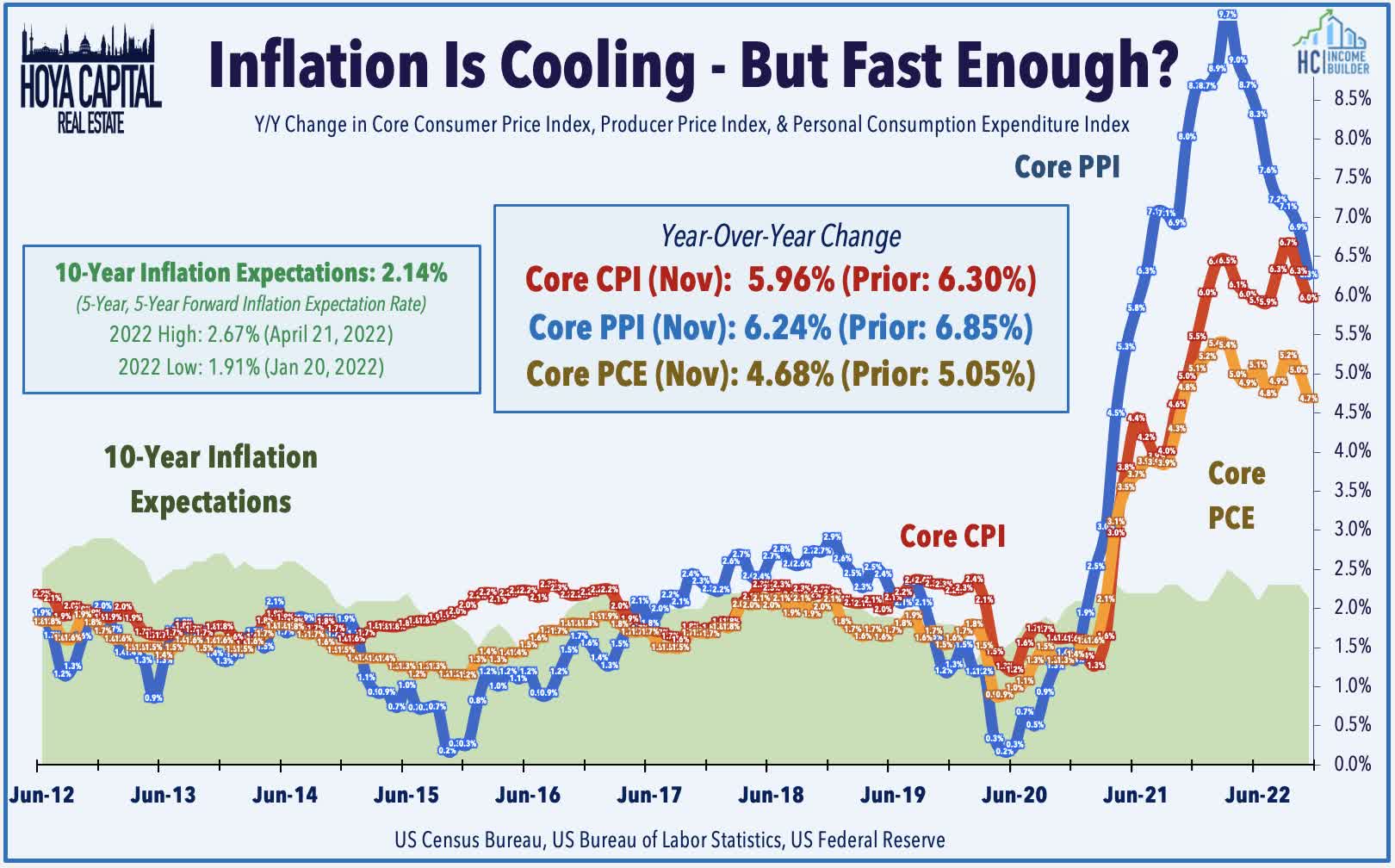

- Following cooler-than-expected CPI and PPI inflation data in the prior two weeks, Core PCE exhibited similar cooling in November. The three indexes now show core inflation trending at a 3% annualized rate over the past quarter - down sharply from the 9% peak in the first quarter.

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on December 23rd.

Real Estate Weekly Outlook

U.S. equity markets declined for a third-straight week as benchmark interest rates surged after the advance of a $1.7 trillion federal spending package and a surprise rate hike from the Bank of Japan overshadowed another slate of encouraging inflation data. Following cooler-than-expected CPI and PPI inflation data in the prior two weeks, the Federal Reserve's preferred inflation gauge - Core PCE - exhibited similar cooling in November with the three indexes now showing core inflation slowing to a roughly 3% annualized rate over the past quarter - down sharply from the 9% peak in the first quarter.

{kind=link}

Declining for a third-straight week and finishing back on the cusp of the "bear market" threshold, the S&P 500 slipped 0.1% on the week while the tech-heavy Nasdaq 100 dipped another 2.5% to push its year-to-date declines back to over 32%. The Mid-Cap 400 and Small-Cap 600 each finished higher for the week. All four major benchmarks are on-pace for their worst year since 2008. Pressured by the surge in interest rates, real estate equities were under renewed pressure this week with the Equity REIT Index slipping by 1.6%, but the Mortgage REIT Index advanced 1.7%. Homebuilders finished lower by 1% after a busy slate of housing market data showed a deepening "winter chill" in activity - but also some reasons for optimism.

{kind=link}

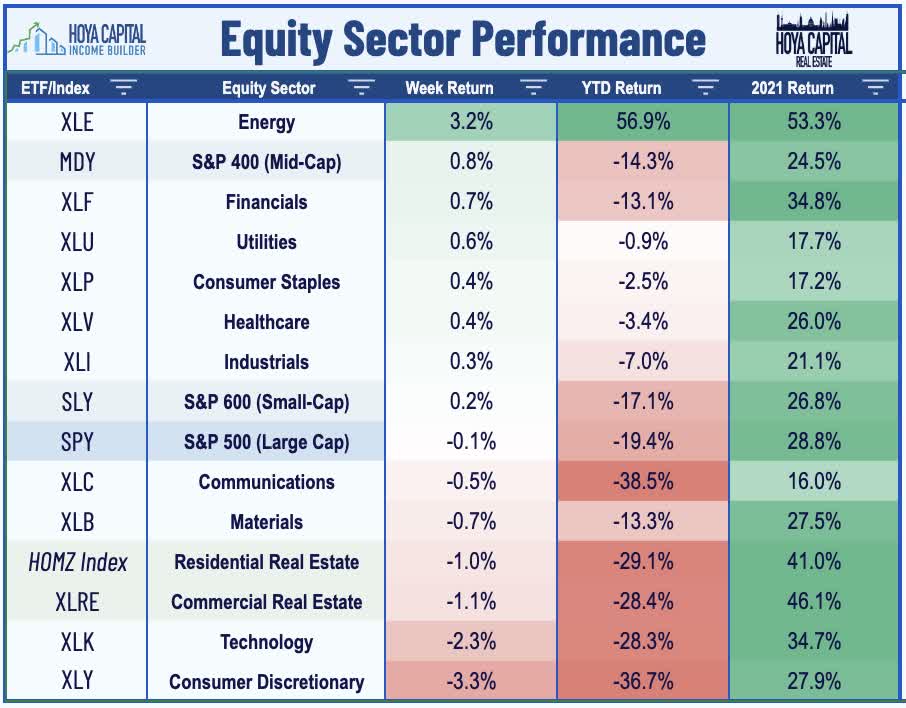

Concerns over the inflationary impact of the omnibus federal spending package and the effects of global central bank tightening negated the encouraging inflation news, sending benchmark interest rates across the yield curve sharply higher. The 10-Year Treasury Yield ( US10Y ) soared 27 basis points to 3.75% while the 2-Year Yield ( US2Y ) jumped 15 basis points to 4.33% even as the U.S. Dollar Index dipped nearly 2% to six-month lows. Unseasonably harsh winter weather in the U.S. and ongoing geopolitical concerns in Eastern Europe - along with concerns over the potential demand uptick related to China's pivot away from "COVID zero" policies - sent Crude Oil and Gasoline prices sharply higher this week, reversing a six-month skid that has pulled U.S. consumer gas prices down to 18-month lows . Six of the eleven GICS equity sectors finished higher on the week, led to the upside by Energy ( XLE ) stocks while consumer-oriented stocks were among the laggards.

