VICI - 10 Of The Best REITs To Buy For 2024

2023-12-15 09:37:00 ET

Summary

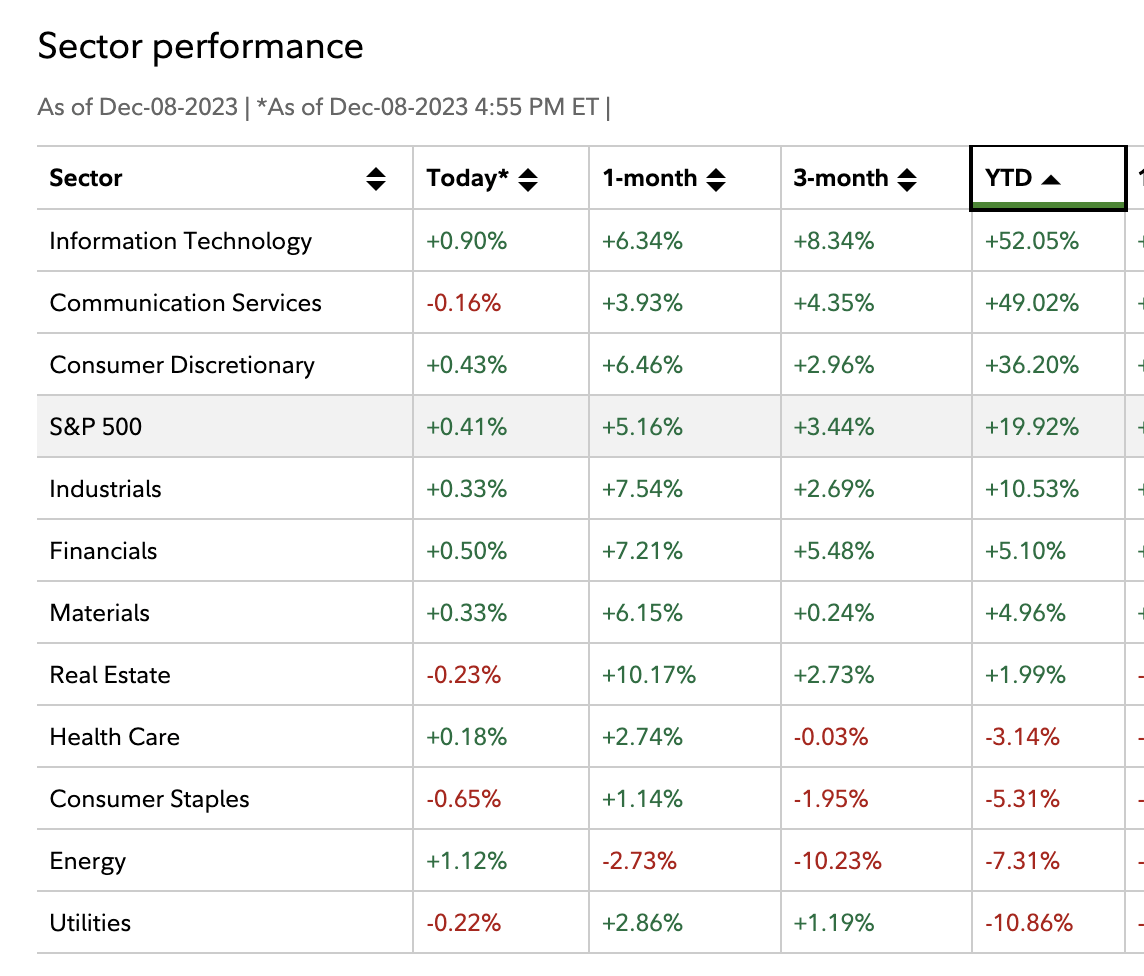

- The real estate sector has been one of the worst-performing sectors in 2023, but recently crossed into positive territory.

- Rising interest rates have negatively impacted REITs, but with the hiking cycle all but completed, REITs are starting to recover.

- There are opportunities to buy high-quality REITs at attractive valuations for 2024.

2023 has been a tough year to say the least for the Real Estate sector as it has been one of the worst-performing sectors year to date. However, given the latest run in the market, the Real Estate sector as a whole finally crossed into positive territory, albeit ever so slightly but still drastically underperforming the S&P 500.

{kind=link}

One of the primary reasons for the underperformance is due to rising interest rates. This was not any normal hiking cycle by the Fed, it was the fastest in recent history.

As such, REITs, an industry that relies on debt to acquire more real estate, faltered. However, with inflation decreasing and investors looking for the Federal Reserve to decrease interest rates in 2024, REITs are beginning to move higher.

Knowing this, and knowing the sheer punishment REITs have taken in the past 18 months, you can still pick up many high-quality REITs at great valuations.

As such, today we are going to take a look at 10 of the BEST REITs to buy for 2024.

10 of the BEST REITs for 2024

REIT #1 - Realty Income Corporation ( O )

Let's begin with the gold standard when it comes to REITs, a favorite among many retail investors and institutional investors alike. Realty Income coined themselves "The Monthly Dividend Company" based on the dividend they pay out every single month.

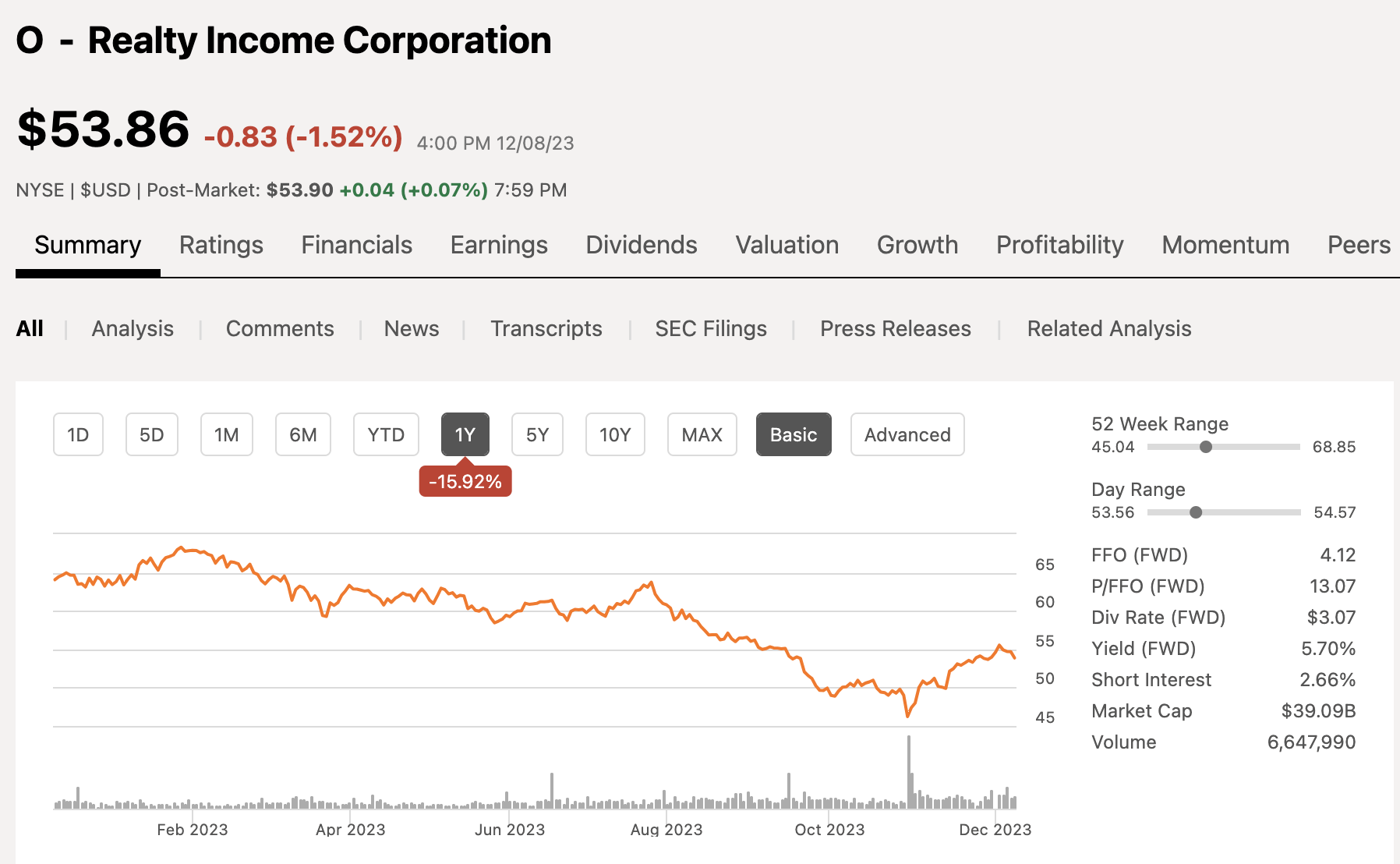

Realty Income operates at as a net lease REIT with a market cap of $39 billion and over the past 12 months the stock has fallen 16%.

{kind=link}

Realty Income has a portfolio of more than 13,250 properties, a number that will increase once they close the pending acquisition of Spirit Realty Capital, Inc. ( SRC ). The portfolio has a high occupancy rate of 98.8% based on their latest quarter.

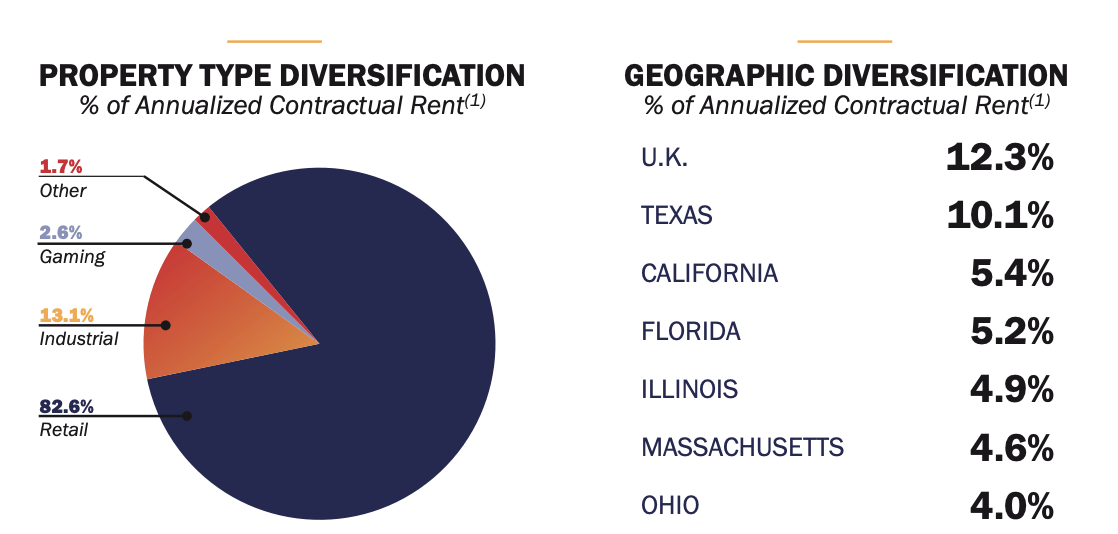

Realty Income is primarily a retail REIT, as that sector accounts for nearly 83% of annualized base rent, with the next largest sector being industrial at 13%, followed by gaming at nearly 3%, and has been a late push by the company the past few years.

{kind=link}

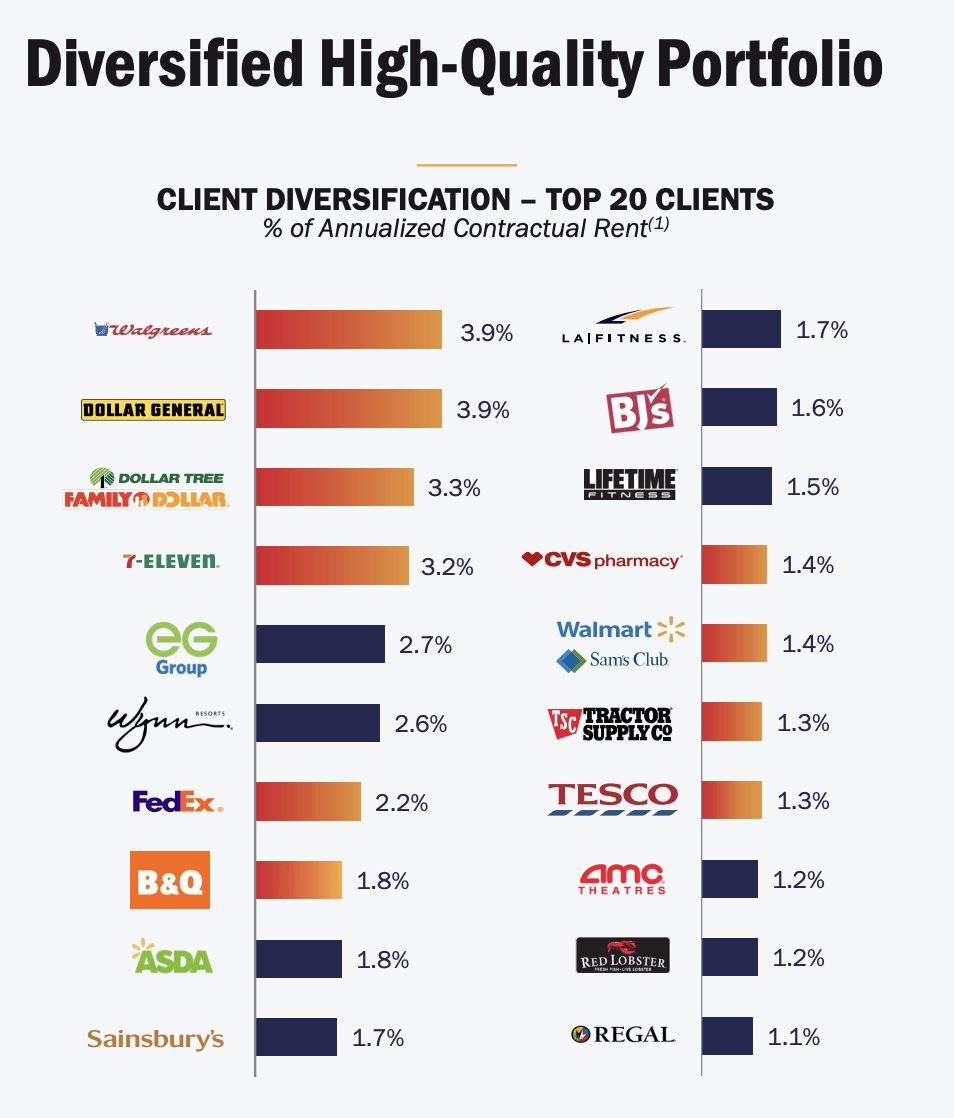

Here is a look at the company's top tenants:

{kind=link}

The portfolio at the top does have some question marks but the good thing is that the REIT is not overexposed to any single tenant.

