DEA - 10%-Yielding Easterly Government Is Too Cheap To Ignore

2023-10-30 08:10:00 ET

Summary

- Easterly Government Properties has fallen by 39% over the past year and currently yields over 10%.

- DEA is the largest owner and lessor of Class A commercial properties leased to the U.S. Government, providing high assurance of rent collection.

- Despite concerns about higher interest rates and debt levels, DEA's lease structure allows for growth with inflation and the stock is trading significantly below book value.

It’s been a while since I last visited Easterly Government Properties ( DEA ) here back in August of 2021. The stock was a solid performer during the era of low rates back then, but has since fallen along with the rest of the REIT category with the market pricing in headwinds from higher rates and competition from Treasury Bonds and High Yield savings.

As shown below, DEA stock has fallen by 39% over the past 12 months, with much of the decline happening over the past 12 months. In this piece, I discuss why value and income investors may want to consider a position in DEA at its current heavily discounted price with the market already having baked in plenty of risks, so let’s get started!

{kind=link}

Why DEA?

Easterly Government Properties is a self-managed REIT that’s the largest owner and lessor of Class A commercial properties leased to the U.S. Government. As one would expect, DEA comes with higher assuredness of rent collection compared virtually all other REITs considering that the government is highly unlikely to default on its rental obligations.

DEA’s portfolio carries a high leased rate of 98% with a weighted average remaining lease term of 10.4 years, which is on the long-side for the REIT industry and is on par with that of net lease REITs such as Realty Income Corp. (O). Its portfolio of 89 properties is also relatively new, with a weighted average age (based on net rentable square feet) of 14 years.

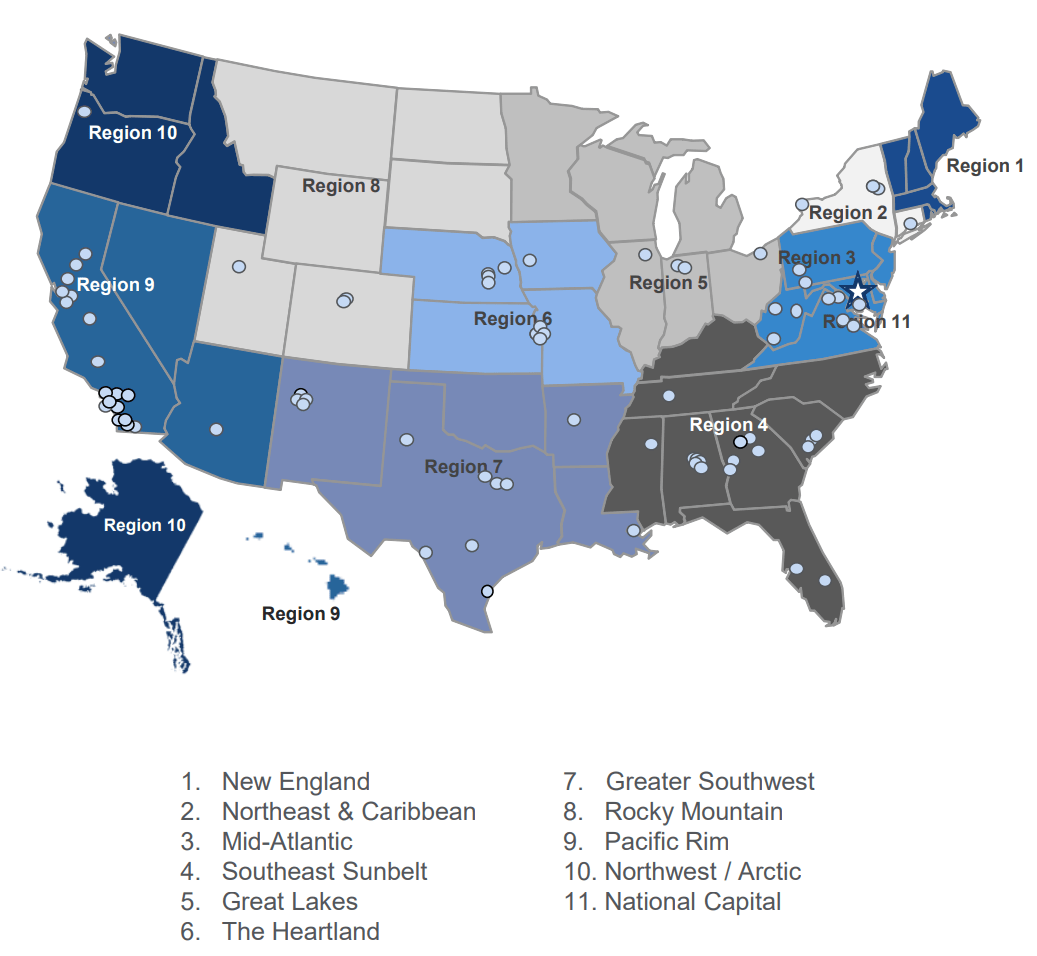

Office properties make up half (51%) of DEA’s annual lease income, with VA Outpatient (26%), Lab (10%), Courthouse (5%) and Other (8%) making up the rest. DEA’s property locations are also diversified by geography with higher concentration in the Washington D.C. area (understandably) and in regions with high population density and skilled workforces along the West Coast and Sunbelt regions of the U.S., as shown below.

