KKR - 1 Main Capital Partners Q2 2023 Fund Letter

2023-07-24 02:46:00 ET

Summary

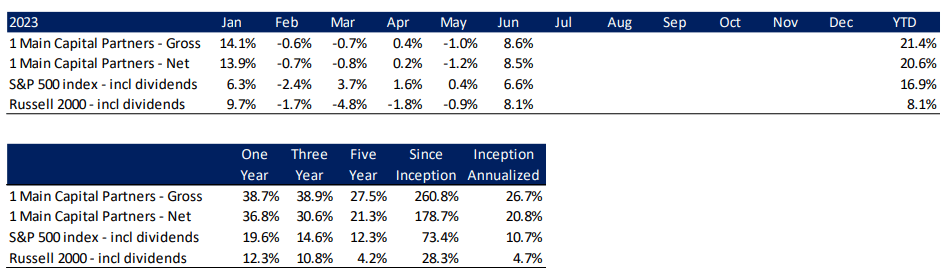

- For the second quarter, 1 Main Capital Partners, L.P. delivered a net return of 7.5%, compared to 8.7% and 5.2% for the S&P 500 and Russell 2000, respectively.

- At quarter-end, the Fund’s top five positions accounted for approximately 70% of capital.

- While I continue to run the Fund with the goal of generating attractive through-cycle returns rather than avoiding near-term volatility, I have steered the portfolio into names that can withstand and capitalize on any economic slowdown should one occur.

Dear Partners,

For the second quarter, 1 Main Capital Partners, L.P. (the “Fund”) delivered a net return of 7.5% 1 , compared to 8.7% and 5.2% for the S&P 500 (“SPX”) and Russell 2000 (“RTY”), respectively. For the first half, the Fund returned 20.6% net, compared to 16.9% and 8.1% for the [[SPX]] and [[RTY]], respectively.

Although 2023 started on a positive note, at quarter-end, the SPX and RTY were still trading 7% and 23% below their previous highs, respectively. They were sitting at these lower levels approximately eighteen months into the inflation-related bear market. The significance of elapsed time is often underappreciated by market observers. After all, equities can become cheaper in two ways: through a decline in price, or simply the passage of time. In this case, both have occurred.

Time and human nature are the friends of bulls and enemies of bears. With time, stocks accrue a compounding rate of return through growth and accumulated earnings. Thus, in a market that goes sideways, equities continuously get cheaper. Additionally, the society aims to solve problems and improve conditions, including fixing bad economies, so measures to mitigate inflation have been implemented and the CPI has been steadily declining for the past year. Better yet, governments and central banks become more sophisticated with each cycle, so are better able to manage downturns today compared to the past.

To summarize, stocks have gone down in price and almost two years have elapsed, while the inflation backdrop has improved. This bodes well for long-term investors.

Of course, the battle against inflation is ongoing. The labor market remains historically tight, and the Fed has more work to do to ensure it does not overheat. However, as John Templeton eloquently said, “Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.”

Currently, many investors harbor skepticism or outright pessimism about the possibility that we may have entered a bull market. At the same time, policymakers and corporations are prepared for a reacceleration in inflation and are now better equipped to respond than they were last year if such a situation arises.

Given this backdrop, I am optimistic about the Fund’s prospects of achieving satisfactory returns in the coming years - especially since our holdings consist of attractively valued, growing businesses.

Game selection

Game selection may be the most important decision an investor can make. The more competitive the game, the more efficient security prices will be on average, meaning less alpha available for capture.

The most competitive public market investing games, in my experience, involve focusing on liquid large-cap stocks that are either:

(i) widely covered with clearly recognizable business quality (whether good or bad); or

(ii) have an obvious catalyst that may trigger a big move in share price over the coming months and quarters.

Regarding category (i), the best businesses usually command high multiples, effectively guaranteeing some multiple contraction over time. They are typically priced to deliver market-like returns driven by above-market EPS growth, offset by ongoing multiple compression. For these to generate above-market returns, their growth must be more durable than what is being priced in–so that earnings surpass consensus and there is less near-term multiple contraction. If growth aligns with or falls below expectations, then they will likely end up delivering underwhelming returns due to multiple contraction.

