VNQ - 10 REIT Investor Mistakes: Avoid Them At All Costs

2023-03-23 08:05:00 ET

Summary

- REITs can be very rewarding.

- But they can also be very punishing if you pick the wrong ones.

- I highlight 10 REIT investor mistakes to avoid at all costs.

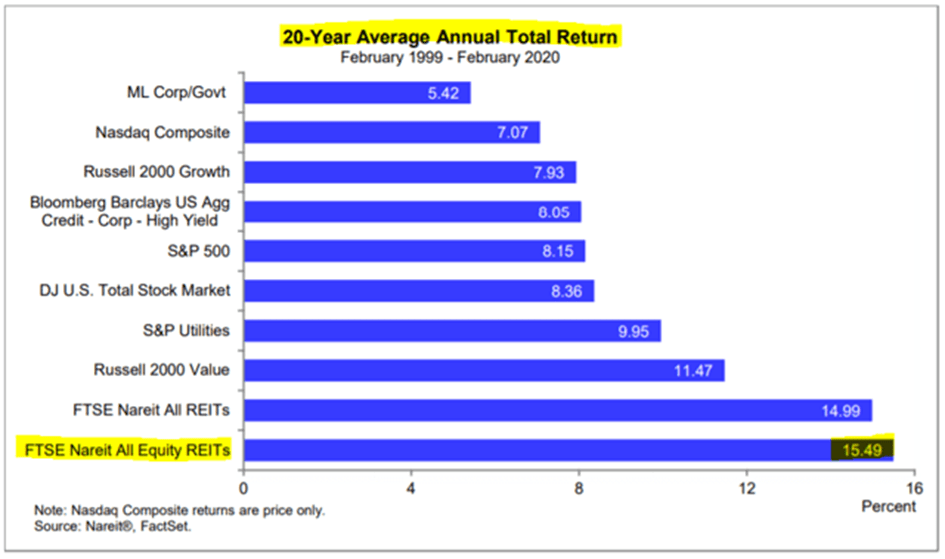

Real estate investment trusts, or REITs, have been some of the most rewarding investments of all-time.

Up until the crash of the pandemic, they generated 15% average annual returns, far outpacing the returns of the S&P 500 (SP500) or even tech stocks ( QQQ ):

{kind=link}

Since then, their performance has, of course, came down a bit as REITs suffered two crashes within two years, and today, we remain in a bear market.

But overall, over long periods of time, REITs have been incredible wealth-building machines for the average individual investor.

I would also note that this is just the average performance of the sector.

This means that some REITs did even better than average. Some of the best performers of all-time include Realty Income Corporation ( O ), Public Storage ( PSA ), and American Tower Corporation ( AMT ).

But this also means that there must have been many REITs that did a lot worse than the average of the market, and unfortunately, it seems to me that individual investors often make very poor choices when investing in REITs.

