PRME - 10 Potential 10x Return Stocks For The Next 10 Years

Summary

- While others flock to safety, should you do the opposite?

- Some of the best times to invest in highly speculative names are when no one wants them, as long as the reasons are macro and not company or industry specific.

- Now that the tax loss bloodbath is over, here are some potential treasures from the rubble. Very high risk, but also the potential for high returns over the next decade.

Many, if not most, of the companies I am about to discuss will likely be bankrupt within 10 years. If not technically, it will be the equivalent thereof for you as a shareholder; you will be diluted into oblivion with a 95-99% loss.

So why would you want to buy any of them?

Because all it takes is 1 or 2 big winners to make up for all your losers, and then some.

Let's say you buy 10 names in equal weight. From them, you get a 3-bagger, a 5-bagger, and 10-bagger. The other 7 go to zero.

Your total return would still be 80%.

Is that exceptional? No. In fact, that will likely underperform the S&P 500. Considering the highly speculative nature of these names, 80% would be a poor risk-reward. However the point is to show you how all you need are a couple big winners to offset many losers, even if those losers are complete losses.

When it comes to ten-bagger stocks, you may assume they are likely to be in tech, biotech, junior miners/oils, and other high risk, high reward industries. Yes, there are plenty of those, but many if not most come from relatively boring and mundane industries you wouldn't expect. I won't get into all the research here but if you haven't read it, the book 100 Baggers by Christopher Mayer has excellent qualitative and quantitative data to back this up.

Though when you and I seek out potential 10-baggers, naturally we will often gravitate towards the higher risk companies. Part of this is not our fault, as it can be hard to predict which boring companies will 10x in 10 years. Especially if they haven't been public for decades, so you can't track their long term ROE, ROA, and other metrics which can give a hint as to future growth.

For that reason, don't be surprised that the following companies I'm about to highlight are highly speculative. It's not that I believe spec stocks offer better long term rewards. Rather, it's just much harder to differentiate which boring companies today have the potential to 10x in 10 years. Coming up with safe candidates that I expect to 3-5x is relatively easy. Doing the same for 10x potential is quite difficult (but if you have safer ideas to put forth, please share in comments).

