FSK - 14% Yield 20% Below Book Value - FS KKR Is A BDC Gem

2023-10-11 10:44:39 ET

Summary

- FS KKR Capital Corp trades at a 20% discount to its book value, offering a high annualized yield of 14.4% and showcasing resilience in an elevated interest rate environment.

- Potential reasons for the discount include historical poor performance, high leverage, and lack of dividend growth, but recent strategic shifts and strong financials have debunked these concerns.

- FSK presents an attractive buying opportunity at its current price. However, caution is advised due to potential economic headwinds.

Introduction

The other day, I wrote an article covering the business development company ("BDC") Hercules Capital (HTGC). Hercules is an (historically) outperforming BDC, which trades 50% above its book value as investors reward the company's top-tier portfolio, which goes well beyond traditional debt financing.

While HTGC has a lot of fans, it seems that most aren't willing to buy a BDC that trades at a significant premium to its book value.

In this article, I'll dive into a BDC giant I covered for the first time on May 18 in an article titled FS KKR: The Best 15% Yield I've Seen So Far .

FS KKR Capital Corp (FSK) has returned 10% since then! With 6% coming from its dividend, which shows the tremendous power of consistent dividend payers with very elevated yields.

Even after that surge, FS KKR is still yielding 14% and trading 20% below its book value.

Having said all of this, let's dive into the details!

A Titan Trading At An Unusual Discount

FS KKR is a non-diversified, closed-end management investment company regulated as a business development company under the Investment Company Act of 1940.

As I wrote in a prior article (emphasis added):

Business development companies are closed-end investment companies that serve the purpose of investing in small and emerging businesses , as well as financially distressed enterprises .

By investing in BDCs, individuals gain exposure to a diverse range of assets within private companies' capital structure, including senior secured and subordinated debt and preferred and common equity.

BDCs face certain investment restrictions and primarily allocate their funds to eligible portfolio companies. Typically, these companies include small businesses in the early stages of development or financially troubled enterprises lacking access to conventional financing options. With traditional lenders, such as banks, burdened by increased regulatory requirements, they struggle to provide loans to small and mid-sized businesses.

In other words, BDCs benefit from great yields as they invest in companies that usually don't have access to the cheaper funding sources that the large blue chip companies on the stock market may have.

This means that elevated yields also come with elevated risks.

Having said that, the book value of a BDC is essentially the total value of the company's assets minus its liabilities (divided by the number of outstanding shares, in the case of per-share numbers). It represents the theoretical value of the company based on its financial statements.

Some top-tier BDCs like Hercules and Main Street Capital ( MAIN ) trade well above their book value. FSK trades roughly 20% below its book value - it also has a higher yield, which is related to its valuation.

There are a few things that can cause this. In general, reasons like economic turmoil could lead to a discount. However, we need to look for reasons that explain a relative discount. After all, some large BDCs trade at a premium!

I believe there are three reasons that could explain why some BDCs trade at a discount.

- Poor Investment Performance : If the BDC's portfolio underperforms or faces a high level of non-performing loans or investments, investors may be reluctant to pay a premium for shares, causing the BDC to trade at a discount to book value.

- High Leverage : BDCs that have a high level of leverage may trade at a discount to book value because investors perceive higher risk due to the potential impact of debt on the company's financial stability.

- Lack of Dividend Growth : If a BDC cuts or fails to increase its dividends, it may disappoint income-seeking investors and trade at a lower premium or a discount.

In other words, poor historical performance, elevated risks, and disappointing dividend growth could all be reasons for people to opt for other BDCs. And who can blame them? After all, the market has many great BDCs.

But guess what?

FSK is one of them!

FSK Is Much Better Than Its Valuation Suggests

FSK shares have returned 48% over the past ten years. This is a very poor performance, as even the BDC ETF ( BIZD ) has returned 90%.

I'm bringing this up because FSK's poor performance prior to the pandemic has caused its longer-term underperformance.

