DEA - 1 REIT To Buy 1 REIT To Sell

2023-08-01 13:06:07 ET

Summary

- REIT valuations have declined by over 25% in the past year and a half, creating opportunities to buy undervalued REITs.

- It is important to choose REITs with increased cash flows and avoid those with declining cash flows to avoid dividend cuts.

- I give you one REIT to buy and one REIT to sell.

Dear readers/followers,

It's no secret that REIT valuations ( VNQ ) have compressed significantly over the past year and a half with the broader REIT index declining by over 25%.

The selloff has created many opportunities to buy undervalued REITs, but the reasons that caused the selloff have also significantly increased the chances of dividend cuts and overall poor performance. It is now more important than ever to pick wisely and choose the right REITs.

To me that means buying well positioned REITs whose cash flows have increased significantly over the past year and a half, yet their stock price has plummeted. At the same time, it means staying away from REITs whose cash flows have declined increasing the probability of a dividend cut.

Today I give you one REIT to buy and one REIT to sell starting with my sell recommendation.

Easterly Government Properties ( DEA )

DEA is a unique REIT which focuses on single-tenant properties leased to various agencies of the US government. Their leases come with very long durations, with a WAULT of 10.4 years and are backed by the full faith and credit of the United States government.

{kind=link}

DEA Presentation

Sounds great, right? Well, not so fast. It's true that DEA doesn't have to worry about collections which means their rent is highly visible. But just as any other REIT, they still have to do their best to retain tenants when leases expire. Luckily for DEA, the percentage of leases expiring this and next year is quite low at 3.6% and 5.9%, respectively.

But the thing is that eventually, leases will expire and with the ever increasing government deficit it's likely that the government might want to cut costs by consolidating their buildings. Work from home likely won't help either. I expect it to be even more threatening to DEA's buildings than to traditional offices, because government agencies aren't looking at employee productivity as much as corporation, and are therefore more likely to be OK with more people on home office.

Not only that, but DEA is going to hold the shorter end of the stick in re-leasing negotiation, because their buildings are build-to-suit and cannot really be leased easily to another tenant, because of how specifically designed they are. This means that DEA's rent is unlikely to grow and could actually contract if the REIT is forced to provide rent discounts to keep their properties occupied.

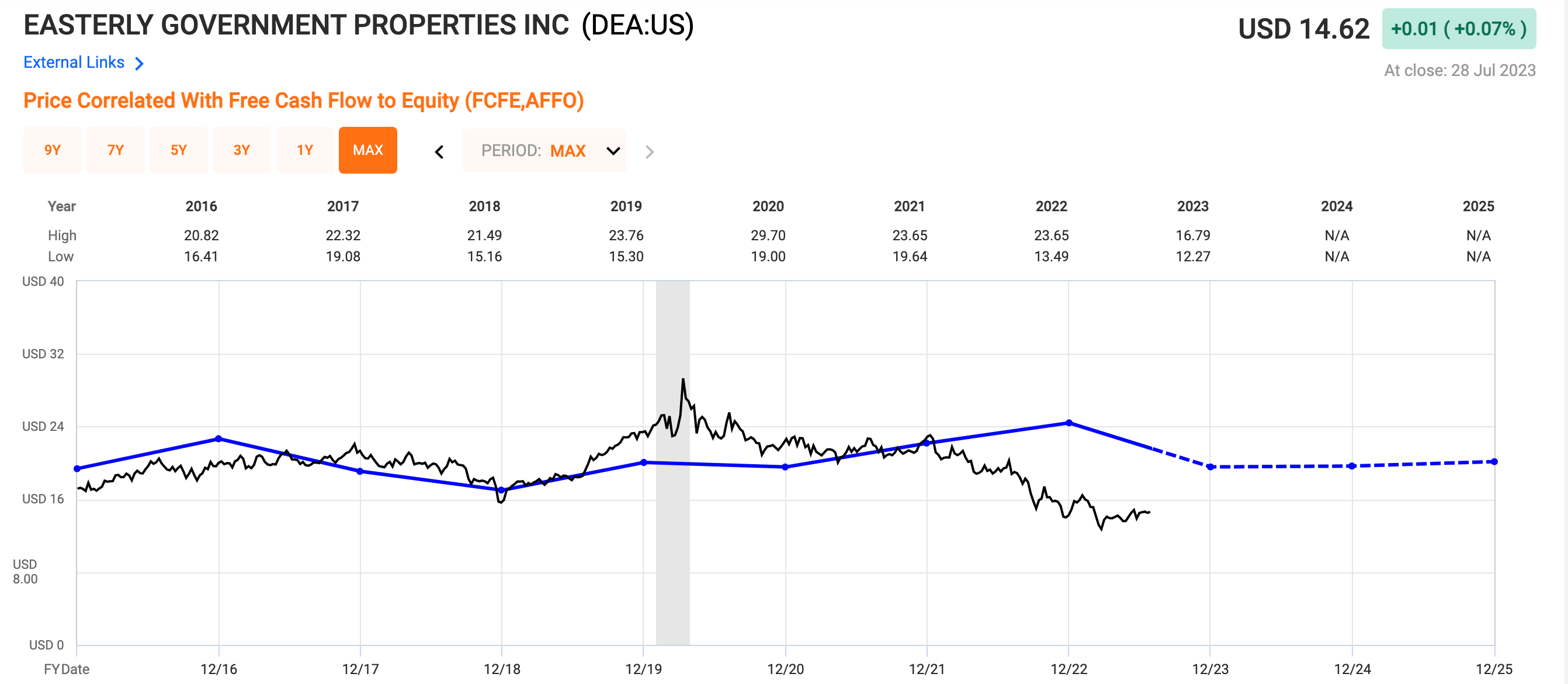

This is nothing new as the company's FFO has been flat over the past 8 years. This to me says one thing - their business model doesn't work, not even during the good times.