{kind=link}

While DEA’s high exposure to office buildings may give some investors pause, it’s worth considering that 87% of these facilities are deemed mission critical, build-to-suit, and leased to important government agencies such as FBI Field Offices, DOD Command Center, DEA regional offices, and National Weather facilities.

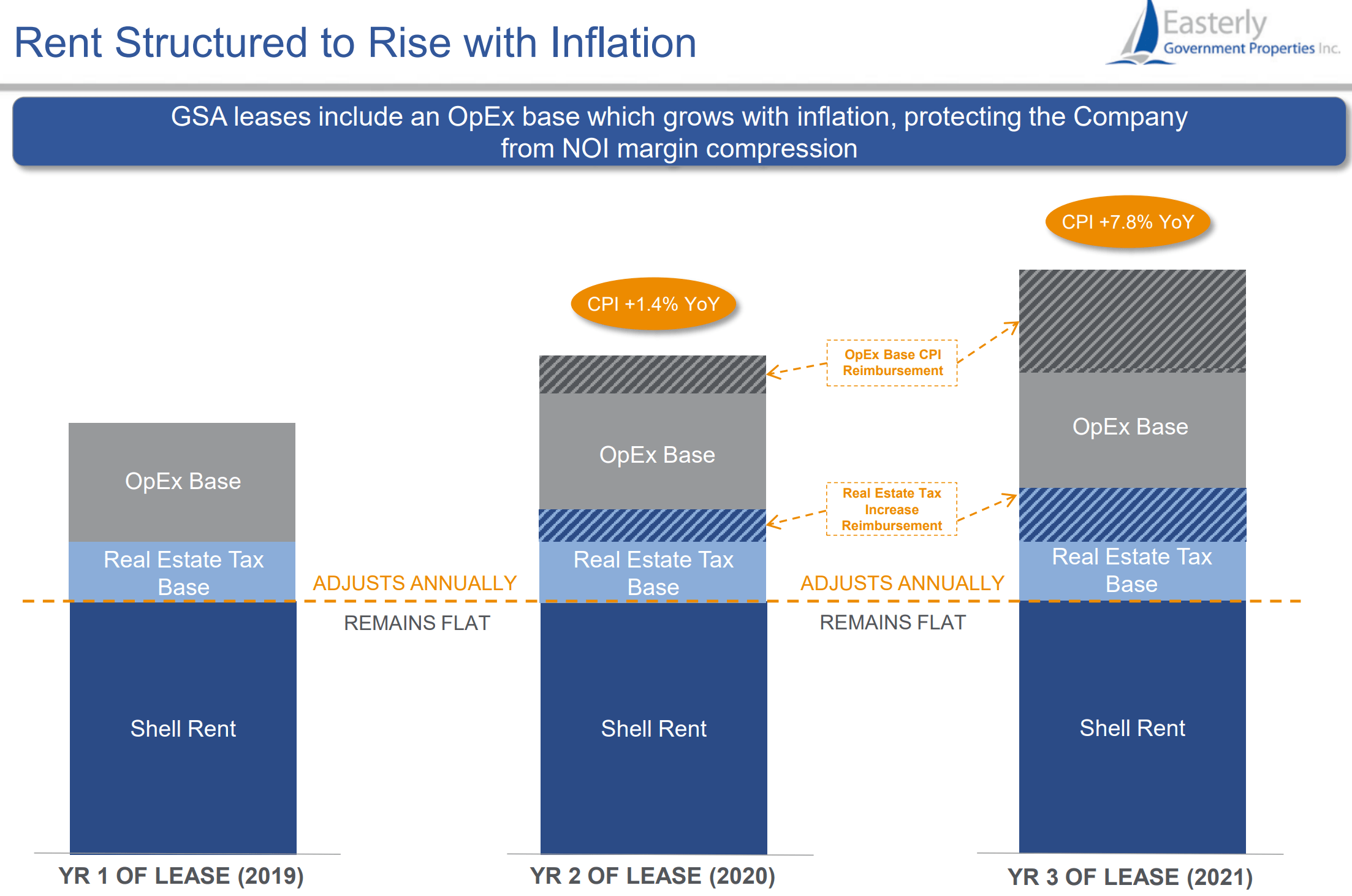

Other concerns around DEA may stem from its presumed ‘bond proxy’ nature of real estate holdings. However, it’s worth considering the nature of GSA leases which grow with inflation, thereby enabling DEA to maintain a healthy NOI margin. As shown in the 2019 through 2021 example below, DEA’s lease structure has enabled Operating Expense Base CPI reimbursement growth to adjust the 1.4% and 7.8% YoY CPI growth in 2020 and 2021, respectively.