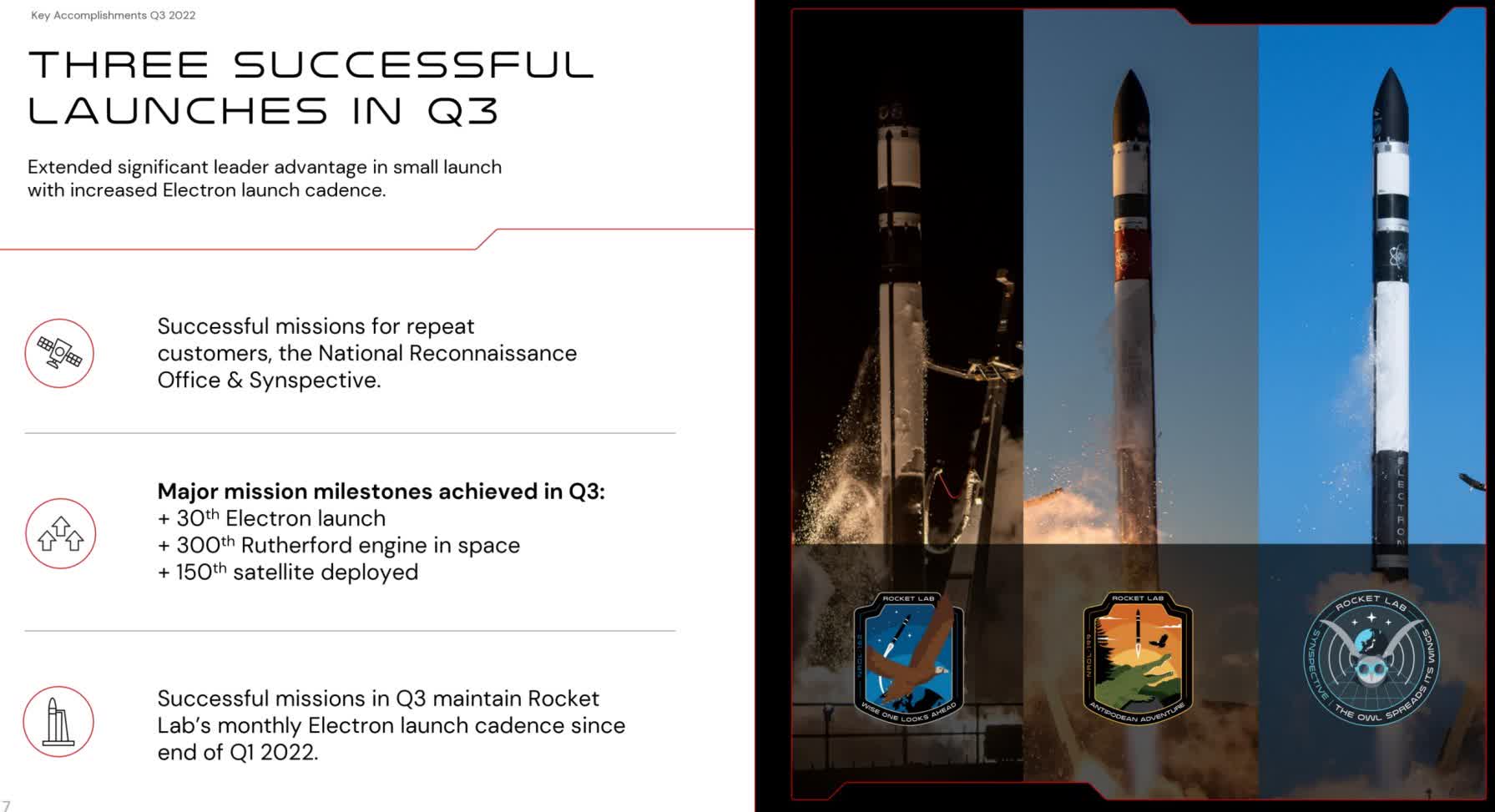

1. Rocket Lab

Of course I'm going to start the list with the sexiest. This is not accidental. Going back to the research of 100-baggers, much of their gains come from multiple expansion rather than revenue or earnings growth. Tesla ( TSLA ) is a recent example of this. Amazing company but before its recent selloff, most of the gains during 2019-2022 had come from multiple expansion. In other words, hype.

Rocket Lab ( RKLB ) is another company ripe for hype. Since I've already written an in-depth article on here, go check that out to learn more. It's fittingly titled Rocket Lab Vs. SpaceX: Buy 2nd Place For 98% Less .

Founder CEO Peter Beck has said he wishes he named the company Space Lab, because they are far more than just the 2nd best private launch provider. They are an end-to-end space company with their hand in many facets of satellite manufacturing, management, and more.

Rocket Lab Q3 2022 investor presentation

{kind=link}

Will Rocket Lab supplant SpaceX's ( SPACE ) lead in the next decade? Nope. They don't need to though to become a 10-bagger. Given the valuation discrepancy, they just need to attain a valuation that's 1/5th of what SpaceX is right now.

