MAA - 10 REITs To Buy In 2024

2023-12-31 07:00:00 ET

Summary

- I don’t want to put my money into lackluster or even mere “decent” holdings.

- And you shouldn’t either.

- That should be an automatic new year’s resolution – even if you hate making them.

- Commit right now as 2024 dawns to buying up only quality companies that can make your life better….

Let’s address the big question everyone’s asking now that Christmas is past.

For the record, I hope you had a wonderful Christmas filled with every good thing… and that you managed to somehow keep the weight off from all those cookies, eggnog, and other tasty treats.

If you didn’t, well… Everyone needs a good list of inspiring new year’s resolutions, right?

(See my REIT Resolutions here )

But even if you can miraculously step on the scale and find that your weight didn’t spike, that hardly means you’ve got nothing to strive for in 2024. Especially when it comes to the stock market.

There’s always room to grow there, right? And in more ways than one.

That’s why I’ve compiled this list of 10 real estate investment trusts, or REITs, that should pay off this new year. Because I do expect them to grow in both share price and dividends.

Now, here’s where I need to add a disclaimer: These recommendations are not reliant on whether the Fed makes any rate cuts anytime soon.

Everything considered, it does seem like that will happen – though perhaps not by as much as some seem to expect. But I don’t believe in buying shares based on big-deal projections alone.

That’s why, whenever I predict a merger, I stress all the reasons I like the company as-is. So that, if the story plays out differently than I expect, the investment still stands on its own.

With that said, I never object to a bonus. And I doubt you do either.

A REIT for (Almost) Every Resolution

What are your new year’s resolutions for 2024? A quick Google search shows that common ones include:

- Quit smoking.

- Start exercising/eat healthier/get in shape/lose weight.

- Drink less.

- Improve finances/increase savings/reduce spending.

- Spend more time with family.

- Get more sleep.

- Learn something new.

- Take better care of yourself.

- Reduce stress.

- Travel more.

- Get organized.

- Read more.

Do any of those ring a bell?

More than likely, you wouldn’t object to seeing at least one of those happen in the next 12 months.

Obviously, I can’t completely help you with all of them. But I could be instrumental in at least putting you on better footing to accomplish them with the 10 REITs I’m about to dive into down below. Your life tends to improve in more ways then one, after all, when you’re not stressing about money.

Think about it…

Why do you smoke (if you smoke)?

It’s an addiction, yes, but one that’s so much easier to justify when life feels too hard to handle. The same goes for excessive drinking, of course.

Why don’t you exercise the way you’d like to? It might have something to do with being too busy trying to make money.

And, if you’re too busy trying to make money, you could just as easily be jilting your family, losing out on sleep, stressing out, traveling less, and seeing piles and piles of paper and other stuff – including books – building up around you that you just don’t have time to get to.

But what if you were already confident your finances were in order?

What then?

Commit to Having the Best Possible REIT-Filled New Year

Let me repeat that first question with a new follow-up idea or two…

What if you were already confident your finances were in order? And what if those finances were working for you even while you slept?

That’s the whole point of REITs, as my regular readers know. They might not give you the fastest share price gains out there.

But they are designed to give you steady, reliable, and even growing dividends that can either be put toward a happy, healthy retirement or make the retirement you’re already enjoying better still.

For those in the “retirement planning” phase, the best thing to do is to take those quarterly – or, better yet, monthly – dividend payments and reinvest them in the same stocks they came from. That way, the next time dividends are distributed, you have even more coming in!

Which you then reinvest again for even more payout potential over and over again until you retire.

Again, my regular readers know this. In fact, they might have already skipped ahead all this explanatory preamble to get to “the good stuff.”

Speaking of such, I’ll also risk wasting people’s time by pointing out that some REITs are better at delivering “the good stuff” than others. So you’d better believe I carefully considered which 10 belonged on my list.

I don’t want to put my money into lackluster or even mere “decent” holdings. And you shouldn’t either.

That should be an automatic new year’s resolution – even if you hate making them. Commit right now as 2024 dawns to buying up only quality companies that can make your life better…

Not just in the short term but for years and hopefully even decades to come.

Then, once you do, carefully consider the following 10 REITs.

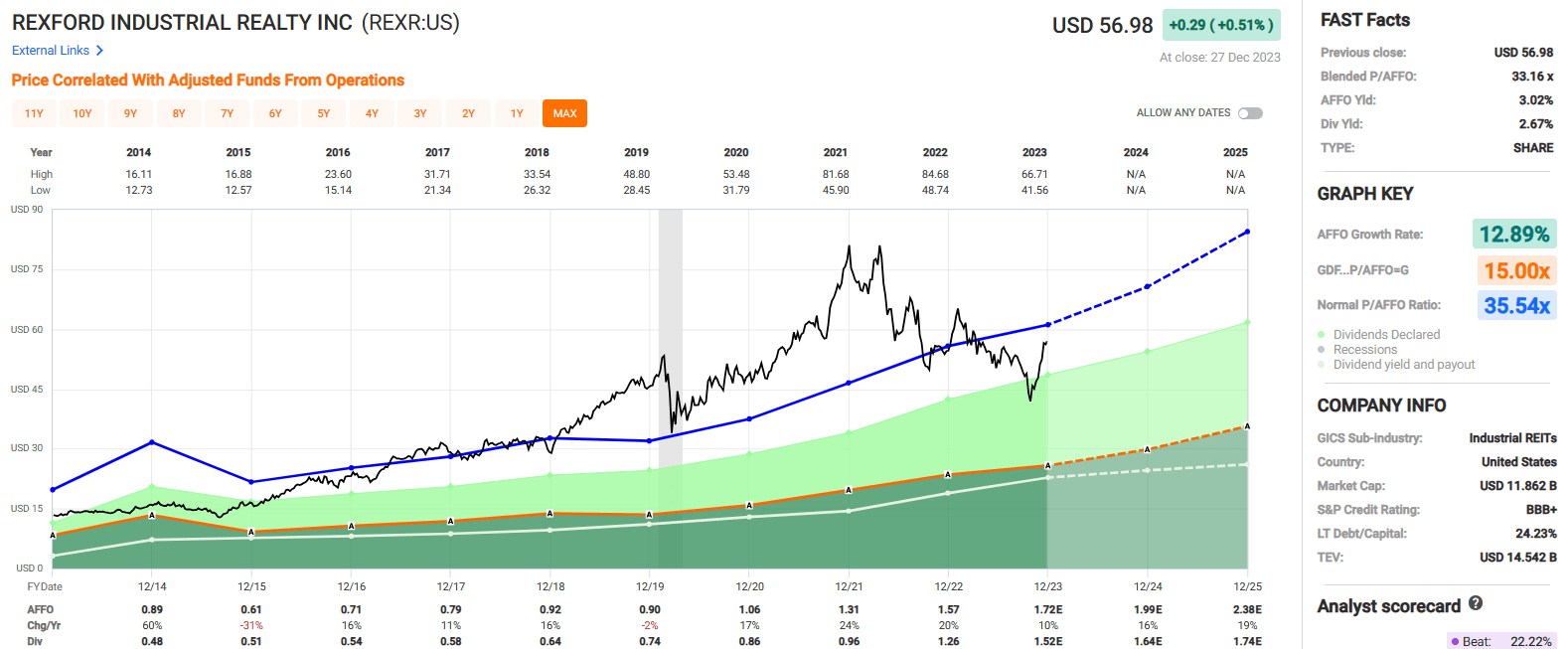

Rexford Industrial Realty ( REXR )

