NONOF - 1 Dividend Legend Potentially Set To Soar And 2 To Ignore

2023-10-13 07:25:00 ET

Summary

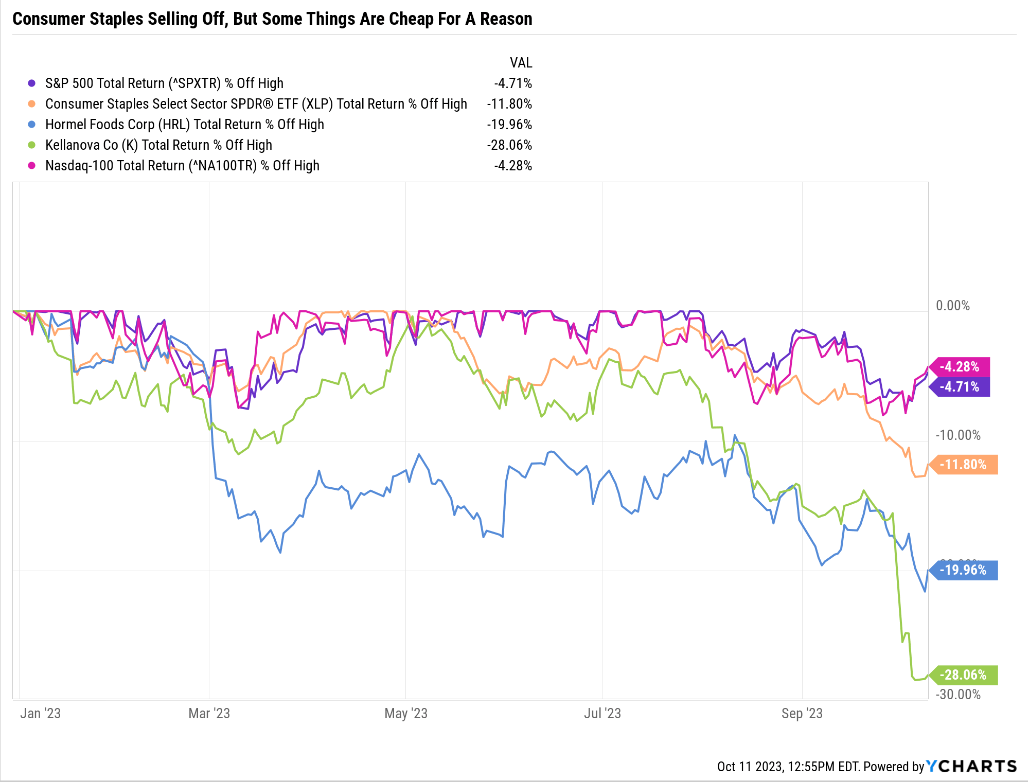

- Consumer staples stocks, including legendary dividend stocks like Hormel Foods Corporation and Kellanova (formerly Kellogg), have crashed between 20% to 30%.

- The media has attributed the decline in consumer staples to factors such as weight loss drugs on food sales and soaring interest rates, but these explanations are wrong.

- Food companies were in an epic bubble in recent years, and now that bubble has popped.

- One company, despite selling unhealthy products, is growing like a weed, reporting 14% pricing power and 11% international growth. Its growth rates are 3X that of Hormel and running circles around its peers.

- The future of healthy food is likely to be dominated by today's food giants. The individual winners and losers are less certain, but that's why I'm here to keep our pulse on the best available data to help you avoid the losers and buy the winners of future food.

It's been an amazing few weeks, with the S&P 500 (SP500) falling into an 8% pullback and the Nasdaq (COMP.IND) about the same. And for many legendary dividend stocks, the pain has been a lot worse.

{kind=link}

Consumer staples have suffered 50% worse declines than the Nasdaq, and individual consumer staples legends like Hormel Foods Corporation (HRL) and Kellanova (formerly Kellogg) (K) have fallen 20% or even 30%!

Let me share with you why people think that consumer staples are in the toilet, why they actually are, and why Hormel is a wonderful company you should not buy even in this bear market.

And finally, and most importantly, I'll share with you one of my favorite ways to profit from this consumer staples bear market. Is it Kellanova? No! Kellanova is even worse than Hormel, a stock that no one other than index investors should be buying right now.

I know of a dividend growth legend that is growing 10X faster than Kellanova and is also down about 30%. It's potentially set to soar, too cheap to ignore, and a recommendation you can't afford to miss.

Why The Media Says Consumer Staples Is In The Toilet

As Ritholtz Wealth Management CEO Joshua Brown says, "Narrative always follows price."

In other words, after something dramatic happens, the media will come up with a plausible-sounding reason to explain it.

That's understandable; it makes us sound smart, and people crave a sense of understanding. It makes them feel safe, unlike being a leaf in a hurricane.

Here are the two big narratives the media is saying are causing consumer staples legends like Hormel and Kellanova to suffer.

Ozempic and Wegovy are dampening food sales, Walmart's John Furner has said. The success of drugs like Ozempic and Wegovy in treating weight loss could be driving Americans to spend less money on food , a top Walmart executive has said." - Fortune (emphasis original).

I'm not saying Walmart's (WMT) U.S. head is a liar. But this catchy headline sounds important, and that's why the media is fixated on it.

But here's another quote from Furner that's a lot less exciting.

We definitely do see a slight change compared to the total population, we do see a slight pullback in overall basket," John Furner, the chief executive officer of Walmart's sprawling US operation, said in an interview Wednesday. " Just less units, slightly less calories. "...

Furner said it's too early to draw any definitive conclusions about the appetite-suppressing drugs made by Novo Nordisk A/S, and similar medicines. - Bloomberg (emphases added).

Wow, a lot less dramatic, isn't it? Not nearly the "Walmart and Costco (COST) are doomed!" story, you thought, right?

OK, so let me bust out the spreadsheet math for you and show you what food companies might expect. I'm not making any official forecasts, but here's some context.

According to one study about Ozempic, a drug produced by Novo Nordisk (NVO), that looked at 1,500 type 2 diabetic patients over 40 weeks, the average weight loss was about 15 lbs on the maximum dose.

- approximately 3,500 calories ( 3,436 and 3,752 is the actual range).

So that's about 52,500 calories in the average weight loss for Ozempic. Over 40 weeks, that's 1312 calories per week or 187 per day.

- 0.37 lbs per week

- I have lost 6 lbs per week for 11 weeks eating 2,000 calories per day of plants

- maybe I should start selling my "secret" to weight loss magic?;)

Side effects with Ozempic like nausea, vomiting, diarrhea, stomach pain or constipation are common." - Drugs.com .

Is everyone going to go on these drugs? Nope. But what if they did?

How much is 1312 calories? Here are some popular foods with that many calories.

- A large pepperoni pizza from Domino's

- A large order of fries and a Big Mac from McDonald's

- A Whopper and a large order of fries from Burger King

- A 12-pack of chicken nuggets and a large fries from Chick-fil-A

- A large burrito bowl with steak, rice, beans, cheese, and sour cream from Chipotle

- A large order of chicken wings and a side of fries from Buffalo Wild Wings

- A large milkshake from Five Guys

- A large ice cream sundae from Baskin-Robbins

- A large box of popcorn and a large soda from the movie theater

- A large bag of chips and a large candy bar

- A large bottle of soda and a large bag of candy.

Should PepsiCo (PEP) be quaking in its boots that the idea that Americans will all go on Ozempic and eat one less bottle of soda or bag of Dorritos?

Pepsi just reported 7% sales growth driven by 10.5% pricing power offsetting 2.5% volume declines.

So no, consumer staples likely aren't falling fast and hard because of Ozempic or Wygovy (Eli Lilly's (LLY) version).

It's Interest Rates Stupid!