With respect to category (ii), catalyst-rich special situations are a fertile hunting ground for stocks that can move quickly. Consequently, they attract significant attention from institutional capital–which, in many cases, is set up to optimize performance for “this calendar year” - causing them to be priced more efficiently. On top of that, many event-driven opportunities involve sub-par companies that command less investor interest in the absence of a catalyst. Thus, if an expected catalyst fails to materialize, there are many sellers and not a lot of buyers; obviously, this is not a great backdrop for capital preservation.

Fortunately, the Fund has the flexibility to play in less competitive, more winnable games. This involves looking at smaller, off-the-radar investments and extending our investment horizon beyond the immediate twelve months.

Over time, I have developed and refined a process that allows me to source, vet, and invest the Fund’s capital in high-quality businesses that trade at below-market multiples. As earnings grow, it is my belief that we are less likely to suffer from multiple contraction and could possibly even enjoy multiple expansion during our ownership period.

The value of using conservative assumptions

When underwriting an investment, it is prudent to use conservative base case assumptions. If an acceptable return isn’t achievable with conservative assumptions, then the stock probably isn’t cheap enough to warrant initiating an investment.

This principle is critical because if your assumptions aren’t conservative when you first invest, then you will almost certainly make them conservative once a position starts to move against you. Losing faith in investment after a decline in price is not a good way to generate strong long-term returns.

This lesson applies to growth stories, where people are sizing a TAM and assessing how quickly a company can penetrate it. It also applies to cyclicals, where they are trying to evaluate a stock based on normalized earnings.

Over time, I have found it easier to own businesses that are cheap on normalized earnings and are currently under-earning rather than over-earning. After all, there will inevitably be a period where it seems like a company’s earnings will overshoot normal levels (to the upside or the downside), and I want to benefit from potential overextrapolation rather than be harmed by it.

For this reason, the Fund’s holdings tend to be in companies where I believe the true earnings potential is higher than what current reported numbers suggest.

Current positioning

At quarter-end, the Fund’s top five positions accounted for approximately 70% of capital. This is a bit more concentrated than usual. However, I believe the weightings are justified by the highly attractive risk-adjusted IRRs. Below are my latest thoughts on each of these holdings.

Basic-Fit ( BSFFF ) ((BFIT))

As outlined in the Fund’s Q4’21 letter , BFIT is the largest low-cost gym operator in Europe, with approximately 1,300 locations and four million members. After experiencing significant member attrition during COVID, the company’s mature locations are finally expected to surpass pre-COVID membership levels and profitability this year.

Having nearly tripled its location count over the prior six years, BFIT plans to continue growing locations by 15%+ for the foreseeable future. Given the robust unit economics and rapid paybacks, the company is well-positioned to internally fund this growth and eventually return capital to shareholders, as well.

Since new locations are unprofitable until they ramp, the company’s reported profitability significantly understates its steady-state earnings power. This discrepancy should gradually decline as more locations mature, allowing free cash flow to significantly outpace location growth in the coming years.

Nearly all the company’s revenues are driven by recurring monthly membership fees. Better yet, low-cost gyms have historically demonstrated resilience during economic downturns as people trade down from high-cost options. Additionally, many small private European gym operators, still financially unstable post-COVID, lack access to capital markets like BFIT. Therefore, in the event of a severe recession, BFIT stands to gain from reduced competition, leading to accelerated membership growth, more attractive new locations, and more favorable lease terms.

The company’s CEO, who holds a 15% stake in the company, was a cofounder of HealthCity in 1984, which eventually acquired BFIT in 2013. He is an excellent operator who is highly aligned with us.

Reason for mispricing: Rapid unit growth and COVID-related membership attrition have distorted underlying business profitability.

dentalcorp ([[DNTCF]], [[DNTL:CA]]) ((DNTL))

DNTL, the largest dental practice operator in Canada, with over 500 practices, continues to remain a stable, growing, and cash-generative business, as I explained in the Q1’23 letter . The company’s strategic review process ended without a sale, which led to a drop in the share price. This presented an excellent opportunity for us to significantly increase the Fund’s position.