Rexford Industrial is a real estate investment trust (“REIT”) that specializes in the acquisition, redevelopment, and operation of industrial properties throughout infill Southern California (“SoCal”).

REXR has a market cap of almost $12 billion and a portfolio of 371 industrial properties that covers approximately 45 million square feet across the SoCal region.

Having their entire portfolio concentrated in the SoCal region is a strategic decision due to the nature of the SoCal industrial market. SoCal is the largest industrial market in the U.S. and consistently has a supply / demand imbalance.

The economy in SoCal is enormous, consisting of roughly 22 million residents and over 600,000 businesses while the supply of developable land is scarce due to the natural barriers (mountains / ocean) that surrounds the region.

Essentially, instead of spreading their resources and expertise across multiple markets within the U.S., REXR has chosen to exclusively focus on SoCal due to its size and favorable characteristics.

At the end of the third quarter, REXR reported an average same property portfolio occupancy of 97.8%.

REXR has an investment-grade balance sheet with a BBB+ credit rating and excellent debt metrics including a net debt to adjusted EBITDA of 3.7x, a long-term debt to capital ratio of 24.23% and an EBITDA to interest expense ratio of 7.92x.

Since 2014, REXR has delivered an adjusted funds from operations (“AFFO”) average growth rate of 12.89% and an average dividend growth rate of 13.08% over the last 8 years.

Analysts expect rapid growth in AFFO with projections for AFFO to increase by 16% in 2024 and by 19% in 2025.

Currently REXR pays a 2.67% dividend yield that is well covered with an AFFO payout ratio of 80.25% and trades at a P/AFFO of 33.16x, compared to its average AFFO multiple of 35.54x.

We rate Rexford Industrial a Buy.

{kind=link}

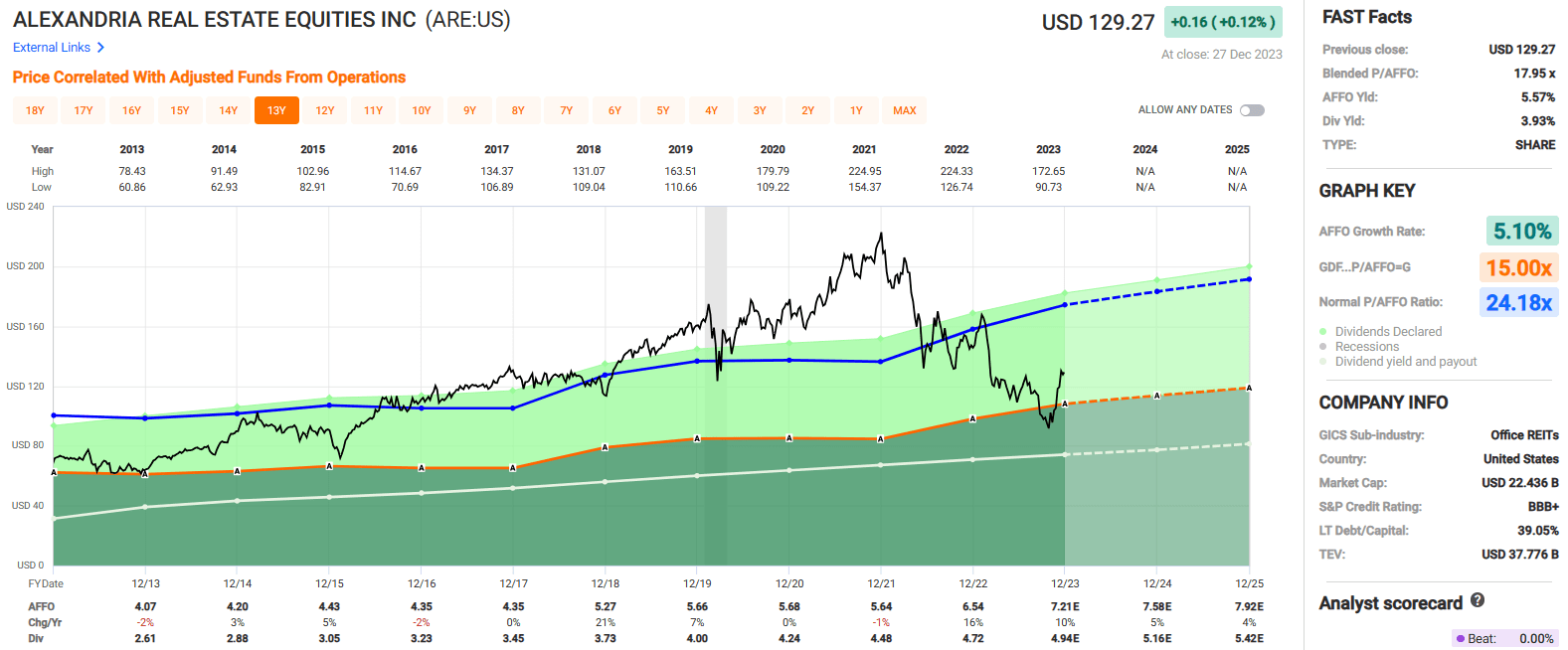

Alexandria Real Estate ( ARE )

Alexandria is a life science REIT that develops, owns, and manages a portfolio of Class A/A+ collaborative life science properties in AAA innovation cluster locations within leading markets such as Boston, New York City, San Francisco, San Diego, Seattle, Maryland, and the Research Triangle.

ARE has a market cap of approximately $22 million and an asset base in the U.S. covering roughly 75.1 million square feet which consists of 41.5 million rentable square feet (“RSF”) of operating properties, 14.5 million RSF of properties in development or undergoing construction, and 19.1 million square feet of future developments.

ARE has around 800 tenants which include top pharmaceutical and biotechnology companies such as Eli Lily, Moderna, and Bristol-Myers Squibb and 16 out of their top 20 tenants are investment-grade rated.