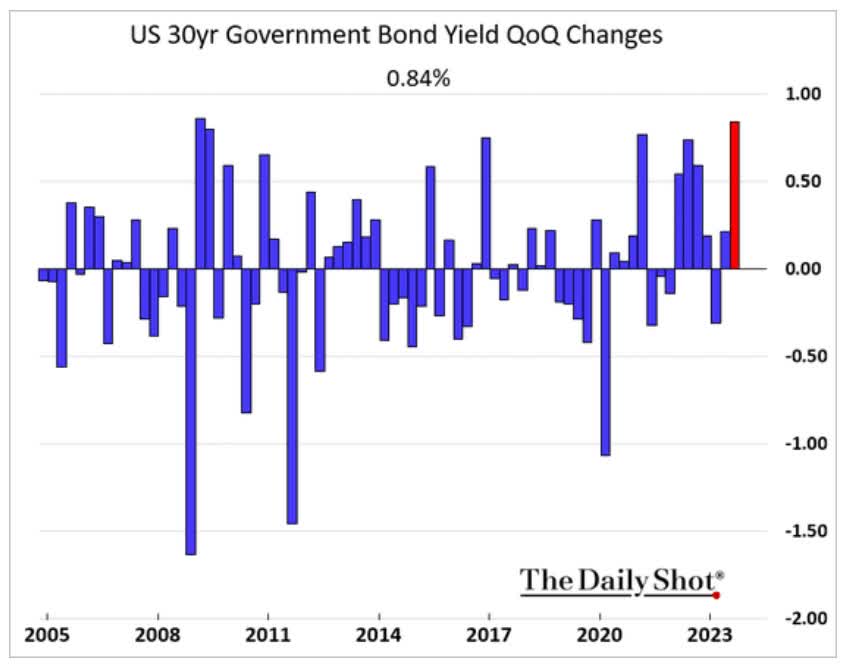

Another popular media explanation for the big correction in consumer staples is soaring interest rates.

{kind=link}

Rates have soared at the fastest rate in at least 20 years.

So that must be it, right? Rates are up, REITs, utilities, Midstream, YieldCos, and consumer staples are down right?

All the bond alternatives are suffering during the worst bond bear market in history.

Nope. It's a lie.

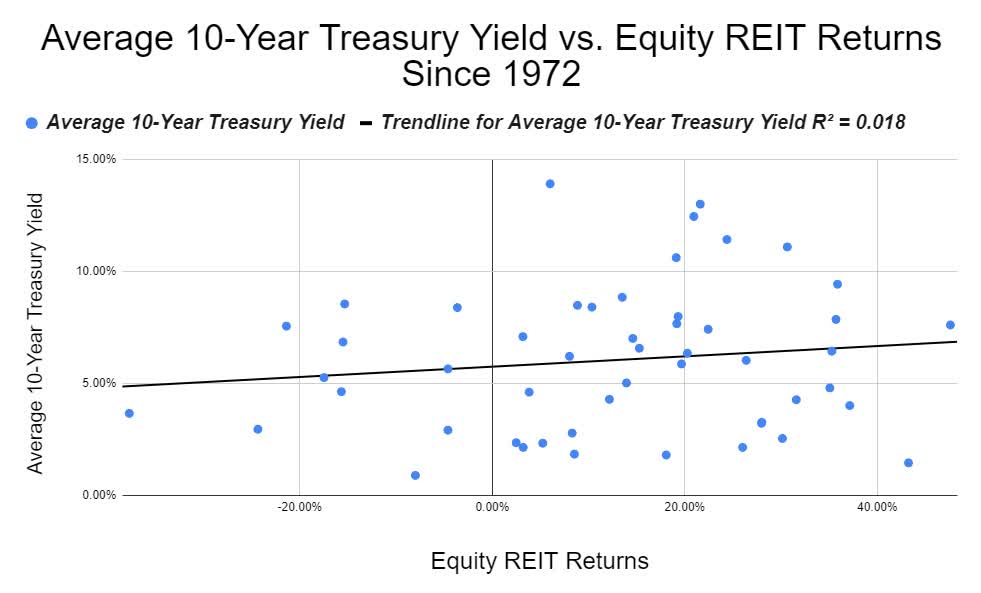

{kind=link}

REITs aren't actually rate-sensitive over the long term, just over the short term (1 to 3 years).

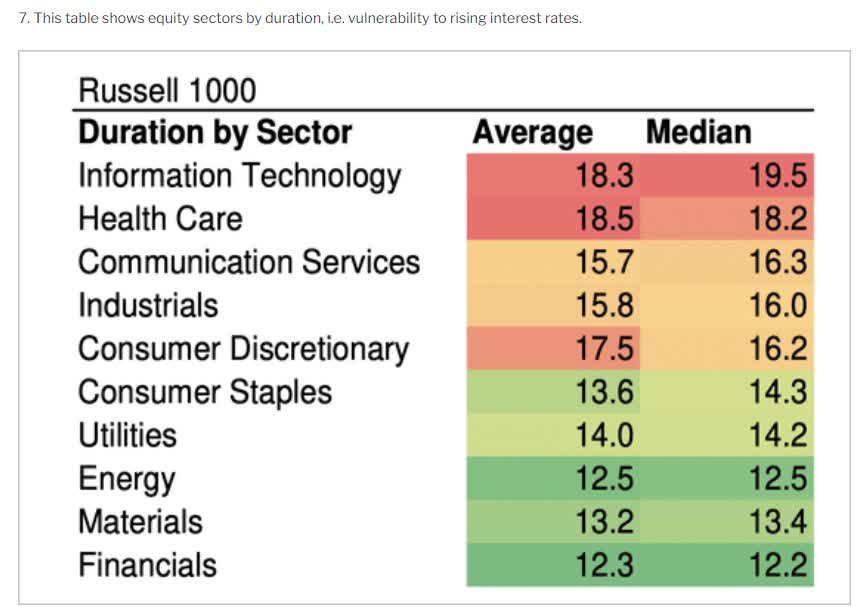

And what about other sectors?

{kind=link}

Long term, utilities are less rate-sensitive (and so are consumer discretionary) than tech.

{kind=link}

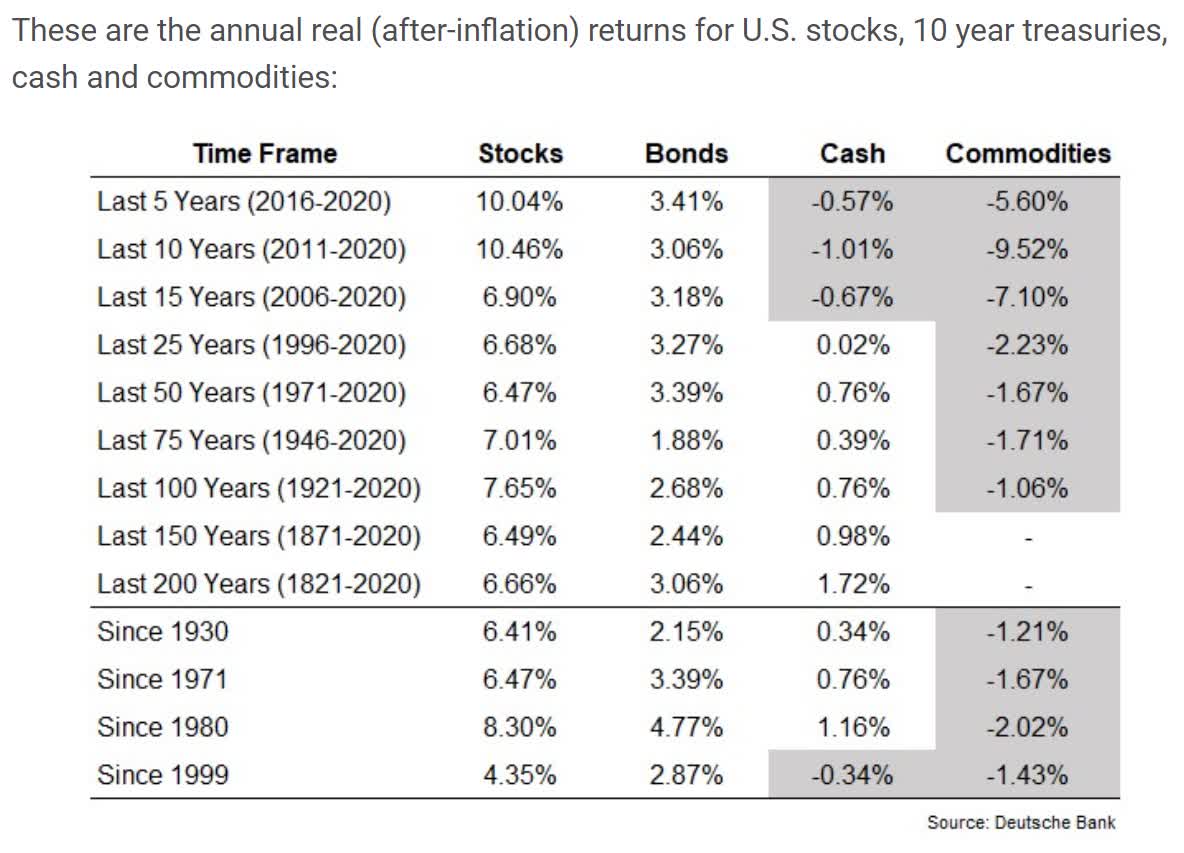

Here are 200 years of inflation-adjusted returns for stocks and bonds. Notice anything? Stocks historically deliver 2X the real return of bonds.