Since 2018, FSK is a whole new company. In 2018, the company merged six separate BDCs, including the merger between FS Investment Corporation and Corporate Capital Trust.

In 2021, the company acquired FS KKR Capital Corp. II and entered into a new investment advisory agreement with FS/KKR Advisor, LLC.

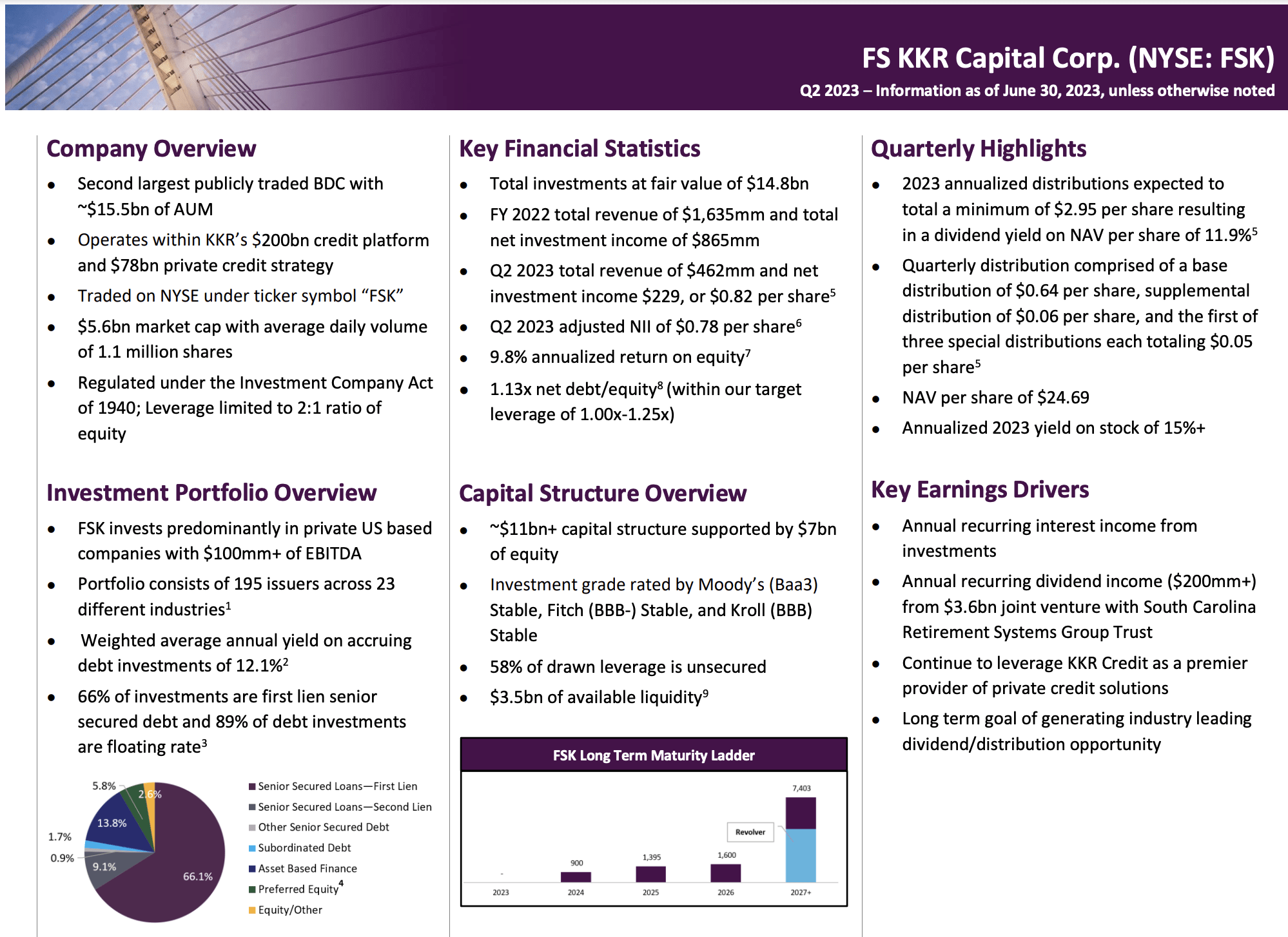

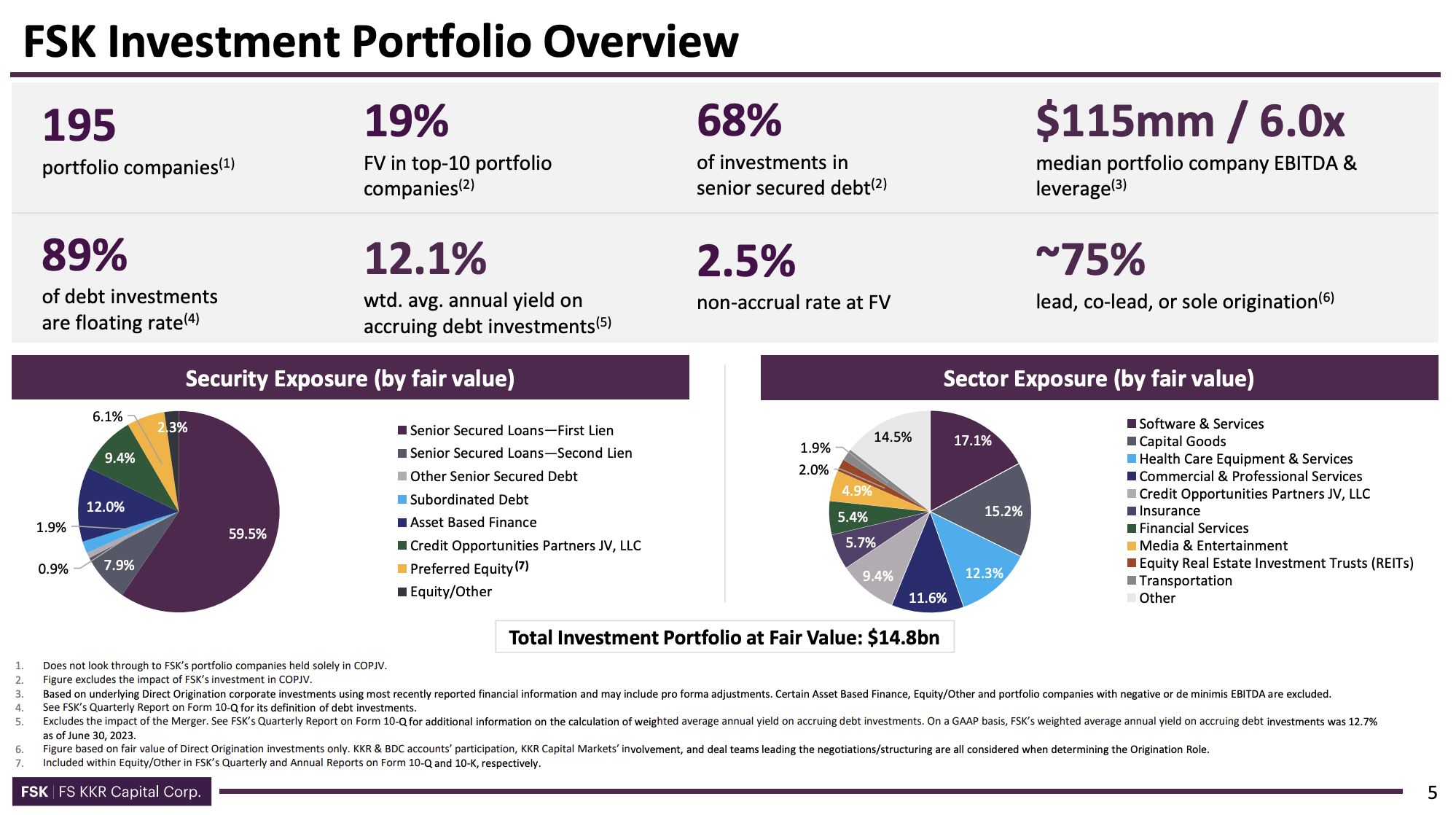

Now, FSK is the second-largest BDC, with close to $16 billion in assets under management. It benefits from KKR's ( KKR ) $200 billion credit platform, and it has a portfolio of 195 issuers in 23 industries.

Over the past three years, it has outperformed its peers.

To minimize risks, the company only invests in companies with more than $100 million in annual EBITDA. 66% of its investments are first-lien senior secured debt. 89% of its debt investments have a floating rate. This is common in the industry, as it allows BDCs to increase their income when interest rates (in general) are rising.

{kind=link}

Having said that, in this environment, FSK is doing very well.