Due to the nature of the processes performed in ARE’s laboratory space, such as drug development, many of the tasks performed at ARE’s properties are regulated and cannot be done from home.

At the end of the third quarter, ARE reported occupancy of 93.7% for their operating properties with a weighted average lease term (“WALT”) of approximately 7 years.

Alexandria has an investment-grade balance sheet with a BBB+ credit rating and excellent debt metrics including a net debt plus preferred stock to adj EBITDA of 5.4x, a long-term debt to capital ratio of 39.05%, and a fixed charge coverage ratio of 4.8x

Over the last decade, ARE has had an average AFFO growth rate of 5.10% and an average dividend growth rate of 8.62%. Analysts expect AFFO per share to increase by 5% in 2024 and then by 4% in 2025.

ARE pays a 3.93% dividend yield that is well covered with an AFFO payout ratio of 72.17% and trades at a P/AFFO of 17.95x, compared to its 10-year average AFFO multiple of 24.18x.

We rate Alexandria Real Estate a Buy.

{kind=link}

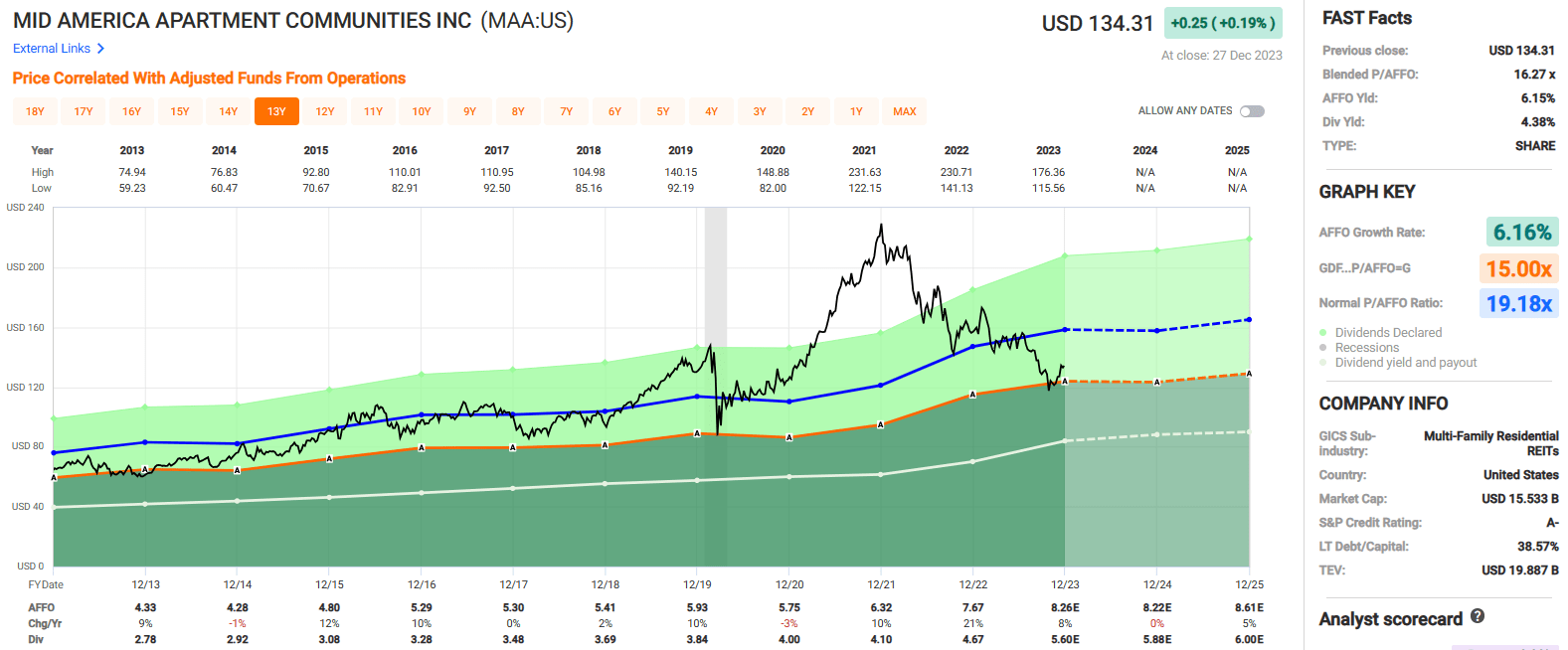

Mid-America Apartment ( MAA )

MidAmerica is a multifamily REIT that specializes in the development, acquisition, and management of apartment communities which are primarily located in high-growth markets within the Sunbelt region of the country.

MAA has a market cap of approximately $15.7 billion and a portfolio which consists of multifamily communities located in 16 states and Washington D.C. that in total contain approximately 102,000 apartment homes.

When measured by same-store net operating income (“same-store NOI”), MAA’s top markets include Atlanta at 12.7%, Dallas at 10.0%, Tampa at 6.9%, Orlando at 6.7% and Charlotte at 6.4%.

MAA’s portfolio is composed of multiple types of apartment communities including garden style (3 stories or less), mid-rise (4 to 9 stories), and high-rise (over 10 stories). Based on gross asset value, the majority of MAA’s portfolio consists of garden style apartments at 62%, followed by mid-rise at 34% and high-rise at 4%.

At the end of the third quarter, MAA reported an average physical occupancy of 95.7%.

MAA has an investment-grade balance sheet with an A- credit rating and strong debt metrics including a net debt to adjusted EBITDAre of 3.4x, a long-term debt to capital ratio of 38.57%, and a debt service coverage ratio of 7.8x.

Since 2013, MAA has had an average AFFO growth rate of 6.16% and an average dividend growth rate of 5.92%. Since its IPO in 1994, MAA has never suspended or reduced its quarterly dividend and just recently announced a 5% increase to their dividend on December 12 th .

MAA pays a 4.38% dividend yield that is secure with an AFFO payout ratio of 60.95%. The stock currently trades at a P/AFFO of 16.27x, compared to its 10-year average AFFO multiple of 19.18x.

We rate Mid-America Apartment a Buy.

