VNORP - 10% Yielding REITs That I Am Buying

2023-03-28 08:05:00 ET

Summary

- Some REIT preferred shares now yield over 10%.

- Not only that, but they also offer 50-100% upside potential to par.

- We highlight a few of our Top Picks.

The big story over the past several months is that inflation began to cool down:

This is very good news for preferred stocks ( PFF ) because they don't enjoy the same level of inflation protection as common stocks.

Preferred stock investors earn a fixed yield and their par value is capped, generally at $25, so they don't participate in the long-term growth of the company.

This is a problem during times of high inflation because your total return may not be enough to make up for the inflation.

A 6% yield can rapidly turn into a negative real return once you account for taxes and inflation if the underlying value of the investment isn't growing.

This is why we avoided most preferred stocks over the past year.

But this is now changing. Inflation is coming back down, and many REIT preferred stocks remain discounted and offer exceptionally high yields and upside potential.

We think that they are particularly attractive today because:

- Inflation now appears to be cooling down

- Eventually, we expect interest rates to also return to lower levels

- This could be the catalyst that will push preferred stocks higher

- In a coming recession, they offer safer income and downside protection

- And so the overall risk-to-reward is compelling for today's world

Our preferred equity investments represent right around 18% of our Retirement Portfolio, and in today's article, we will highlight two of our Top Picks. They yield 9-11%, or right around 10% on average. They allow us to boost our average portfolio yield and help us achieve our main portfolio objective, which is to maximize safe income.

Vornado Realty Trust Series M Preferred Shares ( VNO.PM )

Vornado Realty Trust ( VNO ) is an office REIT that focuses primarily on NYC. It recently made headlines because it cut its common dividend by nearly 30%:

Seeking Alpha

{kind=link}

{kind=link}

I am not interested in its common equity at this time because there is too much uncertainty. As we have discussed in previous articles, the office sector is going through severe disruption and NYC is particularly heavily impacted .

The same is true for SL Green ( SLG ) and Alexander's ( ALX ).

However, VNO's preferred equity ( VNO.PM ) has become quite attractive lately.

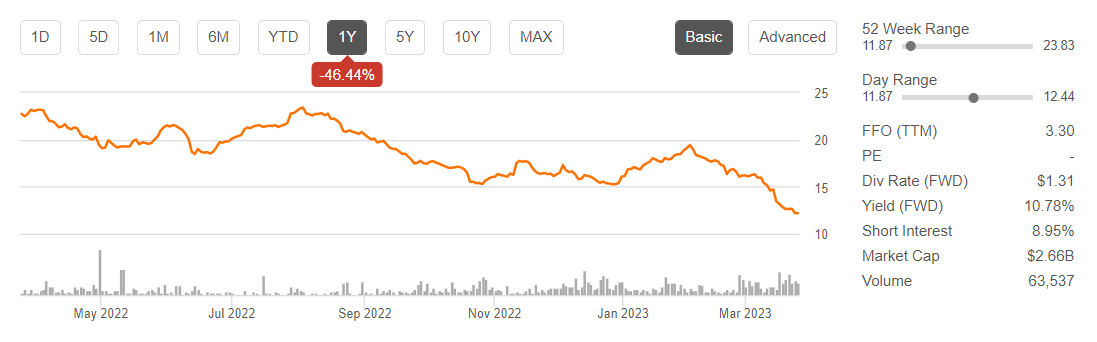

It is down 46% over the past year and as a result, it is now offered at $12 per share, representing a steep ~50% discount to its par value:

{kind=link}

The preferred shares now offer an ~11% dividend yield and eventually, as the shares return to par value (which is where they traded just a year ago), they will also appreciate by ~100% from here.

That's quite attractive coming from the preferred shares of a high-quality REIT.

Yes, the office sector in NYC is going through tough times and there is great uncertainty affecting the common equity. But otherwise, this is a great REIT:

- It owns Class A office buildings, which benefit from the flight to quality. Last year, its comparable FFO was up 10%, and the management noted at a conference that they expect their performance to be among the strongest in their sector in the coming 2-3 years. Since then, interest rates have risen and the economy has deteriorated, but this is just to show that these are good assets that will remain desirable in the long run.

- It is not fully exposed to office space. Today, most of its office buildings have a mixed-use component and as a result, about 20% of its NOI comes from retail space. Moreover, it is currently building the Penn District, a major mixed-use development projects, which upon completion will represent about 1/3 of its NOI. They own 10,000 square feet of space there and expect to expand it to 15-18,000 while growing average rents from $65 to $100+ per square foot. The below market rents also provide margin of safety in a coming recession.

- It has an investment grade rated balance sheet with a BBB- rating and $3.4 billion of liquidity, including $1.5 billion in cash and $1.9 undrawn on its credit facilities. That's very significant for a company with a $4.5 billion market cap. They could pay off the debt maturities many years ahead, and they could also delay their development project if needed.