{kind=link}

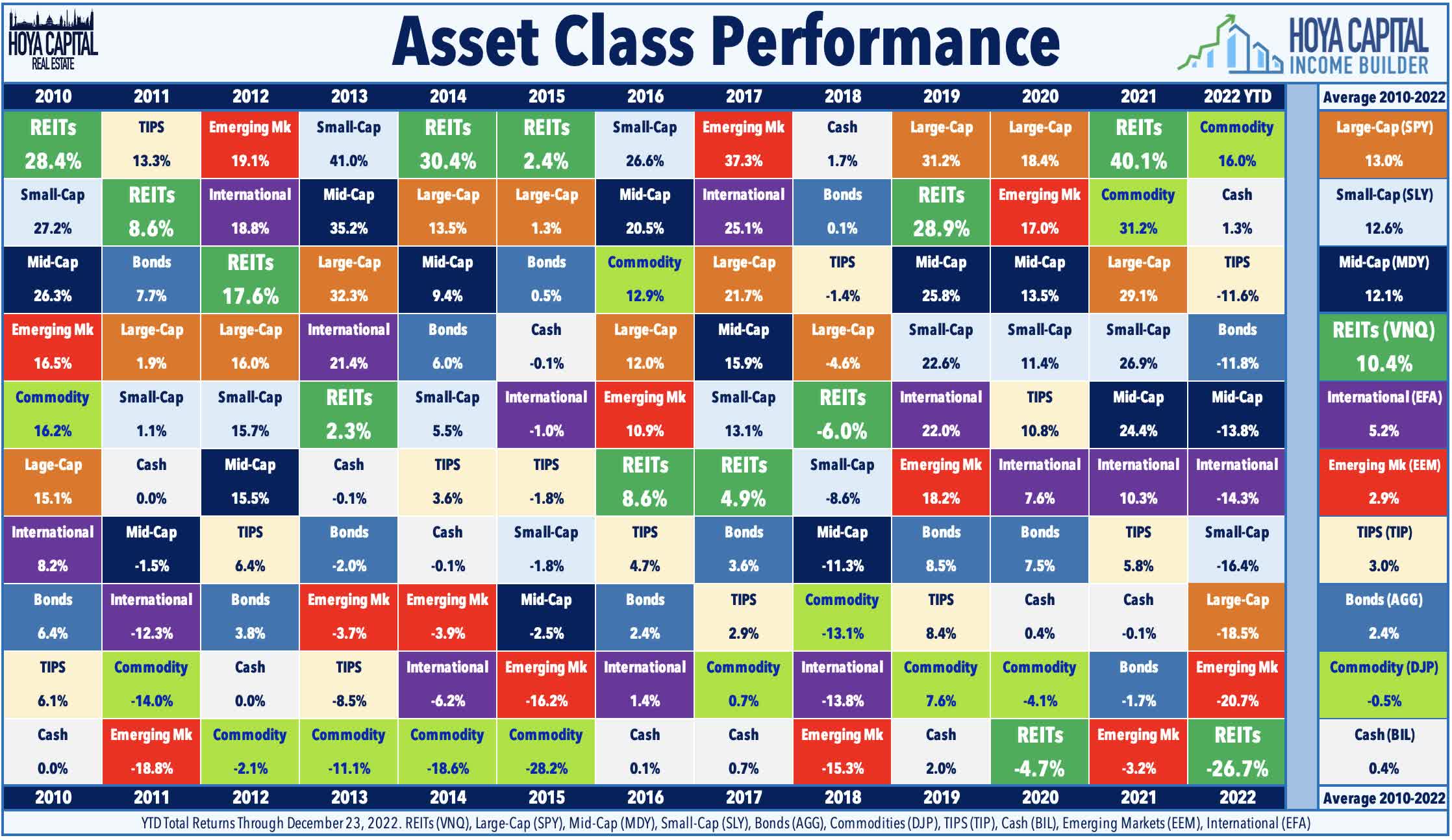

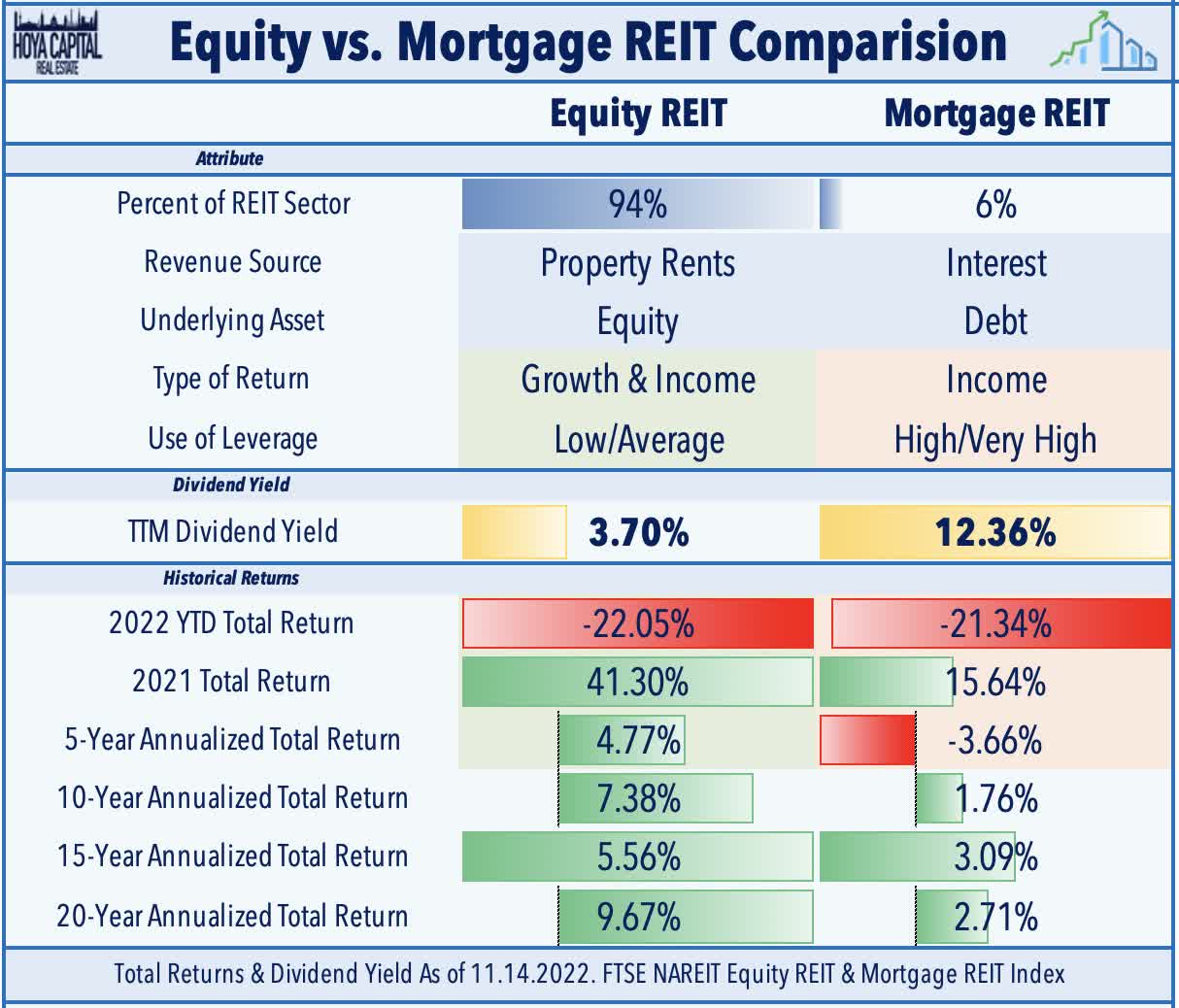

With just one week left of 2022, the Equity REIT Index is lower by 28.7% on a price return basis for the year - on pace for its second-worst year of performance behind the 37% declines in 2008 - while the Mortgage REIT Index is lower by 30.8%. This compares with the 19.4% decline on the S&P 500 and the 14.3% decline on the S&P Mid-Cap 400. At 3.75%, the 10-Year Treasury Yield has surged 224 basis points since the start of the year, but is well below its 2022 highs of 4.30%. Despite the rebound over the past month, the US bond market is still on pace for its worst year in history with a loss of 12.1% on the Bloomberg US Aggregate Bond Index, which is 4x larger than the previous worst year back in 1994 (-2.9%).

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

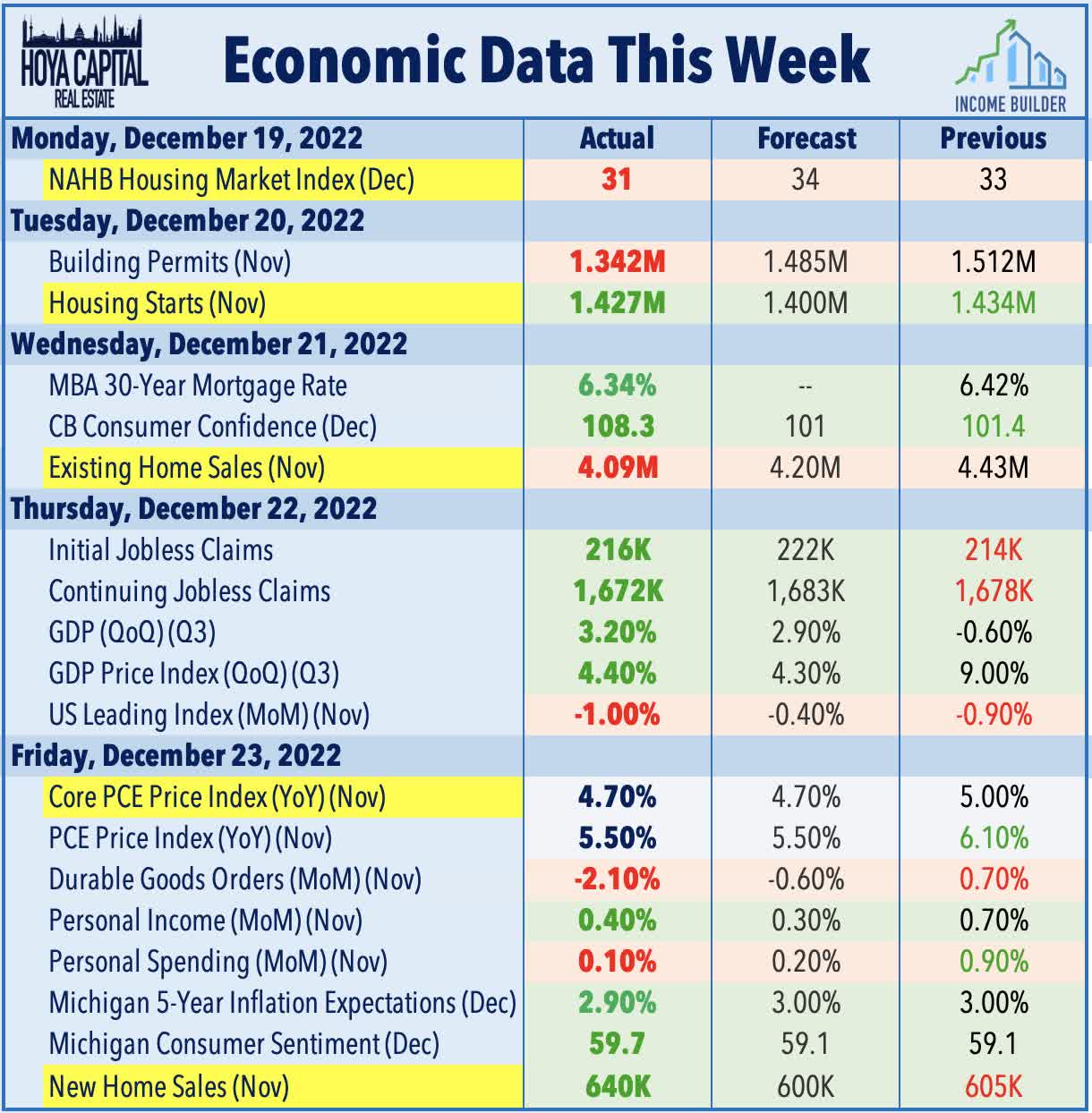

While "peak" inflation now appears firmly in the rear-view as the effects of pandemic-era fiscal expansion fade, there remains an unanswered question about whether "trend inflation" ultimately settles back in the 2-3% pre-pandemic range or at an elevated 3-5% sustained level - the answer to which has significant implications for central bank policy and financial asset values. Personal Consumption Expenditures data this week pointed more to the former with the Core PCE posting a 0.17% month-over-month increase in November - a 2.0% annualized rate - which pulled the year-over-year increase to the lowest since late 2021. The cooler-than-expected PCE print follows data last week showing that the CPI-ex-Shelter Index - the metric that showed the surge in inflation a year before it was reflected in the headline CPI - was negative for the fourth month in the past five, recording one of the most deflationary five-month periods for that particular metric on record.