{kind=link}

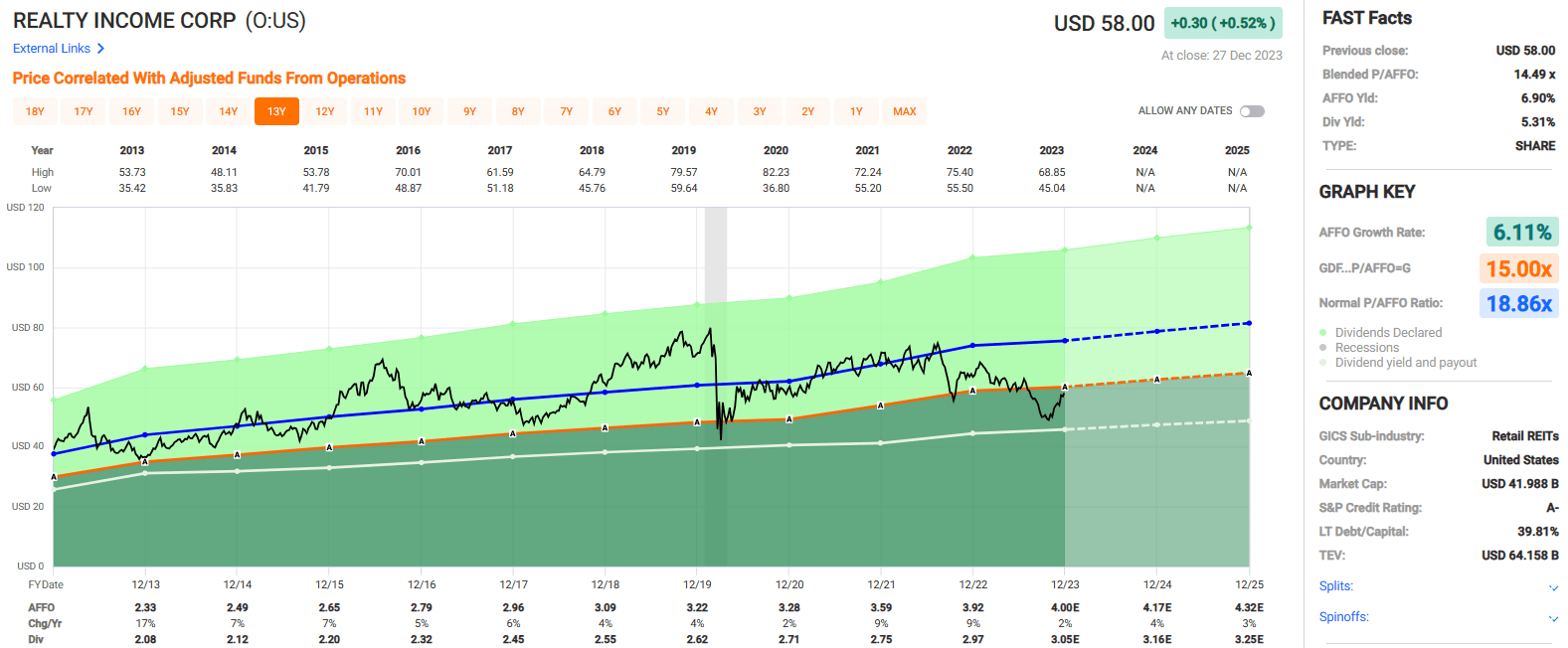

Realty Income ( O )

Realty Income is a triple-net lease REIT that invests in single-tenant, freestanding commercial properties which are leased to retailers in defensive industries and operators of industrial and gaming properties.

The net-lease REIT has a market cap of approximately $42 billion and a 262.6 million SF portfolio that consists of over 13,000 commercial properties located in all 50 states, the United Kingdom, Spain, Italy, and Ireland.

In total, O’s properties are leased to roughly 1,300 tenants doing business in 85 separate industries. Retail properties make up 82.6% of O’s portfolio, while industrial and gaming properties make up 13.1% and 2.6% respectively.

Realty Income targets retail properties used in industries that are resistant to recession and ecommerce such as grocery stores, convenience stores, and dollar stores. As a percentage of their contractual rent, grocery and convenience stores are their largest industries and make up 11.4% and 10.6% respectively of their annual rent.

As of their most recent update, Realty Income’s portfolio had a 98.8% occupancy rate and a WALT of approximately 9.7 years.

Realty Income has an investment-grade balance sheet with an A- credit rating and solid debt metrics including a net debt to pro forma adj EBITDAre of 5.2x, a long-term debt to capital ratio of 39.81%, and a fixed charge coverage ratio of 4.5x.

O pays a monthly dividend and has consistently done so over its 54-year operating history. It is one of the few REITs to earn the title of a Dividend Aristocrat, having increased their monthly dividend for 29 consecutive years and for 105 consecutive quarters.

Since 2013, Realty Income has had an average AFFO growth rate of 6.11% and an average dividend growth rate of 5.76%. Analysts expect AFFO per share to increase by 4% in 2024 and by 3% in 2025.

Currently Realty Income pays a 5.31% dividend yield that is well covered with an AFFO payout ratio of 75.69% and shares trade at a P/AFFO of 14.49x, compared to its 10-year average AFFO multiple of 18.86x.

We rate Realty Income a Buy.