Because they don't just pay a dividend, they pay a growing dividend.

And do you know what else?

{kind=link}

The only thing that beats the S&P over the long-term? Dividend stocks!

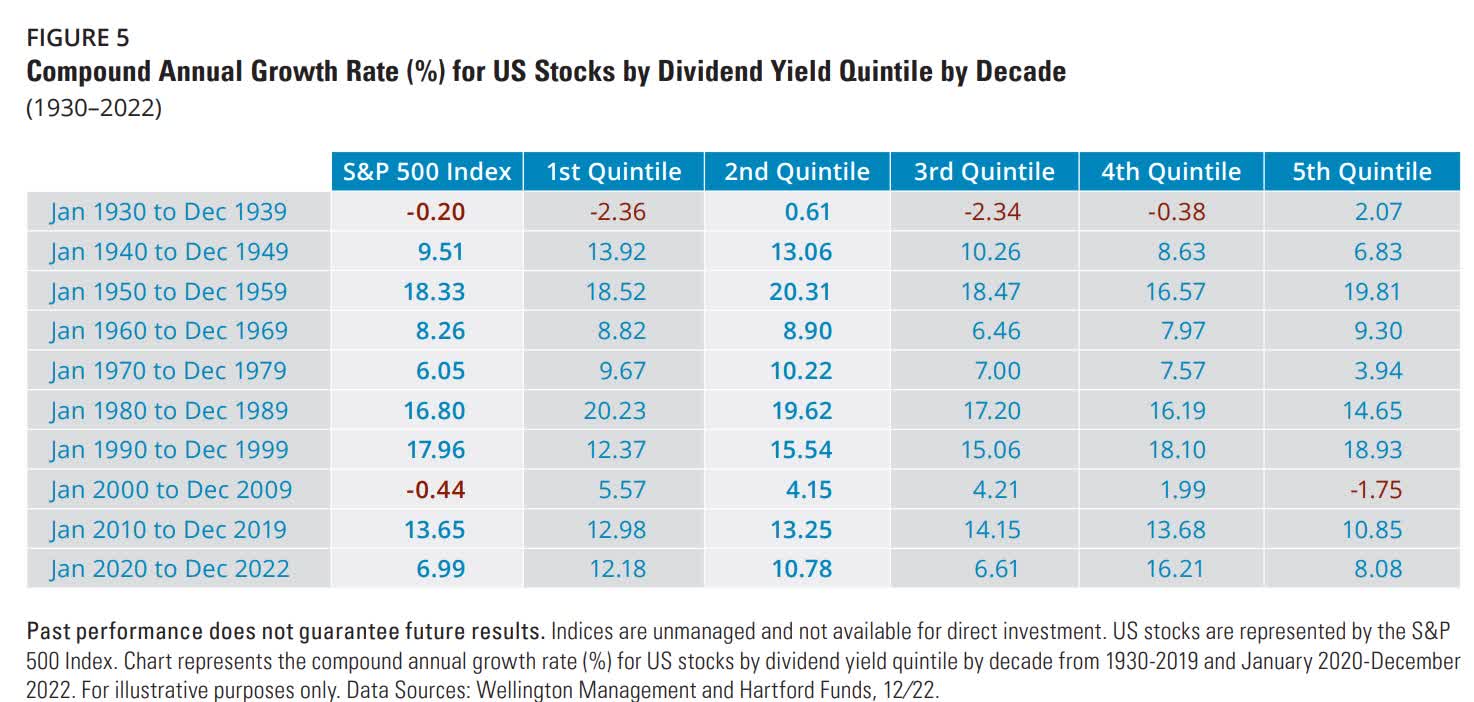

What about high yield vs. low yield?

{kind=link}

The highest yield does sometimes suffer, but anything with a yield of 4% or less generally doesn't.

And consumer staples yield 2.8% on average, 2nd quintile, the best-performing quintile.

- consumer staples is one of the only sectors to beat the QQQ since inception.

So the point is that interest rates are only moderately responsible. Not anything like what the media is saying.

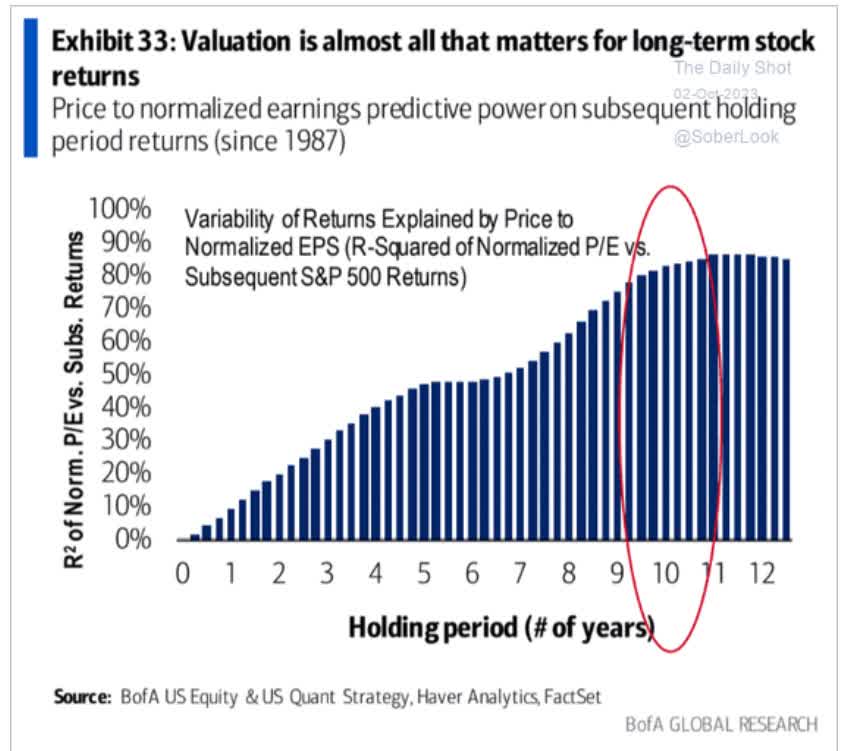

Why The Sector Is Actually Suffering

{kind=link}

Over the long-term valuation, i.e. fundamentals, are almost all that matter.

| Time Frame (Years) |

| Total Returns Explained By Fundamentals/Valuations |

| 1 Day |

| 0.02% |

| 1 month |

| 0.33% |

| 3 month |

| 1.0% |

| 6 months |

| 2.0% |

| 1 |

| 5% |

| 2 |

| 10% |

| 3 |

| 15% |

| 4 |

| 28% |

| 5 |

| 36% |

| 6 |

| 47% |

| 7 |

| 58% |

| 8 |

| 68% |

| 9 |

| 79% |

| 10+ |

| 90% |

| 20+ |

| 91% |

| 30+ |

| 97% |

(Sources: DK S&P 500 Valuation Tool, JPMorgan Asset Management, Bank of America, Princeton, RIA.)

In the short term, valuation doesn't mean much. In fact, over any 1 month period luck/sentiment/momentum are about 300X more powerful than fundamentals.

But in the long-term fundamentals and valuation are all that matter (well, 97% of all that matter).