{kind=link}

Cooling rate pressures can't come soon enough for the U.S. housing sector, which continues to bear the brunt of the impact of extreme monetary tightening that has more-than-doubled the interest rate for a conventional 30-Year Fixed Mortgage. A busy slate of data this week showed a deepening "winter chill" across the housing industry, underscored by a 10th straight monthly decline in existing home sales to the lowest levels in over twelve years - excluding the brief dip during the 'shutdown months' in early 2020. Notably, the -35.4% plunge in sales was the sharpest year-over-year decline on record, exceeding that of the 2008 housing crisis which saw a peak year-over-year decline of -30.3% in January 2008. The median existing-home sales price dipped to $370,700 in November - down 10.4% from the peak in June 2022. New Home Sales, meanwhile, unexpectedly climbed in November as builders have been more proactive in offering price reductions, but sales were still lower by more than 15% from the prior year.

{kind=link}

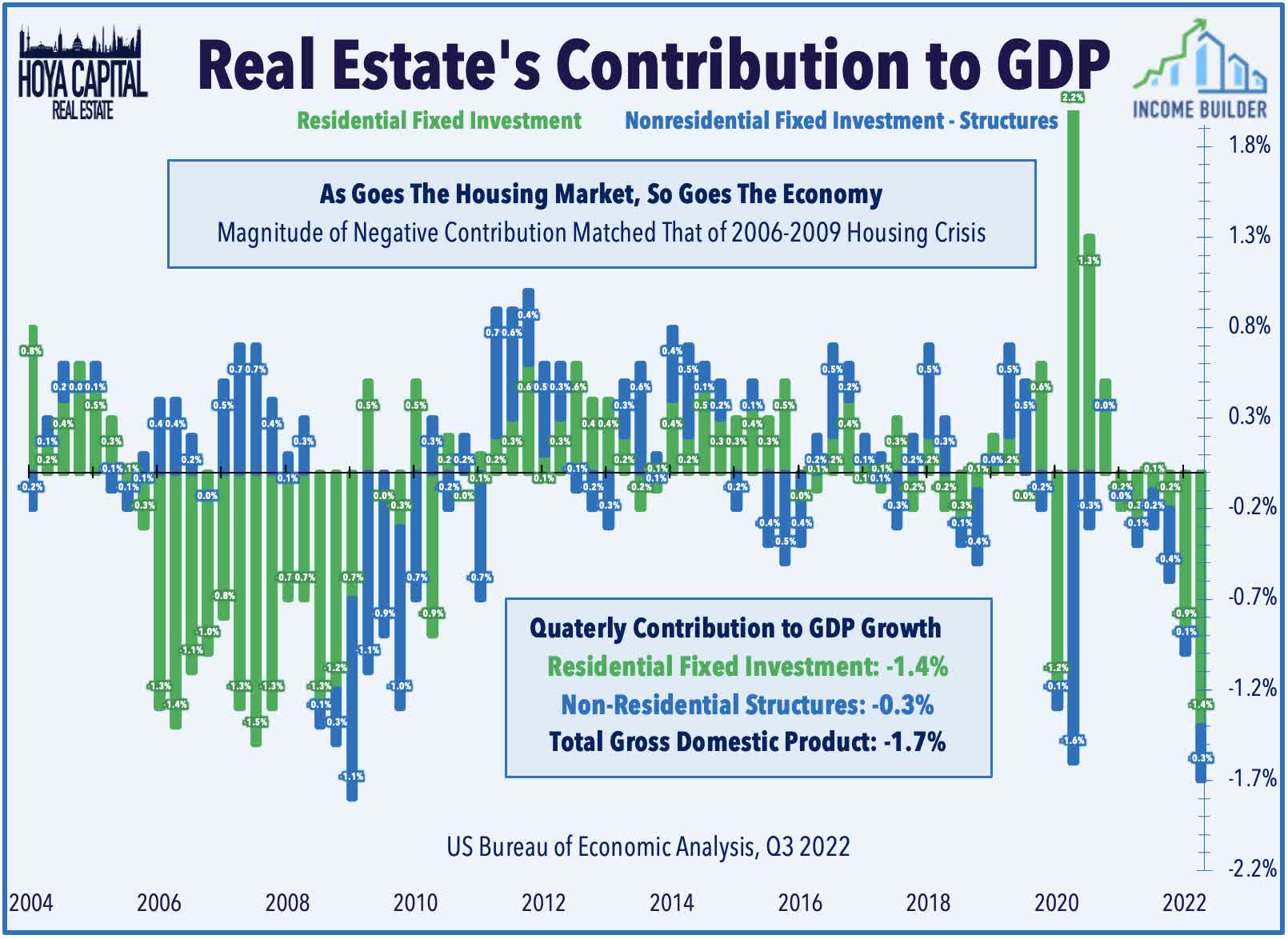

Notably, revised Gross Domestic Product data this week showed that Residential Fixed Investment was responsible for a 1.42% drag on third-quarter GDP - the second worst quarterly contribution for the housing industry behind the 1.54% drag in Q4 2007. Census Bureau data showed that Housing Starts tumbled 16% from last year to the lowest levels in over two years while Building Permits dipped 22.4% from last year to the lowest level since June 2020. Exposing a paradox in the central bank approach to tame inflation, the resulting pull-back in housing development is likely contributing to a higher longer-term level of housing inflation - which has been driven primarily by a lack of housing supply resulting from a decade of historic underinvestment. Symptomatic of this dynamic, housing inventory levels have remained near historic lows despite the sharp drop-off in demand over the past several months. The months supply of Existing Homes remained at just 3.3 months in November - still well below historical averages - while the Median Number of Months on the Sales Market for Newly Completed Homes stood at just 1.6 months - barely above the record-lows in October of 1.5 months.