{kind=link}

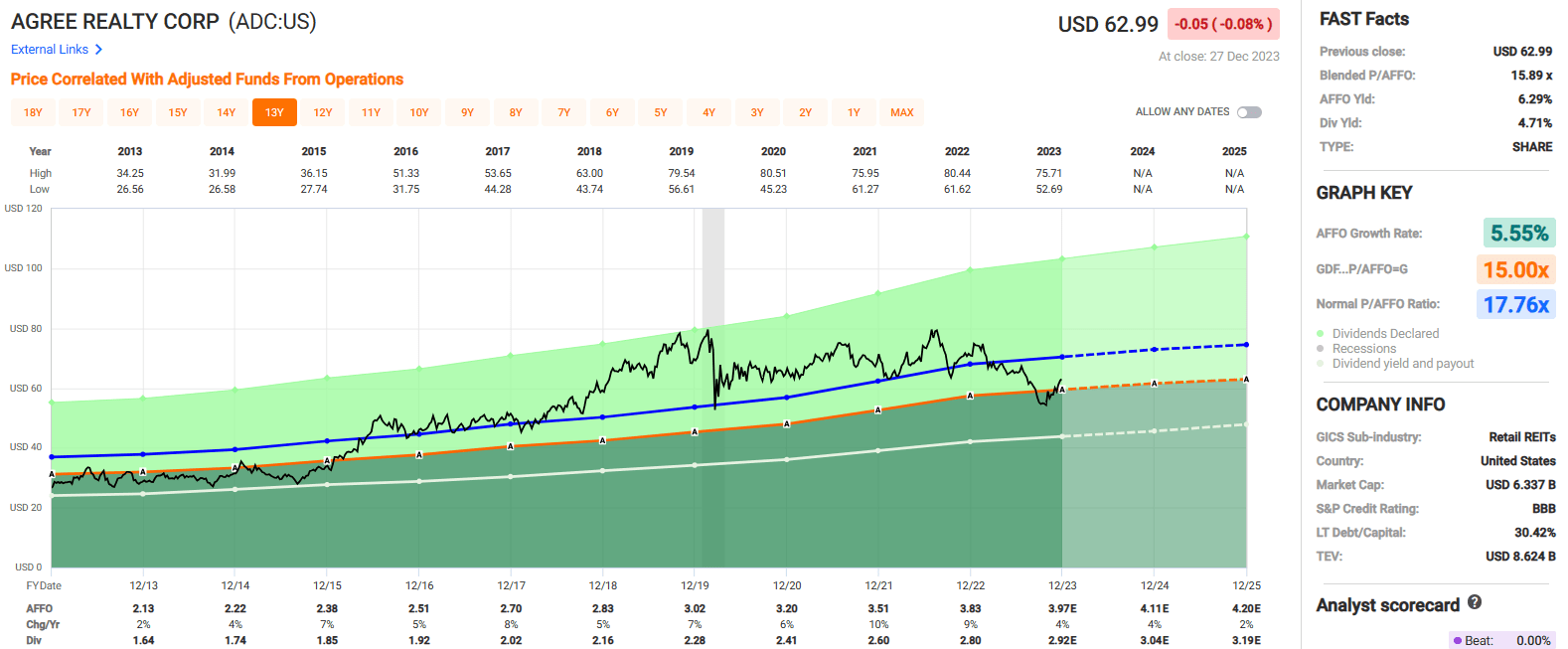

Agree Realty ( ADC )

Agree Realty is a net-lease REIT with a market cap of approximately $6 billion and a 43 million SF portfolio that consists of free-standing retail commercial properties.

ADC owns or has an ownership interest in more than 2,000 retail properties located across 49 states which are leased to leading retailers such as Walmart, Home Depot, Costco, and Lowes.

ADC targets high-quality retail tenants and as of its most recent update, the company received almost 69% of its annualized base rent (“ABR”) from investment-grade tenants.

Agree Realty looks to acquire retail properties used in defensive industries that are insulated from the threat of ecommerce and recession. Grocery is ADC’s top retail sector and makes up 9.7% of their ABR, followed by home improvement and tire & auto service which makes up 8.6% and 8.5% respectively of its ABR.

In addition to its free-standing net-leased properties, ADC also has a ground lease portfolio which made up approximately 11.6% of its total portfolio ABR. Their ground lease portfolio consists of 217 leases with a WALT of 10.8 years and 88% of the ABR derived from their ground lease portfolio comes from investment-grade tenants.

At the end of the third quarter, ADC’s portfolio was 99.7% leased with a WALT of approximately 8.6 years.

ADC has an investment-grade balance sheet with a BBB credit rating and strong debt metrics including a net debt to recurring EBITDA of 4.5x, a long-term debt to capital ratio of 30.42%, and a fixed charge coverage ratio of 5.1x.

Since 2013, ADC has had an average AFFO growth rate of 5.55% and an average dividend growth rate of 5.79%. ADC pays monthly dividends and has paid 141 consecutive dividends over the past 10 years. Originally, Agree Realty paid quarterly dividends, but changed to a monthly payout in 2021.

ADC pays a 4.71% dividend yield that is well covered with an AFFO payout ratio of 73.24% and trades at a P/AFFO of 15.89x, compared to its 10-year average AFFO multiple of 17.76x.

We rate Agree Realty a Buy.

{kind=link}

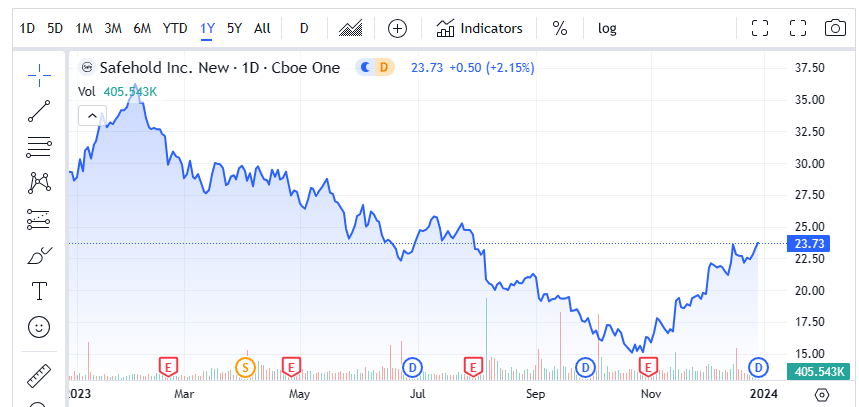

Safehold ( SAFE )

Safehold is an internally managed REIT that specializes in ground leases. Ground leases split the improved commercial property from the land upon which it sits. SAFE will acquire the ground and lease it back to the building owner on a triple-net basis.

Ground leases structured on a triple-net basis are similar to other net leased properties in that the tenant is responsible for all property level expenses including insurance, taxes, and maintenance. However, ground leases have several characteristics that distinguish them from traditional net leases.

SAFE’s ground leases have very long lease terms that can range between 30 to 99 years and hold residual rights which allows SAFE to take the ground and building once the lease expires, or if the tenant defaults on the ground lease.

Safehold structures ground leases for multiple property types including office, multifamily, hotel and life science. SAFE has a 34.1 million SF ground lease portfolio which consists of 15.8 million SF of multifamily properties, 12.5 million SF of office properties, 3.8 million SF of hotel properties, and 1.3 million SF of life science properties.

During 3Q-23, SAFE reported net income (excluding merger and caret related costs and non-recurring gains) of $22.5 million, or $0.33 earnings per share (“adj EPS”). Based on 3Q-23 adj EPS annualized, SAFE currently trades at a P/E ratio of 17.99x and pays a 2.99% dividend yield that is covered with a 3Q-23 dividend payout ratio of 53.63%.

Safehold has an investment-grade balance sheet and was upgraded from Baa1 to A3 by Moody’s subsequent to the third quarter. They have a total debt to book equity ratio of 1.8x, a total debt to equity market cap ratio of 3.7x, and a weighted average term to maturity of 22.5 years.

We rate Safehold a Strong Buy.