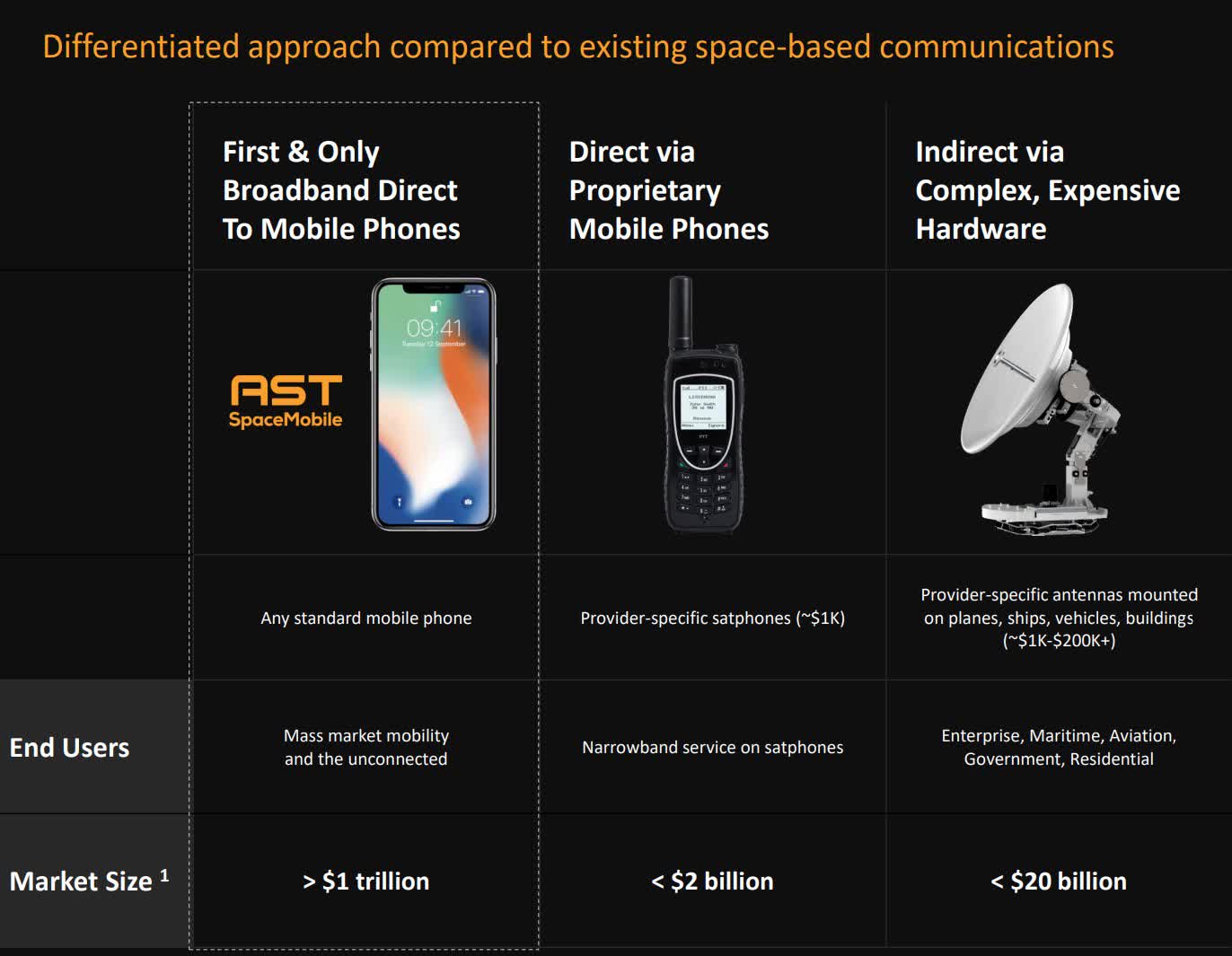

2. AST SpaceMobile

What is probably the 2nd sexiest company on my list. When I published my first piece on AST SpaceMobile ( ASTS ) over a year and a half ago, on the same day they de-SPAC'd, some people basically laughed at me agreeing with what seems like a pie-in-the-sky business; the ability to connect your ordinary cell phone to a satellite over 720 km/447 miles away. Without any special hardware or app. I'm talking your current phone, not a future model.

The reason I could be so confident in the feasibility is because it's based on simple physics. The execution is the risk, not the physics. Here's a quote from my earlier piece:

Using just a 3.7-meter (12 ft) antenna, right now Voyager 1 - which is the deep space probe launched over 43 years ago - is communicating with us from over 14,000,000,000 miles away. It's in interstellar space, outside our solar system.

Not to get too technical here, but in short, the further away an object is, the larger the antenna you need on the other end. In other words, you can compensate for great distance with great size, if you know exactly where to look.

SpaceMobile isn't changing the size of the antenna in your phone. They are changing the size on the other end, in space.

Now perhaps those same people aren't laughing, as Elon Musk and T-Mobile ( TMUS ) have since announced a similar plan for cellular connectivity in dead zones via satellites.

AST SpaceMobile investor presentation, Aug 2022

{kind=link}

Perhaps T-Mobile is doing that because some of their competitors already teamed up with AST SpaceMobile. Partners include AT&T ( T ), American Tower ( AMT ), and Vodafone ( VOD ).

3. Planet Labs

One more space name, because you know it's an industry ripe for high multiples.

Given the recent $6.4B cash takeout offer (that's a 129% premium) for Maxar Technologies ( MAXR ), the potential for Planet Labs looks even brighter.

As with Maxar, Planet Labs ( PL ) is an earth imaging company. Unlike Maxar, they don't have dinosaur satellites. They have around 200 satellites, which is already the biggest fleet in the industry. What's not big is the cost or size per satellite, yet they are higher performance than Maxar's.

{kind=link}

I generally hate talking about TAMs because that's a term typically used to support a bubblicious company or sector. That said, I'm including this graphic just to show you of the many applications for earth observation data collection.

With a market cap of $1.2B and an EV slightly below $1B, doing a 10x in 10 years won't be easy. They're not yet profitable. Though I remind you of the $6.4B Maxar buyout and when you layer on a decade of inflation, what would that price tag equal in 2033 dollars?

4. JFrog

JFrog ( FROG ) is down over 70% from the highs it reached shortly after its IPO in late 2020. They are a DevOps platform for what's known as "liquid software." They coined that term. Their system allows developers to automatically and continuously update software they build. While many count this company as DevOps SaaS, I count it as IT security first and foremost.