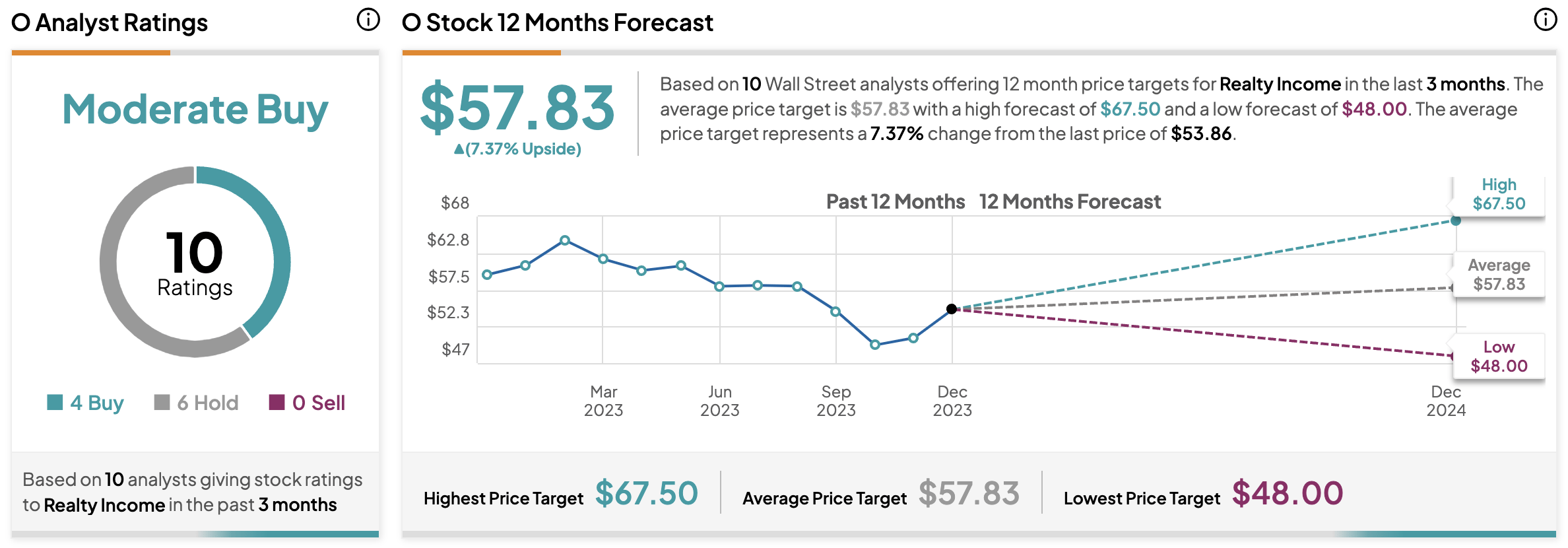

Now for the dividend, which is one of the major reasons why investors like Realty Income. They are about as consistent as they come when it comes to paying a dividend and increasing their dividend. Realty Income is one of three REITs on the dividend aristocrat list, meaning they have paid a growing dividend for at least 25 consecutive years. Realty Income currently yields a high dividend of 5.7%.

{kind=link}

In terms of valuation, analysts are looking for an AFFO of $4.16 per share in 2024, which equates to an AFFO multiple of 12.9x which is well below the company's historical average of 19.4x, providing a lot of value for investors at the current levels.

{kind=link}

Analysts have a 12-month price target of $57.83 per share equating to a little over 7% upside to go along with the nearly 6% dividend yield as well.

{kind=link}

REIT #2 - VICI Properties Inc. ( VICI )

VICI Properties is one of my favorite REITs and it is also my largest REIT holding as well. You have heard me talk about the REIT in the past being the largest landlord on the Las Vegas strip. Never do you see hotel/casino vacancies on the strip.

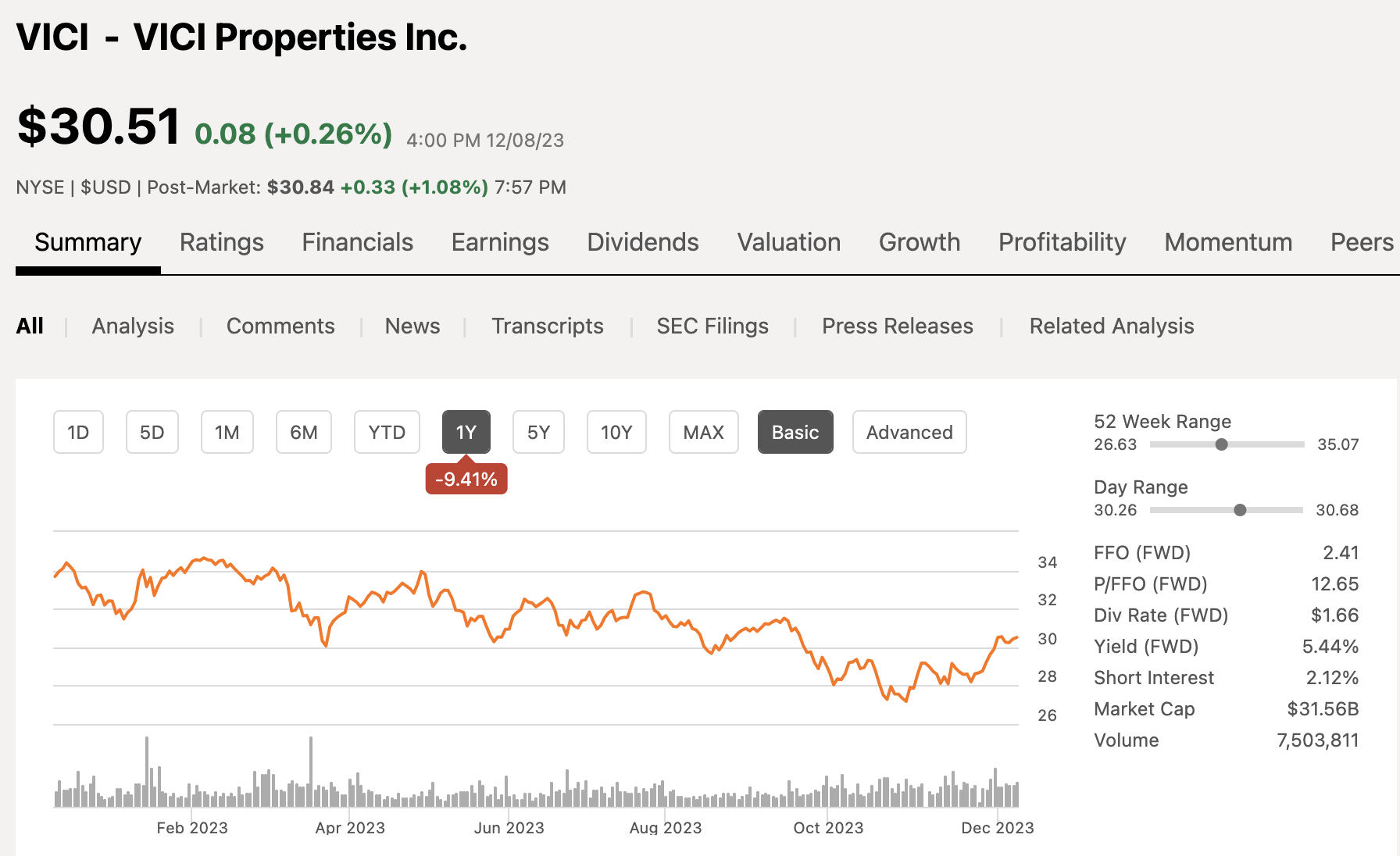

VICI has only been public for about a handful of years so still a relatively new REIT. The company currently has a market cap of $32 billion and over the past 12 months shares of VICI are down nearly 10%.

{kind=link}

VICI has some high-quality assets such as:

- Caesars Palace.

- MGM Grand.

- Park MGM.

- Mandalay Bay.

- New York New York.

- The Mirage.

And many more.

The REIT works with the finest hospitality and casino operators around, and the quality is evident based on the REIT having a 100% collection rate throughout the pandemic, a time when many REITs saw a collection rate of 50%.

Looking at the dividend, VICI has paid a growing dividend every year they have been a public company. They now yield a dividend of 5.4% but they also have some strong dividend growth with an average growth rate over 17%.

{kind=link}

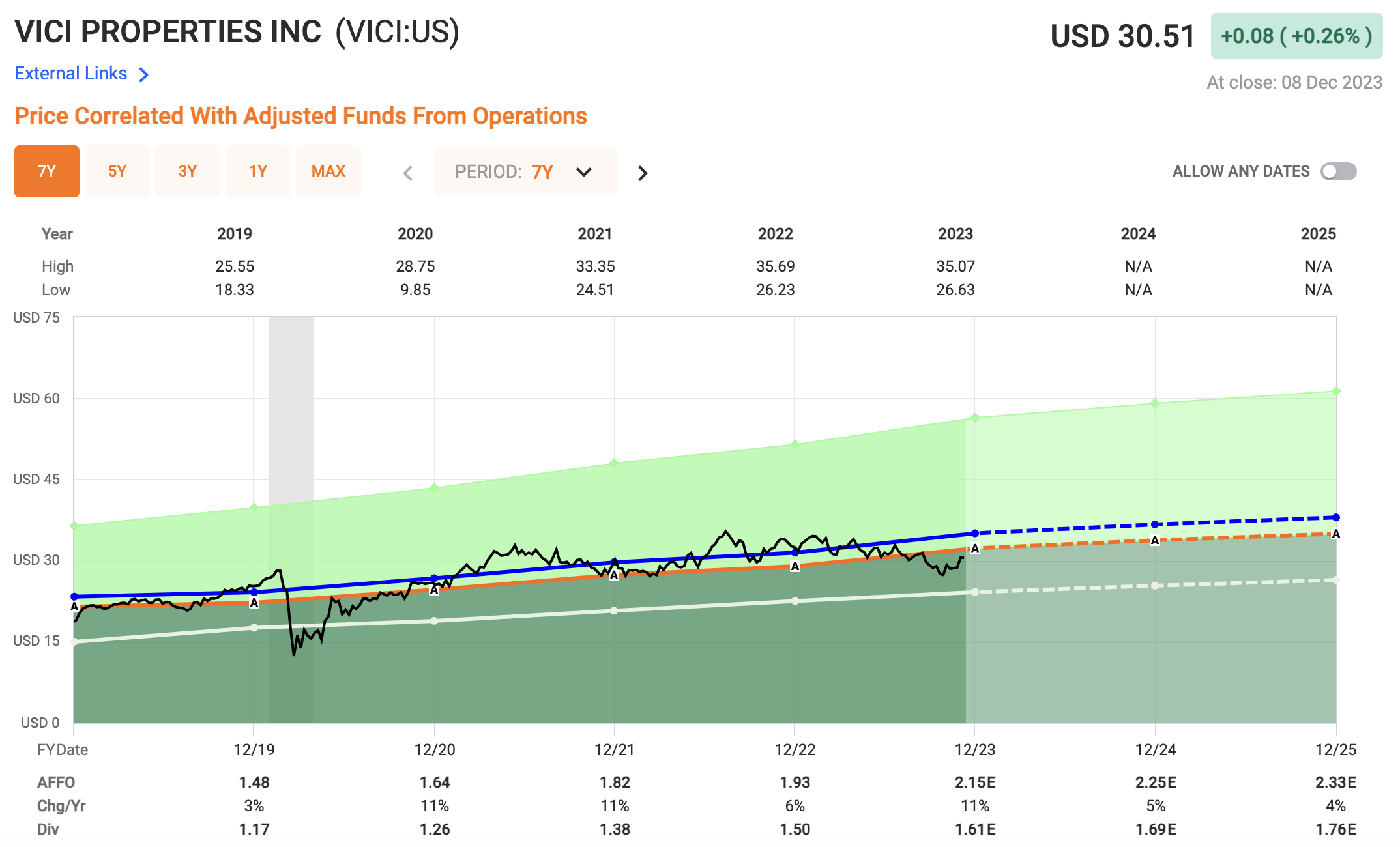

In terms of valuation, analysts are looking for AFFO of $2.25 per share in 2024, which equates to an AFFO multiple of 13.5x which is well below the company's historical average of 16.3x

{kind=link}

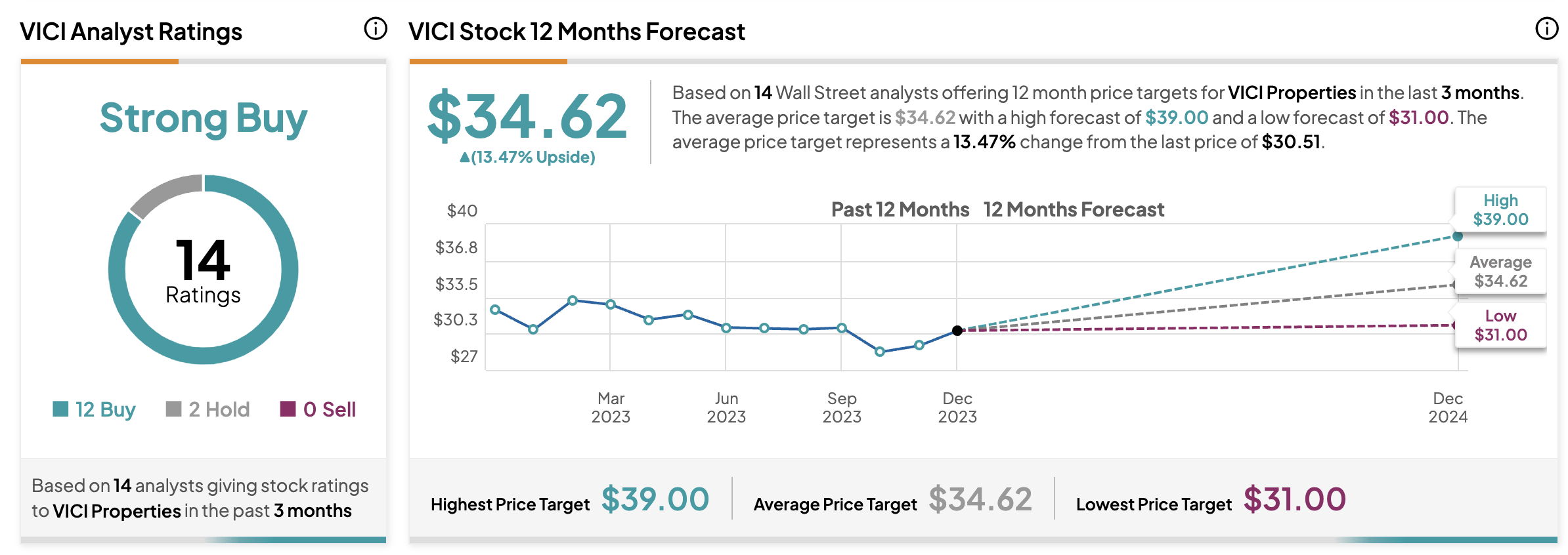

Analysts rate the stock a STRONG BUY with an average 12-month price target of $34.62 per share equating to a 13.5% upside from current levels.