{kind=link}

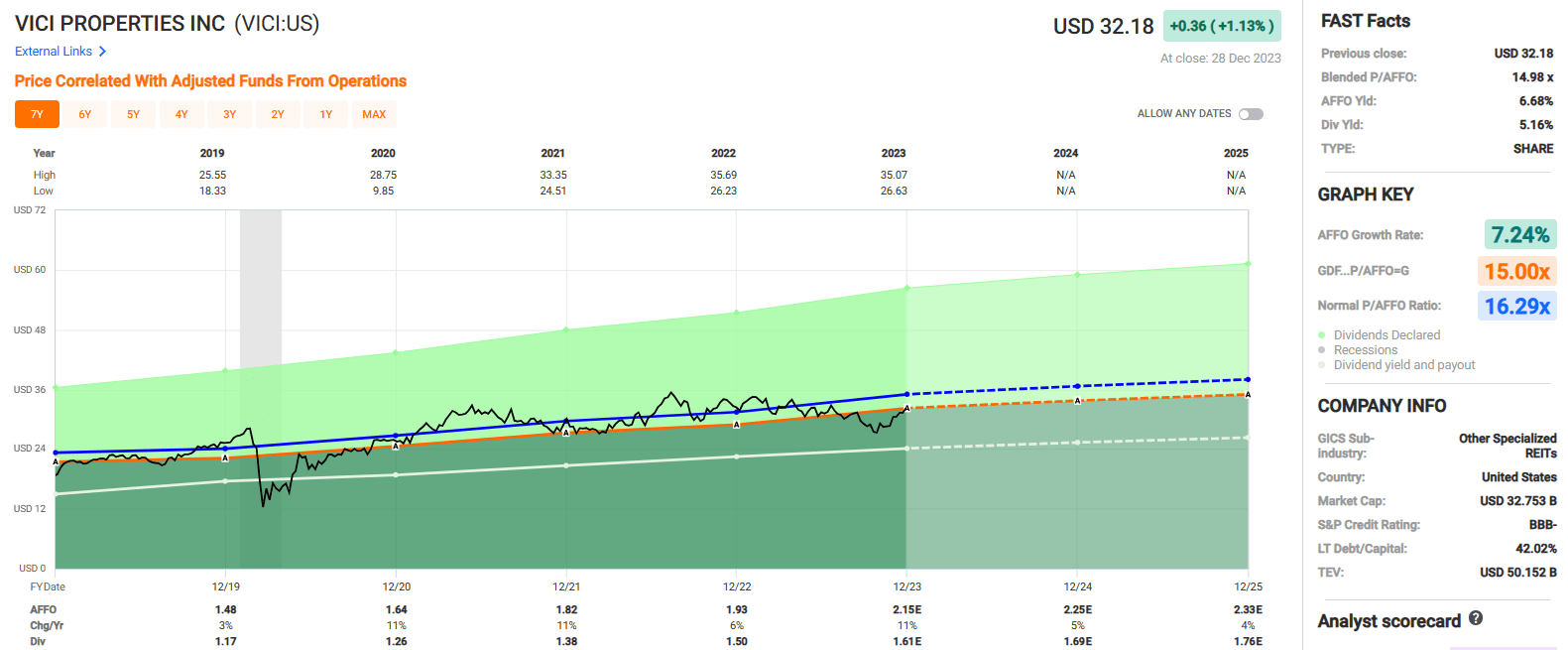

VICI Properties ( VICI )

VICI is a gaming REIT that specializes in experiential real estate with a 127 million SF portfolio that consists of top gaming, hospitality, and entertainment destinations. VICI’s portfolio includes 93 experiential assets located across the U.S. and Canada that are leased to leading operators on a triple-net basis.

It has 54 core gaming properties and 39 non-gaming experiential properties which are primarily bowling entertainment centers that VICI recently acquired from Bowlero ( BOWL ).

VICI’s 54 gaming facilities include iconic trophy properties such as Caesars Palace Las Vegas, the Venetian Resort, and MGM Grand Las Vegas and in total their gaming properties feature more than 60,000 hotel rooms, around 500 retail shops, and approximately 500 bars, restaurants, nightclubs, and sportsbooks.

Additionally, VICI owns 4 championship golf courses and over 30 acres of developable land next to the Las Vegas Strip.

At the end of the third quarter, VICI’s portfolio had an 100% occupancy rate and a WALT of 41.5 years when including all tenant extension options.

VICI is investment grade with a BBB- credit rating. The gaming REIT has solid debt metrics including a net leverage ratio of 5.7x, a long-term debt to capital ratio of 42.02%, and an EBITDA to interest expense ratio of 4.07x.

Since 2019 VICI has had an average AFFO growth rate of 7.24% and an average dividend growth rate of 10.80%. Analysts expect AFFO per share to increase by 5% in 2024 and then by 4% in 2025. VICI pays a 5.16% dividend yield that is well covered with an AFFO payout ratio of 77.72% and trades at a P/AFFO of 14.98x, compared to its average AFFO multiple of 16.29x.

We rate VICI Properties a Buy.