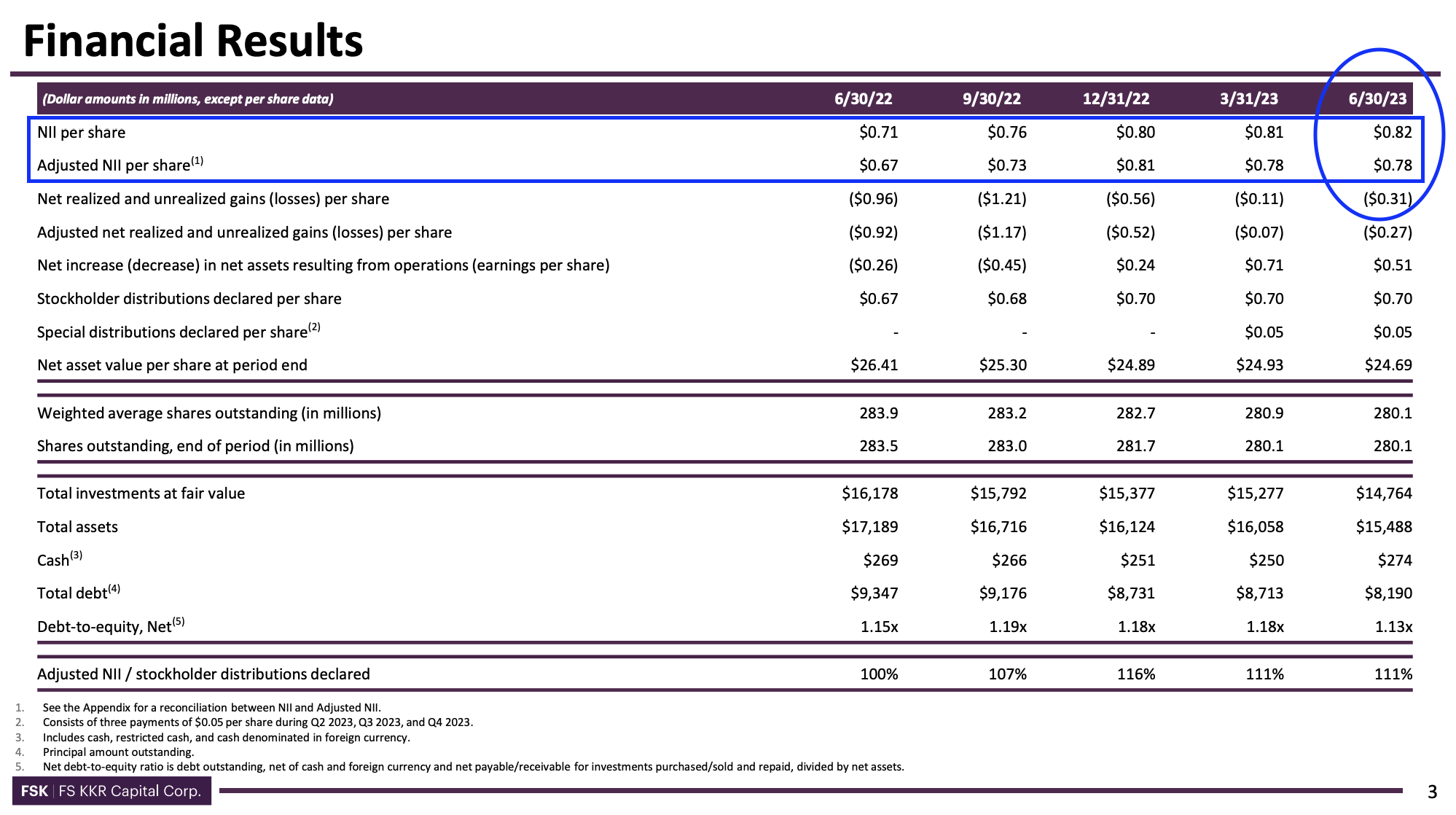

The company generated net investment income of $0.82 per share and adjusted net investment income of $0.78 per share during 2Q23, outperforming the public guidance of approximately $0.78 and $0.75 per share, respectively.

I highlighted these numbers in the somewhat complex table below.