So many security exploits are not the result of stolen credentials but rather, exploits in software which hackers use as a backdoor to sneak in. When an exploit is found, it must be patched immediately.

Although now retired, I dealt with this for over a decade with my credit card business and other online ventures. JFrog is badly needed for security and that is why they're growing like a weed, contrary to what the share price would suggest:

It reminds me a lot of MongoDB ( MDB ) several years ago. Just as investors didn't understand how big NoSQL databases were going to be (which are still in their infancy), I don't think they appreciate the potential for JFrog.

With a market cap of only around $2B and an EV even lower, it's not far-fetched to see this thing going up 10-fold in the next 10 years.

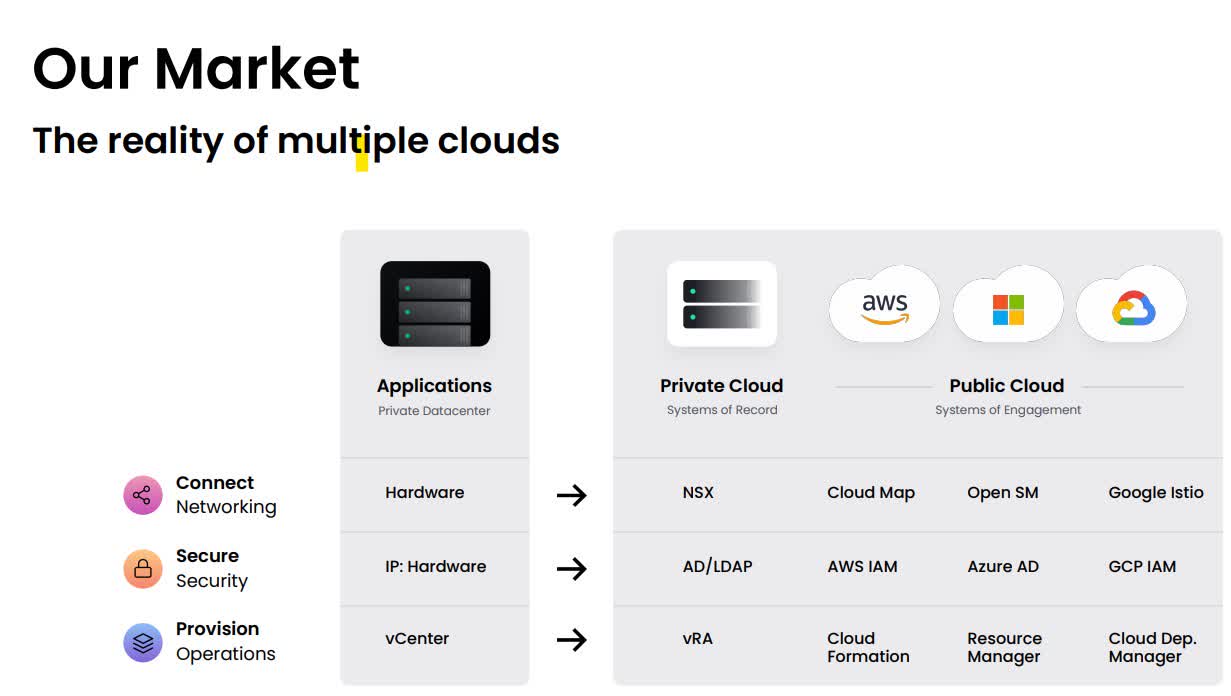

5. HashiCorp

With its $5B market cap, a P/S of around 10, and the fact they're losing money, it may seem like a stretch to suggest 1,000% gains ahead. Yet, I'd argue it's possible. Yes, I realize that would imply something like an $80B+ market cap in 2033, after you factor in future dilution.

HashiCorp ( HCP ) is a freemium software company which is by far the market leader in multi-cloud infrastructure automation software. What that means is they make it possible for businesses, particularly those at enterprise level, to seamlessly use multiple cloud vendors at the same time.

HashiCorp Q3 FY23 corporate overview HashiCorp Q3 FY23 corporate overview

{kind=link}

{kind=link}

The model of committing to a single provider - such as Amazon ( AMZN ) AWS, Microsoft ( MSFT ) Asure, or Google ( GOOG ) Cloud - is a model of the past. Today, businesses (and governments) don't want to be held hostage by a single company. They want the ability to pivot between providers in order to get better pricing and performance. HashiCorp makes that possible.