{kind=link}

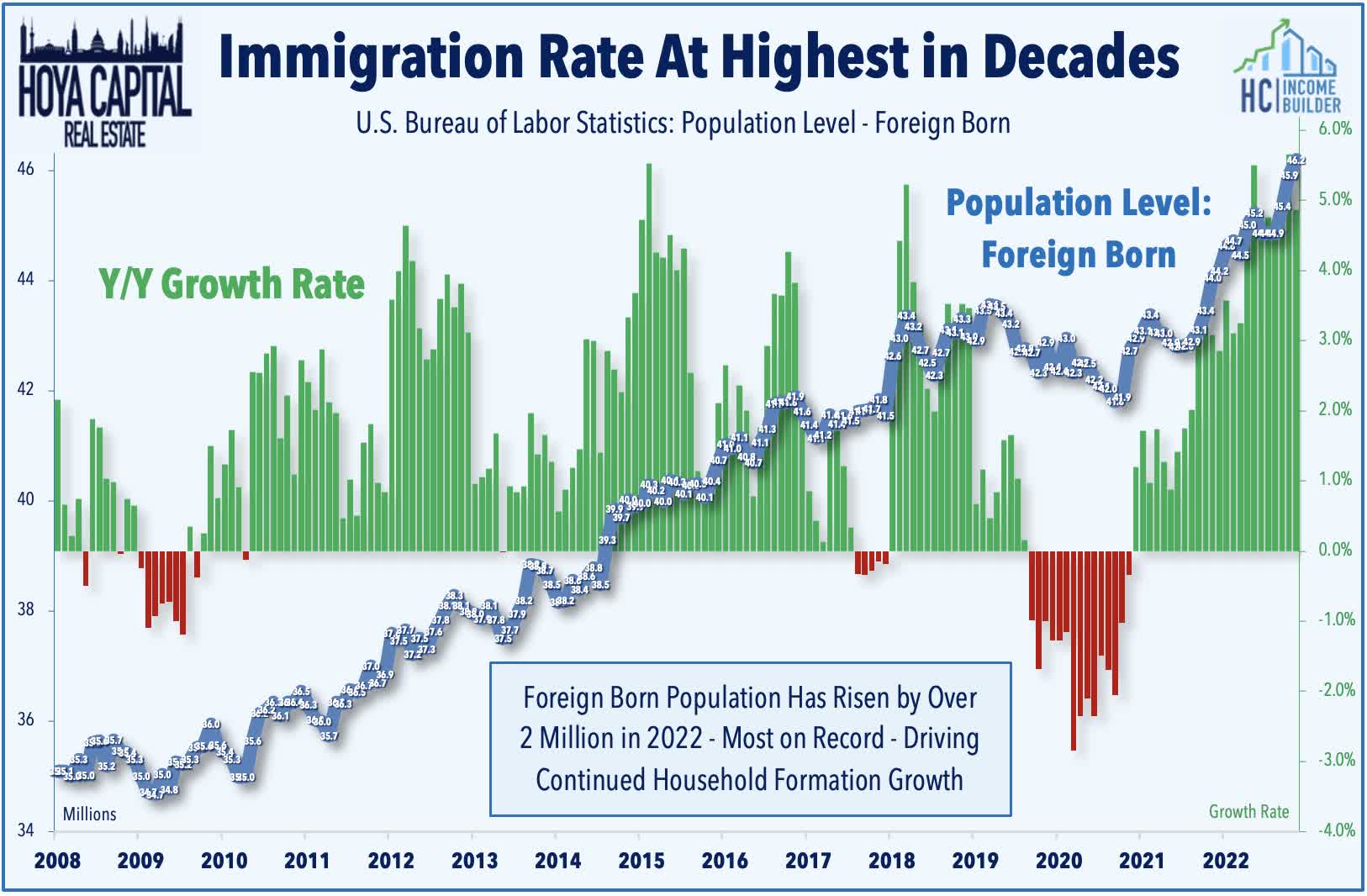

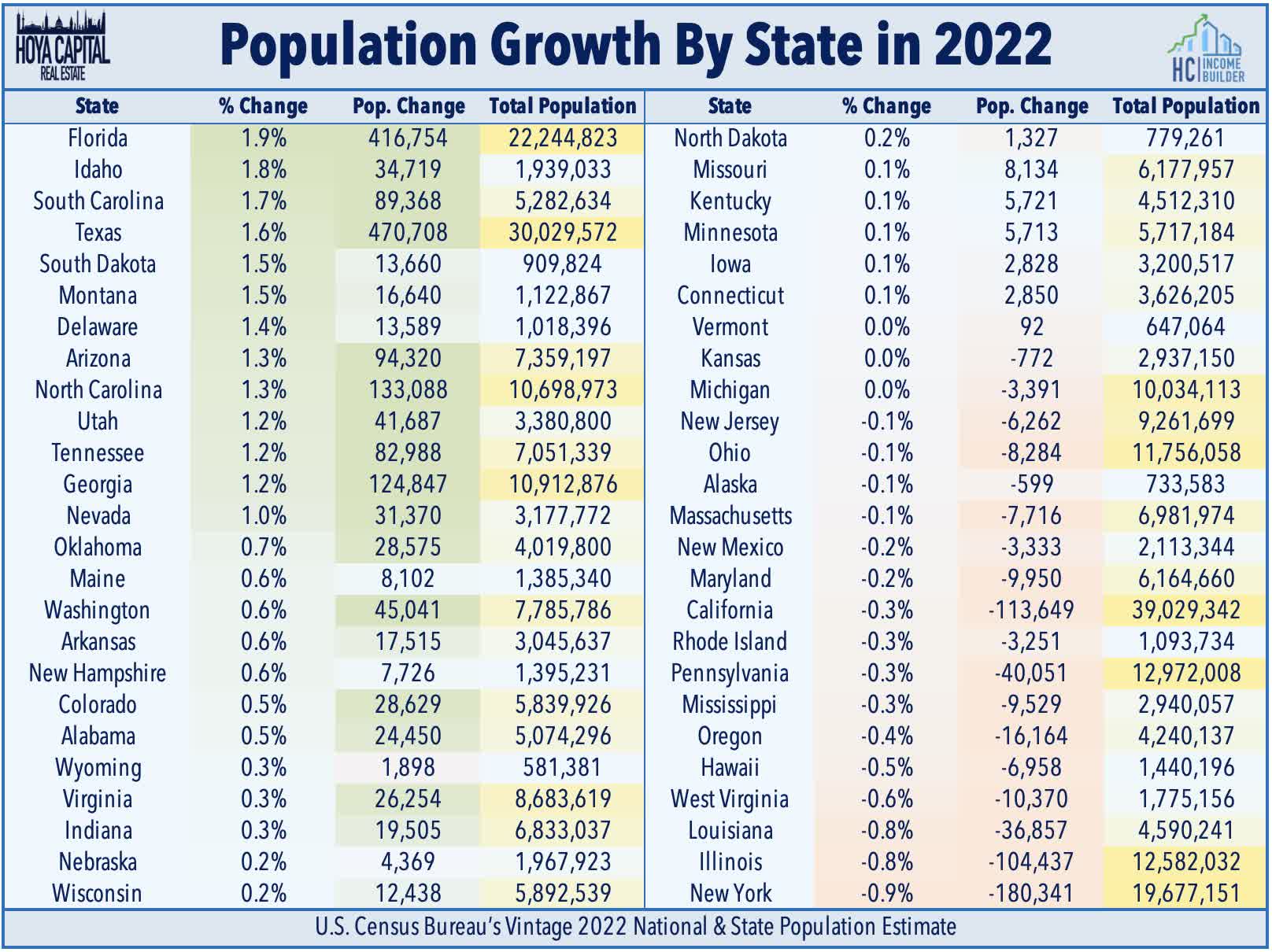

This discussion is particularly timely given the release of the Census Bureau's annual population estimates data this past week which showed that the U.S. population growth rebounded in 2022 driven by a significant rebound in net international migration to the United States - a theme that we've discussed over the past several months in our reports on apartments and homebuilders. Net international migration added more than a million people to the U.S. population between July 1, 2021 and July 1, 2022 - a 168.8% increase from the prior year - marking the largest single-year increase since 2010. Net international migration added 1,010,923 people between 2021 and 2022 while "natural change" (births minus deaths) increased the population by 245,080. Interestingly, despite the sharp housing cooldown, household formations remain on a positive trajectory this year driven by this net population growth - challenging two core tenants of housing skeptics' prognoses.

{kind=link}

Diving deeper into the newly-released Census data, we observe that Florida was the fastest-growing state in 2022 on a percentage basis with an annual population increase of 1.9% while Texas earned the top spot on an absolute basis with the addition of nearly a half-million new residents. New York saw the highest outflows on both a percentage basis and an absolute basis, losing nearly 1% of its total population this past year. California and Illinois also recorded six-figure decreases in the resident population. At the regional level, the South was the fastest-growing and the largest-gaining region last year, increasing by 1.1% while the West region recorded an annual increase of 0.2%. The Northeast and the Midwest regions, however, recorded population declines of -0.4% and -0.1% residents, respectively.