{kind=link}

Recent headwinds include a lower FFO/share during the second quarter, with it coming in at $0.29, which sits $0.04 below where it was in the prior year period. However, this shouldn’t come as a surprise for investors and shouldn’t be the reason for why the stock dropped by so much this year.

That’s because management fully communicated its full-year Core FFO/share guidance in the range of $1.12 to $1.15 back in February of this year, and recently tightened its guidance range to $1.13 to $1.15 for this year. The decline in Core FFO/share from $1.28 last year is due more to a timing issue, related to the closing of DEA’s VA-Corpus Christi building sale, and investments into its development pipeline.

Looking ahead to Q3 results and beyond, I would expect Core FFO/share to be around $0.29 for the next two quarters. Potential upside includes the deployment of proceeds from equity offerings (at share prices above $20) earlier this year, which netted the company $89.1 million. This could go a long way in driving growth considering that DEA carries an equity market cap of just $1.11 billion.

Risks to DEA include a higher payout ratio than I’d like to see of 93%, and DEA has kept its dividend flat since 2022. DEA also has a net debt to EBITDA ratio of 7.0x, which sits higher than the 6.0x level that’s generally considered safe by ratings agencies. While the higher leverage may be ok for a lower interest environment, considering the durability of DEA’s lease contracts with the U.S. government, risks are elevated for the current higher interest rate environment. DEA carried a weighted average interest rate just 3.88% on debt as of the end of June, and that could go higher as debt rolls over (DEA has a weighted average debt maturity of 5.2 years).

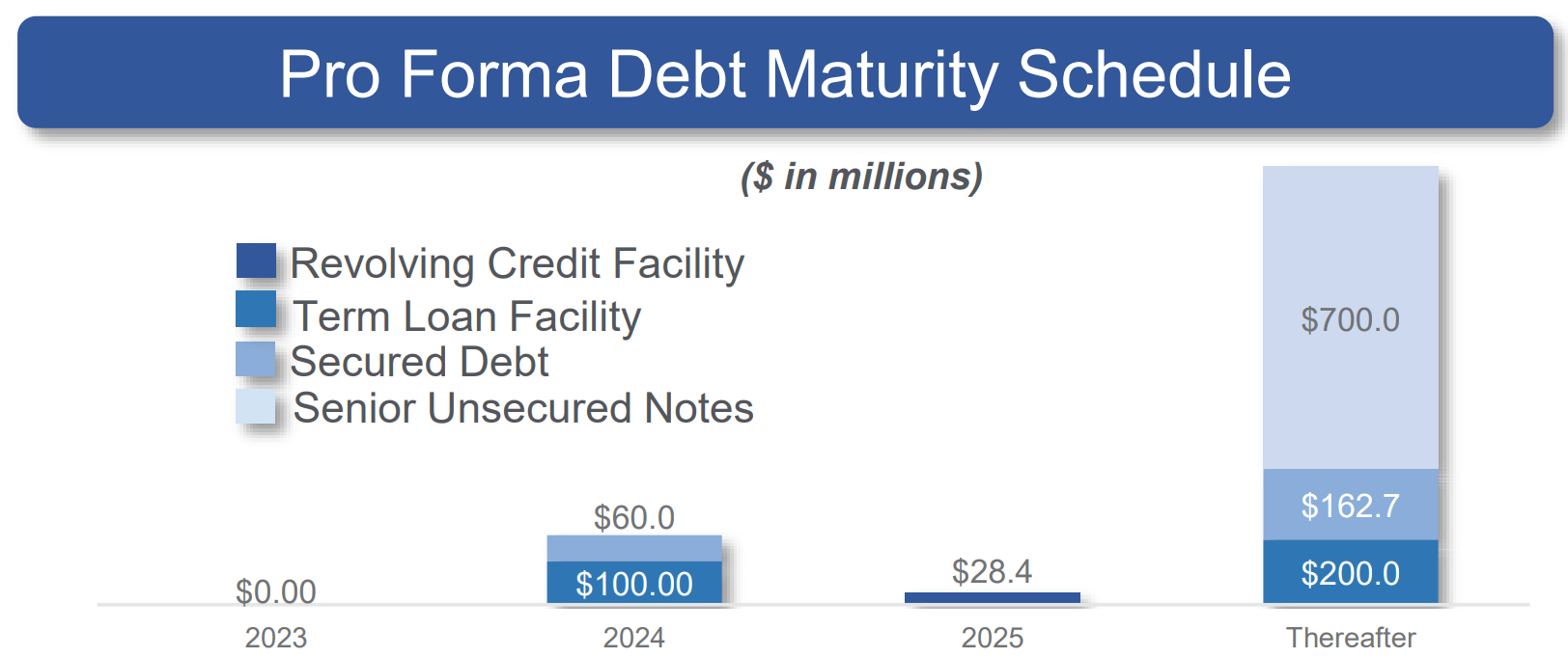

Nonetheless, DEA carries a healthy cash interest coverage ratio of 3.6x and 98% of its debt is held at fixed rates. As shown below, DEA has no debt maturities this year, and limited maturities over the next two years.