DNTL has margin upside, as well as a long reinvestment runway where it can redeploy its free cash flow into practice acquisitions at attractive returns.

Reason for mispricing: Inflation, rising rates, and inflated bolt-on multiples led to the company missing consensus estimates post-IPO. Furthermore, leverage is slightly higher than is typical for a high-quality public company. Lastly, there has been significant selling from event-driven investors following the conclusion of the strategic alternatives review. However, I believe that estimates have bottomed, leverage should decline meaningfully over the next few years, and the event-driven selling is almost done.

IWG ( IWGFF ) ((IWG))

As a global leader in the flex office market, IWG is transitioning towards a capital-light business model, which I discussed in the Fund’s Q3’22 letter. Despite the negative perceptions associated with the office market, IWG stands to benefit from high office vacancies, as landlords are pushed to explore capital-light managed partnerships with IWG.

Recently, a large UK-based investment firm turned into a forced seller of its holdings when its founder was accused of sexual assault. Following the accusations, several of the fund’s counterparties terminated their relationships while redemption requests from investors accelerated. The fund owned a significant position in IWG that would have likely taken it many months to liquidate in the open market. Over the last few weeks, a UK-based trading house put together some block trades to help clean up this forced seller. I believe that the near-term pressure associated with this has been alleviated.

I put together a comprehensive write-up on IWG. Please reach out to me if you’d like to receive a copy.

Reason for mispricing: Investors underestimate and undervalue the new managed-partnership business line. Also, IFRS-16 lease accounting makes IWG appear highly leveraged. Lastly, it is a UK-listed, small cap that is focused on office space. However, leverage is not as high as it appears and the company is likely to re-list in the US, its largest market, within twelve to eighteen months.

KKR & Co ( KKR )

As a leader in the alternative asset management space, KKR has seen tremendous growth in AUM from just shy of $200 billion when I first highlighted the company in the Fund’s Q2’19 letter, to over $500 billion today. Additionally, dry powder has grown from $60 billion back then to over $100 billion currently.

Importantly, many of KKR’s businesses remain subscale relative to their potential, including real estate, infrastructure, credit, Asia, and democratized products for high-net-worth individuals. Within a reasonable period, I believe KKR’s AUM can still grow several multiples relative to its current levels.

Currently, KKR’s realizations have slowed, meaning that performance and investment income have declined significantly, and there is very little visibility on when they may come back. However, these earnings are simply deferred rather than lost.

Reason for mispricing: During bull markets, investors fear owning levered beta into a potential downturn. During bear markets, the alts have very limited earnings visibility and fundraising slows meaningfully. As such, the alts continue to trade at low multiples despite consistently growing at attractive rates through multiple cycles.

Limbach ( LMB )

The Fund’s Q1’23 letter outlined my reasoning for reinitiating a core position in LMB, an HVAC–focused specialty contractor. The company has historically sold most of its work through general contractors but has been transitioning towards building owners. I continue to be impressed by the new CEO’s vision for the existing business and future M&A opportunities.

LMB has a net cash balance sheet and is currently benefiting from a strong demand environment, allowing it to be even more selective with new engagements (higher quality, higher margin projects). It is using this environment to be long-term greedy by developing and strengthening its relationships with the types of customers who most highly value LMB’s expertise–operators of mission-critical infrastructure.

I expect LMB to continue expanding margins meaningfully over the next few years while deploying its FCF into highly accretive M&A.

Reason for mispricing: Limbach is undergoing management change and transformation towards an owner-direct model, with an underappreciated opportunity to consolidate its industry at attractive valuations.

Economic sensitivity

I have strategically positioned the Fund towards holdings with recurring business models and limited economic sensitivity. BFIT benefits from recurring gym membership fees. DNTL provides dental services that are necessary regardless of economic conditions. With respect to IWG, most businesses still need office space whether their revenues are growing or declining. KKR earns very predictable management fees from its committed capital. Owners of mission-critical infrastructure still need LMB to help them maintain and improve their HVAC systems in good times and in bad.