{kind=link}

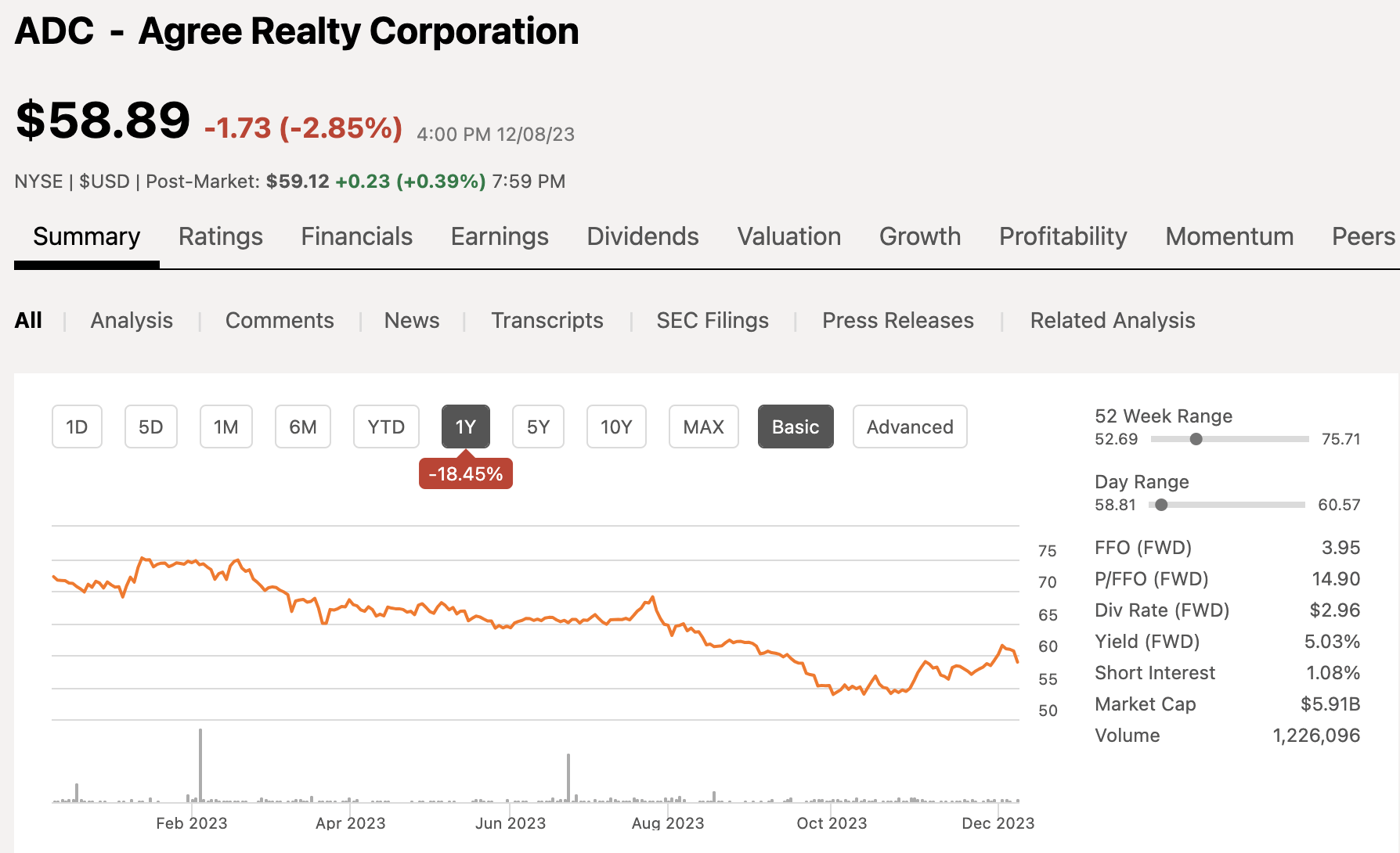

REIT #3 - Agree Realty Corporation ( ADC )

Agree Realty, although not new to the public markets, can be seen as the little sibling to Realty Income. They both operate as a net lease REITs within the retail sector, and they actually both went public in the same year back in 1994.

Agree Realty has a market cap of $6 billion, so much smaller in size than Realty Income. Over the past 12 months, shares of ADC have fallen nearly 20%.

{kind=link}

As you can see, total shareholder return has been 26% over the past 5 years and they have generated an 11.3% compounded average total return since going public back in 1994.

{kind=link}

Now let's have a closer look at the company's portfolio. As you can see, the top three sectors include grocery, home improvement, and auto service, three strong sectors to say the least. The top three tenants include Walmart Inc. ( WMT ), Tractor Supply Company ( TSCO ), and Dollar General Corporation ( DG ). I personally like the top three tenants for ADC more than those of Realty Income.

{kind=link}

Given that the portfolio is a bit smaller than Realty Income, the exposure rate to top tenants is a little more.

In terms of the dividend, ADC has been growing their dividend every year since 2011, the only reason the graphic shows three years is due to the fact that ADC switched from a quarterly paying company to a monthly paying company, yet another thing they now have in common with Realty income. The dividend currently yields 5.0%.

{kind=link}

Looking at valuation, analysts are looking for ADC to generate AFFO of $4.11 per share in 2024, which equates to an AFFO multiple of 14.1x, which is well below their five-year average of 20x.

{kind=link}

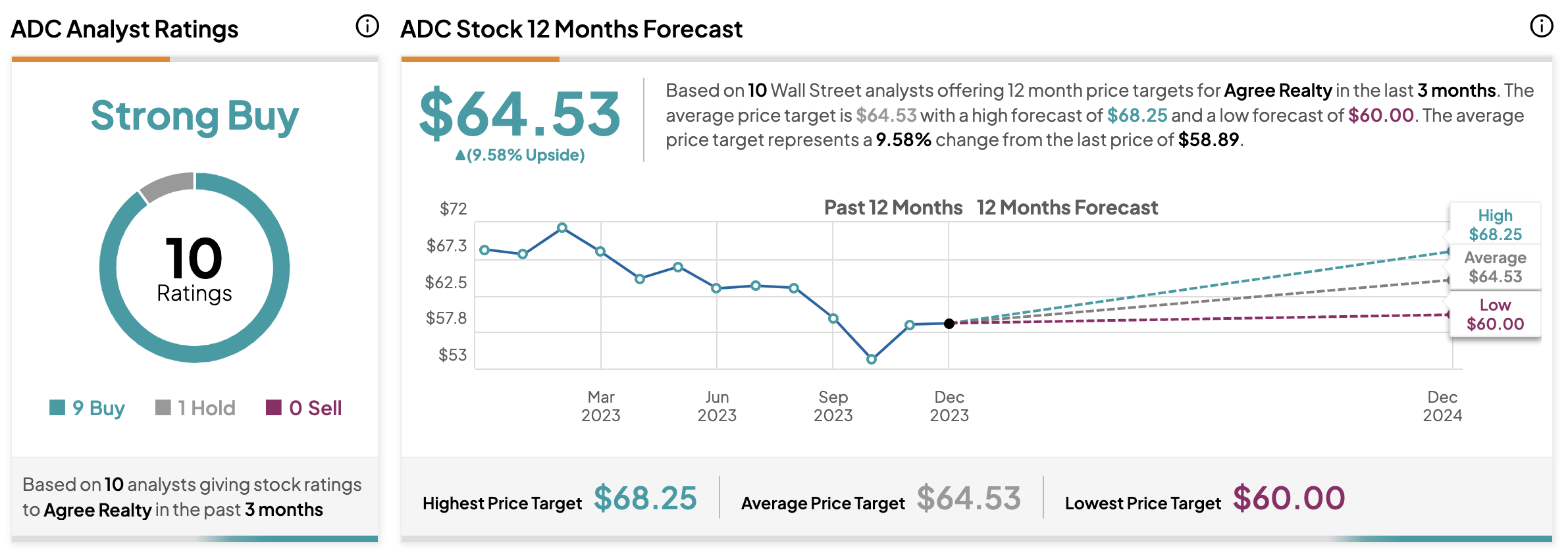

Analysts also rate the REIT a STRONG BUY with an average 12-month price target of $64.53, equating to nearly 10% upside from current levels.

{kind=link}

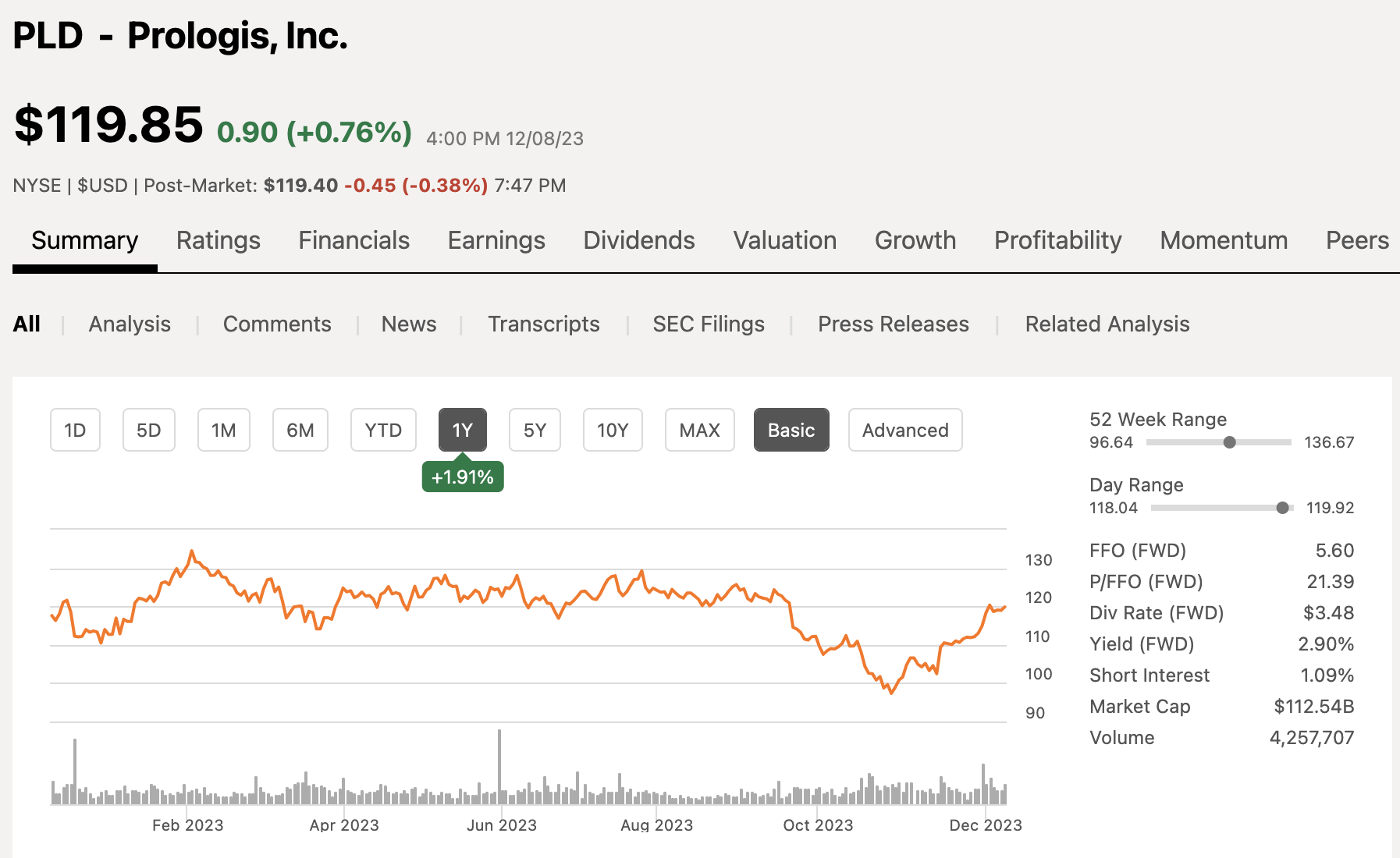

REIT #4 - Prologis, Inc. ( PLD )

Prologis is the largest industrial and warehouse REIT and is an indirect way to play the future growth in e-commerce.

PLD currently has a market cap of $112 billion and over the past 12 months the stock is relatively flat.

{kind=link}

As I mentioned, PLD is a way to play the growth in e-commerce. Most people think about growth of e-commerce and think Amazon.com, Inc. ( AMZN ) and Shopify Inc. ( SHOP ), but those are the ones having to make the sales. You can play the real estate side of things, as those companies or their sellers need somewhere to store all their inventory. Amazon is Prologis' largest tenant.