{kind=link}

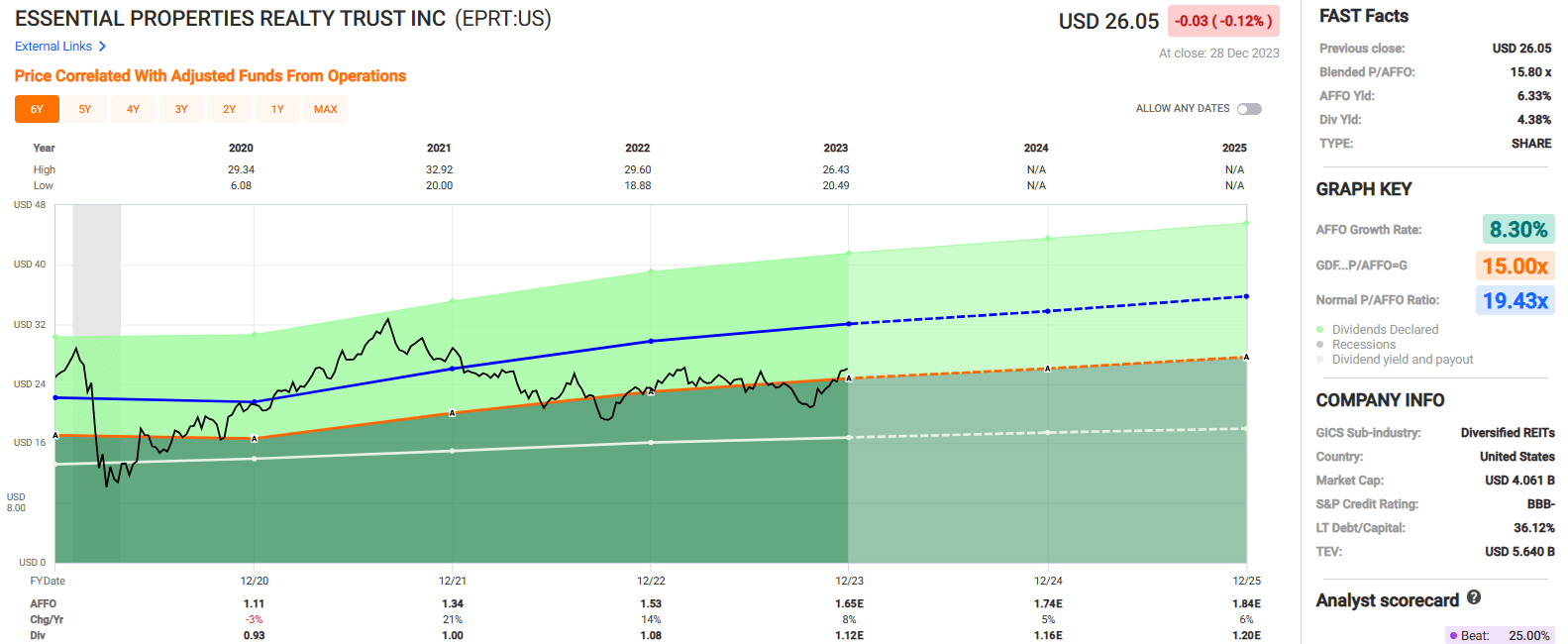

Essential Properties Realty Trust ( EPRT )

Essential Properties is a net lease REIT that specializes in the acquisition and management of single-tenant properties that are leased to companies that operate primarily in experience-based or service-oriented businesses.

EPRT has a market cap of approximately $4 billion and a 17.8 million SF portfolio comprised of 1,793 free-standing properties leased to 363 tenants operating in 16 separate industries across 48 states.

EPRT focuses on sale-leasebacks (“SLBs”) with middle market companies that provide unit-level reporting and tend to occupy smaller-scale, single-tenant properties that are fungible in nature.

Their investment strategy targets tenants operating in businesses such as car washes, quick service restaurants and casual family dining, medical services, auto services, early childhood education and convenience stores.

Their largest tenant industry is car washes which represents approximately 15% of EPRT’s portfolio, followed by early childhood education which made up approximately 12%.

At the end of the third quarter, EPRT’s portfolio was 99.8% leased with a WALT of 13.9 years and a weighted average rent coverage of 4.0x.

EPRT has an investment-grade balance sheet with a BBB- credit rating and excellent debt metrics including a pro forma net debt to adjusted EBITDAre of 3.7x, a long-term to capital ratio of 36.12%, and a fixed charge coverage ratio of 6.5x.

Since 2020, EPRT has had an average AFFO growth rate of 8.30% and an average dividend growth rate of 6.90%. Analysts expect AFFO per share to increase by 5% in 2024 and by 6% the following year.

EPRT pays a 4.38% dividend yield that is well covered with an AFFO payout ratio of 70.26% and trades at a P/AFFO of 15.80x, compared to its normal AFFO multiple of 19.43x.

We rate Essential Properties Realty Trust a Buy.

{kind=link}

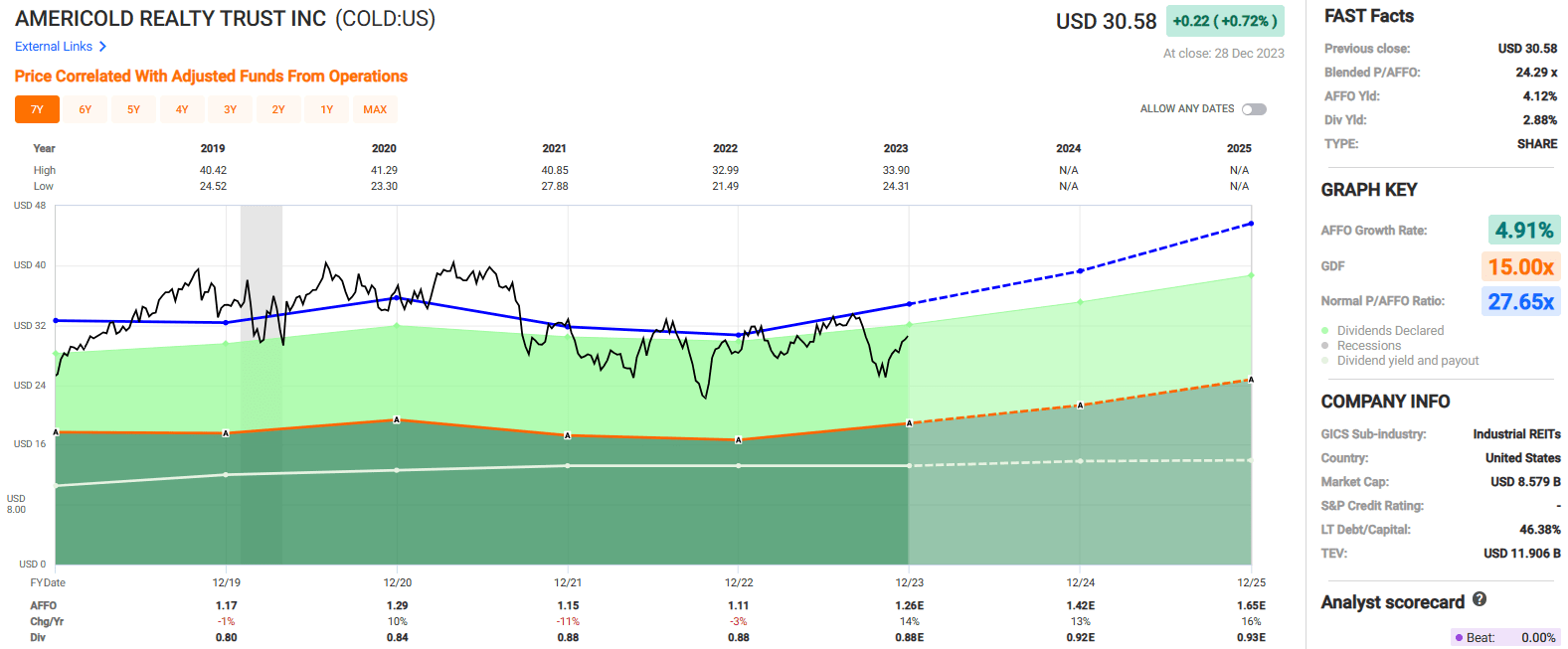

Americold Realty Trust (COLD)

Americold Realty is an industrial REIT that specializes in temperature-controlled warehouses and has one of the largest temperature-controlled storage and distribution networks with properties located in North and South America, Europe, and Asia-Pacific.

COLD has a market cap of approximately $8.6 billion and a 45.7 million SF portfolio comprised of 243 temperature-controlled warehouses that they either own and / or operate.

By region, COLD’s portfolio has 195 warehouses in North America, 27 warehouses in Europe, 19 in Asia-Pacific, and 2 warehouses in South America.