{kind=link}

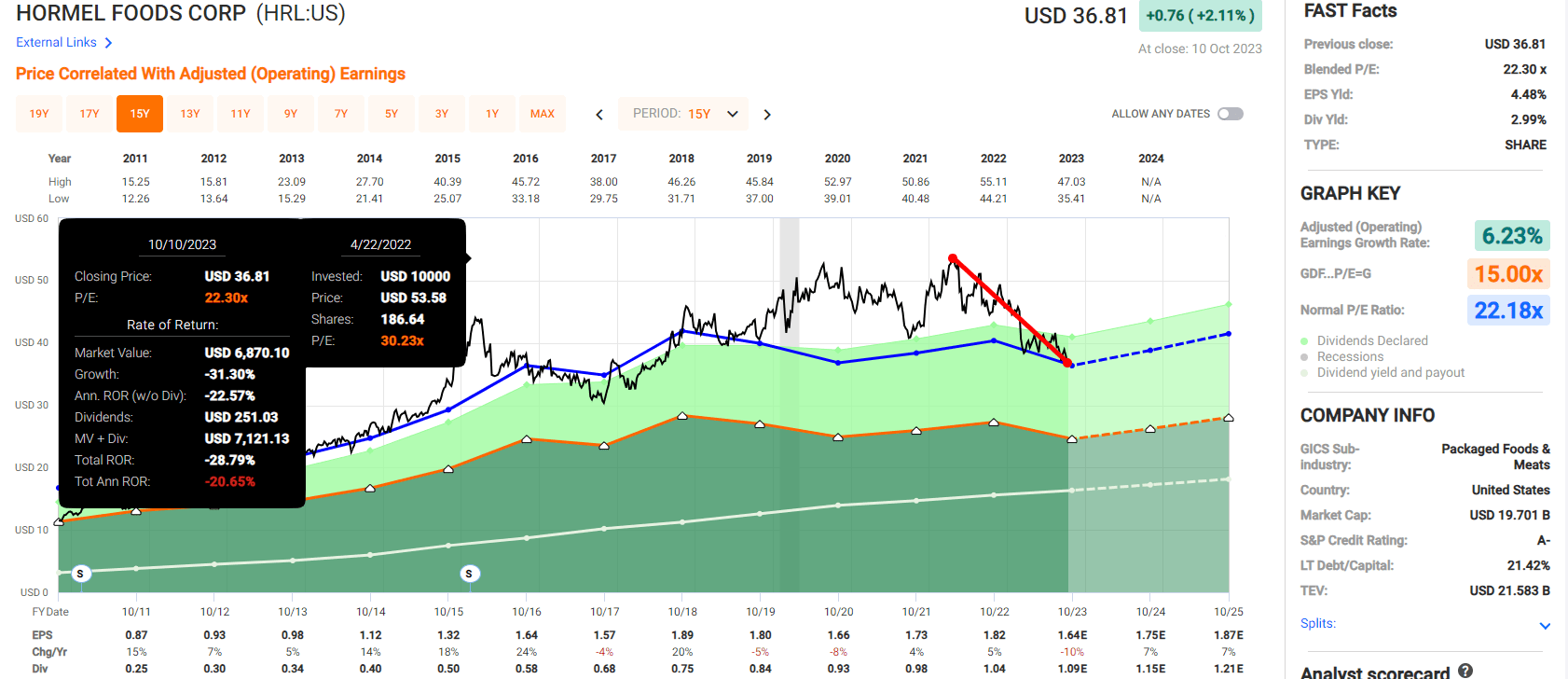

Hormel historically trades at 20 to 24X earnings. It peaked at 30X earnings a 36% historical premium.

This is not a tech stock, you can't pay an absurd valuation and hope that hypergrowth saves your butt.

- valuations also matter with growth stocks, by the way.

{kind=link}

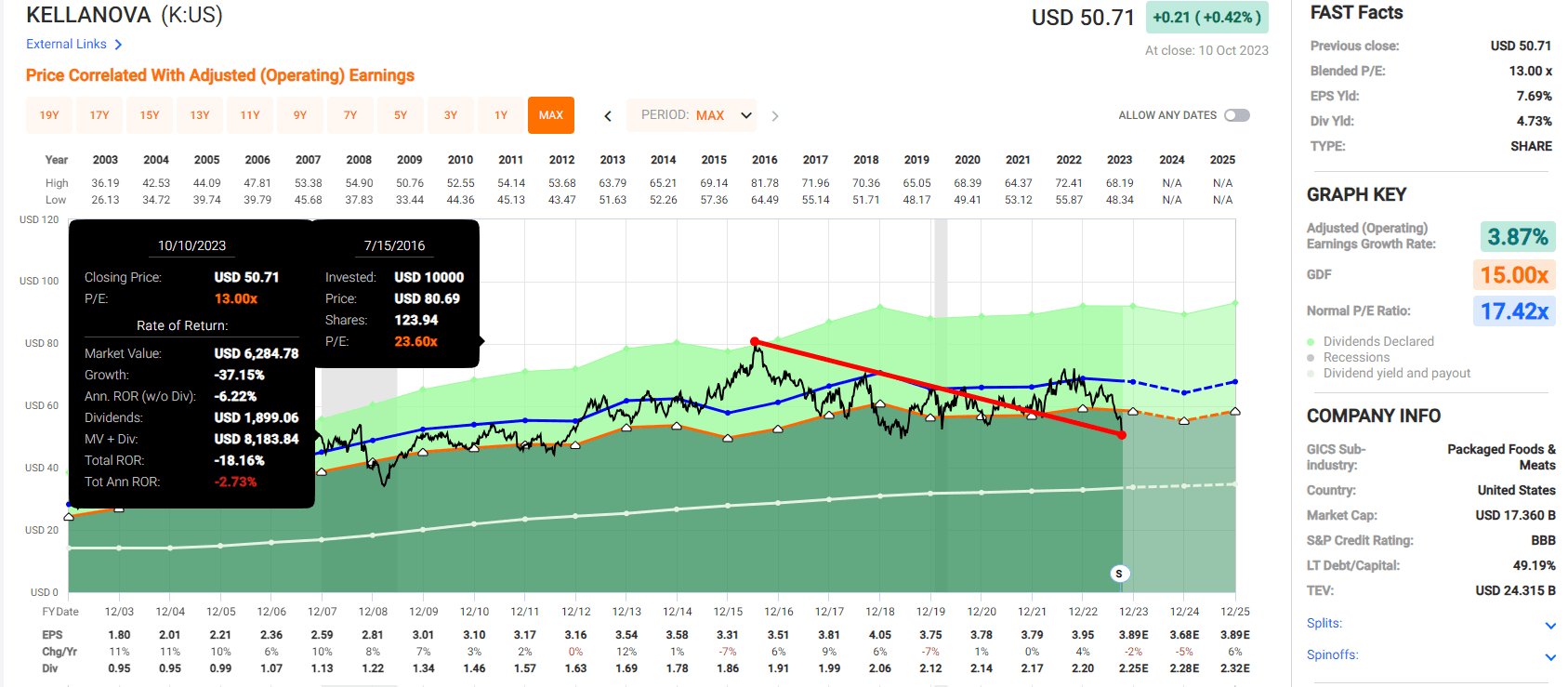

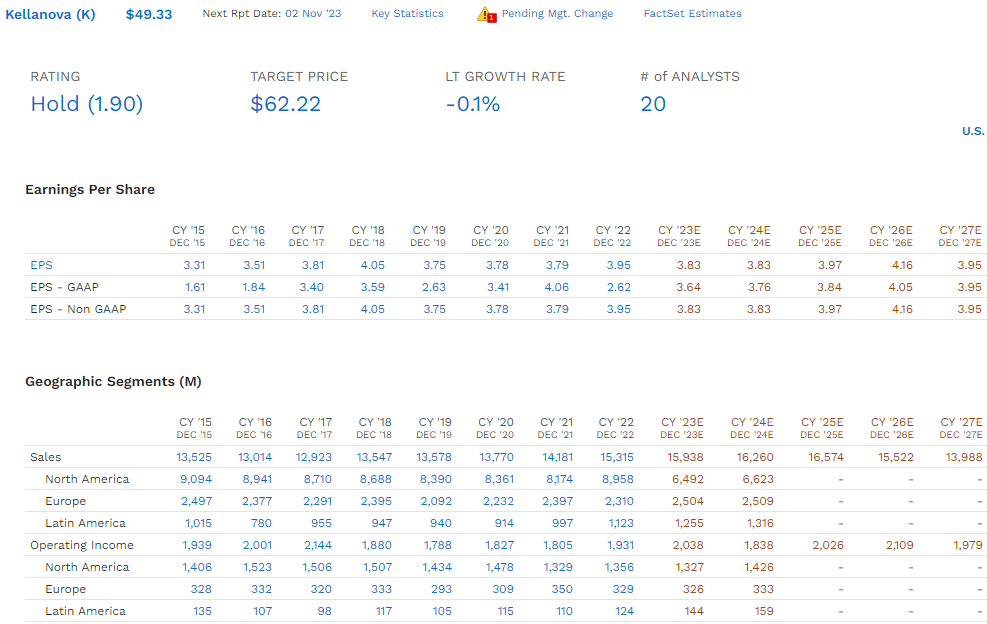

Kellanova (formerly Kellogg) peaked at a 30% premium, and thanks to many years of weak growth has basically delivered zero returns including dividends.