{kind=link}

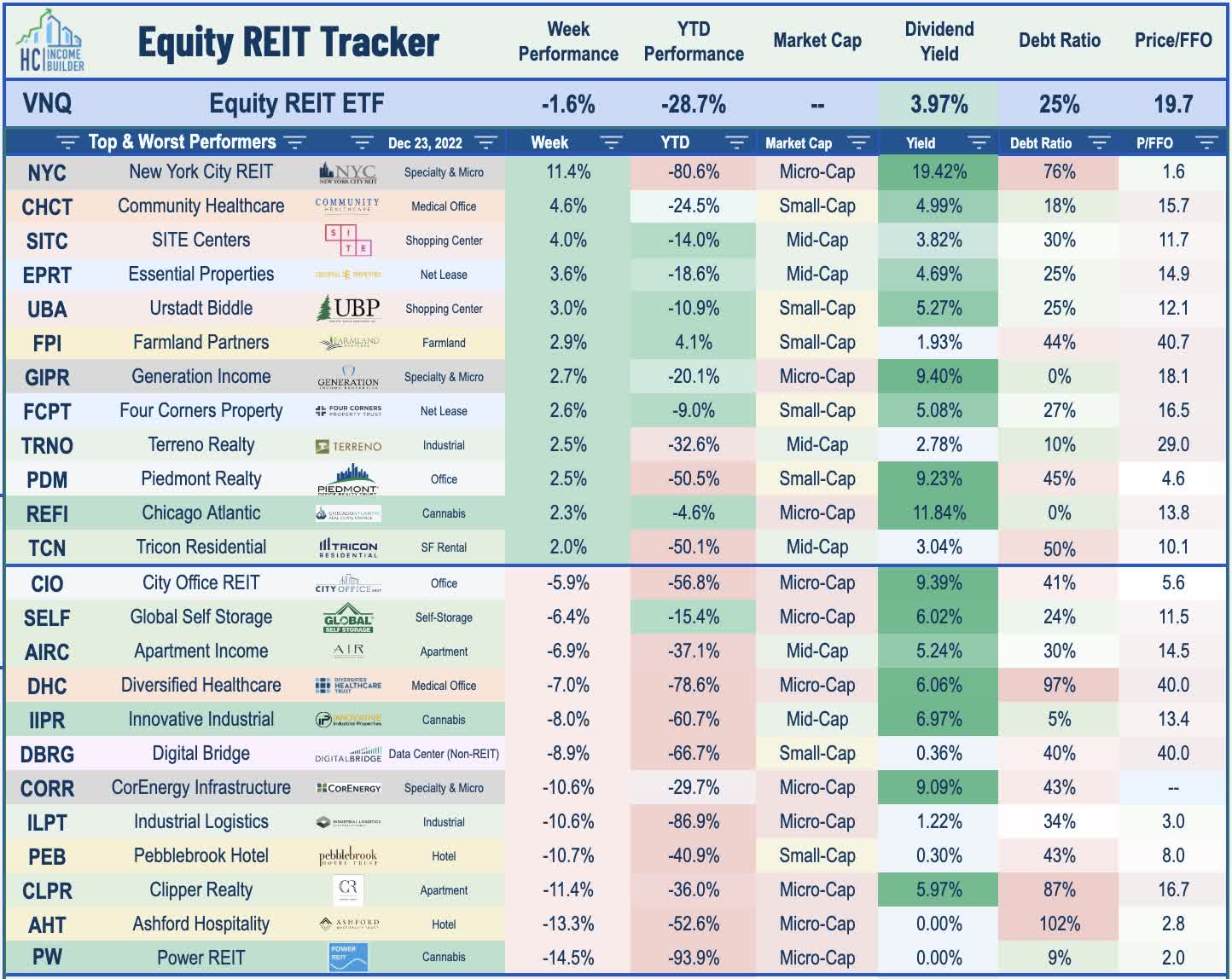

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

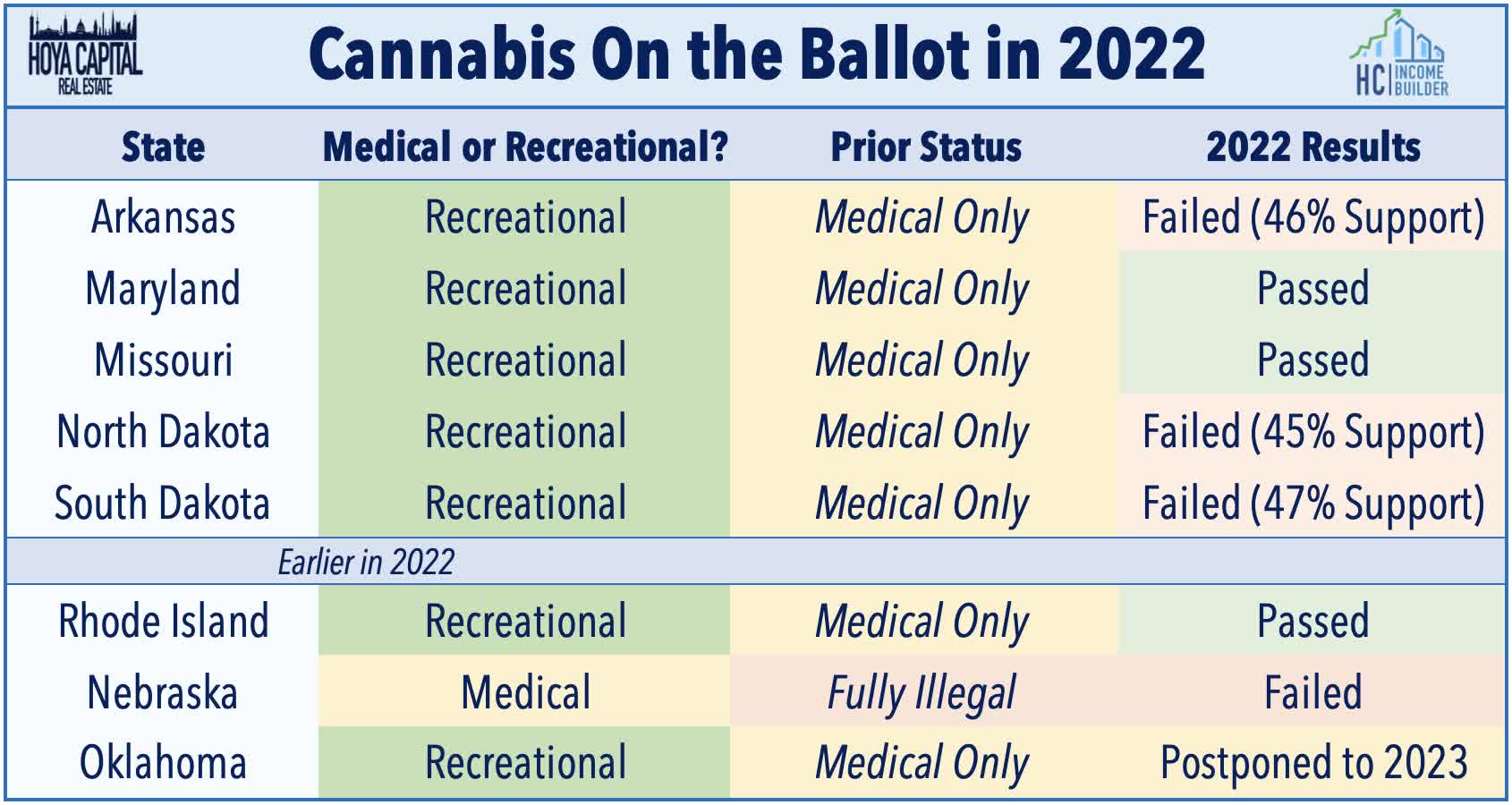

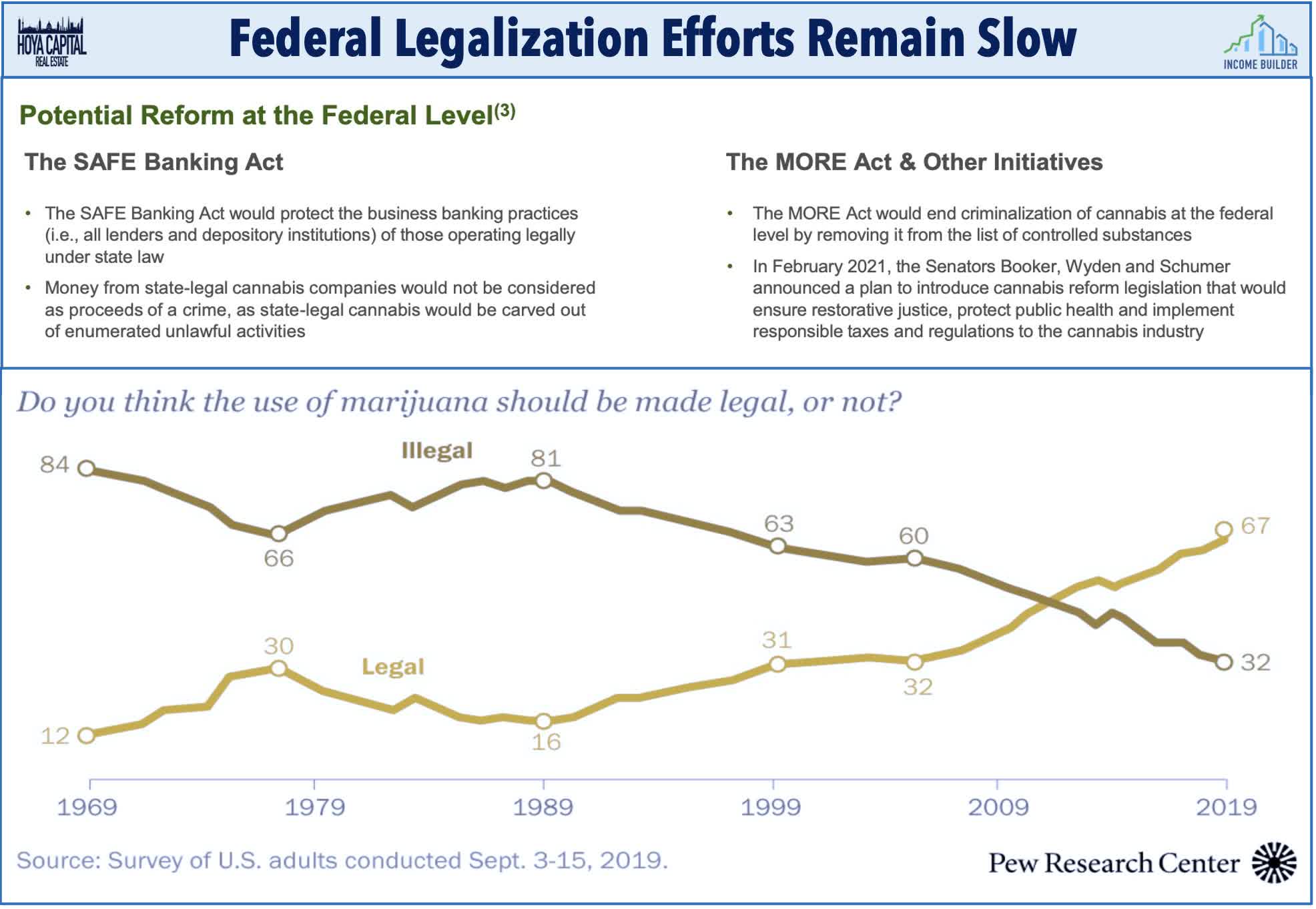

Cannabis : Cannabis REITs Innovative Industrial ( IIPR ) and Power REIT ( PW ) were sharply lower this past week after the omnibus federal spending package excluded the SAFE Banking Act - dimming hopes that any major federal marijuana legislation will be passed during the Biden Presidency. The Secure and Fair Enforcement ("SAFE") Banking Act was designed to protect banks and other financial institutions from penalties for providing services to legitimate cannabis businesses that operate legally under state law. As we'll analyze in our updated cannabis REIT report next week, two more states approved recreational marijuana usage in the 2022 elections - Maryland and Missouri - while legalization narrowly failed in three states - Arkansas, North Dakota, and South Dakota. 21 states now allow recreational cannabis usage.

{kind=link}

Stalled progress on federal legalization has made a challenging fundraising environment enough tougher for struggling cannabis cultivators and retailers. Despite the trifecta of Democrat control in Washington, the once-ambitious legalization efforts have been defined by " broken promises " according to the industry's lobbying group, the National Organization for the Reform of Marijuana Laws. These challenging conditions have led to emerging pockets of stress across the industry including a handful of bankruptcies among smaller operators - including several REIT tenants - but the legal "grey area" does continue to provide cannabis REITs with an interesting niche to be primary capital providers and "first movers" in a relatively high growth industry.