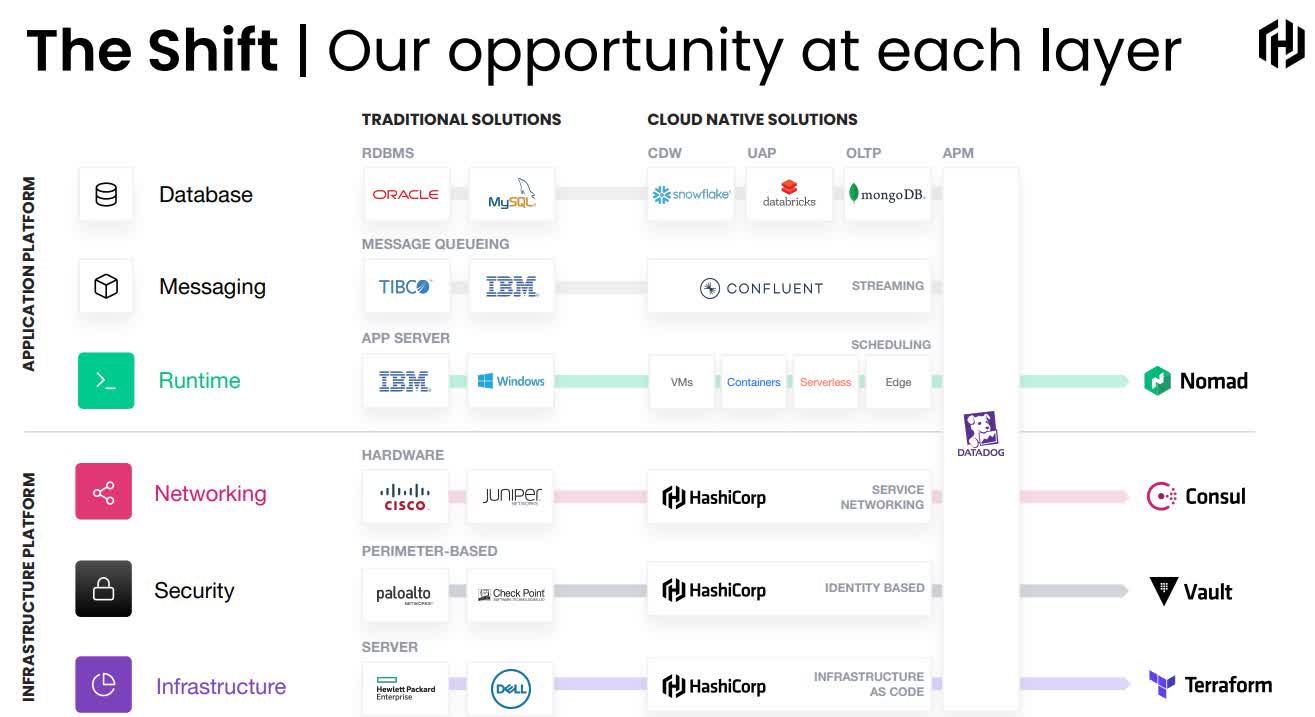

6. Sumo Logic

Given how important the theme of data collection and analytics will be over the next decade, I wanted to include a related name. However, finding a potential 10-bagger among them is hard.

Datadog ( DDOG ) is still way overhyped and priced as such. Snowflake ( SNOW ) is interesting in the low $100s (and I bought some there) but in no way am I suggesting a 10x gain in 10 years. Databricks is not public and already has a private valuation rivaling Snowflake. You may be surprised to hear I believe Elastic ( ESTC ) will produce greater gains than all of the aforementioned, but probably not a 10x in 10 years.

With a $1B market cap and an EV even lower, Sumo Logic ( SUMO ) is small. Growing to a $15B market cap (10x return after dilution) in 10 years is achievable, especially when you consider the size of their rivals. Splunk ( SPLK ), which is also used for big data log analysis, sports a $14B market cap.