Well, I have good news and bad news for Kellanova investors. Yes, the yield of almost 5% is awesome and reasonably safe (about 5% risk of a cut in a severe recession).

But long-term total returns is yield + long-term growth + changes in valuation.

{kind=link}

Kellanova isn't just expected to not grow in the long term, it's expected to have basically not grown from 2017 to 2027. 10 years of no growth including buybacks.

Do you know the statistical probability of a company not growing over 10 years becoming a good long-term investment? 10%.

There is a 90% chance that you don't want to own Kellanova.

But what about Hormel? And my super secret fast-growing, undervalued food recommendation?

Why You Probably Don't Want To Own Hormel

Further Reading

While Hormel is most famous for its SPAM meat in a can brand, it is one of the largest protein companies on earth selling

- Applegate

- Columbus

- Dinty Moore

- Herdez

- Jennie-O

- Justin's

- Hormel Natural Choice

- Wholly

- Hormel Black Label

- Planters.

In 2021 Hormel bought Planters, the #1 peanut company in America with more than 2X the market share of its next biggest rival, for $2.8 billion.

The integration of the largest M&A deal in the company's history has hit some rough spots, with supply chain disruption and slower growth than previously expected.

{kind=link}

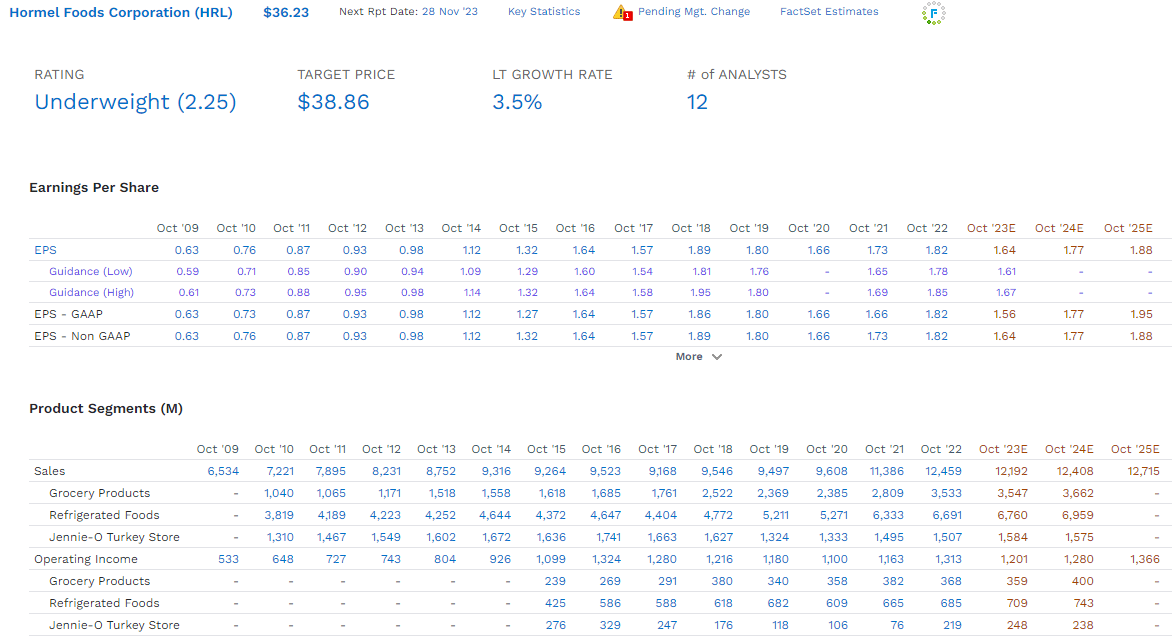

While Hormel grew earnings at 9.2% annually from 2009 to 2020 (before it bought Planters) above its historical 7.7% rate, since buying Plants its growth has slowed to 2.5%.

Worse yet, analysts now believe that, after the Planter's problems are solved, growth will accelerate to just 3.5%.

{kind=link}

Hormel's problem isn't debt. Its deleverage ratio is just 2X next year and its cash + post-dividend free cash flow for 2024 is over $1 billion.

- $342 million post-dividend free cash flow + $687 million cash = $1.029 billion in cash by the end of 2024.

Why does that matter?

{kind=link}

Hormel has $950 million in bonds maturing next year, and over $1 billion in cash and consensus retained free cash flow.

So it will be able to easily repay that bond, though, with a stable A- credit rating, it will almost certainly refinance it.

After 2024 there are no bonds maturing for four years.

What about the processed meat industry? Isn't that on its way out of favor? Didn't the WHO just label processed meat a type 1 Carcinogen (known to cause cancer in humans)?

Yes, processed meats have now joined such other infamous toxic products as Tobacco smoking, Asbestos, Acetaldehyde, Aflatoxins, and plutonium.

Journal Of The American Medical Association

{kind=link}

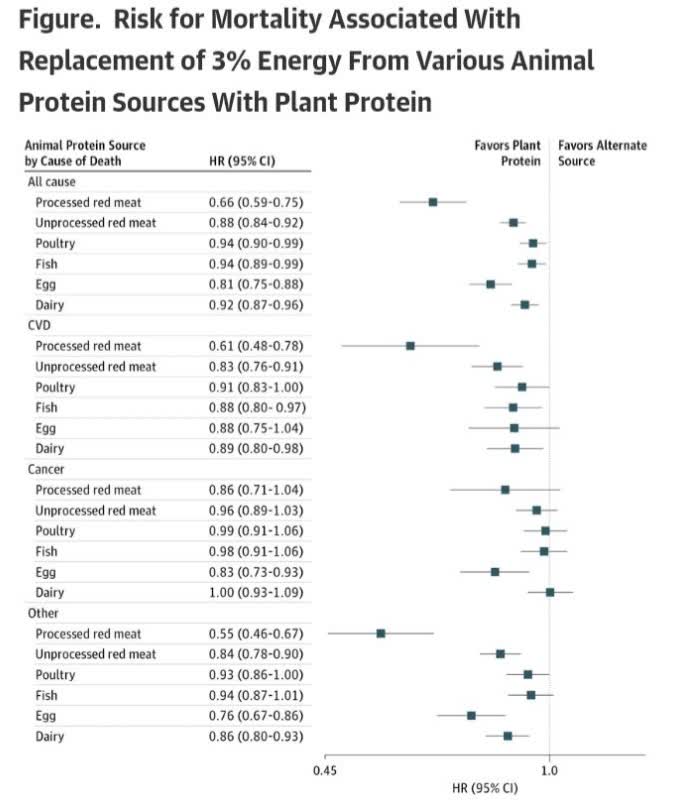

Cutting down on processed meat by just 3% of your calories reduced mortality risk by 45% in 131,000 people.

The study reviewed protein intakes of more than 131,000 women and men from the Nurses' Health Study and Health Professionals Follow-up Study. After tracking their diets for up to 32 years, the authors found that a higher intake of red meat, especially processed versions (sausage, bacon, hot dogs, salami), was linked to a higher risk of death, while a higher protein intake from plant foods carried a lower risk.

Song M, Fung TT, Hu FB, et al. Association of Animal and Plant Protein Intake With All-Cause and Cause-Specific Mortality. JAMA Intern Med. 2016;176(10):1453-1463. doi:10.1001/jamainternmed.2016.4182 " - Harvard School of Public Health .

{kind=link}

That's not surprising given what medical science has learned in recent decades about what's good and bad for us to eat.

So yes, technically, what Hormel is selling is absolutely terrible for our health it doesn't matter, at least for now .