{kind=link}

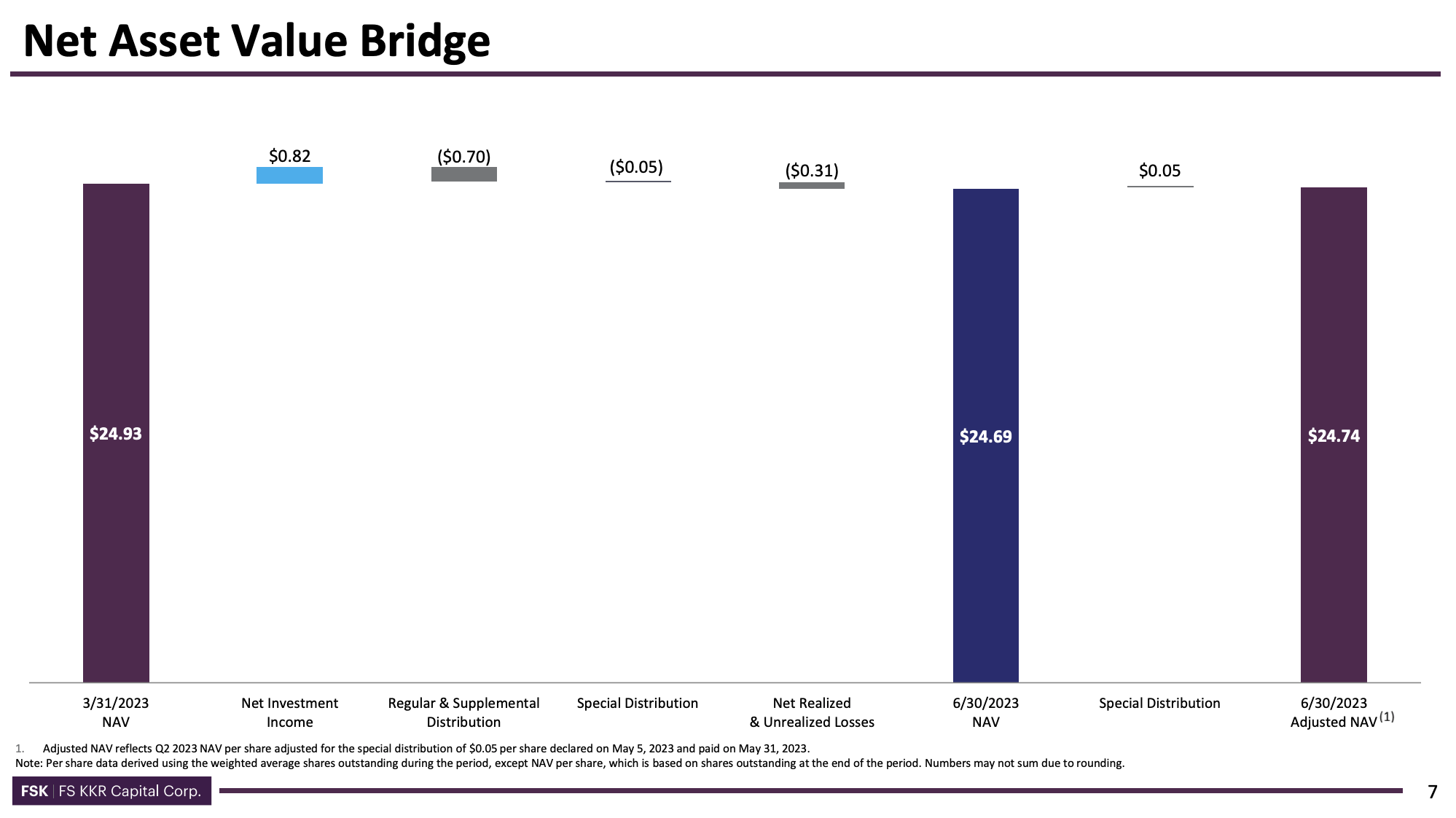

The net asset value per share as of June 30 stood at $24.69.That's before the special dividend.

{kind=link}

Speaking of dividends, the company declared a third-quarter regular quarterly distribution of $0.70 per share, comprising a base distribution of $0.64 per share and a supplemental distribution of $0.06 per share.

The expected quarterly supplemental distribution was reiterated at a minimum of $0.06 per share throughout 2023, sustaining a quarterly distribution of at least $0.70 per share.

This translates to an annualized yield of 14.4%!

In the second quarter, the dividend was protected by an adjusted net interest income coverage ratio of 111%.

Having said that, the company commented on the economy during the 2Q23 earnings call.

FSK highlighted the resilience of the labor market and continued strong consumer spending in the first half of 2023, which has led to the belief that the economy is unlikely to slow down dramatically.

However, the company cautioned that near-term inflation is expected to remain elevated, and they anticipate a persistent higher interest rate environment. As most of my regular readers know, I agree with these comments, as I also believe that inflation is sticky.

As long as FSK engages in (relatively) safe investments with elevated yields, it will be fine in this environment.