E-commerce sales currently equate for less than 25% of all retail sales and that number is expected to grow 1 percentage point per year over the next five years. In addition, e-commerce uses 3x as much logistics space as brick and mortar retailers, which all benefits a leader like Prologis.

{kind=link}

The company continues to see solid demand, strong earnings results, and slowing starts across the sector, all benefitting a leader like PLD.

PLD pays an annual dividend of $3.48 per share which equates to a dividend yield of 2.9% In addition, the company has a five-year dividend growth rate of 12.5% with 9 consecutive years of dividend growth.

{kind=link}

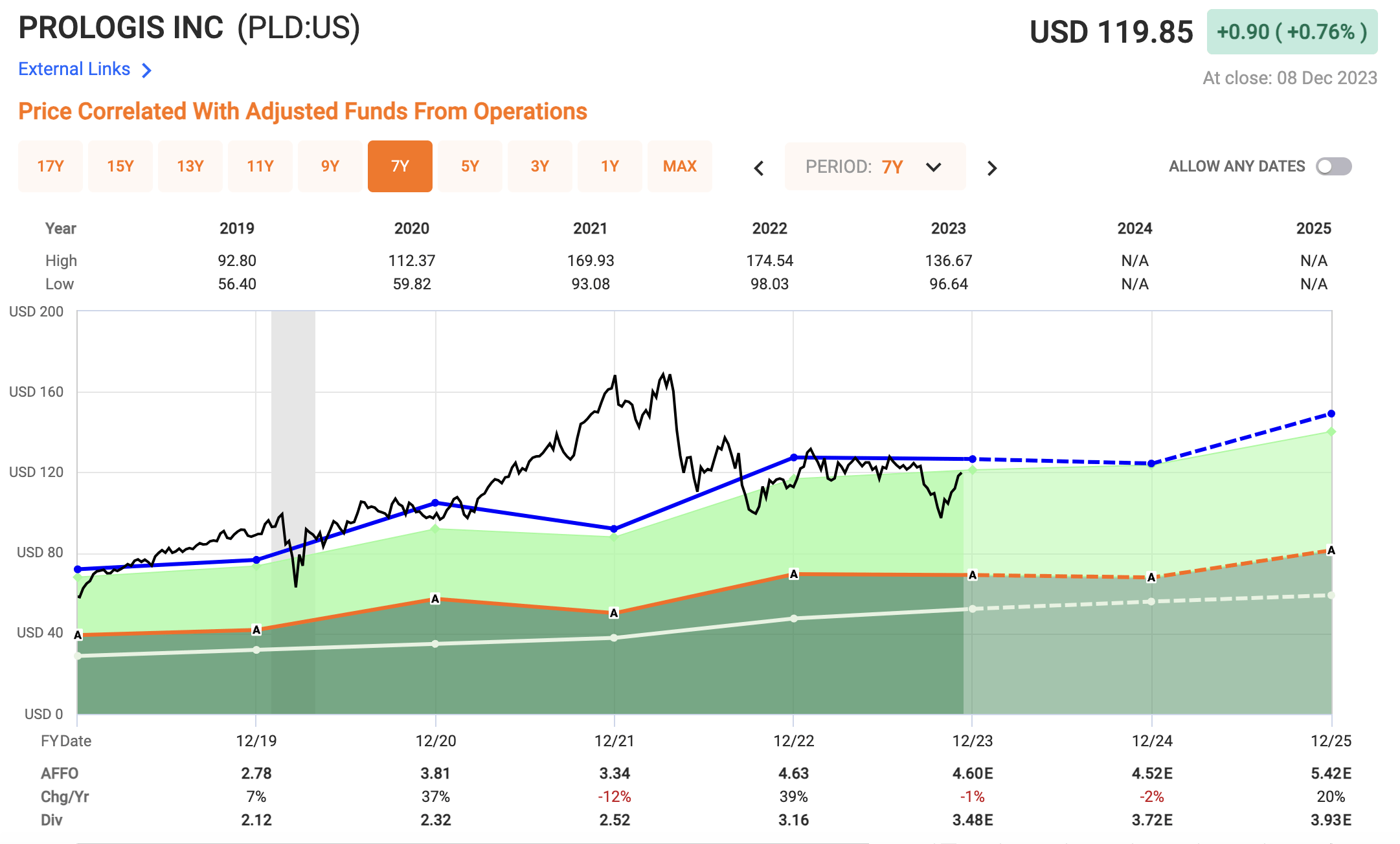

Looking at valuation, analysts are looking for PLD to generate AFFO of $4.52 per share in 2024, which equates to an AFFO multiple of 26.5x, which is below their historical average of 27.5x.

{kind=link}

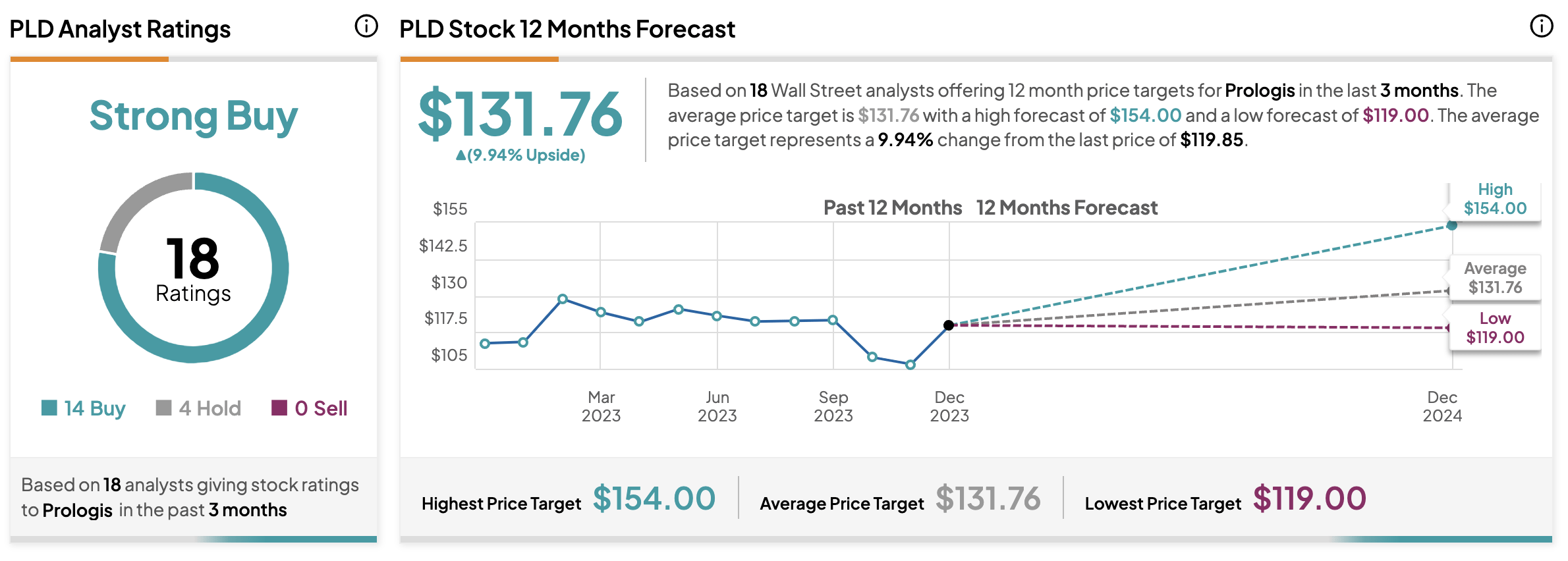

Analysts also rate the REIT a STRONG BUY with an average 12-month price target of $132, equating to nearly 10% upside from current levels.

{kind=link}

REIT #5 - Alexandria Real Estate Equities, Inc. ( ARE )

Alexandria Real Estate has been an interesting REIT and a misunderstood REIT as well. I will get into all of that in just a second.

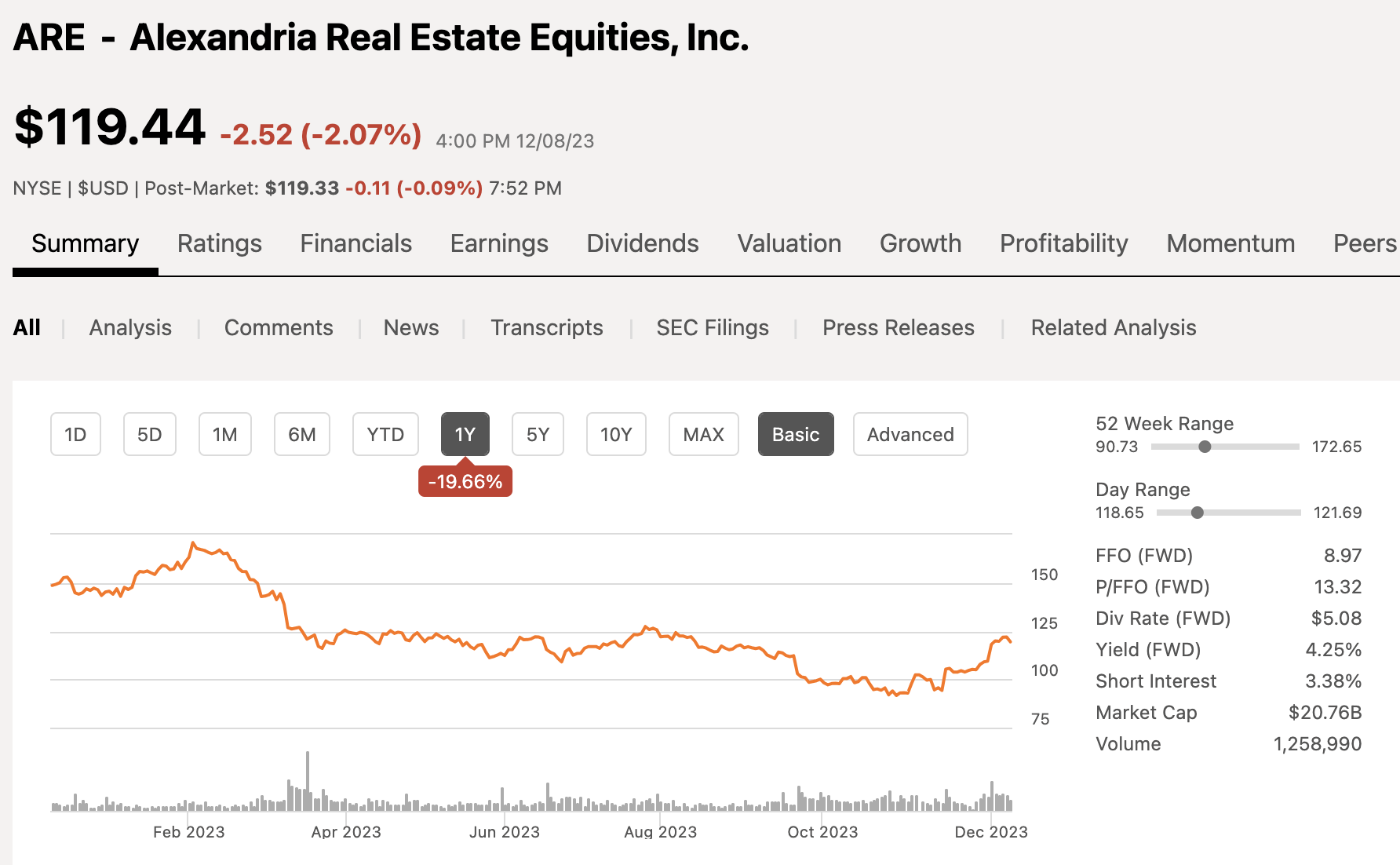

In terms of size, Alexandria has a market cap of $21 billion and over the past 12 months, shares of ARE are down 20%, however, over the past month they are up 20%, so things could be a lot worse.

{kind=link}

Many label the REIT as an office REIT, but it is anything but a traditional office REIT. Traditional office REITs have been far and away the worst sector within Real Estate in 2023 due to high interest rates but more importantly a changing work environment with more flexible work arrangements.

Alexandria caters to the pharmaceutical and biotech sectors, which can differ significantly. In addition, ARE has a number of medical campus properties as well for research, so the demand for research is not slowing for these companies, and if anything, its increasing, which makes ARE very compelling.

If you are a value investor you are definitely going to want to take a closer look at Alexandria Real Estate.

With ARE you get a very low valuation, but you also get a nice dividend that currently yields 4.25%. The dividend has a five-year dividend growth rate of 6% and has been growing for 12 consecutive years.