- in the U.S., processed meat is growing at 1.9% per year

- globally, 5.3% annually (through 2028).

Around the world, people continue to buy processed food. The problem is that Hormel's brands are not doing as well as management had hoped. Its long-term guidance of 7% to 10% EPS growth is based on the plan of growing market share in international markets, such as India and China, where richer people with less time are eager to buy processed meats.

For now, Hormel is struggling to gain market share. So how worried should investors be?

S&P rates HRL's long-term risk management 70th percentile among all companies worldwide.

S&P's risk management scores factor in things like:

- supply chain management

- crisis management

- cyber-security

- privacy protection

- efficiency

- R&D efficiency

- innovation management

- labor relations

- talent retention

- worker training/skills improvement

- occupational health & safety

- customer relationship management

- business ethics

- climate strategy adaptation

- sustainable agricultural practices

- corporate governance

- brand management.

So HRL is likely to pivot and start selling healthier products that aren't carcinogenic as soon as customers start wanting them.

{kind=link}

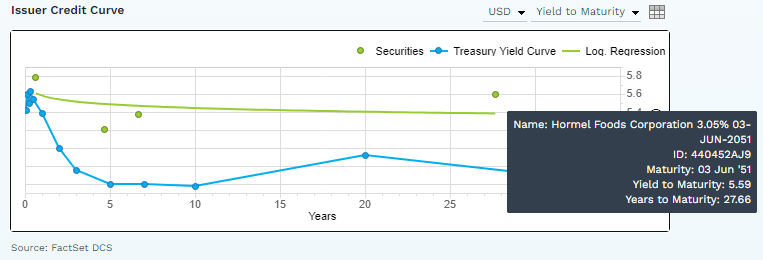

The bond market is confident enough in Hormel's healthy food transition plan to buy its bonds maturing in 2051.

What is Hormel likely to sell in the future? Something like this.

{kind=link}

Mushroom root-based chicken - which I've tried, my father has tried, and my sister has tried, and we all agree: it tastes like chicken. But it has far lower sodium than processed meat, no saturated fat, no cholesterol, and is packed with vitamins and minerals.

- the new staple for my burrito sandwiches.

Whole Food Mushroom Sandwiches With Chili, Shiitake Mushrooms, Garlic, Turmeric, Amla, Super Greens, And High Fiber Spinach Wraps

{kind=link}

- Calories: 326.2

- Fat: 5.0 g

- Saturated Fat: 0 g

- Omega 6: Omega 3 ratio (1 to 3 healthy): 0.848

- Protein: 34.5 g

- Carbs: 55.2 g

- Fiber: 32.4 g

- Sodium: 908 mg (limit 2 per day to stay under 2300 mg, limit 1 per day for Ornish/Esselstyne diet)

- Iron: 67% of daily value

- B12: 355% of daily value

- Folate: 134% of daily value

- Overall vitamins: 62% of daily value

- Overall nutrition: 30% of daily value.

Hormel was founded in 1891 and has grown its dividend for 57 consecutive years. In that 132 years, it's had to pivot many times, including shifting to healthier foods.

Currently, the bond market and S&P are 97.5% confident that Hormel will thrive in the future; it just won't sell carcinogens, just like tobacco companies won't sell cigarettes in 30 years.

The question is not "Will Hormel still be around in 30 years" but "How fast will it grow over the next 30 years? At the moment, that answer looks like 3% to 4% per year, and while today's yield of 3% is attractive for 7% to 10% growth, for 3.5% growth, it's subpar.

- 60/40 retirement portfolio is expected to outperform Hormel right now.

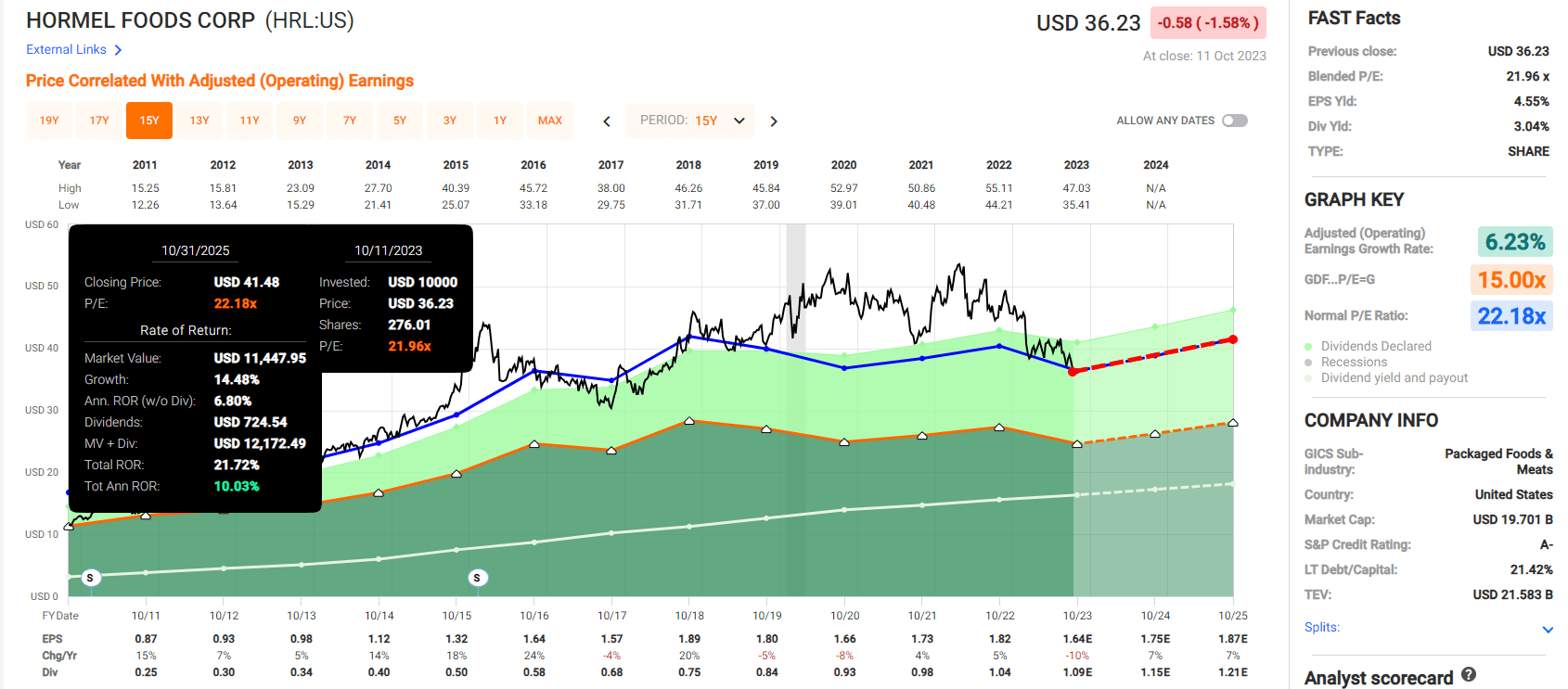

Hormel Fundamental Summary

- yield: 3.0%

- dividend safety: 100% very safe (1.00% dividend cut risk)

- overall quality: 98% low-risk Ultra SWAN dividend king (57-year streak)

- credit rating: A- stable (2.5% 30-year bankruptcy risk)

- long-term growth consensus: 3.5%

- long-term total return potential: 6.5% vs 10.2% S&P 500

- current: $36.23

- fair value: $45.22

- discount to fair value: 20% discount (potential strong buy) vs 5% overvaluation on S&P

- 10-year valuation boost: 2.3% annually

- 10-year consensus total return potential: 3% yield + 3.5% growth +2.3% valuation boost = 8.8%

- 10-year consensus total return potential: = 132 % vs 160% S&P 500.

{kind=link}

Even with a 20% historical discount (dividend yield fair value is higher than earnings fair value), HRL is offering not much better return potential than the S&P even over the short term.

{kind=link}

The S&P is a risk-free long-term investment (it can't go to zero outside of an apocalypse), and the reason for buying individual stocks is that you achieve sufficient returns for your goals.

- long-term returns of 8+% is what I recommend for defensive stocks

- 7% is the 60/40 historical and expected future return.