Additionally, each of these investments would likely capitalize on a potential downturn. BFIT could see increased demand as consumers trade down and as competitors shut their doors in an economic slowdown. It can also get better locations and more attractive lease terms as it continues to grow. DNTL would have the opportunity to acquire more dental practices at lower valuations while driving improved performance by leveraging its best practices, scale, and shared services. Building owners will increasingly seek help from IWG to fill empty spaces if demand for traditional office leases continues to decline. At the same time, smaller flex operators would likely go out of business. KKR could deploy its $100 billion dry powder at more attractive valuations, which would lead to higher future returns, carry, and AUM growth. LMB should be able to complete more acquisitions at lower prices if its core business slows

Outlook

In the Fund’s Q2’22 letter , I stated that “to continue owning risk assets…investors must believe that the Fed governors have zero appetite to repeat the mistakes made by their predecessors in the early 70s and will do whatever it takes to squash inflation, even if it means pushing the economy into a recession.”

Since that time, the Fed has raised short-term rates from 2% to over 5%. At the same time, CPI has steadily marched lower. After hitting a post-COVID peak of 9% last June, its most recent reading was 3% just twelve months later. The combination of higher rates and reopening of supply chains has thankfully slowed inflation without pushing the economy into a recession–yet.

However, as mentioned in the opening section of this letter, the labor market remains historically tight, and the Fed likely wants to see demand slow further to ensure that inflation does not reaccelerate. Its job is complicated by a federal government that continues to run large fiscal deficits, which is inflationary. Accordingly, the Fed may continue to raise rates to ensure its fight against inflation is complete. Because of this, many are calling for a recession later this year or sometime in 2024.

Of course, now that markets are well off their 2022 lows, animal spirits are starting to flow once again. In fact, we are seeing increasing signs of speculation in certain assets - especially in unprofitable growth companies and those positioning themselves as beneficiaries of key trends, like artificial intelligence. In many ways, the speculation is reminiscent of what we saw in the 2021 meme and SPAC manias.

Of course, I have not and will not participate in such mania.

If anything, I believe that risks are equally balanced to the upside and downside. If inflation continues to slow and the economy doesn’t fall into a deep recession, then there is a very steep wall-of-worry that the market can likely continue to climb.

However, with equities now well off their 2022 lows, there is clearly a greater degree of near-term downside should a severe recession materialize. As such, it is more important now than at any time in the past year to stay vigilant and avoid taking on unnecessary risks in the portfolio - whether through taking on leverage or compromising on business quality.

While I continue to run the Fund with the goal of generating attractive through-cycle returns rather than avoiding near-term volatility, I have steered the portfolio into names that can withstand and capitalize on any economic slowdown should one occur.

To summarize, I love what we own and very much believe our holdings can deliver strong results regardless of what the economy does in the coming years.

Personal updates

I am pleased to announce that my wife and I welcomed our second child in early June. Our new arrival has already started pitching some great ideas that have made their way to the top of the watch list–which bodes well for prospective returns of the partnership!

As always, I am excited to see what the future has in store for the Fund. Thank you for your continued support and confidence. Please reach out with any questions.

Sincerely,

Yaron Naymark

Monthly Performance Summary 2

{kind=link}

1 Performance data is presented for the Fund’s Class A Interests, and is net of any accrued incentive allocation, management fees, and other applicable expenses (as disclosed in the Fund’s Confidential Private Offering Memorandum), include the reinvestment of dividends, interest, and capital gains, and assume an investment from inception. Returns for month-end and year-to-date 2023 are estimated and unaudited. For investor-specific returns, please refer to your capital statements. Due to the format of data available for the time periods indicated, net returns are difficult to calculate precisely. Please see the last page for important disclosure information.

2 Performance Data is presented for the Fund’s Class A Interests, and are net of any accrued incentive allocation, management fees, and other applicable expenses (as disclosed in the Fund’s Confidential Private Offering Memorandum), include the reinvestment of dividends, interest, and capital gains, and assume an investment from inception. Returns for month-end and year-to-date 2023 are estimated and unaudited. For investor-specific returns, please refer to your capital statements. Due to the format of data available for the time periods indicated, net returns are difficult to calculate precisely. Please see the last page for important disclosure information.