{kind=link}

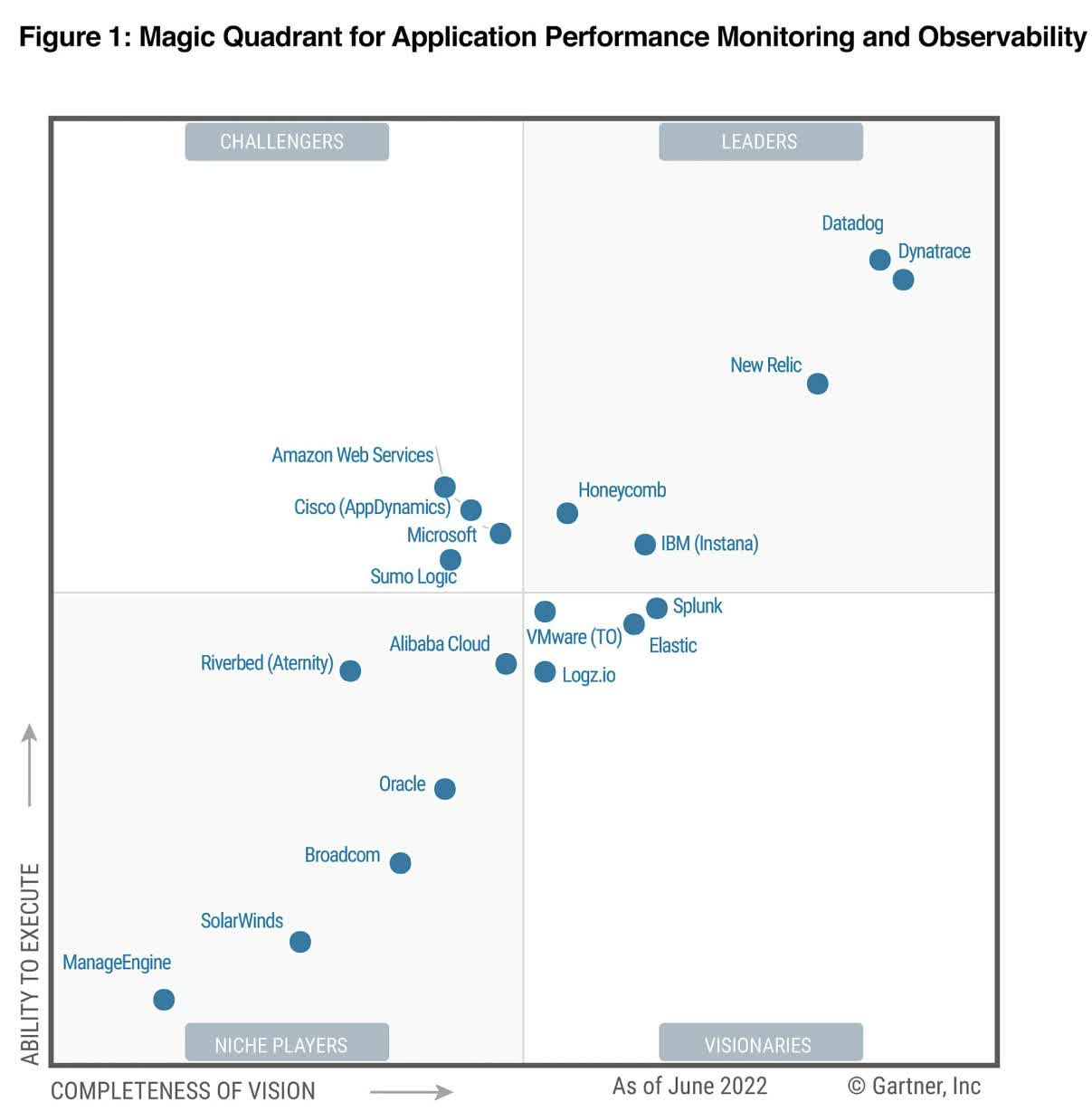

In the Gartner Magic Quadrant for APM and Observability, Sumo Logic was named a challenger last year. Unlike some of its older rivals, Sumo Logic is and has been cloud-native SaaS. Contrast to Splunk, who has been going through the messy transition.

Many large enterprises you know choose Sumo Logic over the competition, such as Fidelity, Ulta Beauty ( ULTA ), Mattel ( MAT ), Okta ( OKTA ), and AB InBev ( BUD ) to name a few. Even though their stock price would make you think otherwise, their growth has been strong:

7. UiPath

Yeah, this is a Cathie Wood Name, which is both a blessing and a curse. It may be a blessing if you're getting in now, because UiPath ( PATH ) has been in all 6 of her funds. Their sell-off throughout 2022, along with the final kick in the groin for tax loss harvesting, has meant intense selling pressure.

UiPath is a leader in Robotic Process Automation ((RPA)). They make software to automate the manual repetitive processes we all hate to do. Things like insurance claims, medical billing, and loan applications may come to mind, but the uses are far beyond that as seen in their case studies .

What I like in particular is this is a founder-led company who has big plans. Daniel Dines is a Romanian programmer who co-founded it with Marius Tîrc?. Today, Dines is co-CEO along with Rob Enslin. He was former president of Google ( GOOG ) Cloud. In other words, you have a visionary leader (Dines) kept in check by someone with business savvy (Enslin).

At only a $7B market cap, assuming it doesn't get bought out, reaching $100B in 2033 is certainly within the realm of possibility. That would be around a 10x return on the stock after customary dilution.