{kind=link}

Fast graphs

Add to that high interest rates, work from home, and a potential recession which will put pressure on government spending and it's easy to see that DEA will not have an easy time going forward.

With flat FFO for years, I imagine that one of the primary motivations for people to hold the stock has been the dividend which, given the safety, is quite solid at 7.5%.

But that might change, as the quarterly dividend of $0.265 is currently barely covered by FFO of $0.29 and if we look at cash available for distribution ((CAD)), which includes maintain CAPEX, the payout ratio is already >100%.

99% of the time, when a REIT cuts its dividend, the stock price heads lower. In DEA's case, since people were mainly investing in the stock for its reliable dividend, the consequence would likely be no different. I see no reason to invest in Easterly Government Properties, especially with the plethora of attractively priced and well positioned companies in the market today.

I now give you one such company.

Alexandria Real Estate Equities ( ARE )

Alexandria is another unique REIT. This one focuses exclusively on Life Science tenants, which makes it largely immune to work from home, because you cannot bring a lab home the same way you can bring a laptop.

The bears argue that ARE is essentially an office REIT and is therefore likely to see its occupancy decline at tenants downsize their offices due to WFH. Moreover, they expect a lot of traditional office space to be converted to Life Science lab, driving up competition and decreasing rents.

On conversions, there has been a lot of research done in High Yield Landlord, but let me tell you that they're not as easy as they seem. Life Science buildings thrive in clusters near universities where ideas are generated so unless an office building is in the right location a conversion won't work there.

Moreover, from a technical standpoint, there are many differences from floor strength, loading docks, vibration resiliency, hazardous waste removal and, of course, zoning laws.

Last but not least, conversions are incredibly costly - Rider Levett Bucknall estimates that a conversion from a standard office to a laboratory involves fit-out costs of $90-190 / sft.

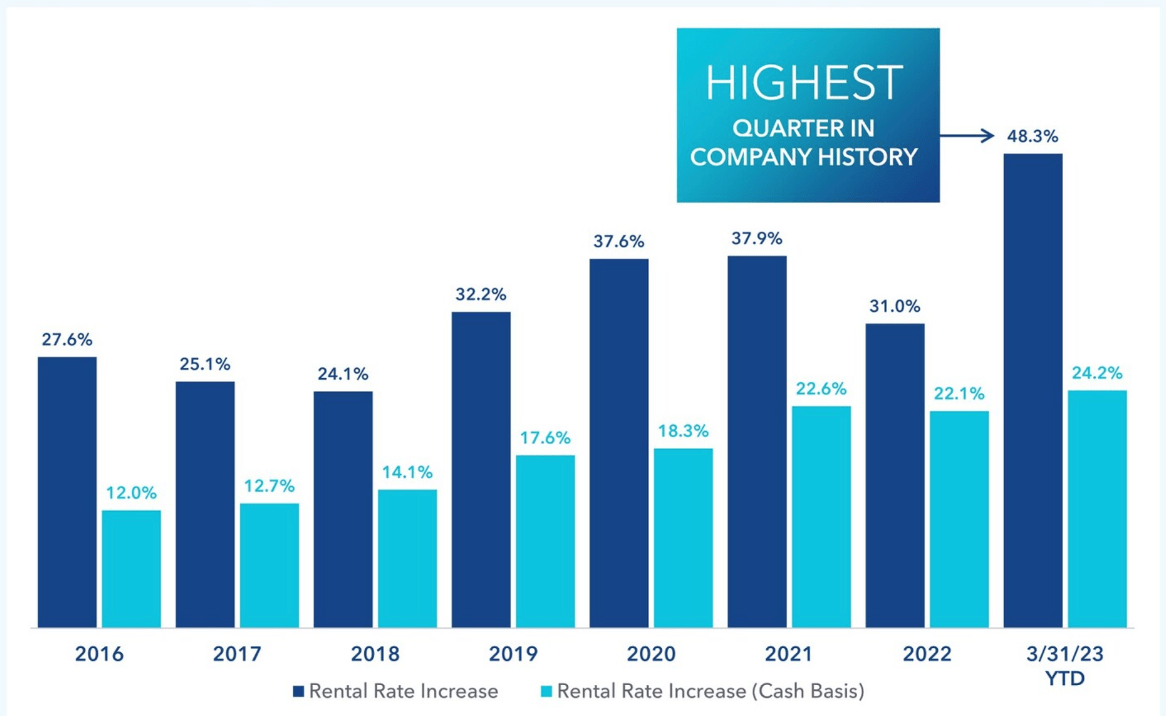

Now on the threat from WFH, I've said it before, but let me say it again. During the most recent quarter, ARE has achieved the highest rent spreads on new leases ever! Spreads reached 48% and 24% on a cash basis. This cannot be explained in any other way than that tenants value the space and they have every intention of keeping it. If this doesn't debunk the bear thesis, I don't know what will.