{kind=link}

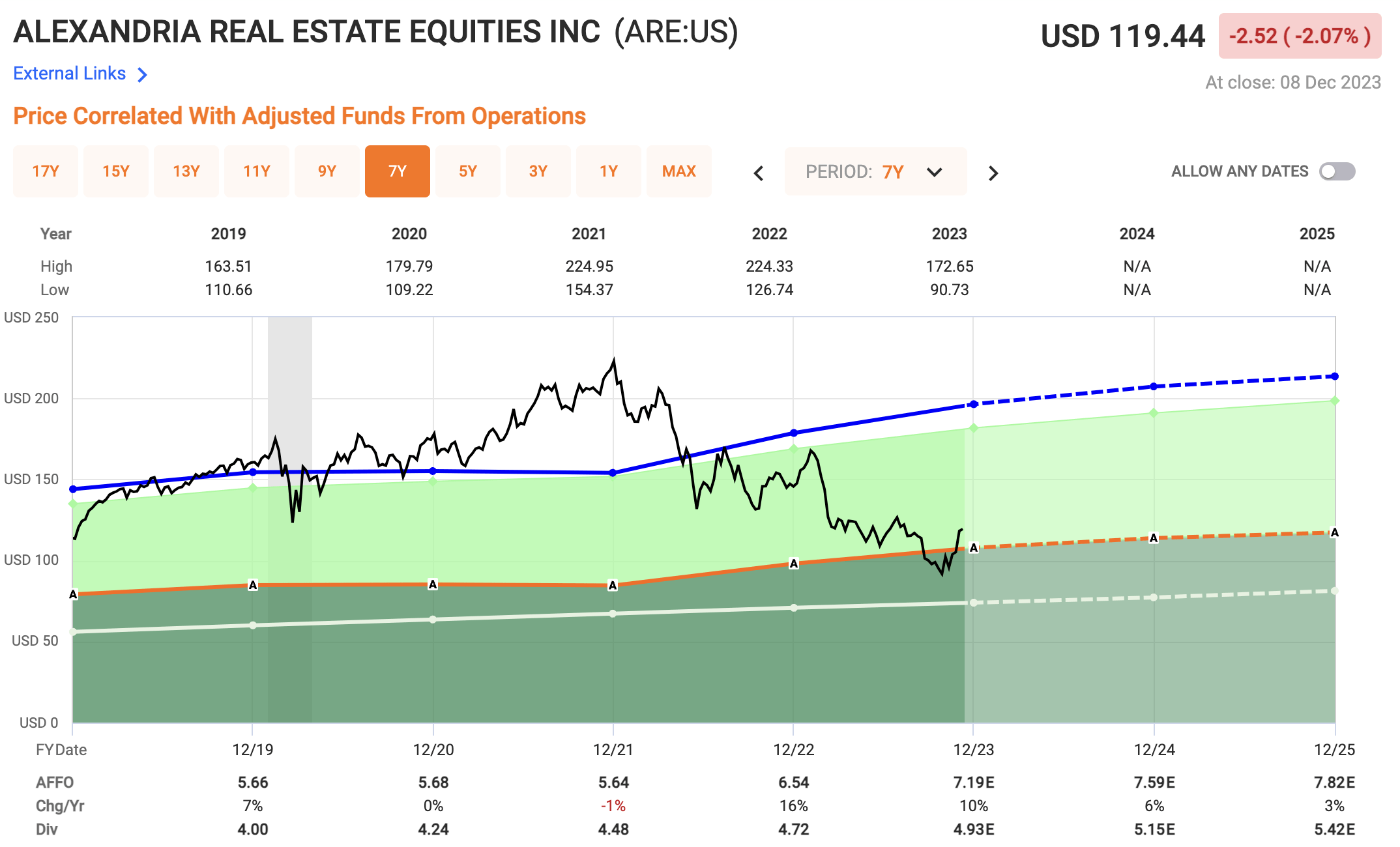

Analysts are looking for ARE to generate AFFO of $7.59 per share next year, growing 6%. This equates to a forward AFFO multiple of 15.7x, well below their five-year average of 27.3x.

{kind=link}

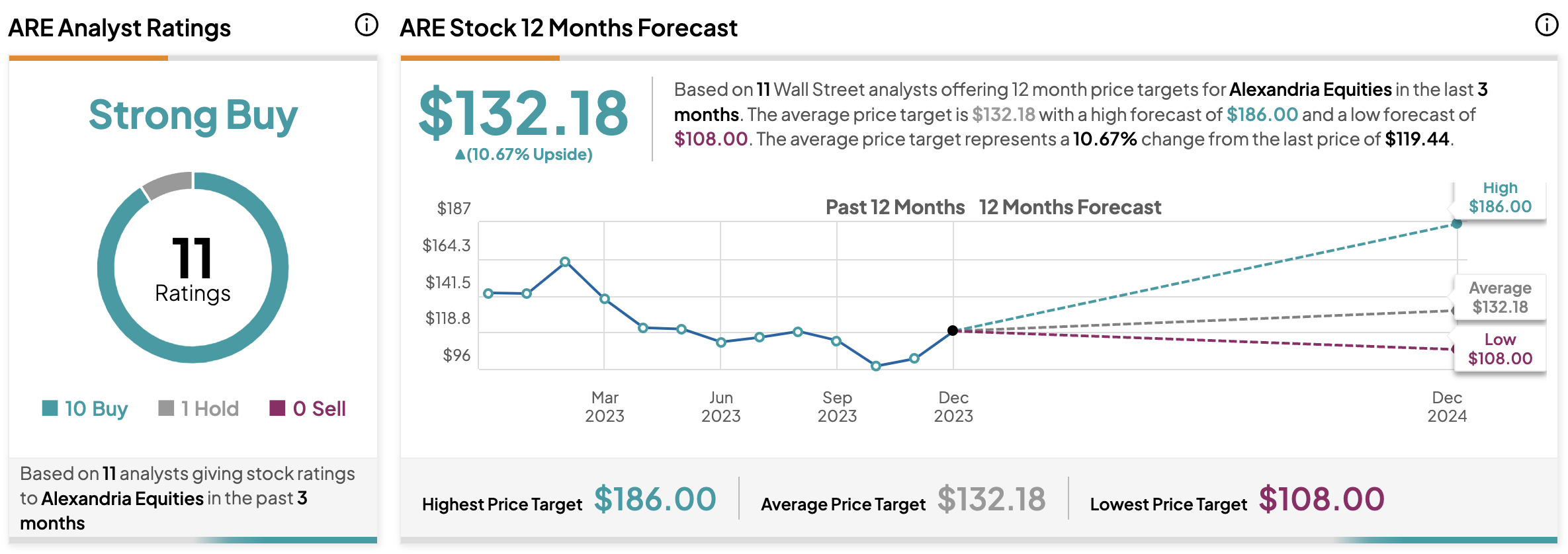

Analysts rate the REIT a STRONG BUY with an average 12-month price target of $132, implying more than 10% upside from current levels.

{kind=link}

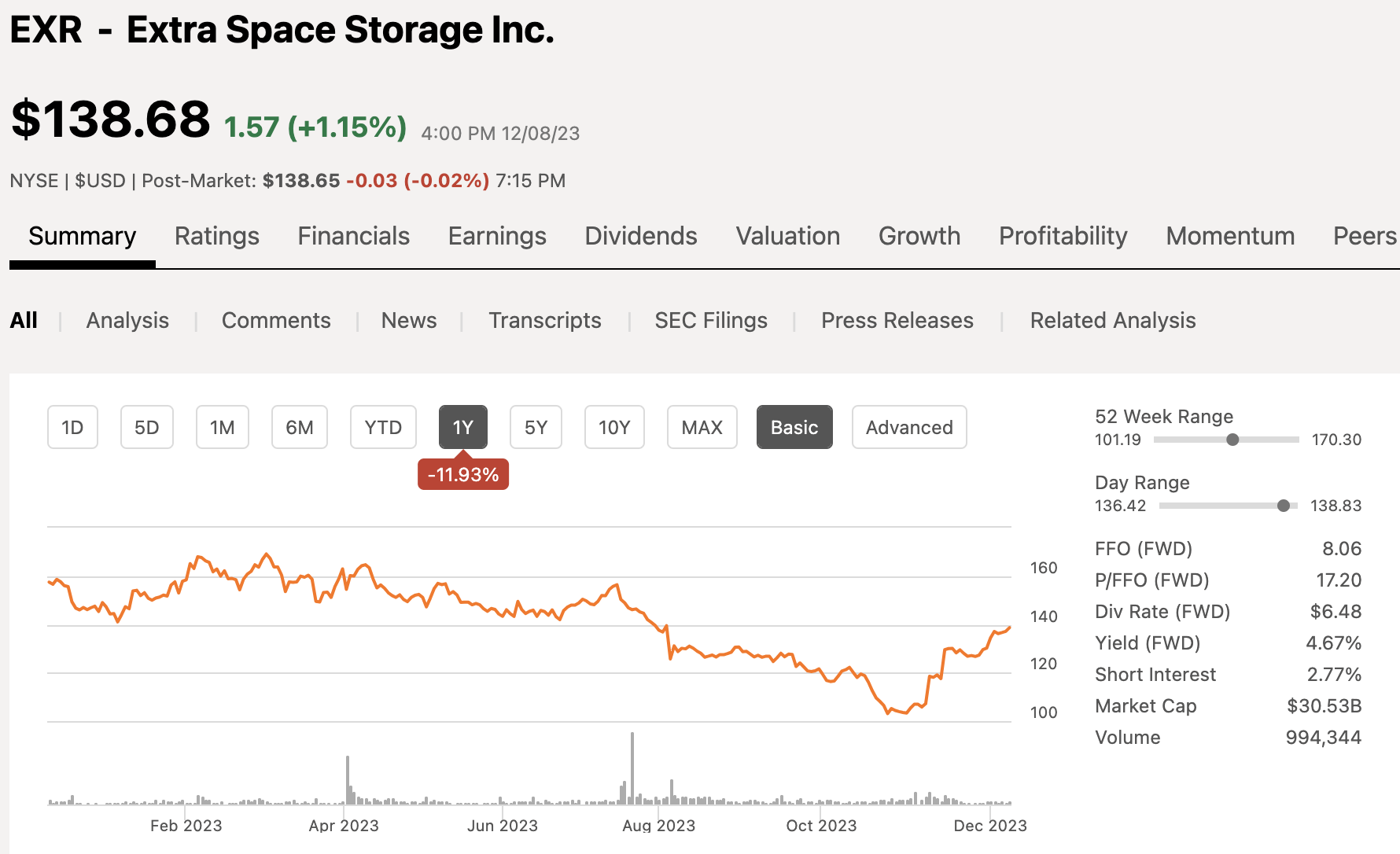

REIT #6 - Extra Space Storage Inc. ( EXR )

If there is one thing that is for sure, it is the fact that Americans are hoarders which plays right into the hands of self-storage companies like Extra Space Storage. This is not changing today and it is not changing tomorrow.

Extra Space Storage is one of the largest self-storage REITs on the market today, trailing only Public Storage ( PSA ). EXR shares currently have a market cap of about $30 billion compared to Public Storage having a market cap of $48 billion. Over the past year, shares of EXR are down more than 12%.

{kind=link}

Extra Space has 3,651 properties within 42 states amounting to more than 2.5 million storage units. These storage units amass more than 279 million square feet of rentable space.

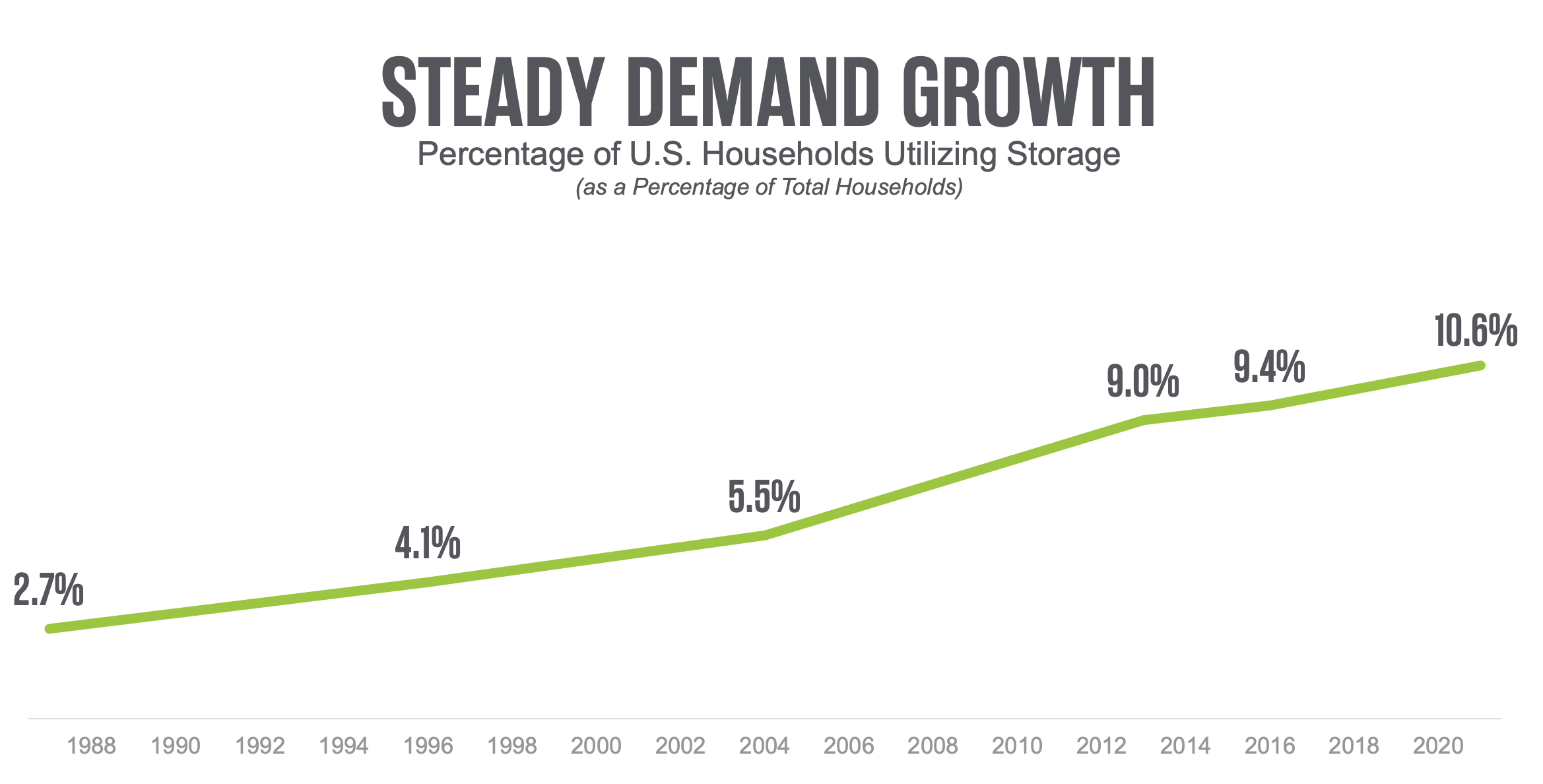

From the late 80s to today, the percentage of households utilizing storage has grown at a consistent clip. In the late 80s, less than 3% of US households utilized storage, but today that number is nearing 11% and growing.

{kind=link}

Storage has proven to be a recession-proof sector over the years, which is why I tend to have some exposure to either EXR, PSA, or even CubeSmart to some degree in my portfolio.

Dividend growth has been a priority for management over the years as the growth has outpaced its closest competitors by a wide margin over the past decade.