8. Beam Therapeutics

Early stage biotech and pharma are the ultimate crapshoots. In almost all other industries, you can successfully sell inferior or even useless products/services, so long as you can convince customers to buy them. In healthcare, not so. You need the blessing of the FDA to sell anything. Furthermore, that blessing is based on quantitative - not subjective - data.

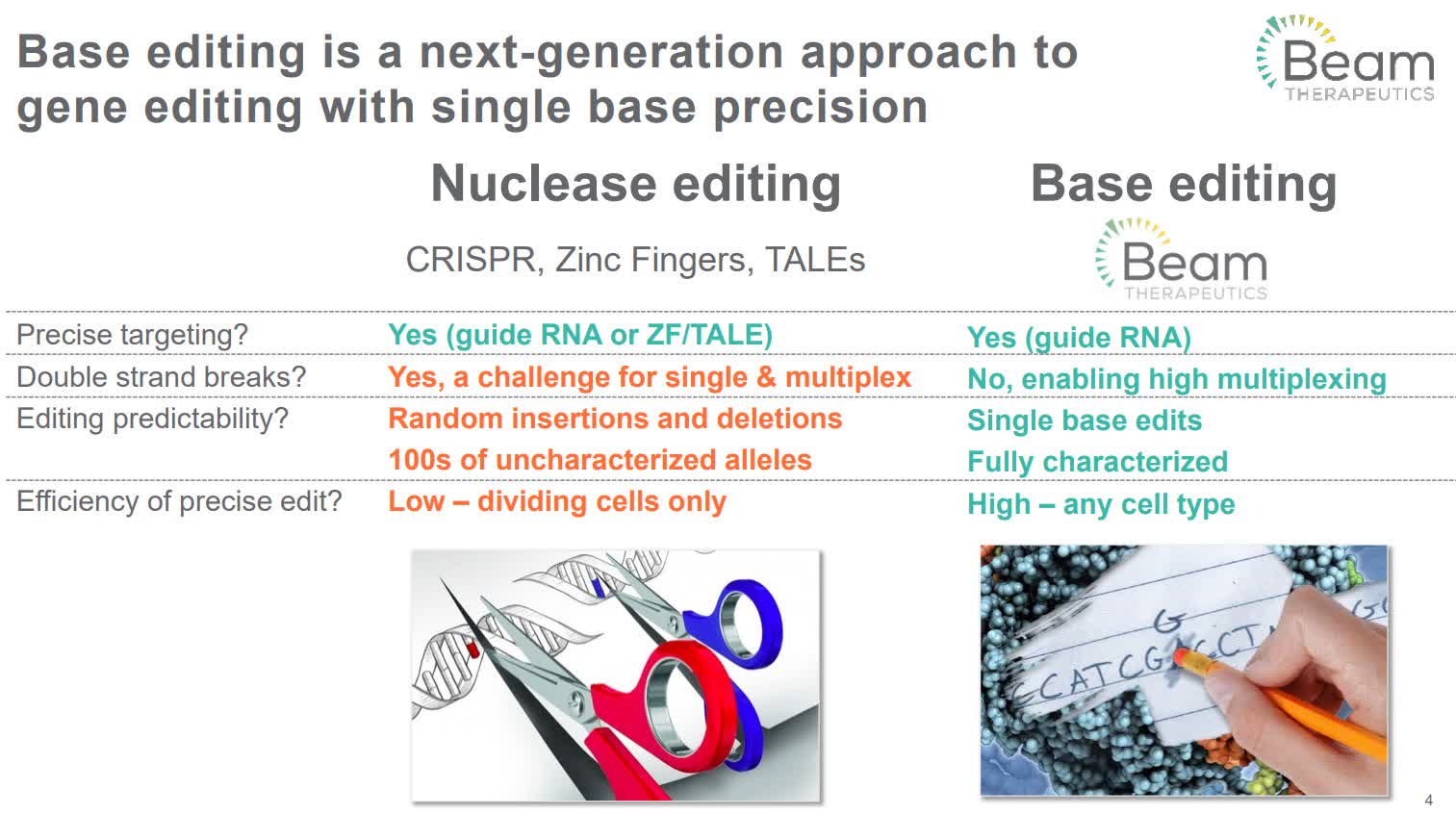

Then there's safety. Even if a therapy works, the benefits can't outweigh the risks. This is why I have always been rather pessimistic on the earliest CRISPR-Cas9 gene editing techniques. CRISPR Therapeutics ( CRSP ) and Intellia Therapeutics ( NTLA ) require double-strand breaks ((DSBs)), which are the most dangerous form of DNA damage. Mutations result, which drive cancer development.