{kind=link}

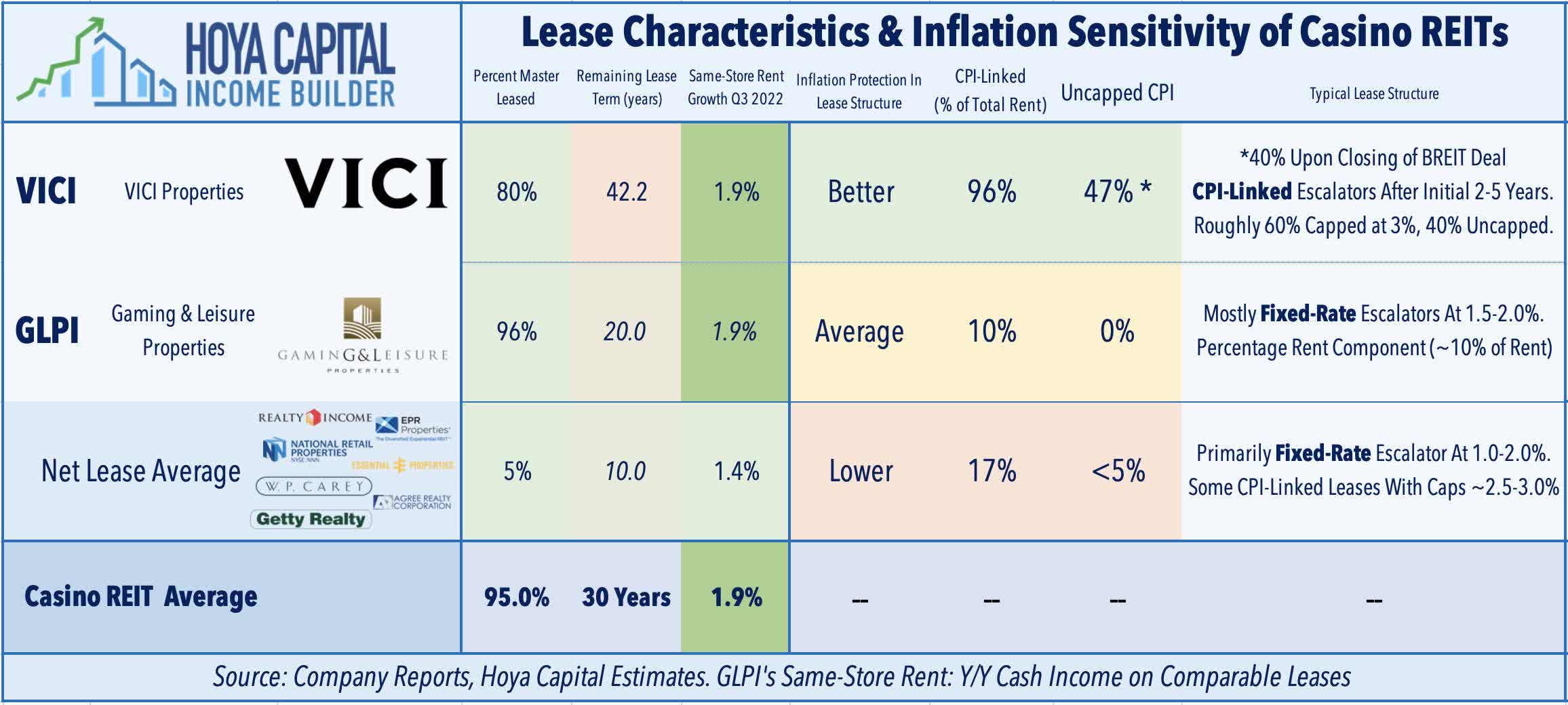

Casino: The busy month of M&A continued for VICI Properties ( VICI ), which announced this week that it acquired two casinos in Mississippi - the Fitz and the WaterView - for $293.4M from Foundation Gaming - an implied cap rate of 8.3%. VICI's master lease with Foundation has an initial annual rent of $24.25M and an initial term of 15 years, with four five-year tenant renewal options. The rent escalates at a 1.0% rate in years 2-3 and at the greater of 1.5% or CPI (subject to a 3.0% cap) beginning in year 4. Earlier in the week, VICI finalized a lease with Hard Rock following its acquisition of the operations of the Mirage Hotel & Casino, which received regulatory approval last Friday. Annual rent for the Mirage will total $90.0M with an initial term of 25 years plus three 10-year tenant renewal options. Rents escalate annually by 2.0% for the first 10 years and will transition to a CPI-based formula in year 11. Last week in Casino REITs: Hold 'Em As Others Fold 'Em we discussed the inflation-hedging characteristics of VICI Properties and Gaming and Leisure's ( GLPI ) lease portfolio and these casino REITs' external growth prospects.

{kind=link}

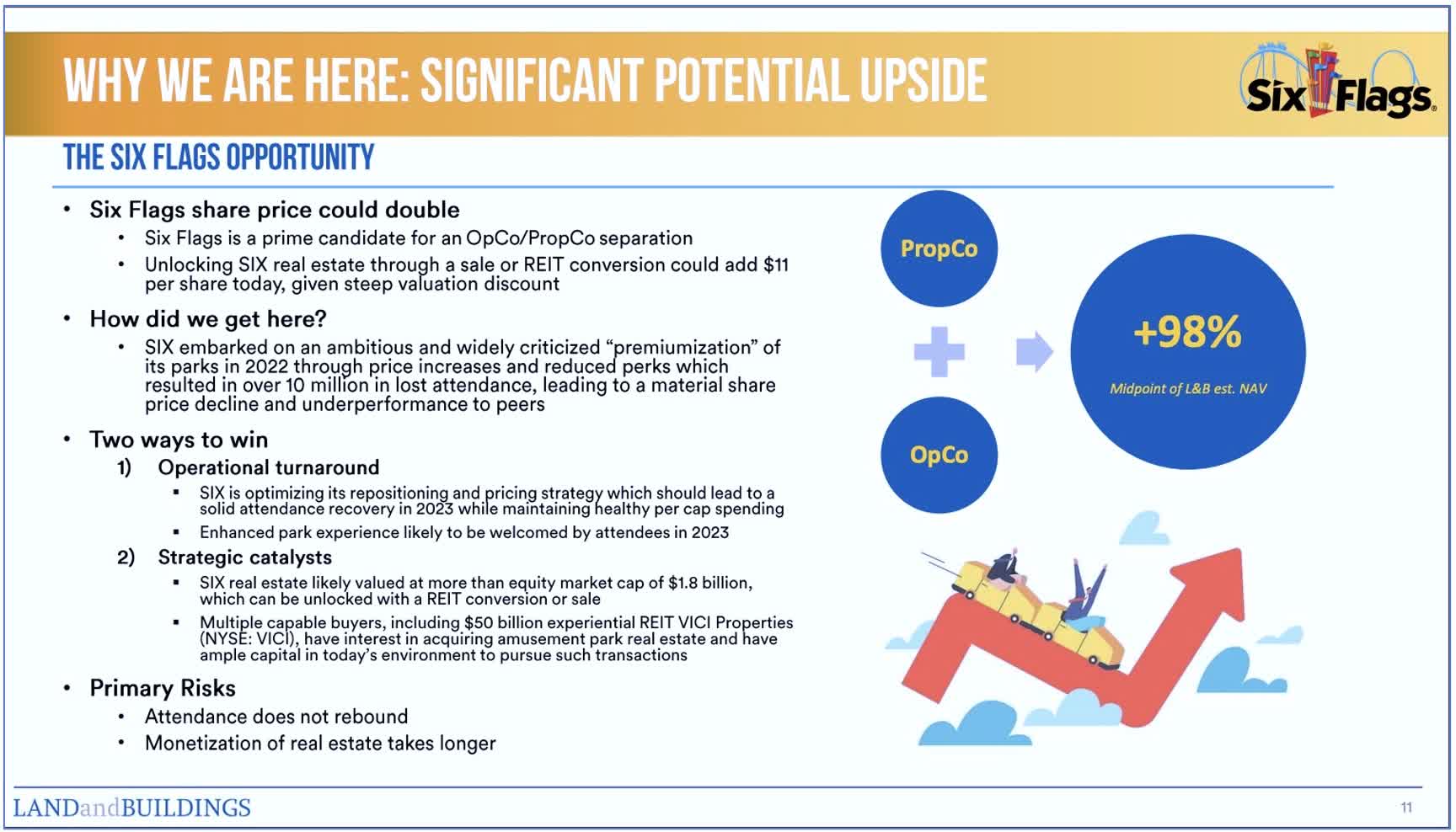

Net Lease : On a related note, activist firm Land & Buildings posted a presentation outlining a proposed strategy for Six Flags Entertainment ( SIX ) to "unlock substantial value by executing a strategy to monetize real estate while also driving an operational turnaround." The report speculated that VICI Properties , Gaming and Leisure , Realty Income ( O ), and EPR Properties ( EPR ) could be potentially interested buyers under a sale-leaseback strategy. Six Flags owns and operates 17 parks across North America and L&B believes that Six Flags is a "prime candidate for an Opco/Propco separation and that its real estate is likely valued at more than the Company's entire current equity market capitalization of approximately $1.8 billion." SIX explored monetizing its real estate in the mid-2010s through a REIT structure, but did not move forward with the plan but noted that it "could revisit the idea in the future."

{kind=link}

Sticking with the activist theme, Global Net Lease ( GNL ) and Necessity Retail REIT ( RTL ) were in focus this week after activist firm Blackwells Capital advanced an ongoing proxy battle by filing a lawsuit against the two REITs - both externally managed by AR Global - after the REITs rejected the firm's director candidate nominations. Blackwells - one of the largest shareholders in GNL - launched a proxy battle earlier this year proposing to terminate the external management agreement with AR Global, citing its relatively high-cost structure and potential conflicts of interest. Blackwells alleges that AR Global is attempting to use amendments to the bylaws in July 220 to "prevent stockholders from voting for Blackwells' two qualified nominees who would improve governance, hold the external manager and the company accountable, and support efforts to maximize value for stockholders." In addition to GNL and RTL, AR Global is also the external advisor to New York City REIT ( NYC ) and Healthcare Trust ( HTIA ).