IMPORTANT DISCLOSURES

In general. This disclaimer applies to this document and the verbal or written comments of any person presenting it (collectively, the “Report”). The information contained in this Report is provided for informational purposes only and does not contain certain material information about 1 Main Capital Partners, L.P. (the “Fund”), including important disclosures and risk factors associated with an investment in the Fund, and no representation or warranty is made concerning the completeness or accuracy of this information. To the extent that you rely on the Report in connection with an investment decision, you do so at your own risk. Certain information contained herein was obtained from or provided by third-party sources; although such information is believed to be accurate, it has not been independently verified. The information in the Report is provided to you as of the dates indicated and 1 Main Capital Management, LLC and its affiliates (collectively, the “Manager”) do not intend to update the information after its distribution, even in the event the information becomes materially inaccurate.

No offer to purchase or sell securities. This Report does not constitute an offer to sell, or the solicitation of an offer to buy, and may not be relied upon in connection with the purchase of any security, including an interest in the Fund or any other fund managed by the Manager. Any such offer would only be made by means of such fund’s formal private placement documents, the terms of which shall govern in all respects.

Performance Information. Unless otherwise noted, any performance numbers used in the Report are for the Fund’s Class A Interests and are net of any accrued incentive allocation, management fees, and other applicable expenses, include the reinvestment of dividends, interest, and capital gains, and assume an investment from inception of such Class. As such, the performance numbers do not reflect the performance of any particular investor’s interest and you should not rely on it as a statement of your actual return.

Past performance. In all cases where historical performance is presented, please note that past performance is not a reliable indicator of future results and should not be relied upon as the basis for making an investment decision.

Risk of loss. An investment in the Fund will be highly speculative, and there can be no assurance that the Fund’s investment objective will be achieved. Investors must be prepared to bear the risk of a total loss of their invested capital.

Portfolio Guidelines/Construction. Information contained in this Report, especially as it pertains to portfolio characteristics, construction, profiles or investment strategies or objectives, reflects the Manager’s current thinking based on normal market conditions, and may be modified in response to the Manager’s perception of changing market conditions, opportunities or otherwise, in the Manager’s sole discretion, without further notice to you. Any target strategies, objectives, or parameters are not projections or predictions and are presented solely for your information. No assurance is given that the Fund will achieve its investment strategies, objectives, or parameters.

Index Performance. The index comparisons are provided for informational purposes only. The S&P 500 Total Return Index ((SPXT)) is a capitalization-weighted index that is designed to measure the performance of the broad U.S. economy through changes in the aggregate market value of 500 stocks representing all major industries. There are significant differences between the Fund and the index referenced, including, but not limited to, risk profile, liquidity, volatility, and asset composition. The index reflects the reinvestment of dividends and other income, is unmanaged, and do not reflect a deduction for advisory fees. An investor may not invest directly into an index. For the foregoing and other reasons, the performance of the index may not be comparable to the Fund’s and should not be relied upon in making an investment decision with respect to the Fund.

No tax, legal, accounting, or investment advice. The Report is not intended to provide, and should not be relied upon for, tax, legal, accounting, or investment advice.

Logos, trade names, trademarks, and copyrights. Certain logos, trade names, trademarks, and/or copyrights (collectively, “Marks”) contained herein are included for identification and informational purposes only. Such Marks may be owned by companies or persons that are not affiliated with the Manager or any of the Manager-managed funds and no claim is made that any such company or person has sponsored or endorsed the use of such Marks in the Report.

Confidentiality/Distribution of the Report. The information in this Report is confidential. By accepting any portion of the Report, you agree that you will treat the Report confidentially. It is intended only for the use of the person to whom it is given and the Manager expressly prohibits its redistribution without the Manager’s prior written consent. The Report is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to law, regulation, or rule.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

1 Main Capital Partners Q2 2023 Fund Letter