COLD’s facilities “mission-critical” and are a vital part of the temperature-controlled supply chain that connects food producers and processors to retailers and consumers. Some of their more notable tenants include Conagra Brands, Unilever, Kraft Heinz, Safeway, Ahold Delhaize, Walmart, and General Mills.

At the end of the third quarter, COLD’s total warehouse segment had a economic occupancy of 83.0% and a physical occupancy of 74.7%.

COLD is investment-grade rated with a Baa3 credit rating from Moody’s. They have a net debt to pro forma core EBITDA of 5.7x, a long-term debt to capital ratio of 46.38%, and an EBITDA to interest expense ratio of 3.38x.

Additionally, their real estate debt has a weighted average contractual interest rate of 3.8% and a weighted average term to maturity of 5.5 years.

Since 2019, COLD has had an average AFFO growth rate of 4.91% and an average dividend growth rate of 5.93%. Analysts expect AFFO per share to increase by 13% in 2024 and by 16% in 2025.

COLD pays a 2.88% dividend yield that is well covered with an AFFO payout ratio of 79.28% and trades at a P/AFFO of 24.29x, compared to their normal AFFO multiple of 27.65x.

We rate Americold Realty Trust a Buy.

{kind=link}

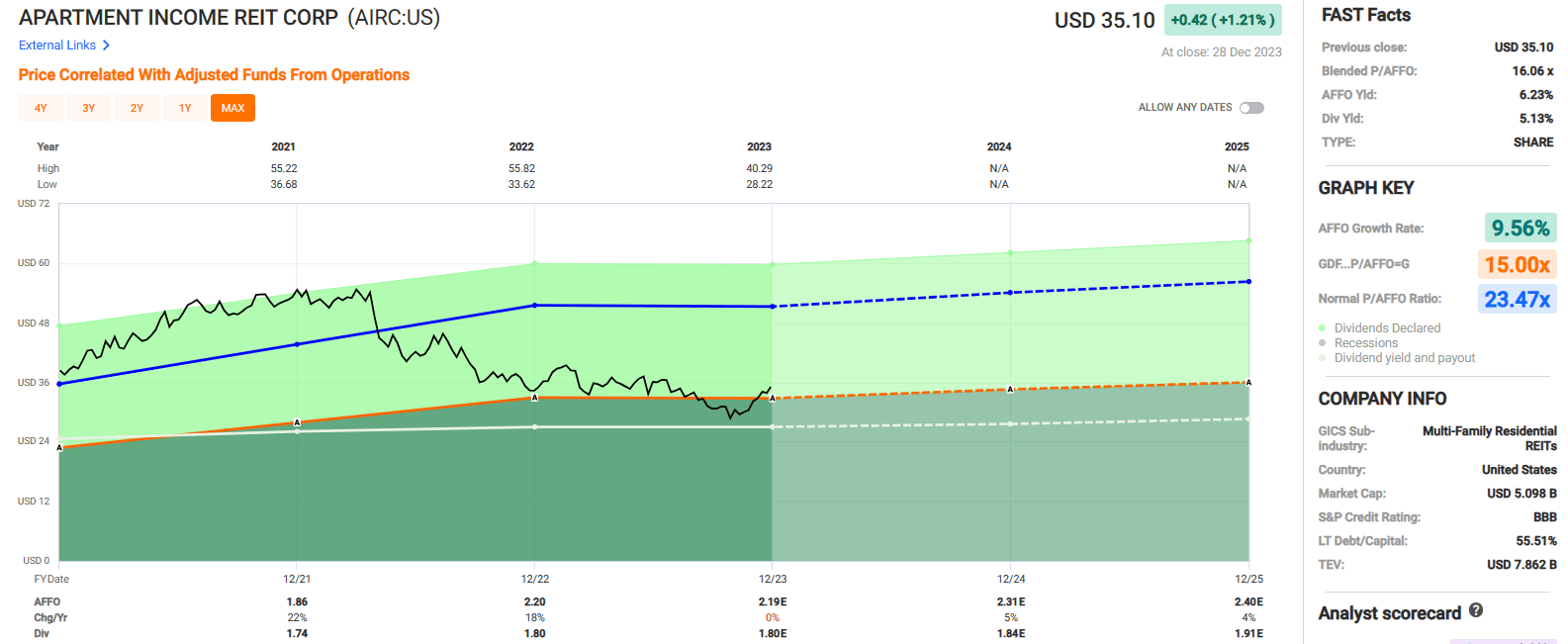

Apartment Income REIT ( AIRC )

AIRC is an internally managed multifamily REIT that has a market cap of approximately $5.5 billion and a portfolio which is comprised of 75 multifamily communities containing a total of 26,623 apartment homes across 10 states and Washington, D.C.

When measured by gross asset value, 57% of their portfolio is made up of Class A properties and 43% of their portfolio is made up of Class B properties.

AIRC focuses on 8 core markets that have good growth prospects and above average wages. Some of their core markets include Boston, Denver, Los Angeles, Miami, and Washington, D.C.

Apartment Income REIT is selective in the tenants they lease to and look for high-quality tenants to fill their apartment homes. As of 3Q-23, AIRC’s tenants had an average income of $241,000 and an average FICO score of approximately 725. AIRC refers to these tenants as “renters by choice”.

Apartment Income REIT has installed smart home technology in every apartment unit in its portfolio including smart locks that eliminate the need for keys, smart thermostats that monitor humidity and reduces the need for moisture-related services, and smart water sensors that can quickly identify leaks to prevent major flooding.

At the end of the third quarter, AIRC reported same store average daily occupancy of 95.3%.

AIRC has an investment-grade balance sheet with a BBB credit rating and sound debt metrics including a net leverage to EBITDAre of 6.3x, a long-term debt to capital ratio of 55.51%, and an EBITDA to interest expense ratio of 3.78x.

Additionally, their debt has a W.A. interest rate of 4.2% with a W.A. term to maturity of 6.9 years.

Since 2021, AIRC has had an average AFFO growth rate of 9.56% and an average dividend growth rate of 4.77%. Analysts expect AFFO growth to normalize over the next several years with AFFO growth of 5% projected in 2024 and AFFO growth of 4% projected in 2025.

AIRC pays a 5.13% dividend yield that is well covered with an AFFO payout ratio of 82.0% and trades at a P/AFFO of 16.06x, compared to its normal AFFO multiple of 23.47x.

We rate Apartment Income REIT a Strong Buy.

{kind=link}

In Closing

I hope you enjoyed my Top 10 REIT Buy List for 2024:

iREIT @rbradthomas

I wish you the very best in the new year and I look forward to your comments and/or questions below.

Happy REIT Investing!

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

10 REITs To Buy In 2024