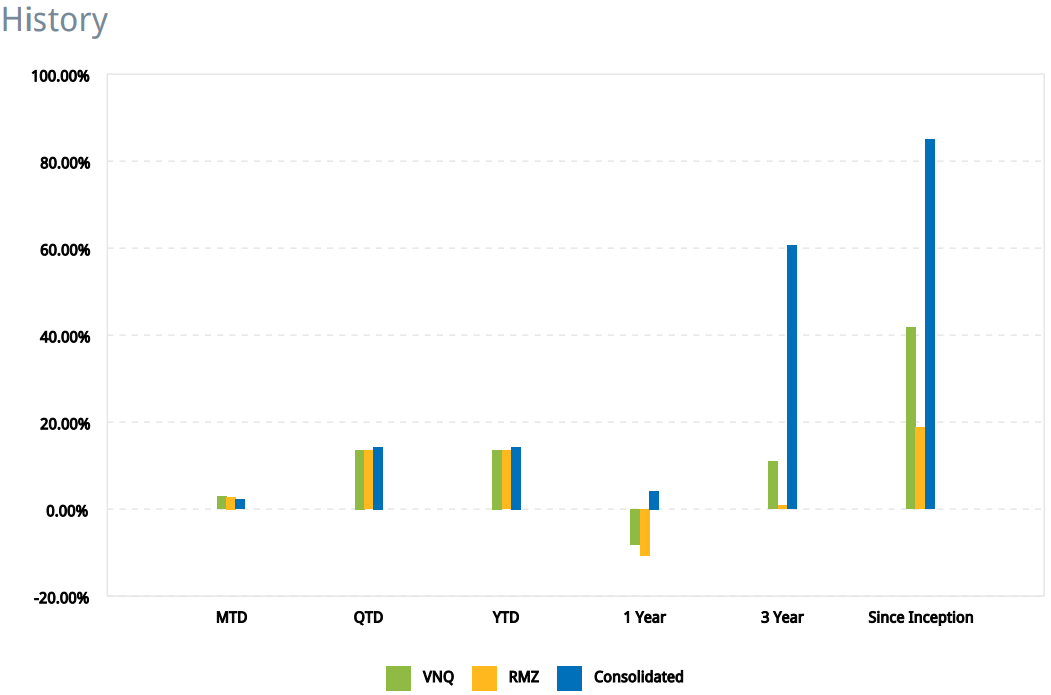

I don't want to pretend that I never make mistakes as I am far from being perfect, but overall, I have done quite well over time and managed to outperform the average of the sector ( VNQ ) by avoiding common REIT investment mistakes:

{kind=link}

In what follows, I highlight ten common REIT investor mistakes to avoid at all cost. Do this and you will already earn a lot better returns than most other REIT investors:

Mistake #1: Reaching for yield

A lot of investors come to the REIT sector in search of yield, and they then end up favoring the REITs that offer the highest dividend yields.

That's a mistake.

If a REIT is priced at a high yield, there is typically a very good reason for that. It is either overleveraged, poorly managed, or suffers declining cash flow. To give you an example, SL Green Realty Corp. ( SLG ) is priced at a 14% dividend yield, but it owns office buildings in NYC and its cash flow is set to decline.

Historically, the highest-yielding REITs have been some of the worst performers.

You should recognize that it is better to earn a safe and growing 5% yield than earn a risky >10% yield that likely won't be sustainable.

REITs are total return vehicles, not yield vehicles.

Mistake #2: Miscalculating dividend coverage

Most REIT investors calculate payout ratios using funds from operations ("FFO"), which is a rough representation of the cash flow.

But this does not take into account the capex, the straight lining of rents, and a few other factors.

Therefore, the dividend coverage will often be overstated. To get a better assessment of the dividend coverage, investors should use AFFO, or adjusted FFO, which deducts capex and makes other adjustments to get a real sense of the cash flow.

Many REITs cover their dividend very well with FFO, but poorly with AFFO. Office Properties Income Trust ( OPI ) is a good example of that.

Mistake #3: Overlooking the impact of capex on leverage

REITs often need to reinvest in their properties to keep them desirable to tenants. This maintenance capex can be very significant in some property sectors and it is not optional. If a REIT fails to properly maintain its properties, it will suffer significant issues down the line.

This capex can greatly reduce financial flexibility and increase the leverage. Investors will often overstate the strength of the balance sheet by overlooking the capex expenses.

I made this mistake with CBL & Associates Properties, Inc. ( CBL ) and paid dearly. You can read my recent article on CBL by clicking here.

Mistake #4: Trusting management teams

Management teams will often paint a rosy picture to hype up their stock.

But conflicts of interest can be significant and you should keep an eye for them to avoid being taken advantage of.

Externally managed REITs can be notoriously conflicted. The managers earn fees based on their assets under management and so they are incentivized to grow as large as possible, even if it comes at the cost of dilution.