{kind=link}

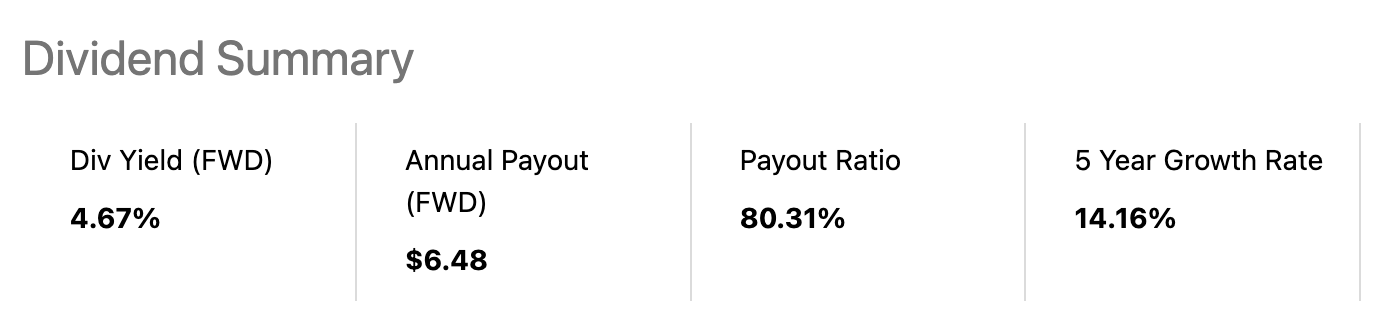

The dividend currently yields 4.7% with the dividend doubling over the course of the past five years.

{kind=link}

Analysts are looking for EXR to generate AFFO of $7.96 per share next year, which equates to a forward AFFO multiple of 17.4, which is well below their five-year average of 22.2x.

{kind=link}

Analysts rate the REIT a MODERATE BUY with an average 12-month price target of $149, implying more 8% upside from current levels.

{kind=link}

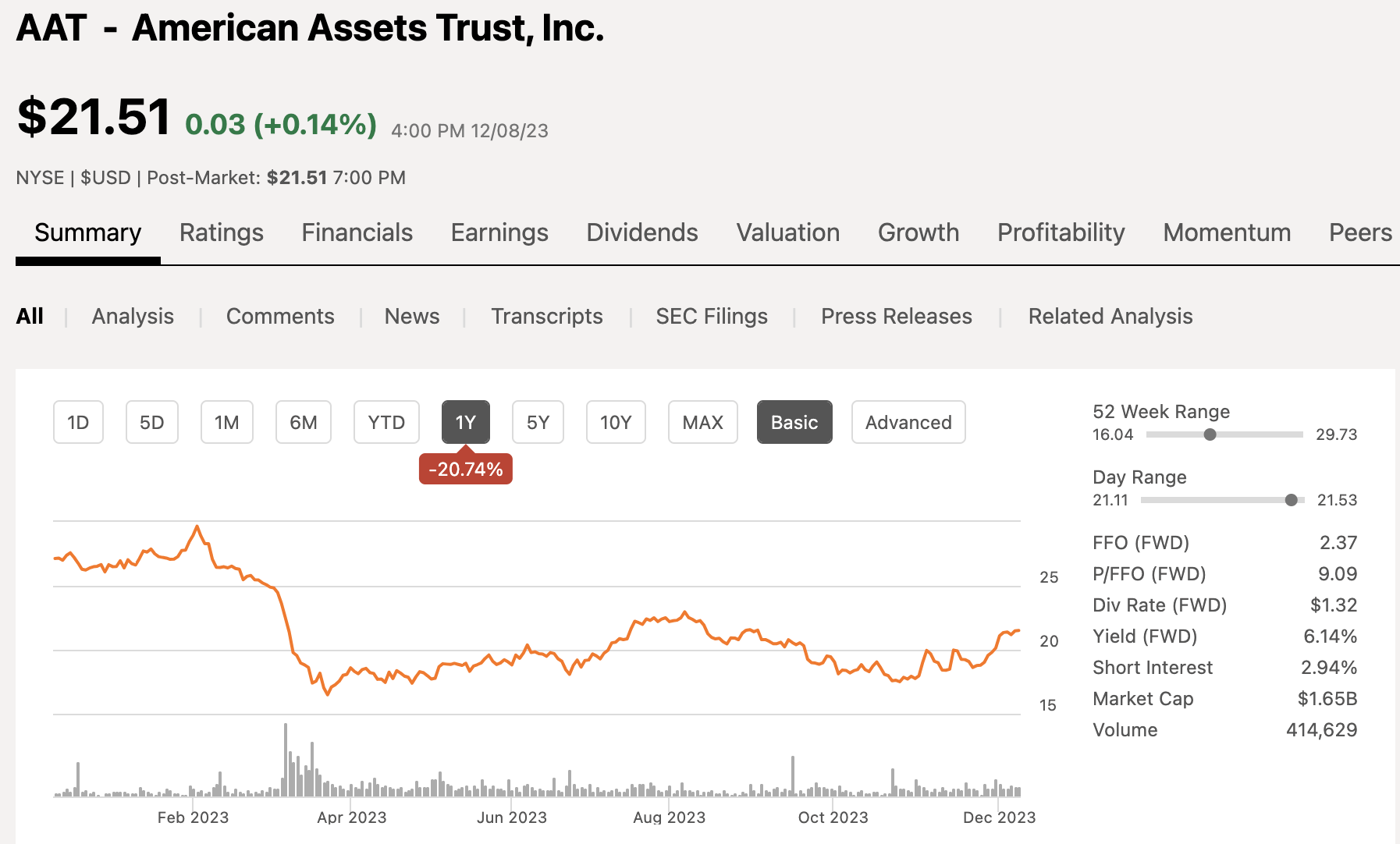

REIT #7 - American Assets Trust, Inc. ( AAT )

American Assets is a REIT I have not discussed before, but one that I have followed for some time. The REIT went public back at the start of 2011, as they were actually the first IPO of the year.

American Assets is a diversified portfolio with exposure to retail and apartments, and then office, which has been the concern of investors.

The REIT currently has a market cap of less than $2 billion. Over the past 12 months, shares of AAT have fallen 20%, significantly underperforming the market and the REIT sector as a whole.

{kind=link}

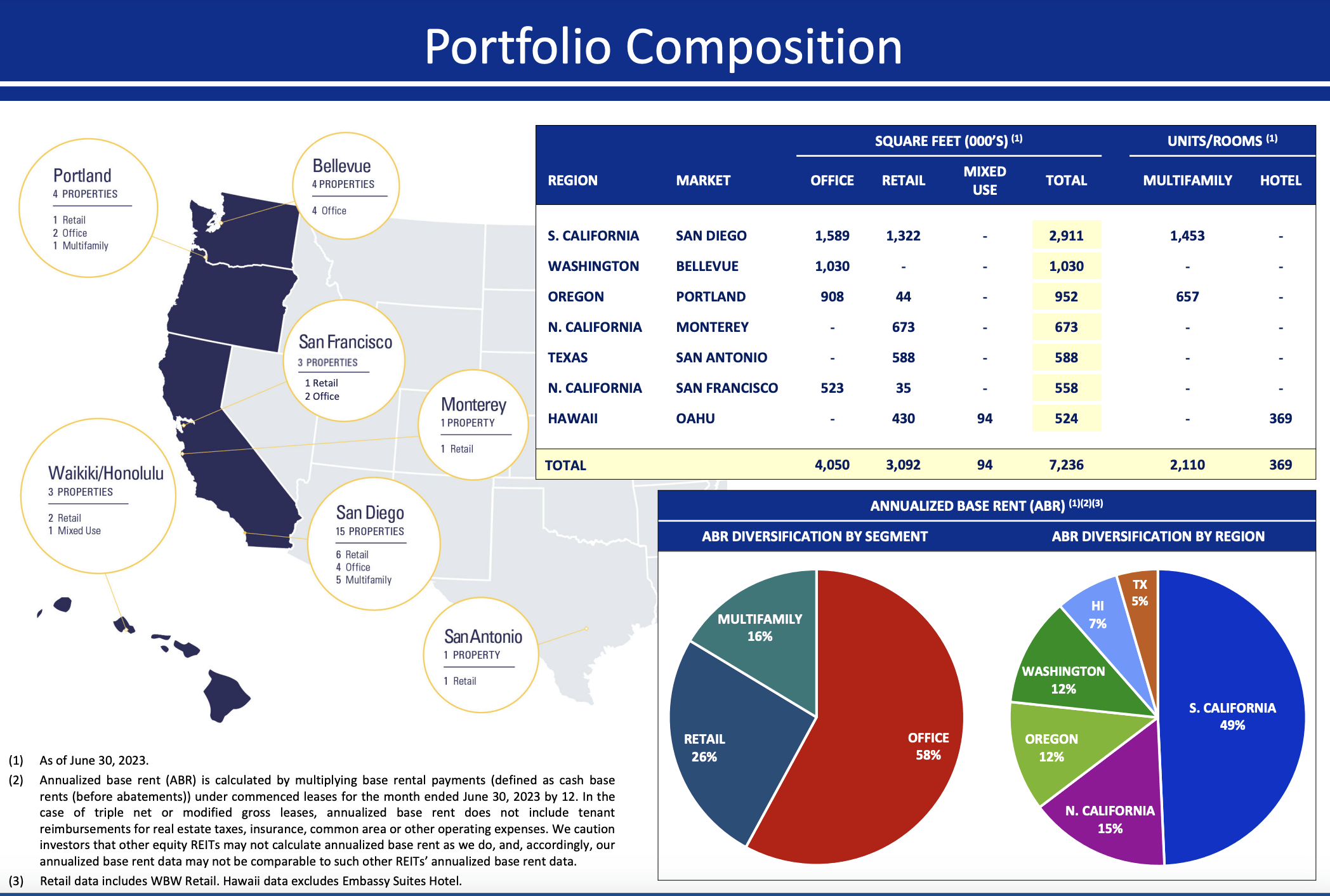

As you can see from this portfolio composition, the REIT has a strong presence along the west coast from Washington all the way down to California, and a few properties in Hawaii. California is the biggest region, particularly Southern California which is where the company is headquartered in San Diego, California.

{kind=link}

The property breakdown shows that the largest property type for the REIT is within the office sector, which has been through a lot of changes in the past three years post-pandemic. A lot of companies moved to a more flexible work arrangement, but that does not entirely call for the end of offices. In fact, the number of companies bringing employees back to work is actually on the rise.

This leads me to compare office REITs to the likes of mall REITs. What I have long said when it comes to mall REITs is the fact that the highest quality will prove to be the only ones worth owning. There is still a need for malls, but the best operators like Simon Property Group, Inc. ( SPG ) are the ones that will succeed and I see office being no different.

As such, if you are value-hunting and looking for a quality REIT with some exposure to the office sector, AAT may be worth a second look.

AAT also pays a high dividend that yields more than 6% with a five-year dividend growth rate of about 4%.

{kind=link}

Now let's take a look at valuation to see if this REIT is worthy of a buy. Not as many analysts cover the REIT compared to the others we have looked at today, so we are going to have to rely more on valuation, which should always be the main priority anyway.

The REIT is expected to generate AFFO of $1.73 per share next year which equates to an AFFO multiple of just 12.4x. Over the past few years, the REIT has traded closer to 22x or higher providing a lot of value at current levels.

{kind=link}

To put this into perspective, SL Green Realty Corp. ( SLG ) which is more of a pure-play office REIT, trades at an AFFO multiple of more than 13x, which means AAT, which has only about half its ABR comes from office is trading below that, which could be an angle to look at the value play that AAT is offering.

REIT #8 - Crown Castle Inc. ( CCI )

Crown Castle is another REIT that has been under heavy pressure in 2023 not only due to higher interest rates, but also due to the threat of satellite, increased competition, as well as a plateau in the number of towers in the industry.

I believe there is still a growth story to be had in the space, which is why I am including CCI on today's list.

Crown Castle currently has a market cap of $50 billion and over the past 12 months, shares of CCI are down more than 15%, which is with a 20% move higher in the stock over the past month.

{kind=link}

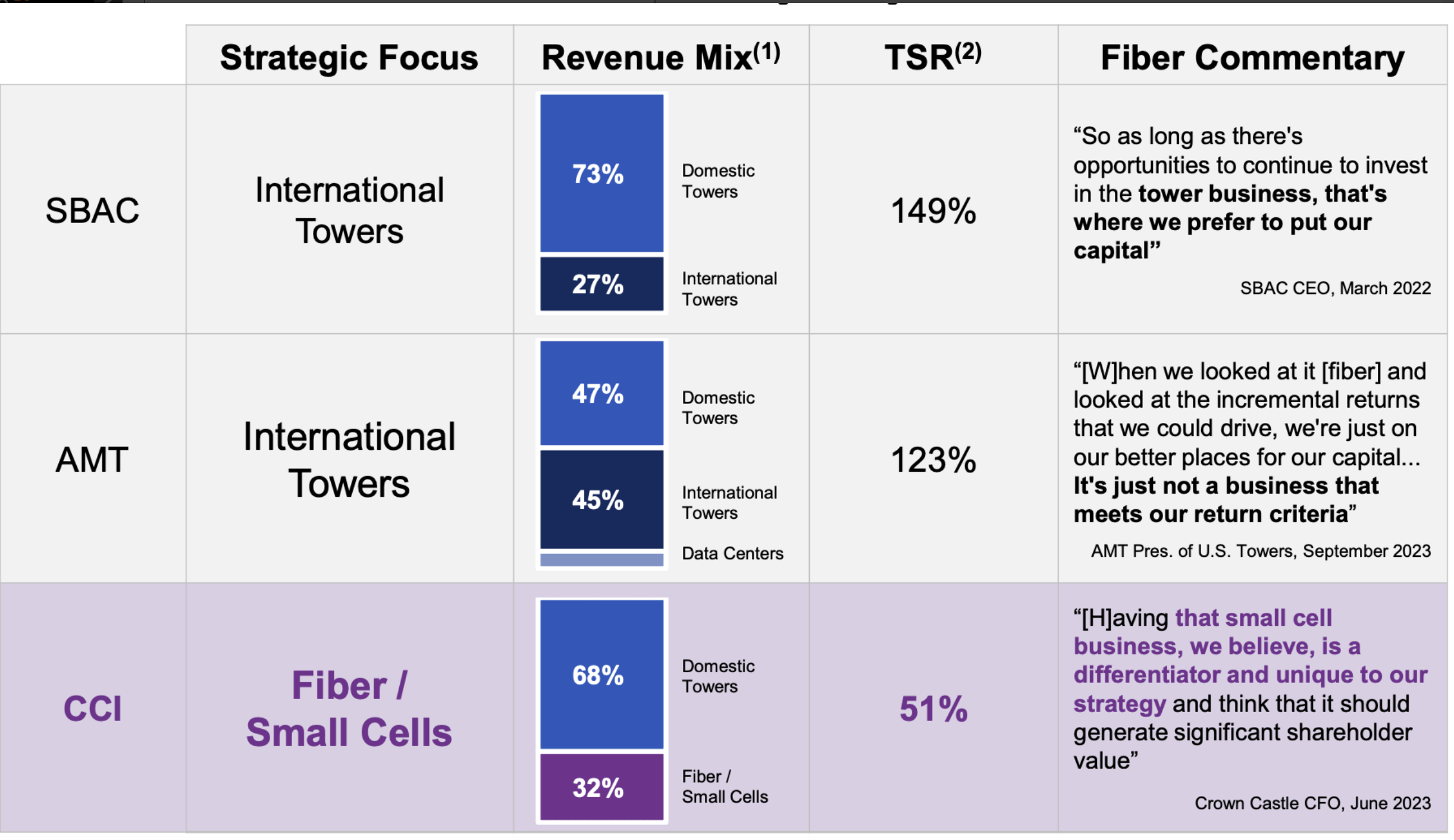

CCI has been in the news of late as they had an activist enter the fray, which ultimately ended up seeing the CEO ousted. Elliott Management acquired a 10% stake in CCI and has pushed for some major changes. These types of takeovers can sometimes be a wake-up call for a company and that is my hope here.