{kind=link}

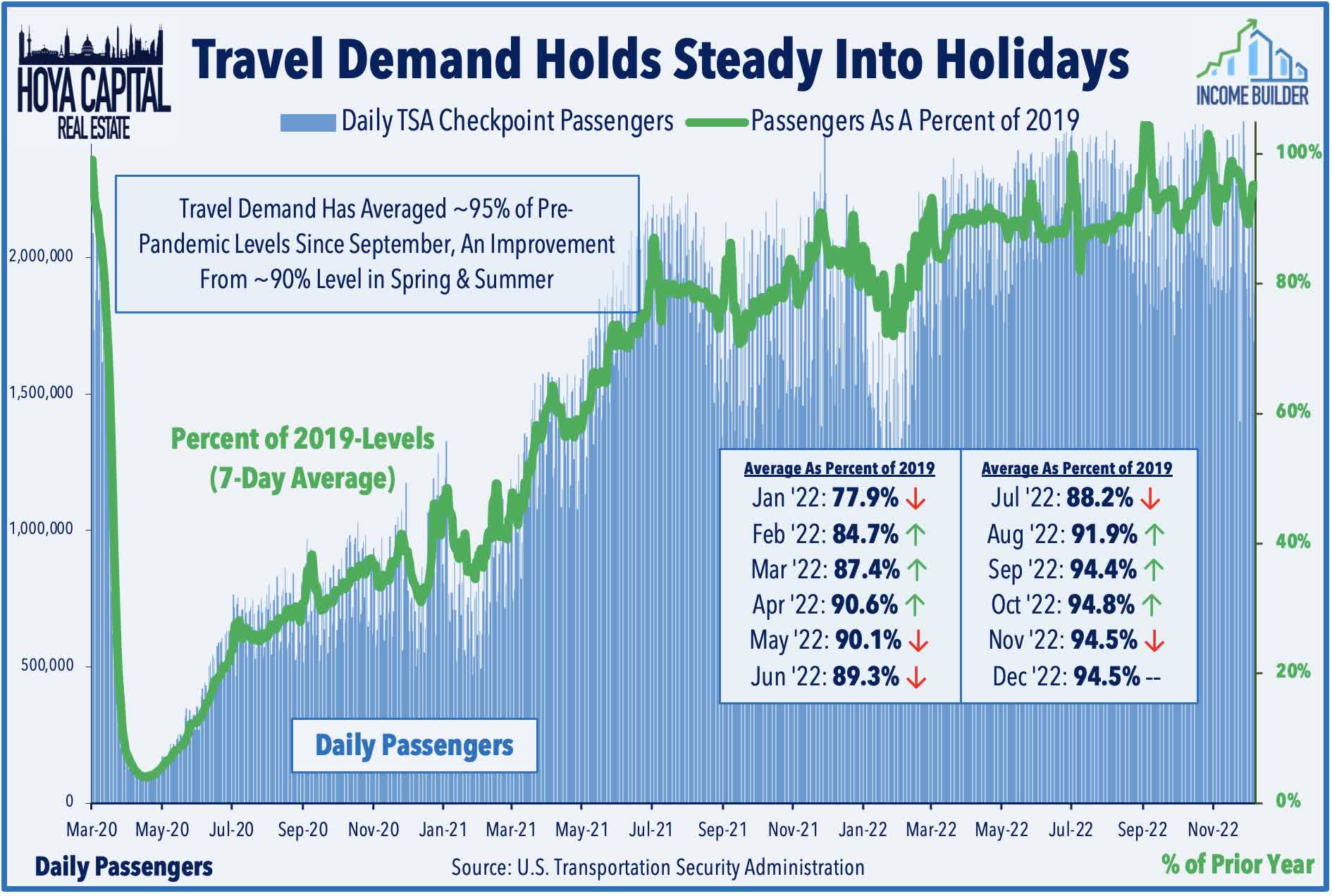

Hotels : Ahead of the critical holiday travel season - one that will be impacted by the "bomb cyclone" sweeping the continent - a trio of hotel REITs provided business updates. Pebblebrook Hotel ( PEB ) dipped more than 10% after it downwardly revised most of its earnings metrics for Q4 citing "a negative impact from Hurricane Nicole and weaker business and leisure demand during the second half of November." Updates from Park Hotels ( PK ) and Ryman Hospitality ( RHP ) were more upbeat, however, with Park boosting its Q4 FFO outlook citing "higher than expected group business" while Ryman noted that its November RevPAR was 14.9% above 2019-levels while noting that its results are "trending toward the top end of our full-year guidance range." TSA checkpoint data shows that domestic throughput climbed to 96% of 2019-levels thus far in December - the highest since the start of the pandemic. Also this week, Apple Hospitality ( APLE ) declared a supplemental special dividend of $0.08/share - the fourth hotel REIT to declare a special dividend. TSA checkpoint shows that domestic throughput climbed to 96% of 2019 levels thus far in December - the highest since the start of the pandemic.

{kind=link}

Office : A pair of office REITs announced progress on "portfolio repositioning" initiatives this past week. Piedmont Office ( PDM ) gained 2.5% on the week after it announced that it sold two Cambridge, Massachusetts assets - One Brattle Square and 1414 Massachusetts Avenue - for total proceeds of roughly $160M. Proceeds were used to pay off the outstanding balance on its $600M line of credit, leaving the full capacity of the line currently available. The firm noted that the sales were a "crucial step in our asset recycling strategy" in which it has sold assets in its coastal markets and invested in Sunbelt markets. Empire State Realty ( ESRT ) gained about 1% on the week after the NYC-focused REIT provided a business update in which it announced that it acquired a multifamily asset in Manhattan for $115M while reaching deals to sell an office building in White Plains, NY for $42M and in Harrison, NY for $53M. The firm commented that the deal is "consistent with our plan to recycle our balance sheet and add well-located NYC multifamily assets."

{kind=link}

Healthcare : Medical Properties Trust ( MPW ) was in focus this week after its largest tenant - Steward Health Care - completed the extension of its credit deal with its lenders through December 2023. MPW has become a fiercely contested "battleground stock" in recent months after coming into the cross-hairs of several vocal short-selling firms, which have focused their critique on the financial health and complex relationship between MPW and Steward and the broader pressure on hospital operators this year. Steward Chairman and CEO Ralph de la Torre commented, "The extension of our ABL coupled with our re-engineered structure position us extraordinarily well for the coming year." MPW gave back its gains, however, after S&P Ratings put the company on watch for a downgrade to its BB+ credit rating, citing its increased tenant concentration to Steward. Welltower ( WELL ) was a leader this week, however, after it closed on the first part of its real estate joint venture with Integra Health, which will eventually transfer a 15% ownership stake in 147 skilled nursing facilities to Integra Health from ProMedica.

{kind=link}

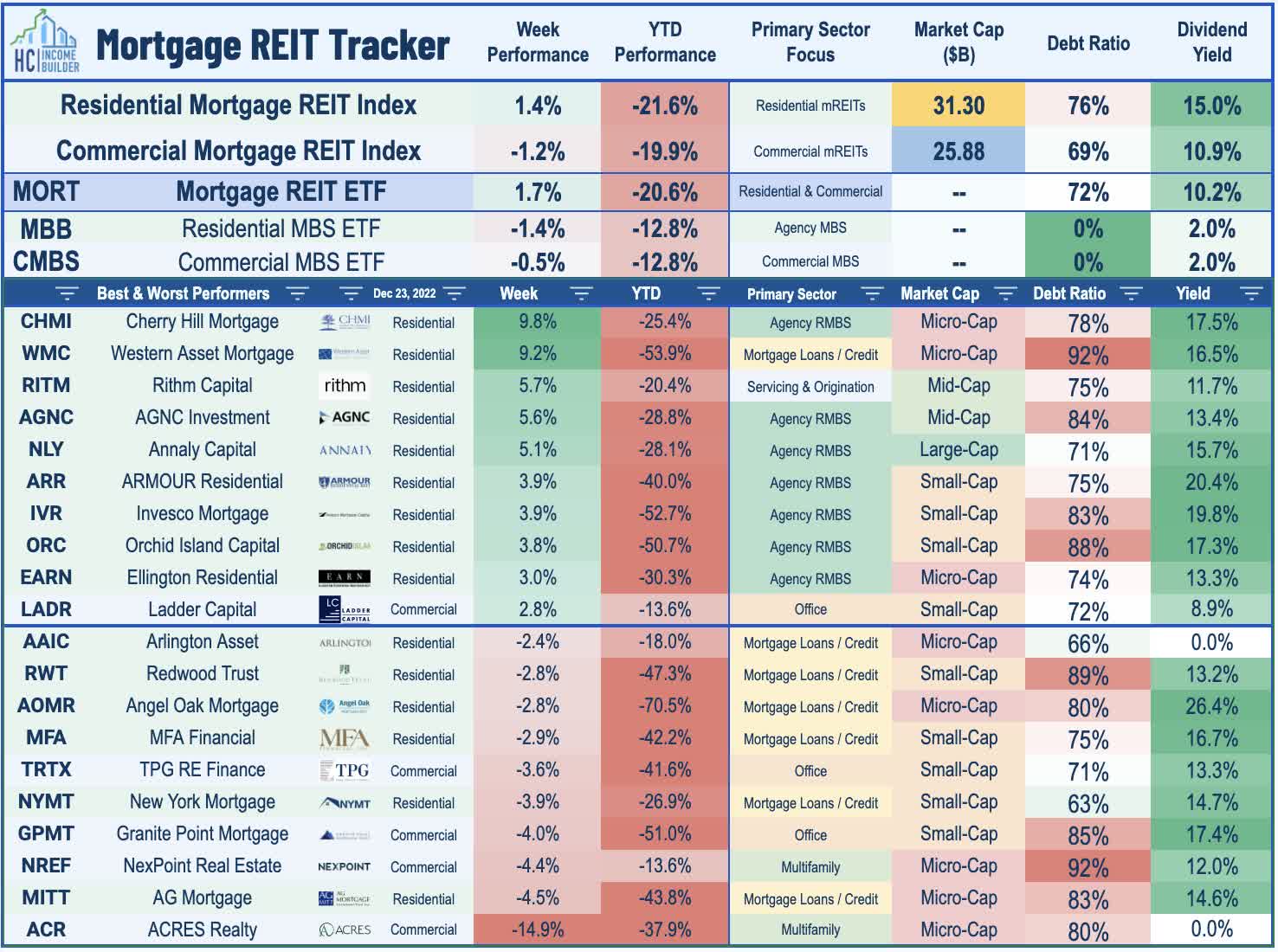

Mortgage REIT Week In Review

Mortgage REITs were mostly higher this past week with the iShares Mortgage Real Estate Capped ETF ( REM ) advancing nearly 2% - led by a rally in several of the largest residential mREITs including Annaly ( NLY ), AGNC Investment ( AGNC ), and Rithm Capital ( RITM ) - each of which gained more than 5%. Ellington Financial ( EFC ) was among the leaders this week after it reported that its book value per share ("BVPS") was $14.89 as of November 30 - up 0.2% from October 31 - while also holding its monthly dividend steady at $0.15/share. Western Asset Mortgage ( WMC ) rallied more than 9% after holding its quarterly dividend steady at $0.40/share , while Invesco Mortgage ( IVR ) gained 4% after holding its quarterly payout steady at $0.65/share . Angel Oak ( AOMR ), meanwhile, lagged after it reported that its BVPS was $9.40 as of November 30 - down about 12% from the end of September.