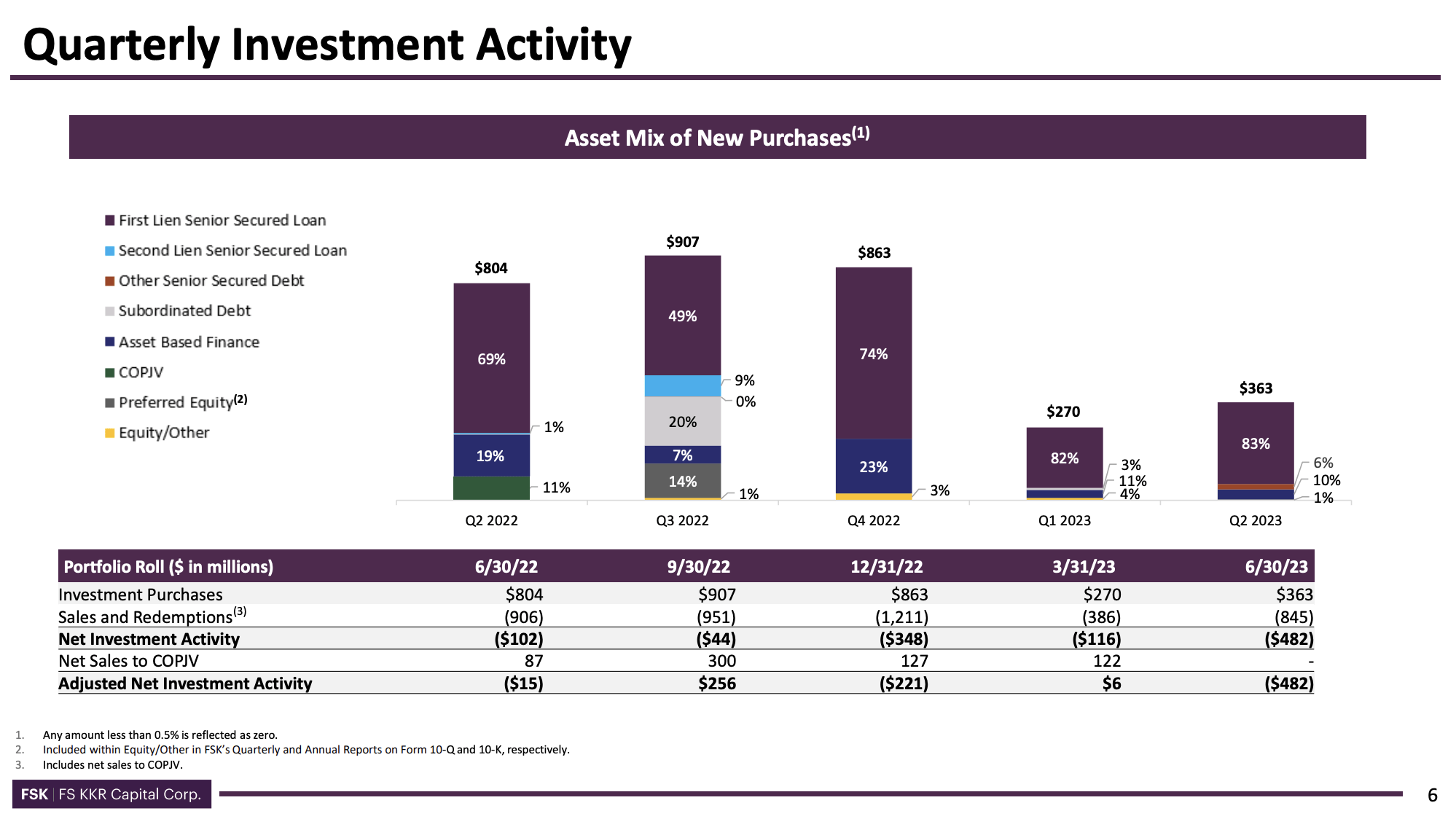

During the second quarter, they originated $363 million in new investments, primarily focused on add-on financings for existing portfolio companies and long-term relationships. 83% of this capital was from first-lien senior debt, emphasizing the company's focus on risk minimization.

{kind=link}

Additionally, the company sold approximately $500 million of lower-yielding investments to a third party, aiming to increase investment capacity due to the accelerating M&A environment.

As a result, the fair value of the investment portfolio stood at $14.8 billion, comprising 195 portfolio companies, down from $15.3 billion and 189 portfolio companies in the previous quarter, primarily due to lower-yielding asset sales.

{kind=link}

The company also saw an improvement in the quality of its portfolio.

As of June 30, 2023, non-accruals improved to 4.8% of the portfolio on a cost basis and 2.5% on a fair value basis, compared to 5.5% on a cost basis and 2.7% on a fair value basis as of March 31, 2023.

Non-accruals related to assets originated by KKR Credit and the FS KKR Advisor were 2.2% on a cost basis and 0.6% on a fair value basis.