Elliott Management put out a 50-page report detailing all the changes and why changes are needed. In that report they stated how management has failed to create meaningful shareholder returns and lagged their competition. In this chart they detailed the lack of shareholder return compared to its competition over the years.

{kind=link}

The company has a portfolio of cell towers as well as small cell and fiber communication operations as well, which have come under question. There is definitely change needed, but there is also undeniable demand for the products they own and lease out to major carriers like Verizon Communications Inc. ( VZ ), AT&T Inc. ( T ), and T-Mobile US, Inc. ( TMUS ) to name a few.

Crown Castle was also in the news recently when their CEO Jay Brown will retire at the start of the new year and be replaced by Anthony Melone on an interim basis.

Given the downturn in the stock, shares now yield a dividend of 5.4% with a five-year dividend growth rate above 8%. Management has increased the dividend for 8 consecutive years now, but that will be under the microscope over the next 12 months.

{kind=link}

Analysts are looking for CCI to generate AFFO of $6.93 per share in 2024 which equates to an AFFO multiple of 16.7x, well below their five-year average of 22.8x.

{kind=link}

REIT #9 - Mid-America Apartment Communities, Inc. ( MAA )

Now we move to a different sector within REITs, and we will be looking at an apartment REIT that looks intriguing for 2024.

Mid-America Apartment Communities is one of the largest apartment REITs on the market today with a market cap of $15 billion. Over the last 12 months, shares are down more than 20%, making this yet another REIT that has been hammered due to high interest rates.

{kind=link}

Mid-America Apartment Communities has a portfolio of more than 100 thousand apartment units. High interest rates have certainly weighed on the REIT but the other thing that has weighed has been slowing rental growth.

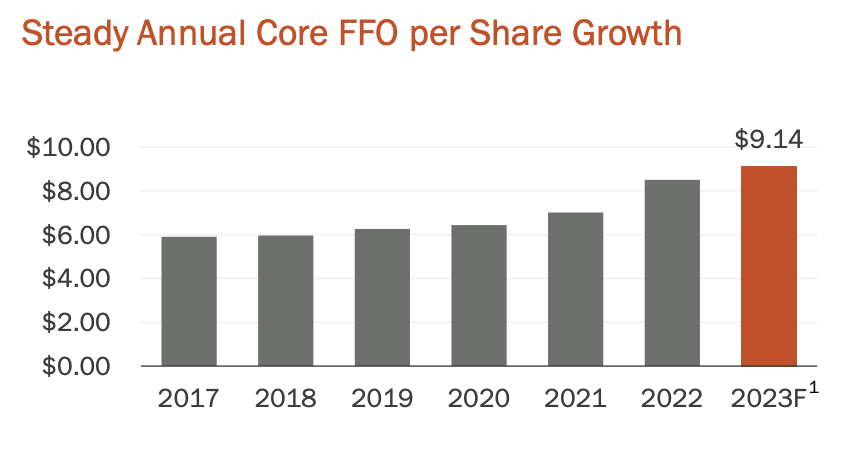

However, even with all of this, management has generated higher Core FFO every year dating back to 2017.

{kind=link}

With a lot of the rental news priced in, evidenced by the strong share price declines, given that I am a value investor, MAA is looking like a great long-term entry point.

Before we look at valuation, let's first look at the dividend. Shares of MAA currently yield a dividend of 4.4% and that dividend has been growing for 13 consecutive years and counting with a five-year dividend growth rate of 8.7%.

{kind=link}

Analysts are looking for the company to generate AFFO of $8.30 per share in 2024, which equates to an AFFO multiple of 15.3x, which is below their historical average of 20.9x.

{kind=link}

Analysts currently have an average 12-month price target of $140.67 per share which equates to more than 10% upside from current levels.

{kind=link}

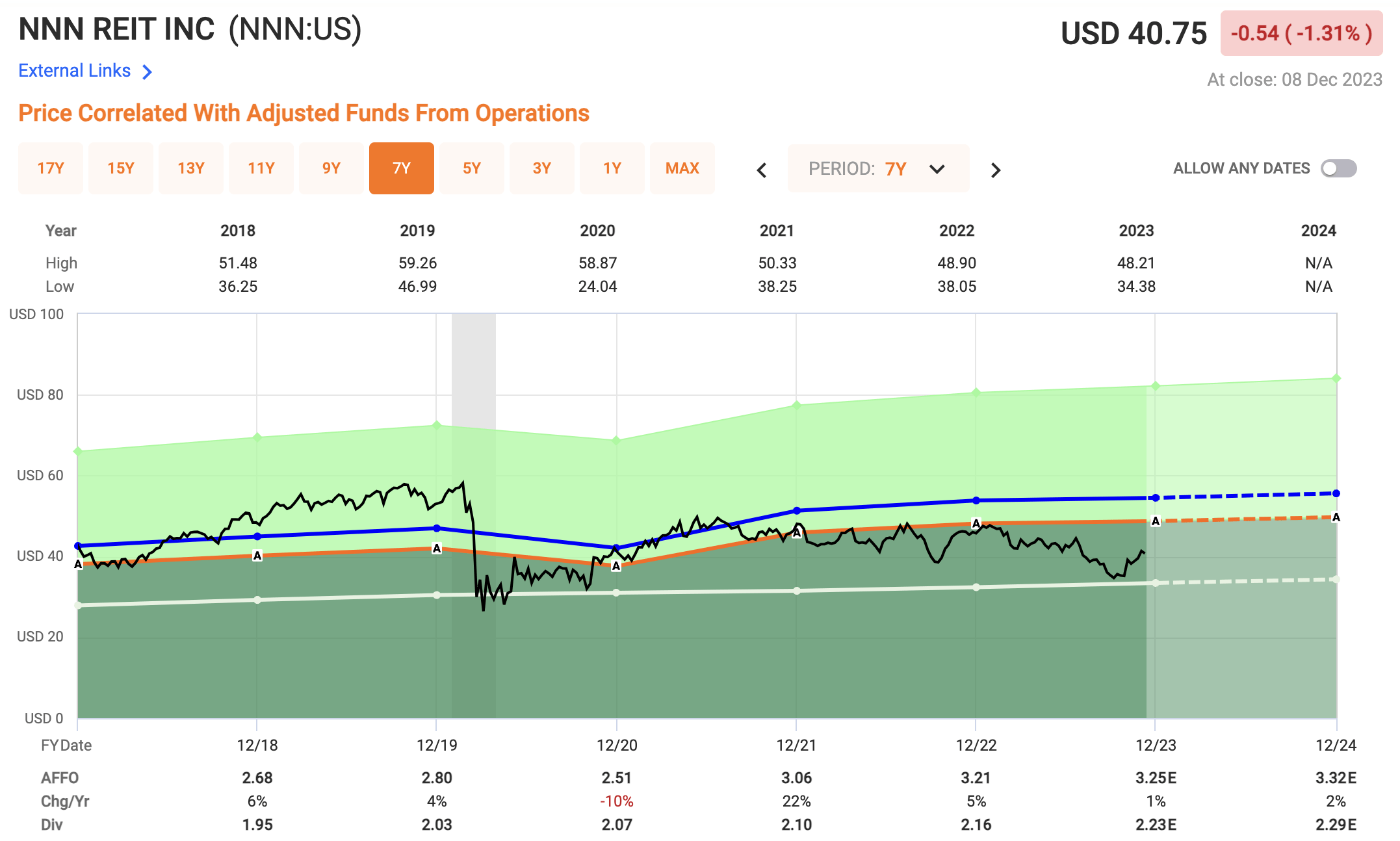

REIT#10 - NNN REIT, Inc. ( NNN )

This brings us to our final REIT on our list today, although there are many others I went back and forth about putting on here. This REIT has been a solid REIT for a number of years, and has been in the shadow of Realty Income for a number of years.

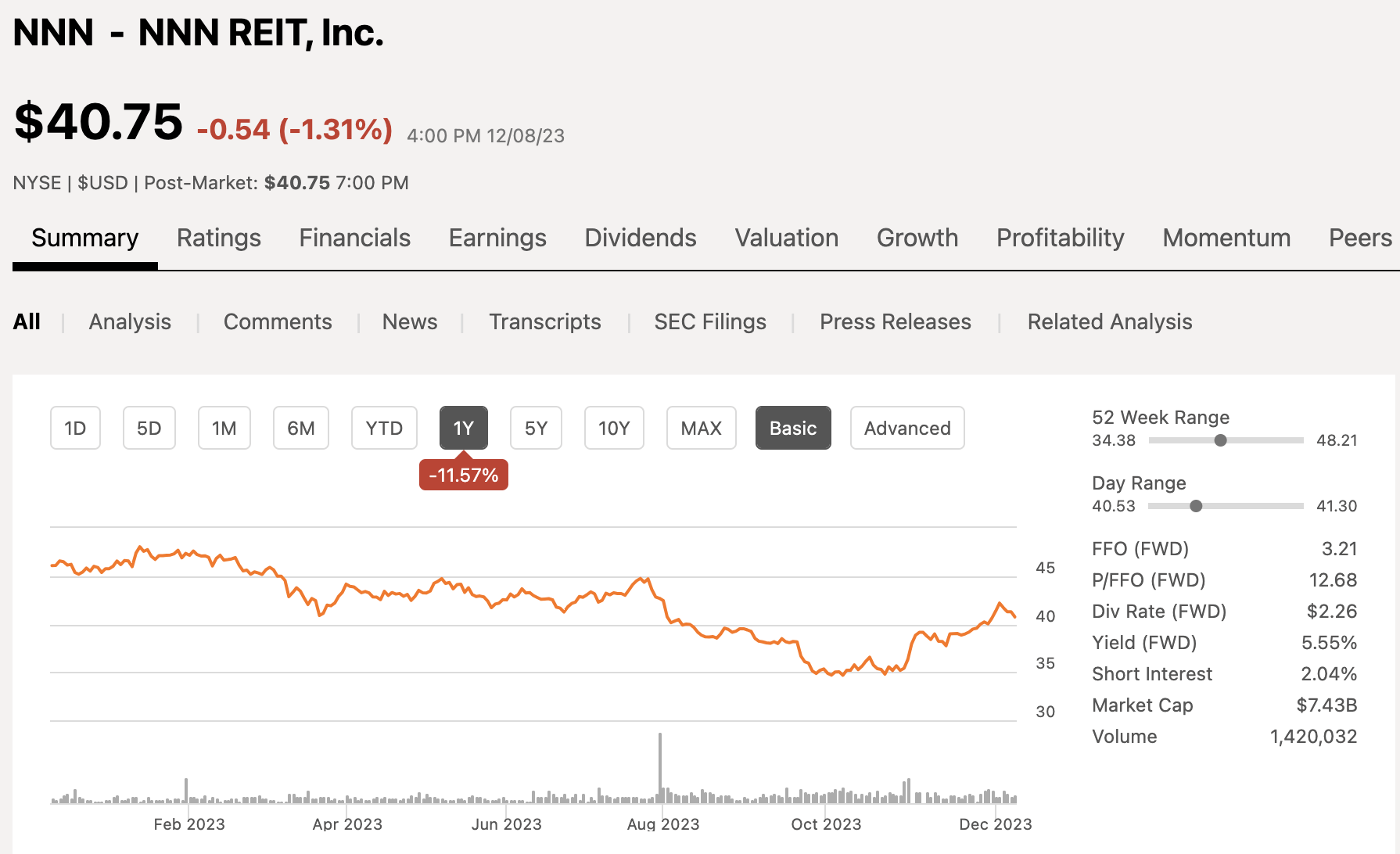

National Retail Properties now goes by the name NNN REIT is another net lease retail REIT. The company currently has a market cap of $7 billion. Over the past 12 months, shares of NNN are down more than 10%.