{kind=link}

A pair of mREITs trimmed their payouts, however, including Ready Capital ( RC ) - which declined 6% after it trimmed its quarterly dividend to $0.40/share from $0.42/share - and MFA Financial ( MFA ) - which slipped 4% after trimming its quarterly dividend to $0.35/share - down from a $0.44/share. Elsewhere, Rithm Capital ( RITM ) dipped 9% despite holding its dividend steady and announcing a new repurchase program of up to $200M in common stock and $100M in preferred stock - replacing an expiring program of the same size. Last month, we published Mortgage REITs: High Yields Are Fine, For Now , which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

{kind=link}

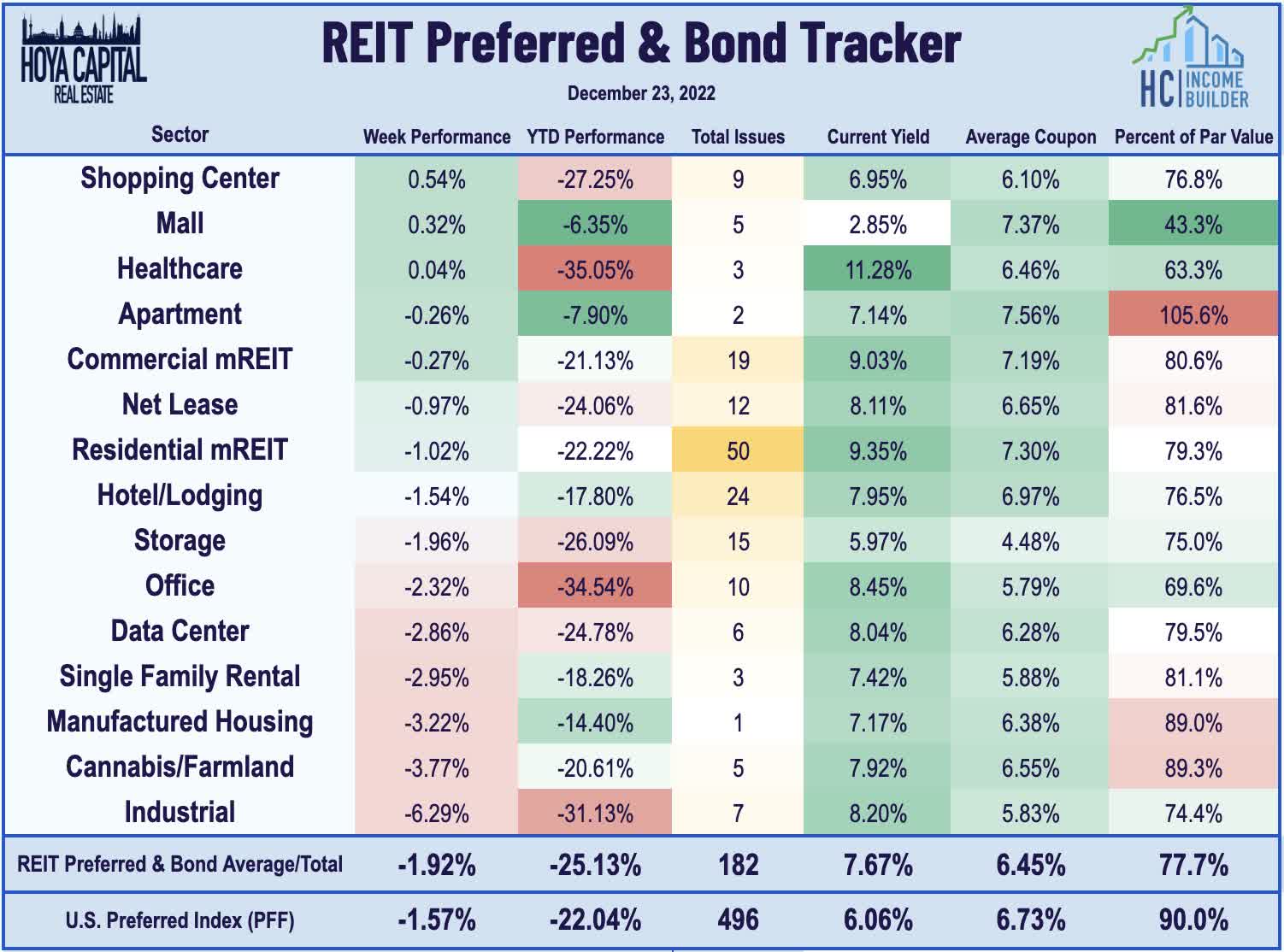

REIT Capital Raising & REIT Preferreds

Pressured by the jump in benchmark interest rates, The REIT Preferred Index ( PFFR ) declined 1.9% this week, lagging behind the broader iShares Preferred and Income Securities ETF ( PFF ) which ended the week lower by 0.9%. This week, small-cap Creative Media & Community Trust ( CMCT ) - a California-focused office REIT formerly known as CIM Commercial - announced that it will redeem all outstanding shares of its 5.5% Series L Convertible Preferred stock on January 25, 2023 at its stated value of $28.37/share. Also of note, PS Business Parks - which was acquired by Blackstone's ( BX ) BREIT subsidiary this past April - officially de-listed its three preferred securities after concluding a controversial tender offer for those shares at a deep discount to par value. Wheeler Real Estate ( WHLR ) - another firm responsible for a controversial acquisition that resulted in losses for preferred shareholders - announced the extension of its exchange offer of its 8.75% Series D Cumulative Convertible Preferred Stock - for newly-issued 6.00% Subordinated Notes due 2027.

{kind=link}

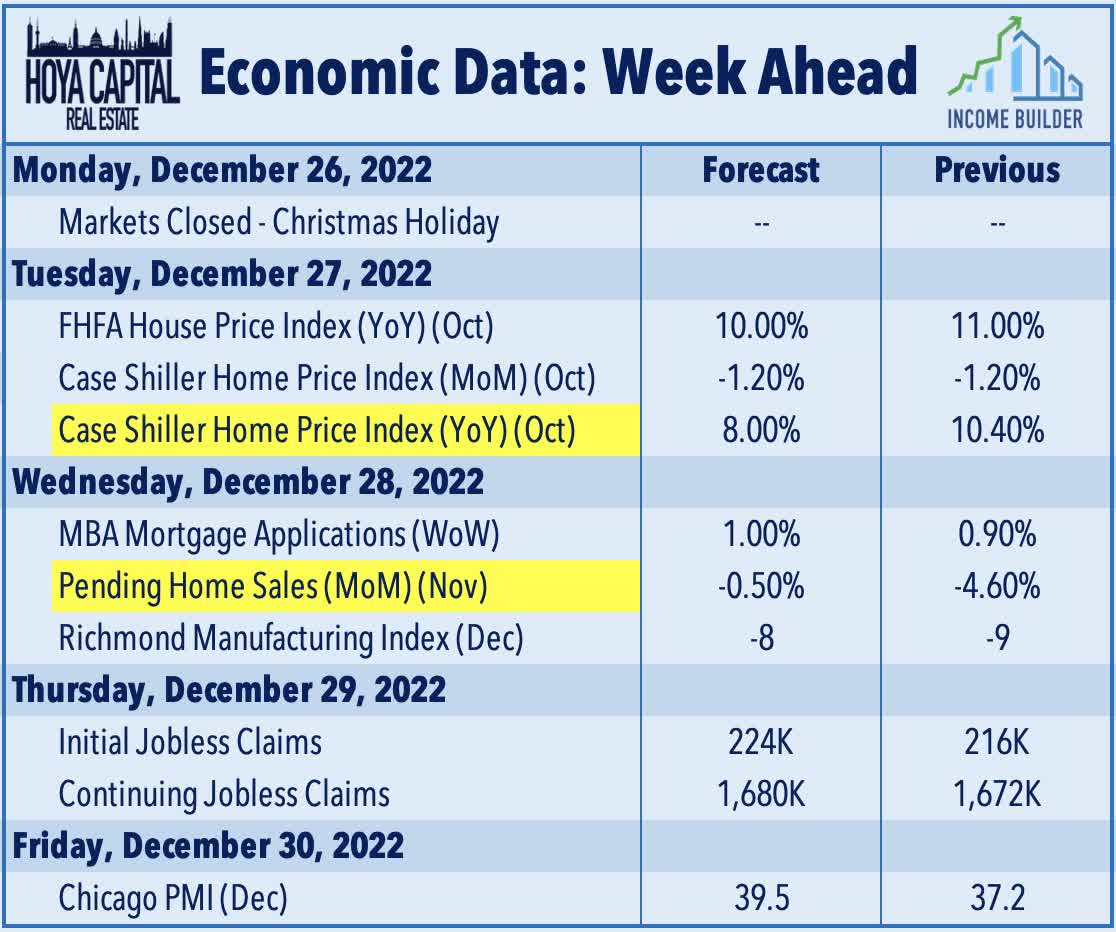

Economic Calendar In The Week Ahead

The economic calendar slows down in the holiday-shortened week ahead with both U.S. equity and bond markets closed on Monday. On Tuesday, we'll see the Case Shiller Home Price Index and the FHFA Home Price Index , each of which are expected to show a fourth-straight month-over-month decline in home prices. Last month, the Case Shiller Index recorded the largest single-month decline since November 2011 while some home price indexes - including the NAR's Median Price of Existing Homes - are showing double-digit price declines from their early 2022 peak. On Wednesday, we'll see Pending Home Sales data for November which is expected to decline for a sixth-straight month to the lowest levels since 2012 as the 30-Year Fixed Rate Mortgage peaked during the week of November 10th at 7.08% before pulling back to 6.27% this past week. Markets will be closed on Monday, January 2nd in observance of New Year's Day.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

'Winter Chill' Dims Holiday Cheer