DNNGY - Ørsted: I Own Shares And Have Sold Options This Is A 'Buy'

Summary

- Ørsted is becoming more and more interesting. As of the latest results, we have some pressure on the company's stock price, seeing it push down to the sub-600 DKK level.

- I believe this represents a material undervaluation to the long-term earnings and return potential. Because of this, I bought shares back below 600 DKK.

- I also took advantage of the volatility and wrote several PUT options on the company, enhancing my income and making it possible to potentially buy at below 550.

- Learn my thesis on Ørsted for 2023.

Dear Readers/Followers,

Ørsted A/S (DNNGY) is still the world's leading renewable company with attractive segments and projects worldwide. While this segment comes with decent amounts of volatility, the underlying value in the current environment/context seems to me to be absolutely clear. The company has very specific ownership circumstances that, if you consider it in a certain way, could make it one of the safer energy investments around. Not the greatest yielder for sure, but a damn good investment nonetheless - and the yield part is one thing I'm going to address here in this article.

The company recently issued some information that caused the company's share price to drop - so let's recap and give this business a thesis for 2023.

Ørsted A/S for 2023 - an attractive business

Ørsted A/S remains an ESG play and one of the most significant in the world. From being a legacy-focused energy play in large part owned by the Danish state, it has become one of the most innovative and ESG-focused energy businesses out there, focusing on wind farms, solar farms, renewable hydrogen, smart energy, and similar projects. This vision includes massive potential upside in the form of future renewable opportunities.

I find it relevant here to showcase the specifics of this vision, and how far the company has already come because Ørsted A/S is already the leader in offshore wind.

Orsted IR (Orsted IR)

As you can see, the company is also no slouch in any of the other segments that it seeks to lead in, and it has the fundamentals to go with it. The majority shareholding by the Danish government is something I view as fairly positive, altogether (50.1% of votes). Dividends will likely never be high or grow massively because the focus of this business is to retain low debt while growing its already-sizeable portfolio.

This should be part of your core thesis when investing - that you want to be aligning yourself with the Danish vision for a green future. This hasn't always been the case either, as Ørsted at one point was one of the coal-heaviest businesses around.

And just to be clear about market leadership - the company at this time owns over 20% of the global offshore capacity in terms of GW. It has the largest farm in all of Europe, with new capacities coming online across the globe over the next year and the next overall years.