{kind=link}

With rents so far below market, there's a lot of growth that's essentially locked in and will gradually become unlocked as leases expire.

Moreover, ARE has a vast pipeline of development projects scheduled for completion within the next three years. These new projects will add another $610 Million in incremental NOI which in itself represent about a 30% increase to NOI.

I also want to point out that these development projects are already 73% pre-leased, which means that ARE's growth from here is highly visible and will most likely total 8-10% per year for the next three years.

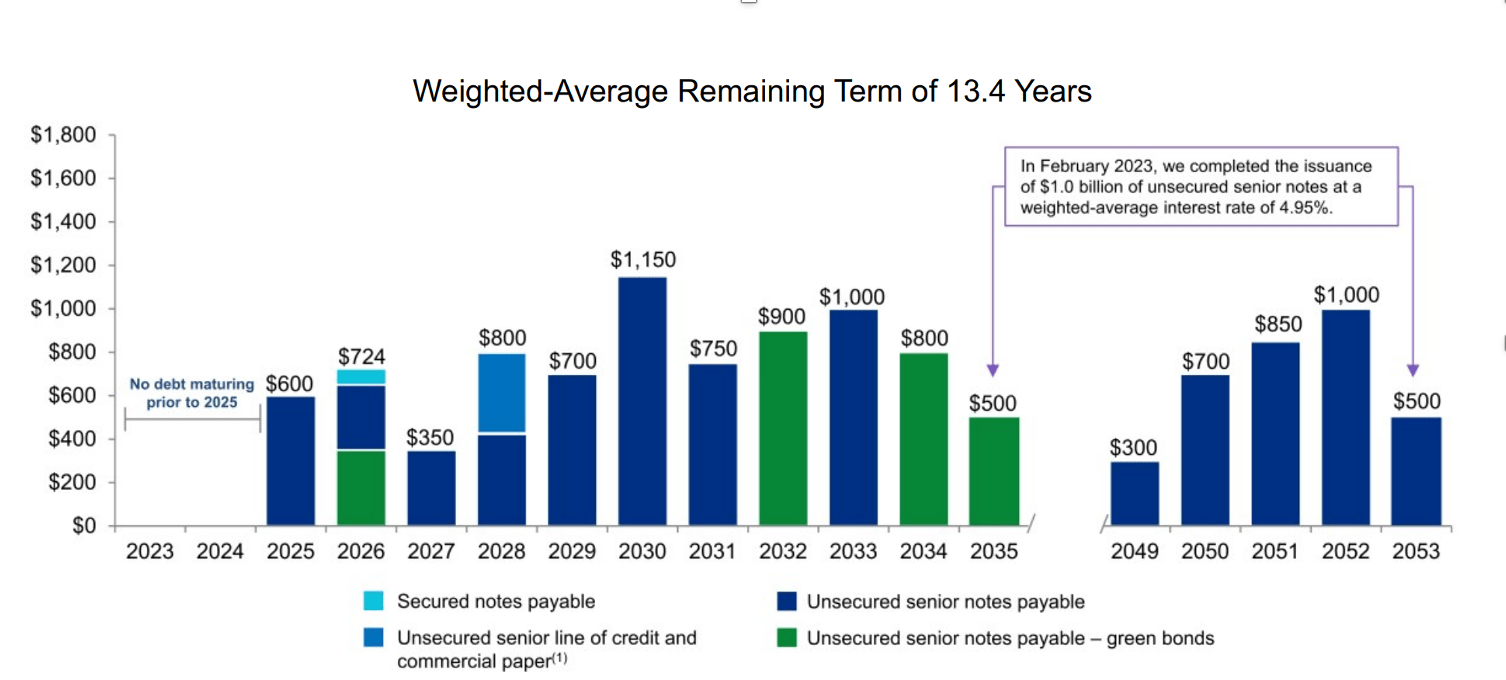

In addition to strong growth prospects, the company also maintains one of the best balance sheets of all REITs. It's BBB+ rated with a very reasonable leverage of 5.3x EBITDA, 96% of debt fixed and a very long weighted average remaining term of 13.4 years. This means that ARE essentially faces no interest rate risk, at least until 2025.

{kind=link}

Despite so many things going right for ARE, the stock price has fallen by about 50% and at one point traded as low as $110 per share. Today, at $126 per share, the stock trades at 18.5x FFO and yields about 4% which in my opinion represent a great opportunity to buy a great company at a great price.

If my REIT thesis plays out the way I expect it, ARE could easily return to 20-22x FFO which in addition to strong FFO growth would result in upside of about 50%.

For further details see:

1 REIT To Buy, 1 REIT To Sell