- The management has historically acted in a shareholder-friendly way. The recent dividend cut was already mentioned in late 2022, but most investors appear to have missed it: "Our policy is to payout dividends equal to our taxable income. We now expect our taxable income to be lower in 2023. We will not have income from 220 Central Park South. We assume no asset sales, and we are budgeting to the interest rate yield curve. As such, our Board of Trustees plans to right-size our dividend in 2023 commensurate with our protection of taxable - projection of taxable income. This will allow us to retain more cash."

The dividend cut is actually a very good thing for the preferred shareholders because it will allow them to maintain an even safer balance sheet.

We think that the preferred dividend was safe already before the cut, and it is now even safer following it.

Earning a sustainable 11% dividend yield is attractive on its own, but we think that there is an upside as well.

I want to be clear that I don't expect VNO.PM to suddenly return to par, which would unlock a 100% upside from here.

I think that it will take time, potentially years. But eventually, as interest rates are cut again to stimulate the economy in a coming recession, I would expect these preferred shares to return closer to par value. Even getting just to $20 would result in a 67% upside, and from there, the shares would still provide an attractive 7.5% yield and be priced at a 20% discount to par.

That's a great risk-to-reward in today's uncertain world, especially for an income-oriented investor who needs a high yield.

EPR Properties Series G Preferred Shares ( EPR.PG )

Just like VNO, EPR Properties ( EPR ) is a REIT that's a bit riskier than average. It owns mainly movie theaters, water parks, ski resorts, and other experiential properties:

EPR Properties

EPR Properties

EPR Properties

Those properties suffered greatly from the pandemic, but most of them have strongly recovered since then.

These properties are leased on a triple-net basis with an average remaining term of 14 years, annual rent hikes of nearly 2%, and no landlord responsibilities, which should provide steady and predictable cash flow as long as its tenants can turn a profit.

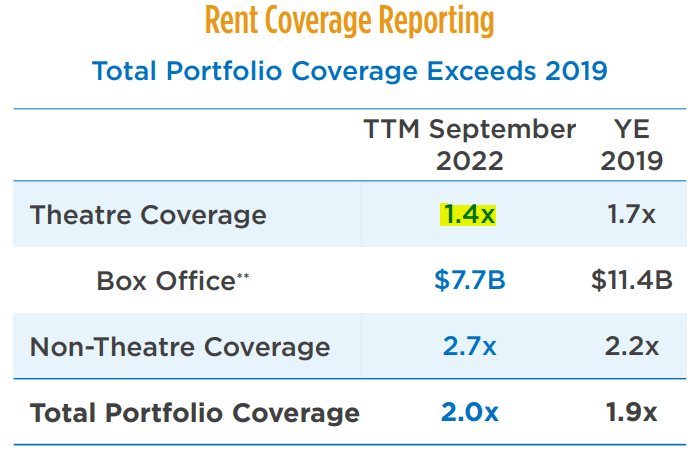

Today, the rent coverage ratio of its non-movie theater tenants, which make up about 75% of its NAV, is highly profitable with a 2.7x rent coverage ratio. This is even higher than before the pandemic. Their recovery has been phenomenal. People are clearly seeking experiences in the post-Covid world, and it benefits these properties.

But its movie theaters are today still struggling. The movie slate has taken some time to recover as studios were experiencing different movie monetization strategies, including direct-to-streaming.

As such, the box office is today still quite a bit below pre-pandemic levels, and so is the rent coverage of EPR's properties:

{kind=link}

But now studios are returning to theaters, and so we think that the box office will continue its recovery in 2023. Paramount ( PARA ), Disney ( DIS ), and even Amazon ( AMZN ) have realized that movie theaters remain the best option to monetize new blockbusters (what a surprise!), and they have a lot of big movies under production.

Ultimately, this should lead to a continued recovery in the box office and rent coverage ratios and should allow most theaters to keep paying their rent to EPR, even if they have to go through a temporary bankruptcy to restructure their finances. EPR owns some of the most productive theaters in the nation

Therefore, we are bullish on the long-term prospects of the common equity, but I would totally understand if it is too risky for some of you. AMC ( AMC ) type tenants are risky, and the common could well go lower before it rises higher.

That's why I also like its preferred equity as a more conservative investment.

It is higher on the capital stack and enjoys good margin of safety because EPR has a strong BBB- investment grade rated balance sheet with ~50% of common equity as an additional buffer for the preferred.

EPR Properties

Yet, today, it is priced at a 33% discount to its par value, and it yields nearly 9% as a result of its low valuation. I think that eventually, the shares will return to par, unlocking up to 50% upside, and you get paid handsomely to wait.

That's a great risk-to-reward if you ask me.

For further details see:

10% Yielding REITs That I Am Buying