In most cases, it would be preferrable to simply stay away from externally managed REITs.

Mistake #5: Focusing too much on quarterly results

Real estate is a long term investment.

Its cash flows and value change slowly over time.

Despite that, investors will commonly trade in and out of REITs based on quarterly results as if they had a significant impact on the fair value of the real estate.

In reality, the value of the real estate should be determined based on decades of expected future cash flow.

Don't make the mistake of overreacting to quarterly results or even short term news.

Mistake #6: Confusing Book Value With Net Asset Value

Some investors look at the book value to get an estimate of the value of the underlying properties, net of debt, and imagine that this is a good estimate of the fair value of a REIT.

But they appear to ignore that according to US GAAP accounting rules, REITs must depreciate the value of their assets. As such, if a REIT like Simon Property Group, Inc. ( SPG ) has owned a mall for decades, it will value it at $0 on its balance sheet, despite it having lots of value.

The point here is that you cannot use the book value that you see listed by many screeners. You need to calculate your own estimates of fair value, which is what we call the "net asset value," or NAV in short. This brings me to my next point:

Mistake #7: Overpaying by ignoring the NAV per share

A lot of REIT investors simply look at the dividend yield and the P/FFO ratio.

But this says very little about the value of the underlying real estate and how much you are paying for it.

To know how much you are paying for the real estate, you should calculate an estimate of the NAV. You can then compare the share price to the NAV per share to see if you are getting a good deal relative to what you would pay in the private market.

To give you an example: Camden Property Trust ( CPT ) is today priced at an estimated 30% discount to its net asset value. This is a great deal because you would pay a lot more for these assets in the private market.

Mistake #8: Forgetting that you are investing in the real estate, not the tenant

REIT investors will often panic at the first sign of tenant issues.

They will sell of the stock as if the value of the real estate had been permanently impaired.

But they forget that the real estate still holds a lot of value and can be released to another tenant, possibly even at a higher rent if it is desirable.

A lot of tenants come and go because of overleverage and poor management. This does not mean that the real estate is worthless.

A good example would be EPR Properties ( EPR ). It is discounted today because AMC Entertainment Holdings, Inc. ( AMC ) is one of its biggest tenants. But the market appears to forget that EPR owns the most productive theaters in North America, and many other movie theater operators would gladly take over the space if AMC was going to fail.

Mistake #9: Having a trader's mentality

This does not apply just to REITs, but many investors will trade in and out of REITs as if they were traders based their emotional reaction to short term news and market volatility.

This is perhaps the biggest mistake that investors make all the time.

Instead of thinking like a trader, you should think like a landlord when investing in REITs. This is why we called our REIT investing group here on Seeking Alpha: "High Yield Landlord."

Mistake #10: Failing to take advantage of market volatility

The best time to invest is when prices are low and fear is high.

Yet, investors will often fail to take advantage of market opportunities, fearing that prices will drop even lower.

We are seeing a lot of investors make this mistake today.

Prices have been plunging, REITs are priced at their lowest valuations in years, and yet, few are capitalizing on these opportunities.

I see a lot of people claim in comment section that "we have not reached a bottom yet" or that it is "too early to invest."

In reality, I think that it is impossible to time the market and no one really knows what the market will do in the short run.

Therefore, you shouldn't try to predict the unpredictable. Instead, you should focus on the bigger picture: what are the fundamentals? and are today's valuations attractive in light of those fundamentals?