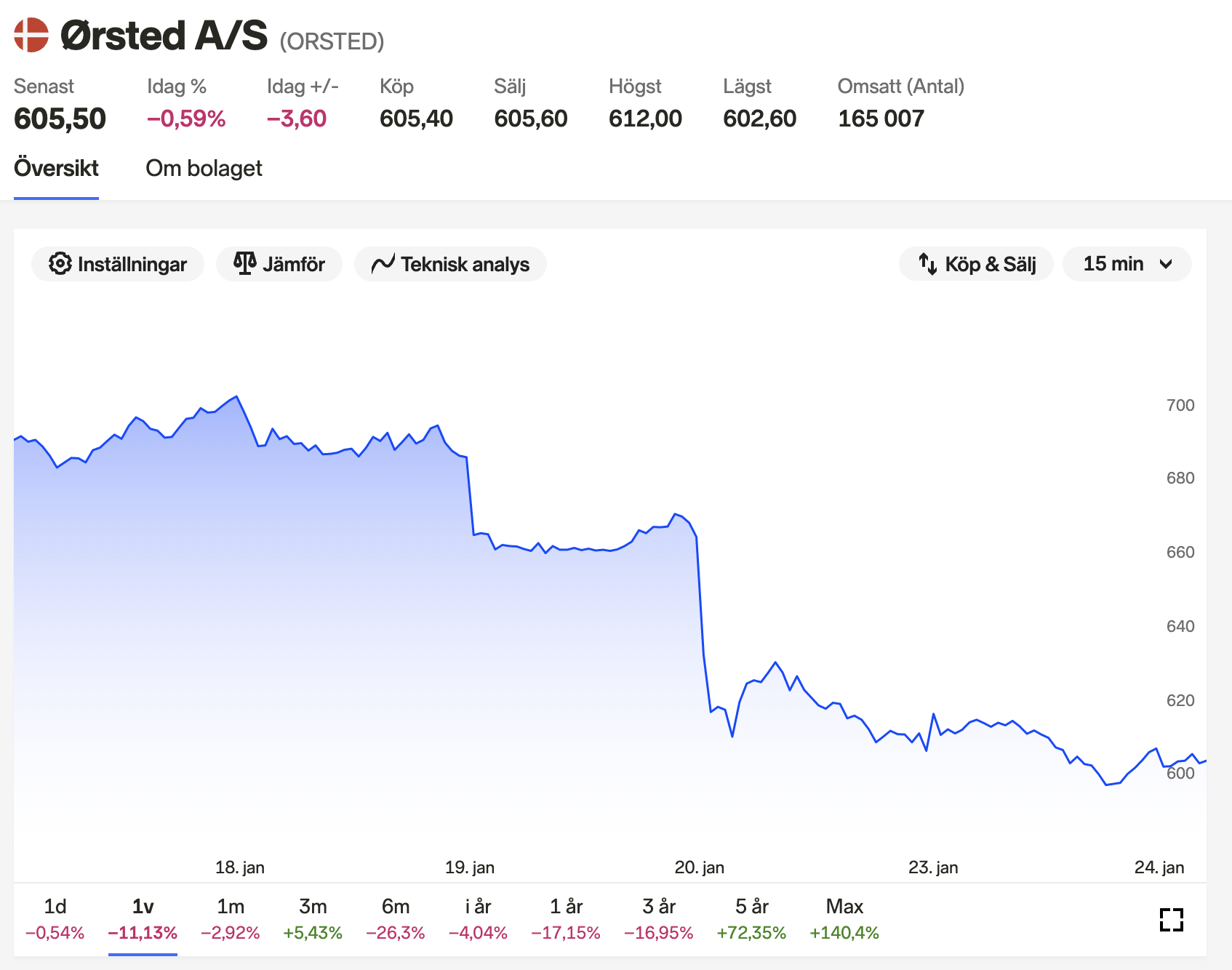

Now, the company hasn't formally announced its results for 2022, but it did give a preview which caused the share to decline by over 8% in a single day.

Why is that?

{kind=link}

Because the company declared a preliminary EBITDA of 21.1B DKK, excluding partnerships and JV's, which is a significant increase from FY21 which came in at 15.8B DKK but is not as good as the market expected. The company also cut the 2023E EBITDA, ex-partners, to a range of 20-23B DKK, which would offer no material or significant increase to 2023, including a write-down on an American partnership.

We'll have to wait for the exact numbers to arrive before making final adjustments to my valuation model, but what has happened here perfectly highlights the flaws of investing in, or forecasting a company like Orsted as high as the analysts have done here.

As a result of these preliminary results, most of the analyst houses and banks significantly cut their targets for Ørsted. However, those cuts were from the very excessive valuation levels that I've published and pointed to before. Nordea cut its target from 1000 DKK to 915 DKK. Oddo BHF cut to 730 from 800 DKK, and some other analysts also did revisions of what were once extremely exuberant targets.

Let me quote my own last article here.

Analysts remain very positive about the company in the longer term. The current average PT is now lower than my last article from S&P Global - around 800 DKK - which is down significantly from the last target.

At the current PT, the company is 16% undervalued to 800 DKK, which puts 14 out of 24 analysts at a "BUY" or equivalent target for the company. I would tendentially agree with the PT, and based on inflation and cost increases impair my previous target to around 800/share, giving the company a 16% upside to a conservative level.

(Source: Ørsted article)

I'm personally not going to cut my target, but it illustrates how quickly those analysts have dropped what was previously a 1000+ DKK price target to where it now stands, and where some are now saying less than 800 DKK or even 750 DKK.

I remind you that my own cost basis is less than 580 DKK for this stock.

I don't consider the growth thesis for Ørsted in any way broken or killed due to these revised estimates, because there were essentially already within my range of expectations and what I was modeling for. The fact that the company is government-owned is also a protection here rather than a liability. A shift to EVs and a tailwind for EVs is going to be government subsidies and support - and the Danish government is likely to continue to provide this when its a company they owned a majority stake in. That isn't to say that Ørsted cannot build without subsidies - they certainly can, because in Germany, three wind farms were built during the mid-2020s by Ørsted (2×240MW) and EnBW (1×900MW) with no subsidies at all. The most recent subsidy-free wind farm, Thor in Denmark, has been awarded to RWE.

As long as Ørsted is a market leader not only in capacity expansion but in expertise in its field, I don't foresee any fundamental issues to the company or risk factors that require massive accounting for or impairing here.

The simple truth is, the company is well ahead of smaller players in getting things to work not only in terms of capacity but in terms of cost. The typical cost structure of an offshore wind farm is 35% turbine, 25% transmission, 25% foundation, and only 15% installation. Transmission costs are charged to the operators - meaning Ørsted has control over the turbines, the foundation, and the overall installation - 3 out of 4. Tell me another 5 operators that have these advantages, and you'll realize how tricky this is to find.

Now, Ørsted doesn't give us much yield, but after the drop, it's 2.06%, which is actually fairly good as I see things. It's not sector-average for energy, but it's definitely not something to ignore any longer. Furthermore, the company has low debt, it has a BBB+ rating, and it's perfectly and 100%-aligned with where the future here seems to be going in terms of energy.

Let me show you the valuation, and how I have elected to invest in Ørsted.

Ørsted Valuation & Investing - many possibilities

So, first of all, I believe Ørsted at 600 DKK or thereabouts is undervalued. You could straight up buy the common shares, and I'd say you got a great deal. I have done this, bought some shares, and added to my position, that's now growing very impressively.

Remember, the company is essentially an alternative energy company with a potential growth story, which explains the spike it saw in the 2020 green bubble. That was a bubble, and we always need to be careful with bubbles.