{kind=link}

Nonetheless, it appears that the market has already baked in plenty of risks for DEA with the stock trading at $10.46, a forward P/FFO of 9.2, and a 10.1% dividend yield. If DEA cuts the dividend to get to a 70% payout ratio (and that’s purely hypothetical), it would still be yielding an appealing 7.6% at the current share price. The 70% payout ratio is based on the Core FFO/share expectation of $1.14 for the full year, and an $0.80 annualized dividend rate.

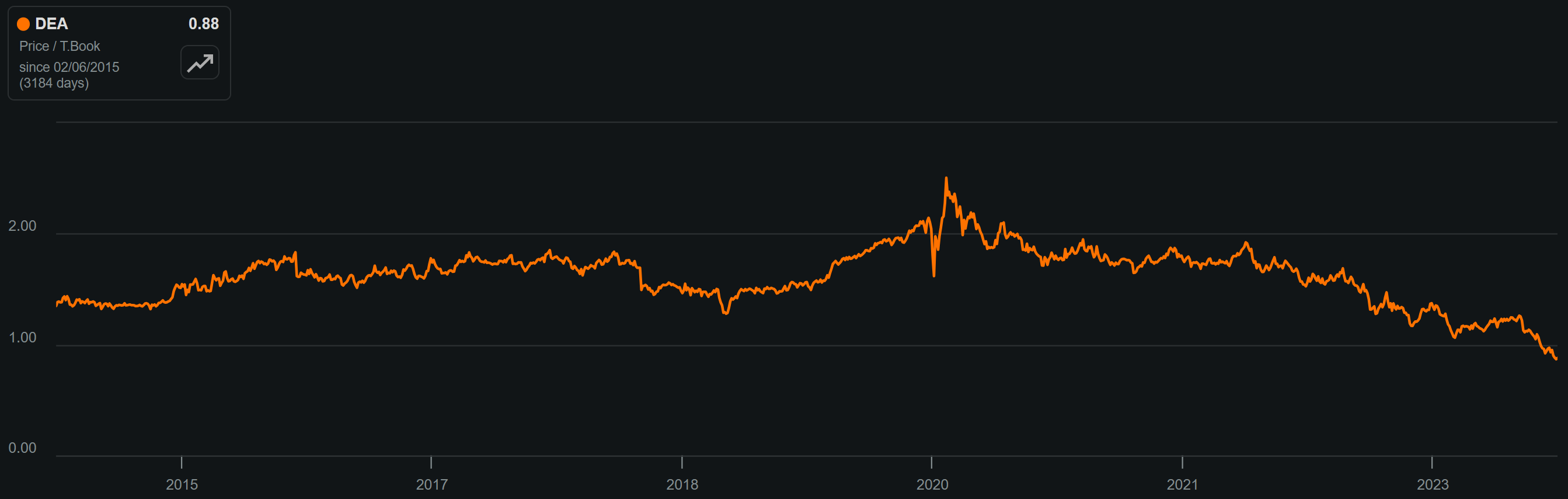

DEA also appears to be undervalued based on price-to-tangible book value. While I don’t typically use this metric to value REITs, I believe it’s worth evaluating given the material share price downturn the stock has suffered. Tangible book value is more conservative than book value, as it excludes goodwill and represents liquidation value of assets in a worst case bankruptcy scenario.

While I don’t believe DEA is going bankrupt, the following chart does illustrate how cheap the shares have gotten. As shown below, DEA trades at a price-to-tangible book value of just 0.88x, sitting at its lowest point in its history as a public company.

{kind=link}

Investor Takeaway

As the largest owner and lessor of mission-critical commercial properties leased to the U.S. Government, DEA offers investors high assurance of rent collection for all economic environments. Additionally, DEA's lease structure allows for growth with inflation, which comes in handy in these years and it continues to perform in-line with what management guided for earlier this year. While higher interest rates give rise to added uncertainty, I believe these concerns are more than priced into the stock with it trading significantly below book value. As such, value and income investors may find DEA to be appealing at its current heavily discounted price.

For further details see:

10%-Yielding Easterly Government Is Too Cheap To Ignore