Why Hershey Is A Potentially Strong Buy Right Now

Further Reading

(1) timeless services or products that customers can easily afford throughout all economic cycles;

(2) high and durable profit margins over the past ten years;

(3) low (or no) long-term debt;

(4) able to reinvest earnings to grow the business without needing to rely on outside financing;

(5) consistently profitable for the past ten years;

(6) low (or no) innovation threats to the core products;

(7) high brand loyalty or other barriers to entry;

(8) consistent dividends and dividend growth;

(9) rising earnings per share over the past ten years;

(10) rising book value per share over the past ten years;

(11) low litigation risk; and

(12) "rising buybacks and falling share count over the past ten years." - Investment Pancake.

The Hershey Company (HSY) doesn't sell anything emphasizing nutrition, so you might think it has no future. If Hormel's processed meat represents 3.5% growth and Kellanova's sugar-loaded cereals (some up to 70% pure sugar) have zero growth, how terrible must candy be?

Let's just consider North American sales, which is 92% of the total for now.

Here is the organic revenue growth that HSY had before the Pandemic.

- 2015: 0.2%

- 2016: 1.1%

- 2019: 2.5%

- 2022: 12.0%

- 2023: 8.1%

- 2024: 3.9%

- 2025: 3.0%.

Inflation has benefited Hershey incredibly well with strong pricing power and its international sales. 11.2% growth in 2022!

So, yes, Hershey is selling what some consider the junkiest of junk food, with no redeeming nutritional value at all.

USDA

The American Heart Association recommends eating 13g of saturated fat per day or less. One Hershey bar gets you 7g of saturated fat, shown to increase LDL bad cholesterol.

It also has a bit of trans fat just to add to the heart-attack-inducing goodness;)

- 30% of calories from pure saturated and trans fats

- nutritionally speaking, the devil's own snack;)

But for now, people can't get enough of Hershey's decadent candy and, long term, the S&P and the bond market are confident that Hershey will still be around.

- A stable credit rating

- 0.67% risk of bankruptcy within 30 years.

HSY's Long-Term Risk Management Is The 43rd Best Risk Manager In The Master List (9th Percentile In The Master List)

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| [[BTI]], [[ILMN]], [[SIEGY]], [[SPGI]], [[WM]], [[CI]], [[CSCO]], [[WMB]], [[SAP]], [[CL]] |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Hershey |

| 95 |

| Very Good |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Hormel |

| 70 |

| Good |

| Low Risk |

| Coca-Cola (KO) |

| 68 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

S&P considers Hershey's long-term risk management excellent, in the top 5% of all companies on earth.

One day, Hershey will have to pivot to healthy snacks, but for now, people can't get enough of their sugar-loaded decadent desserts.

{kind=link}

Kellanova is growing at -0.1%, Hormel at 3.5%, and Hershey? 3X faster than Hormel and even faster than Coca-Cola (KO) and Pepsi!

And Pepsi just hiked its prices by 10% or more for the 7th consecutive quarter! Hershey raised its prices by 14% in Q2!

Is Hershey healthy? No, it's the anti-healthy food company. Is it getting a lot more expensive? At 4X the rate of inflation! Yet the numbers don't lie, Hershey is peddling its sugary deserts like a master and people are gobbling it up.

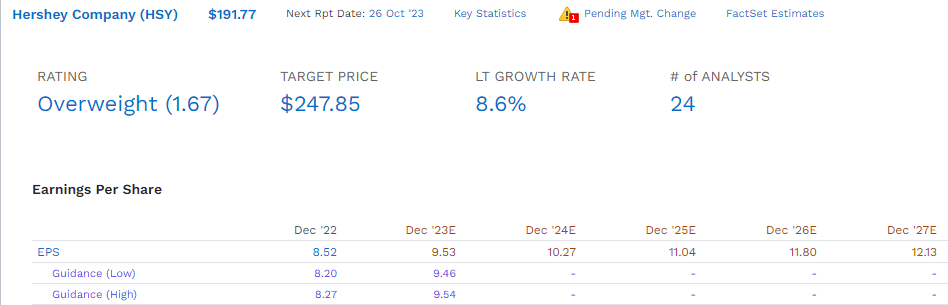

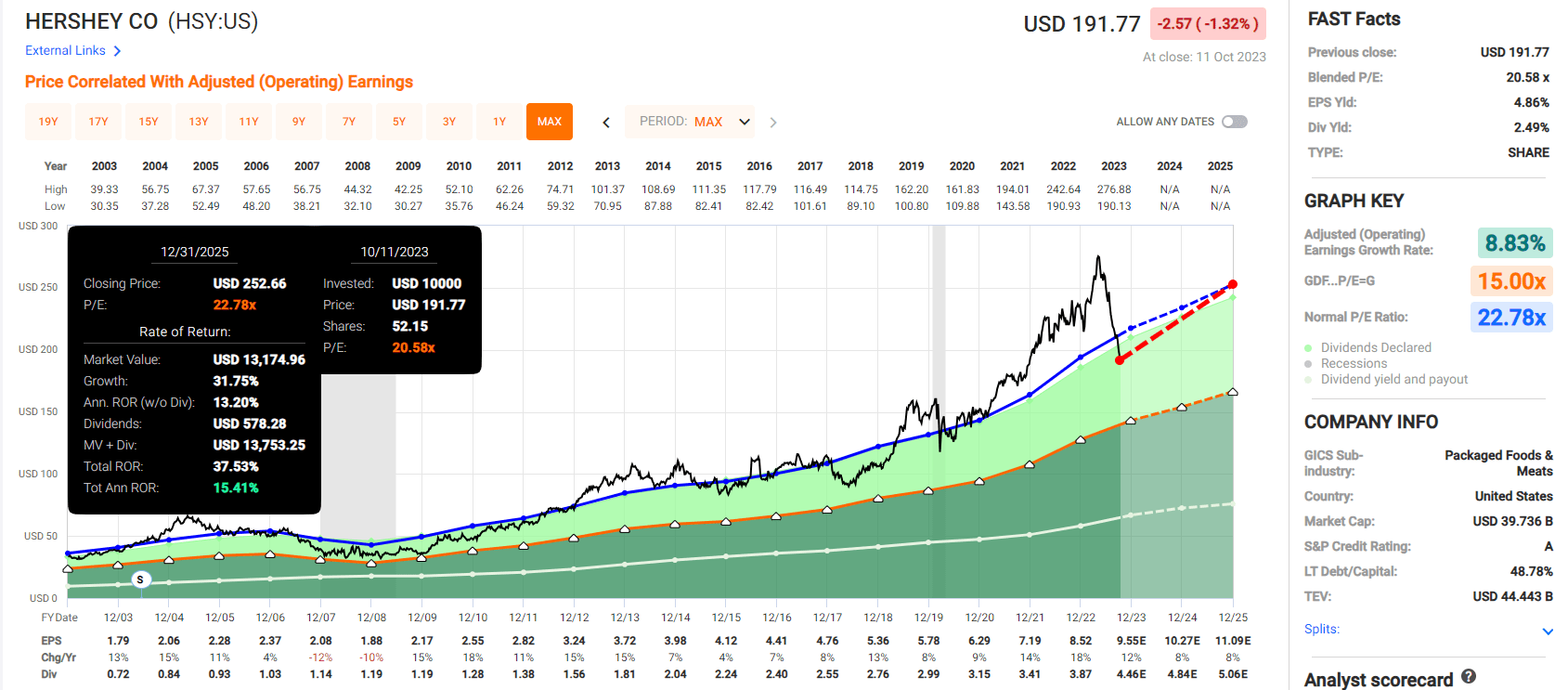

HSY Fundamental Summary

- yield: 2.4%

- dividend safety: 96% very safe (1.2% dividend cut risk)

- overall quality: 94% very low-risk future dividend aristocrat Ultra SWAN (13-year streak and 34 years without a cut)

- credit rating: A stable (0.67% 30-year bankruptcy risk)

- long-term growth consensus: 8.6%

- long-term total return potential: 11.0% vs 10.2% S&P 500

- current: $191.77

- fair value: $230.91

- discount to fair value: 17% discount (strong buy) vs. 5% overvaluation on S&P

- 10-year valuation boost: 1.9% annually

- 10-year consensus total return potential: 2.4% yield + 8.6% growth + 1.9% valuation boost = 12.9%

- 10-year consensus total return potential: = 329 % vs 160% S&P 500.