Since then though, the price has come down significantly, and the returns since 2020 have been negative, and more than negative 17% in one year. That's why I haven't invested until 2022, and why my position, for the time being, is still below a full percent. Because I want to see where it goes. As of writing this article, the company recently shot up to nearly 700 DKK after showing volatility, but then dropped back down to 600 DKK in time to the prelim results.

We've looked at peers - and they exist across the sectors, I even own many of them. Enel ( ENLAY ), in some ways, is one of them, and I own a lot more Enel than I do Ørsted at this particular time. There are others as well, but the main difference here is that Ørsted trades at significant premiums compared to what's available on the market.

As I mentioned in my last article, in order to accept the premium valuation for this business, you need to accept a 7-10% EBITDA growth rate at the very least, for the long term. I personally believe this - but I never go 100% into anything, which is why you see me hedge my bets a little bit for this company by using other investment strategies. If you want to pay over 850 DKK for the company, you're assuming growth rates far higher than that - which I'm not willing to do here.

Analysts still remain positive despite the recent adjustments. The current target range is down from the 1000 DKK average, down from 900 DK average, and down from 800 DKK average. We're now at 770 DKK, with a range of 505 to 1030 DKK. 24 analysts here follow it, and 12 of them are at a "BUY" or at equivalent. The upside here is around 26.1%.

The company still isn't cheap - I doubt it will ever be cheap. But like with other massive-quality companies, Ørsted doesn't exist in a different iteration - if you want quality, you'll have to pay for it. It's also somewhat volatile due to this valuation.

I was positive on Ørsted in my last article, and I'm going to be positive here as well. Let me show you my updated thesis. I won't change my PT here, because the company's growth for 2022 and despite less than expected for 2023E, was still inside my range.

Thesis for the common shares

- Ørsted is a solid renewables company, and one of the relevant market leaders in the entire segment. It is, in fact, a market leader in Wind. It's also state-owned, has a well-filled pipeline, and is one of the most conservative financing pipelines and maturities when it comes to utilities. This makes it a class-A business.

- However, a meager yield and premiums make valuation important - and I would only buy the company as long as it stays within its range. At current numbers, I would not buy it above 800 DKK per share.

- That means that as of right now, Ørsted is a "BUY" for me.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Thesis for the options

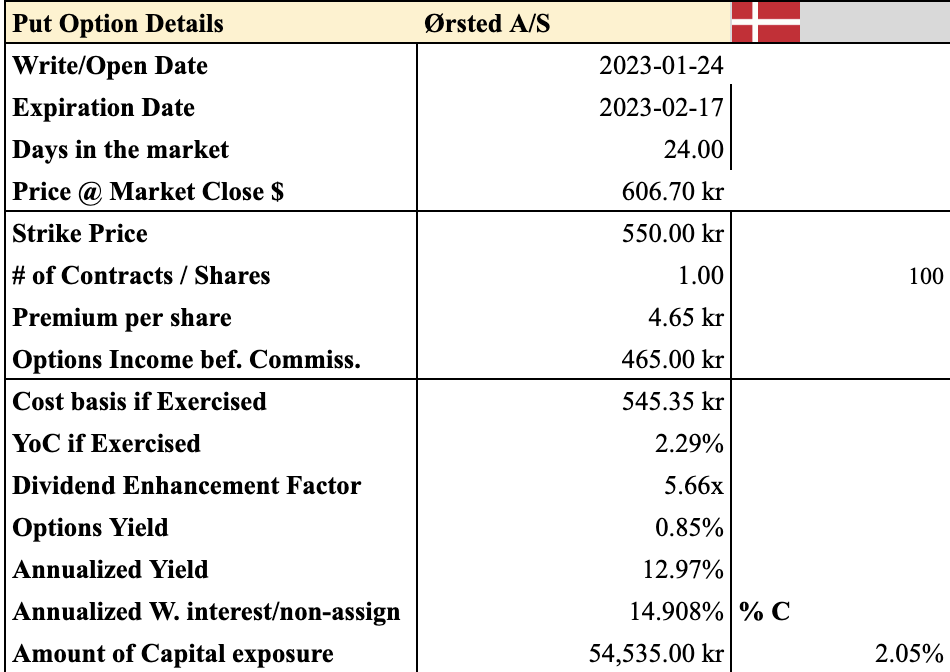

I own the common shares, but I've also hedged my bet here. I've done this by selling put options for Ørsted at two times, one at 525 and one at 550 Strike. At the time of writing, I had sold these options around 1-2 weeks back, and the annualized RoR for these options was 19% and 24% respectively. Today, the annualized RoR available for the February 17 contracts is a lot less, here's what's available at this time.

{kind=link}

It's still a decent 13% RoR, but it also highlights the importance of taking advantage of the volatility and knowing your targets for companies when you look at doing the "options thing".

I consider this to still be workable, and I combine both options and long-term investments here.

For further details see:

Ørsted: I Own Shares And Have Sold Options, This Is A 'Buy'