That's not to say their therapies for sickle cell and beta-thalassemia, among others, won't be approved. But that's only because there aren't safer alternatives in trials… yet. There are newer editing techniques which incorporate the earlier steps in the CRISPR technique, but they don't involve DSBs. Because of that, increased risk of cancers should not result.

Since this is a list of 10 stocks, I'm not going to go into detail on base editing, prime editing, and the newest paste editing, all of which don't involve DSBs. To summarize though, I will say this; among the public companies, Beam Therapeutics ( BEAM ), which does base editing, is the most interesting when you factor in IP ownership/licensing, stage of company, and current valuation.

Beam Therapeutics corporate presentation, Nov 2022

{kind=link}

Base editing can correct misspellings in the four most common bases in DNA; A, C, G, and T. Only about 1/3 of the 75,000 known "misspellings" causing genetic disease could in theory be fixed with base editing. So it's safer, but limited in scope of what it can fix.

9. Prime Medicine

Prime editing does a "search and replace" of larger sequences.

...add in our prime editor, and between the two [base and prime editors] they can finally liberate us from being beholden to the vast majority of misspellings in our DNA.

That's a quote from David Liu, scientific co-founder of Editas ( EDIT ), Beam, and Prime Medicine ( PRME ), along with several other companies.

Prime Medicine IPO'd during a wonderfully bullish time; October 2022. Obvious sarcasm and it's also obvious they needed money, because you don't IPO at time like that unless you have to. With a market cap north of $1.5B and earlier stage than any of the aforementioned in this space, you can count on plenty of secondaries in the future to fund them.

I think it's too expensive to buy here in any significant amount. Odds are high of better entries in the future, perhaps even multiple years out, due to constant dilution and market gyrations. It could play out similar to how the original 3 public CRISPR names have, where you get chances to buy them for equal or better prices long after their IPOs:

Just as those 3 are being disrupted, keep in mind the same can happen to prime editing. Last year, MIT researchers announced PASTE (programmable addition via site-specific targeting elements). As with Prime, PASTE doesn't involve DSBs.

If Prime Medicine remains independent, it is possible to become a 10-bagger stock in 10 years. Keep in mind that might require a market cap exit of $40B+ after factoring in secondary offerings and SBC.

I should also point out that due to the convoluted IP structure of CRISPR, all of the newer editing techniques which build upon the original must license IP. For that reason, owning the old school names still makes sense but only at the right valuation.

IP is why I like Editas down here, despite the mismanagement and lack of clinical progress. The latest court ruling favors them versus CRSPR Therapeutics as being entitled to the original CRISPR technology.

From a risk/reward point, a name like Editas may make more sense than Prime Medicine, but I don't think it will be a 10-bagger stock. I think it will get bought out for IP far before then.

10. AbCellera Biologics

AbCellera Biologics ( ABCL ) is a Canadian-based company that has a full-stack, AI-powered antibody discovery platform. They help pharma find antibodies for specific needs. The best example - and only candidates they've successfully brought to market so far - are COVID-19 antibodies for Eli Lilly ( LLY ).

First Bamlanivimab and then Bebtelovimab were granted Emergency Use Authorization. They brought in hundreds of millions in royalties for AbCellera but each were eventually deemed obsolete, as newer Covid variants rendered them ineffective. Late last year the FDA revoked EUA for Bebtelovimab, while Bamlanivimab was pulled earlier.

With a market cap just shy of $3B, those several hundred million in revenue over a few months were a big deal. Imagine if they continued? Now, imagine if they had royalties coming in from several drugs, or even several dozen?

That is the thinking (or hope?) if you invest in AbCellera. They get relatively small payments upfront from pharma partners, along with royalties on all future sales of approved treatments. I recommend Confoundedinterest who regularly covers this company and here's his last piece from November.

AbCellera corporate overview, July 2022

{kind=link}

The royalties on the Covid antibodies were unusually large, because of the unusual circumstances under which it was needed and approved (pandemic, EUA). I do not know if the exact percentage has been disclosed but the math would suggest around 13-15%. For all others, expect much lower royalties. Think low to mid single digits percentage. 3-7% would be typical for this industry.

Speaking of 10-year bets, I should point out AbCellera was founded about 10 years ago, in 2012. With the exception of the briefly approved Covid antibodies, they haven't brought anything else to market. In drug development things almost always take longer and cost more than expected.

As a shareholder, that means more dilution than expected. For each 10+ bagger in this space, there's a graveyard of dozens which go to zero. Even for those that succeed, often times the earlier investors don't realize outsized gains due to years of dilution. Speculate carefully.

For further details see:

10 Potential 10x Return Stocks For The Next 10 Years