{kind=link}

Bottom Line: Hershey Is Firing On All Cylinders, Hormel Is Struggling, And Kellanova Is Spinning Its Wheels

{kind=link}

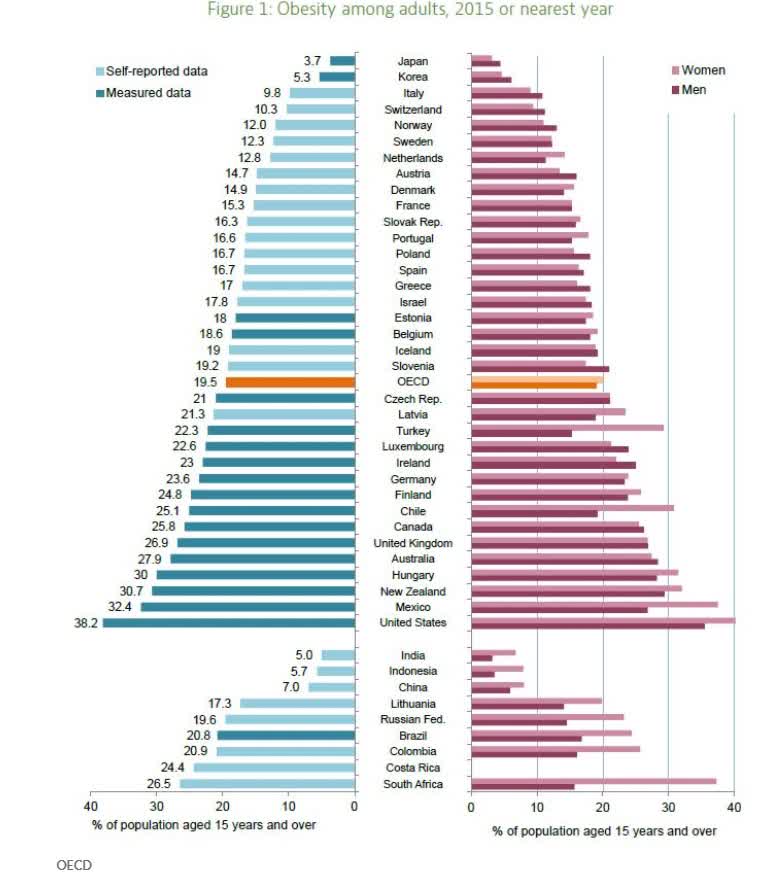

Obesity is a global crisis that's especially bad in the U.S., the fattest nation in the OECD.

By 2030 the OECD estimates the U.S. will be 50% obese and by 2050 the CDC estimates 74%.

- 85% overweight or obese.

Is this a global health emergency? You bet.

Will today's food giants get away with selling the same toxic food they are now selling? Not forever, or else humanity will go extinct.

As the sands of food popularity and government regulation shift, the best thing food investors can do is follow the best available date wherever it leads.

Do you know who will likely dominate the healthier food of the future? Today's food giants. For example.

- Conagra owns Purple Carrot and Gardein

- Coke Owns Vitamin Water, Dasani, Ciel, and Smartwater

- Pepsi owns Quaker Oats, Naked Juice and Sabra Hummus

- Otsuka Pharmaceutical Company owns Daiya (plant cheese)

- Silk plant-based milks? Owned by Danone.

{kind=link}

According to a report by analyst firm GovGrant, by 2040 traditional meat will be down to 40% of the market . If that is accurate and the trend holds to 2050, traditional meat will be down to 10%.

Does that mean Hormel and Tyson are screwed and McDonald's (MCD) is going bankrupt?

{kind=link}

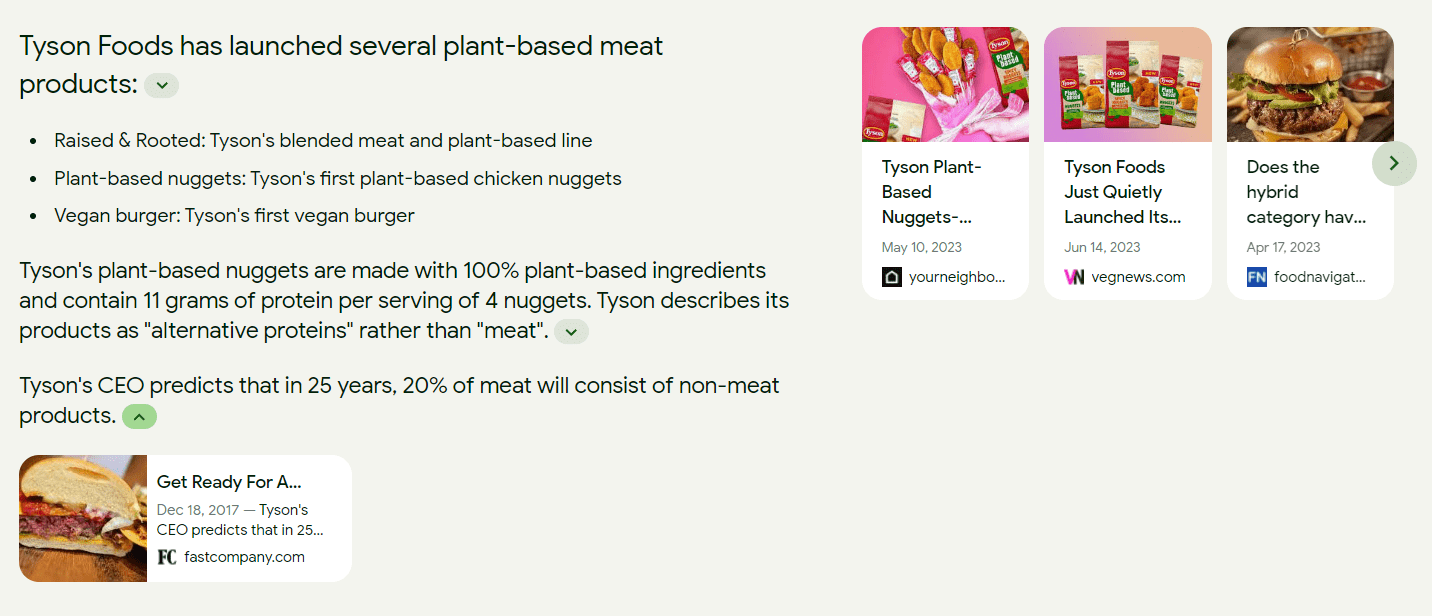

Who owns 6.5% of Beyond Meat? Tyson Foods (TSN). Who is already making chicken that's 50% chicken and 50% pea protein? Tyson. Who is rolling out various lines of plant-based meats? Tyson.

Whose CEO says that by 2043 20% of meat will be plant-based and that his company is preparing for this? Tyson

Who is almost certainly going to be a top provider of protein in the future? Most likely the biggest meat companies operating today.

- Cargill Meat Solutions: Based in Wichita, KS, with 2022 sales of $165 billion

- Tyson Foods: Based in Springdale, AR, and the largest U.S. meat company by sales

- JBS USA: Based in Greeley, CO

- Sysco: Based in Houston, TX, with 2022 sales of $68.636 billion

- Smithfield Foods: Based in Smithfield, VA

- Hormel: Based in Austin, Minnesota

- Conagra Brands: Based in Chicago, IL

- Koch Foods: Based in Park Ridge, IL

- Sprouts Farmers Market: Owns and runs a retail grocery store network.

Yes, the Kock Brothers (or their company, at least) will likely be one of the biggest providers of vegan burgers in the future;)

Not because they will go "woke," but because that's where the money will be.

All the big food companies will adapt or die. 85% diabetes and heart disease rates would lead to the fall of the republic and thus won't be allowed to happen.

The only question is...who will be the winners and losers in the healthy food transition?

For now, Hershey appears to be a big winner (same with Coke and Pepsi).

Hormel is going to have to find some new brands or pivot its existing ones; Kellanova is going to have to figure out something to sell that's not 70% sugar.

But for the next few years? The Hershey Company is potentially set to soar, while Hormel Foods Corporation and Kellanova are legendary dividend food stocks to ignore.

For further details see:

1 Dividend Legend Potentially Set To Soar And 2 To Ignore