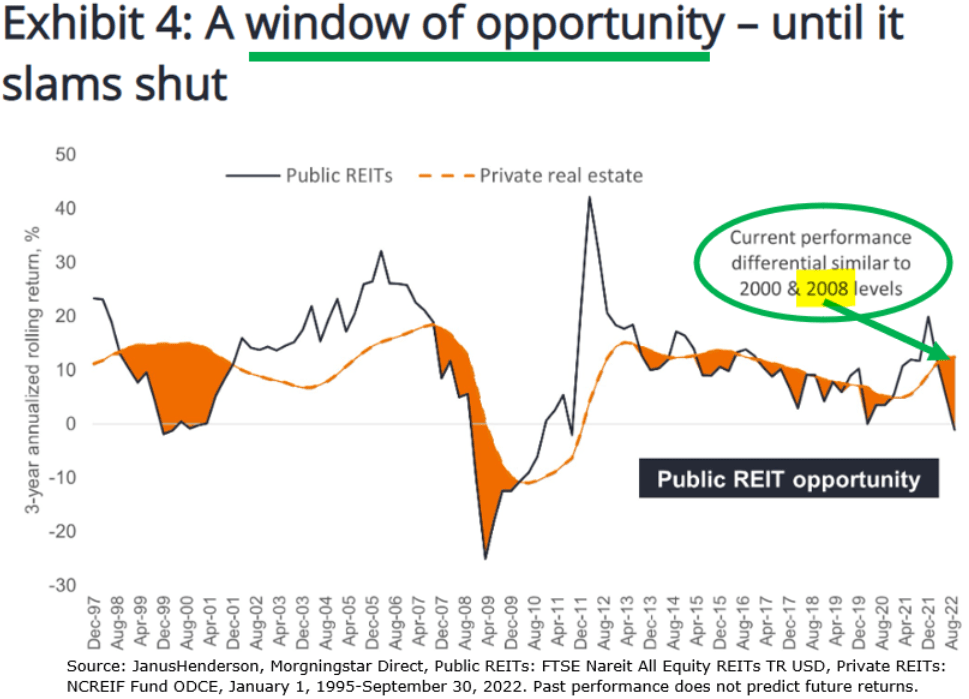

I think that we are today presented with a historic opportunity because REITs are priced at valuations that are reminiscent of the great financial crisis:

{kind=link}

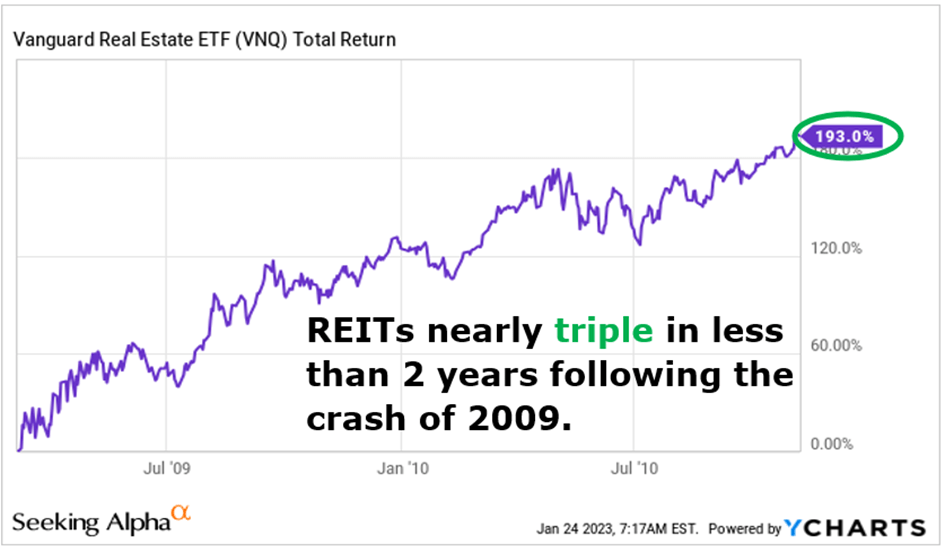

Following the great financial crisis, REITs nearly tripled investor's money in just 2 years:

{kind=link}

Investors made fortunes buying discounted REITs because they took action when others were paralyzed by their fears of lower prices. I won't make this mistake.

For further details see:

10 REIT Investor Mistakes: Avoid Them At All Costs