{kind=link}

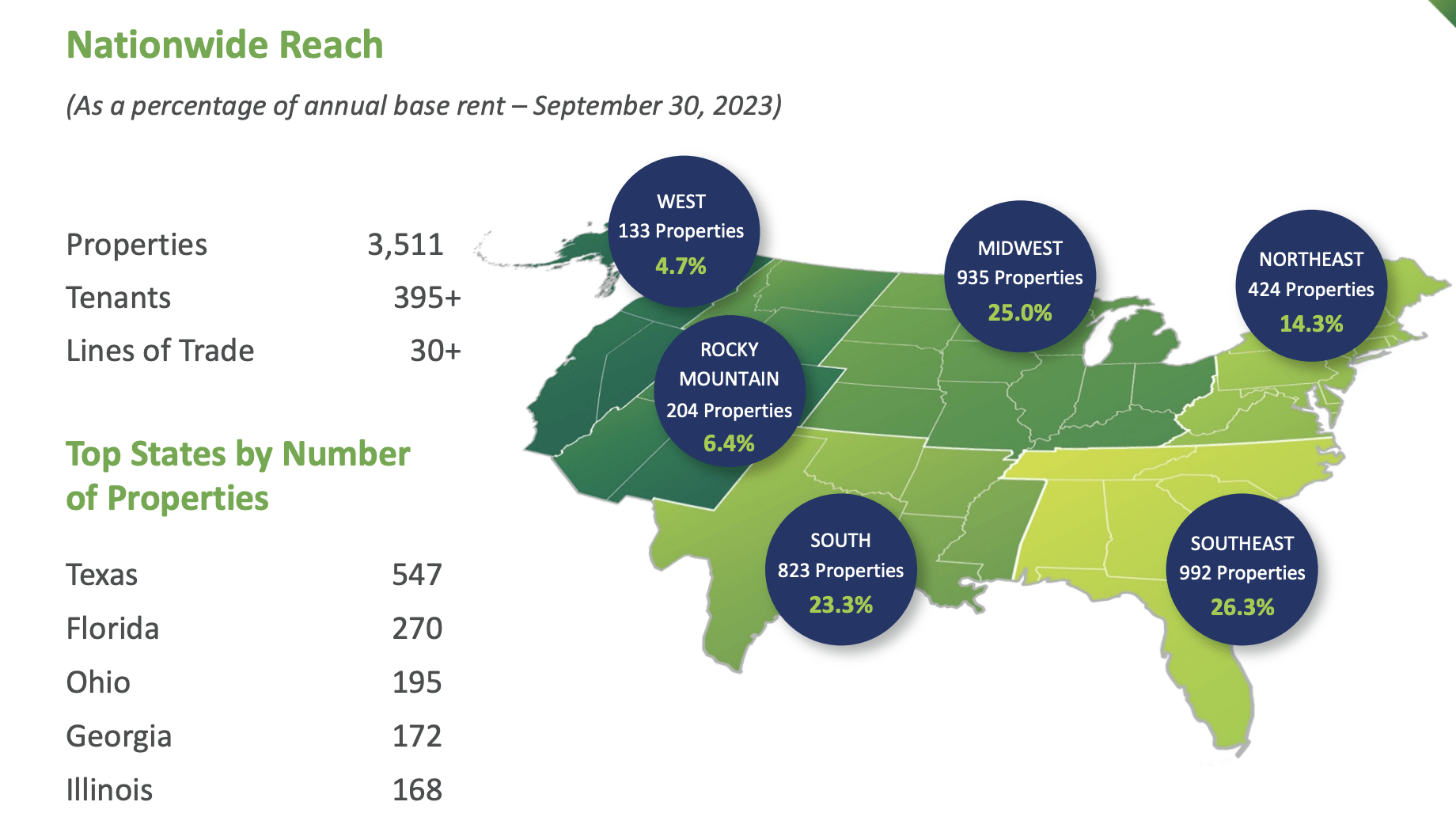

The REIT has more than 3,500 properties with Texas and Florida being the top 2 states. In total, NNN REIT leases to more than 395 tenants across 30+ lines of trade.

{kind=link}

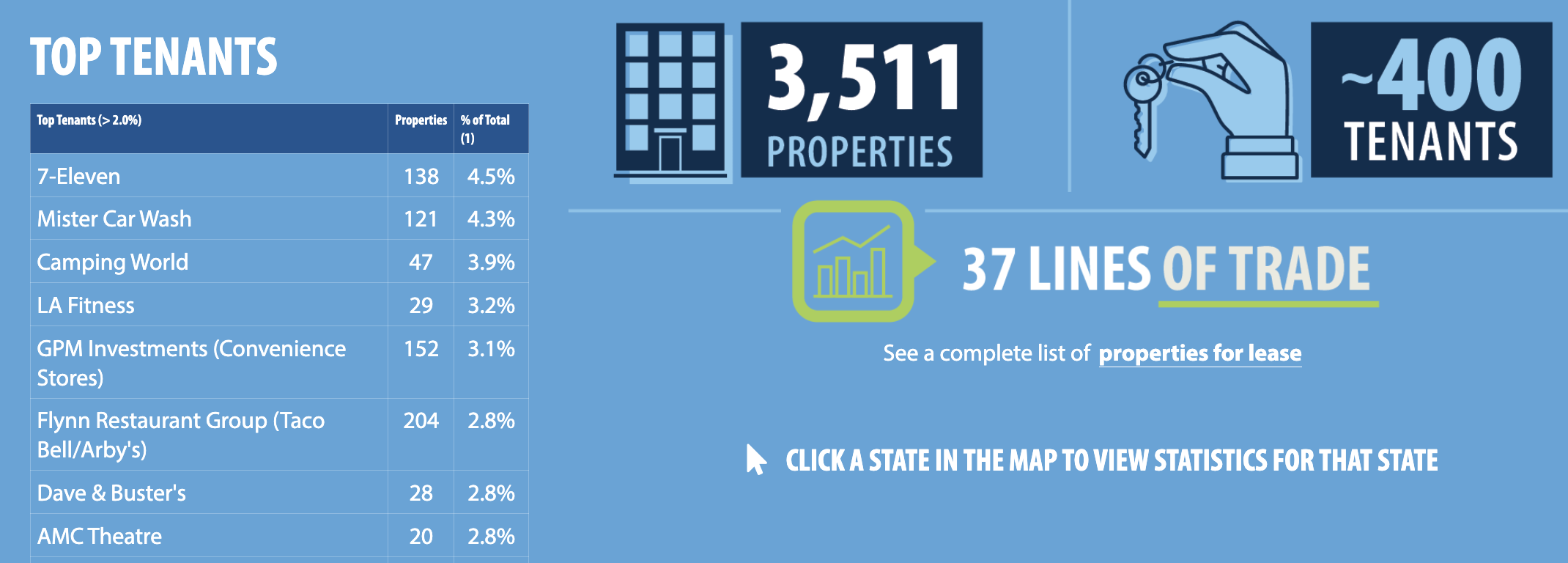

Here is a look at the REIT's top tenants:

{kind=link}

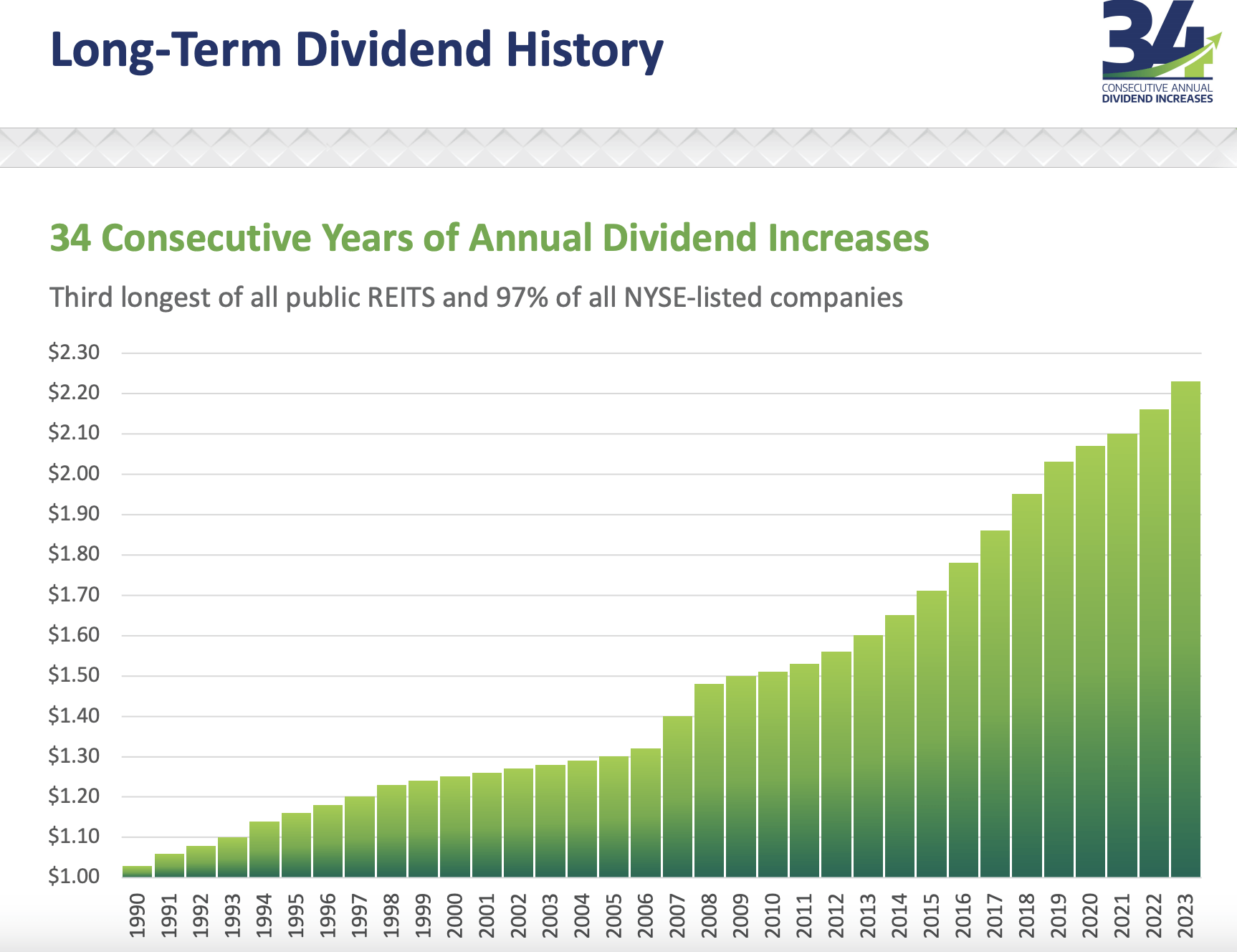

The REIT has a very long history of paying and growing their dividend with 34 years of annual dividend hikes.

{kind=link}

The REIT currently pays an annual dividend of $2.26 per share which equates to a dividend yield of 5.55%. Like Realty Income, you get consistent dividend growth, but not much in terms of growth percentage.

{kind=link}

In terms of valuation, analysts are looking for the REIT to generate AFFO of $3.32 per share next year equating to an AFFO multiple of 12.2x compared to their historical average of 16.8x.

{kind=link}

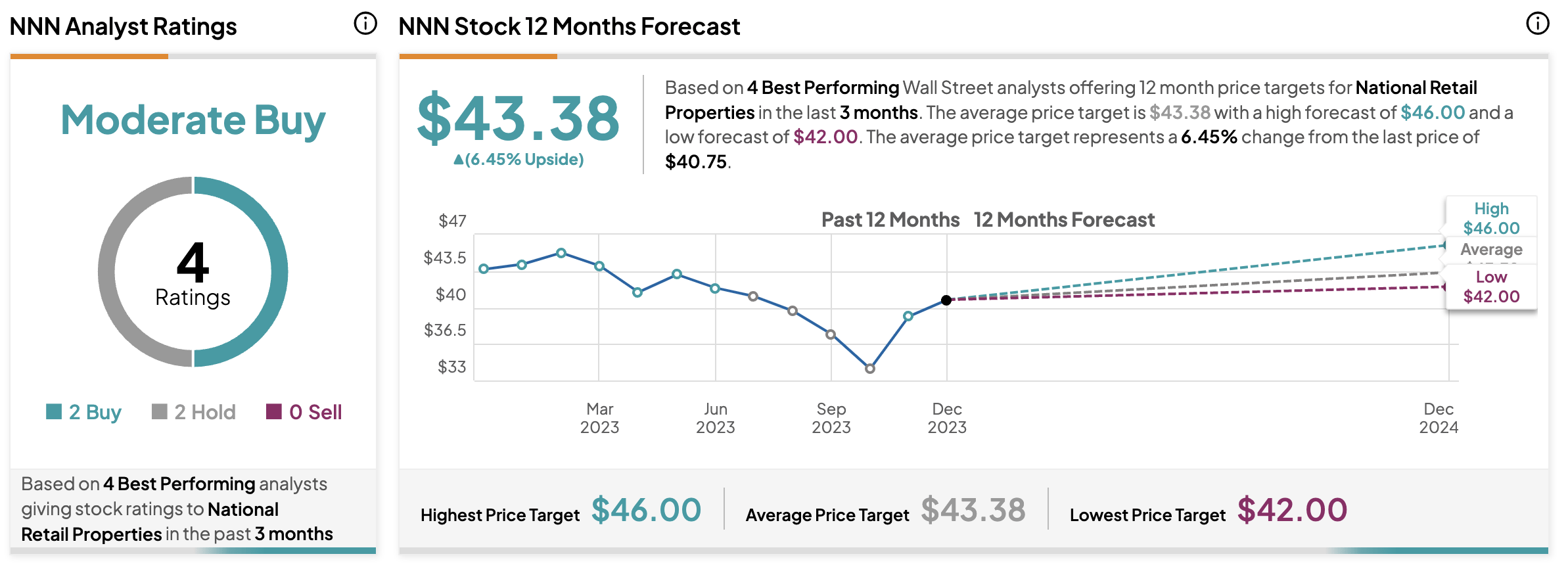

Analysts rate the stock a moderate buy with an average 12-month price target of $43, implying more than 6% upside to go along with that 5.5% dividend yield.

{kind=link}

Investor Takeaway

REITs have been hammered for much of the past 18 months as the Federal Reserve has hiked interest rates at the fastest pace in recent history. However, with the hiking cycle all but over, and rate cuts on the horizon, this could provide a boost to this beaten-down sector.

As such, if you are a value investor looking for great entry points, then definitely look at the REIT sector along with these 10 companies that were discussed today, which all seem to be trading at great valuations.

In the comment section below, let me know which of these stocks you like best for 2024 & beyond.

Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

For further details see:

10 Of The Best REITs To Buy For 2024