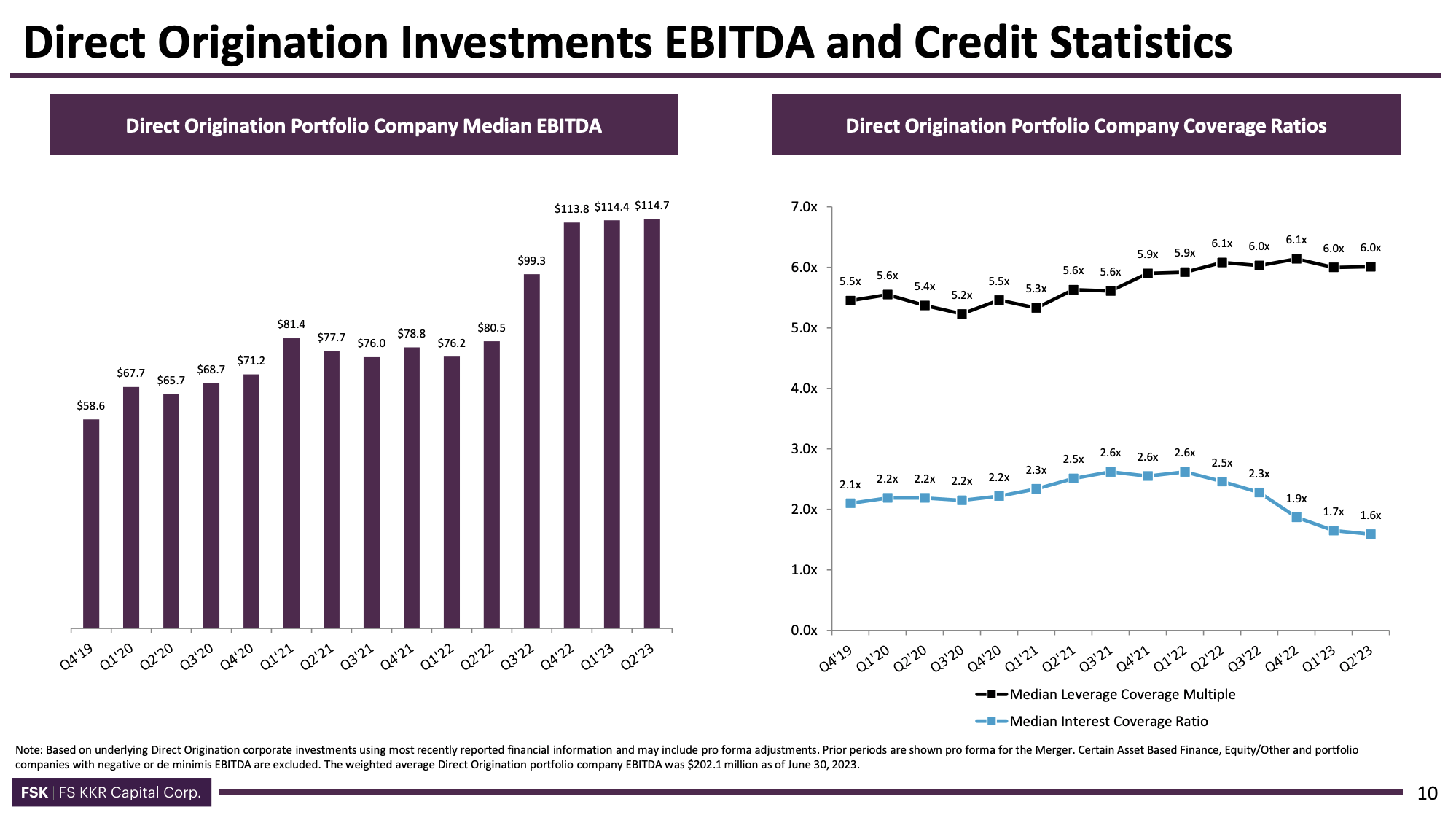

While the median interest coverage ratio has dropped consistently since 1Q22 (when rates started to rise), the company's portfolio remains in a good spot to cover elevated interest expenses. It also helps that companies have kept a steady leverage ratio during this period.

{kind=link}

Not only does FSK have a strong portfolio, but it also has a strong balance sheet itself.

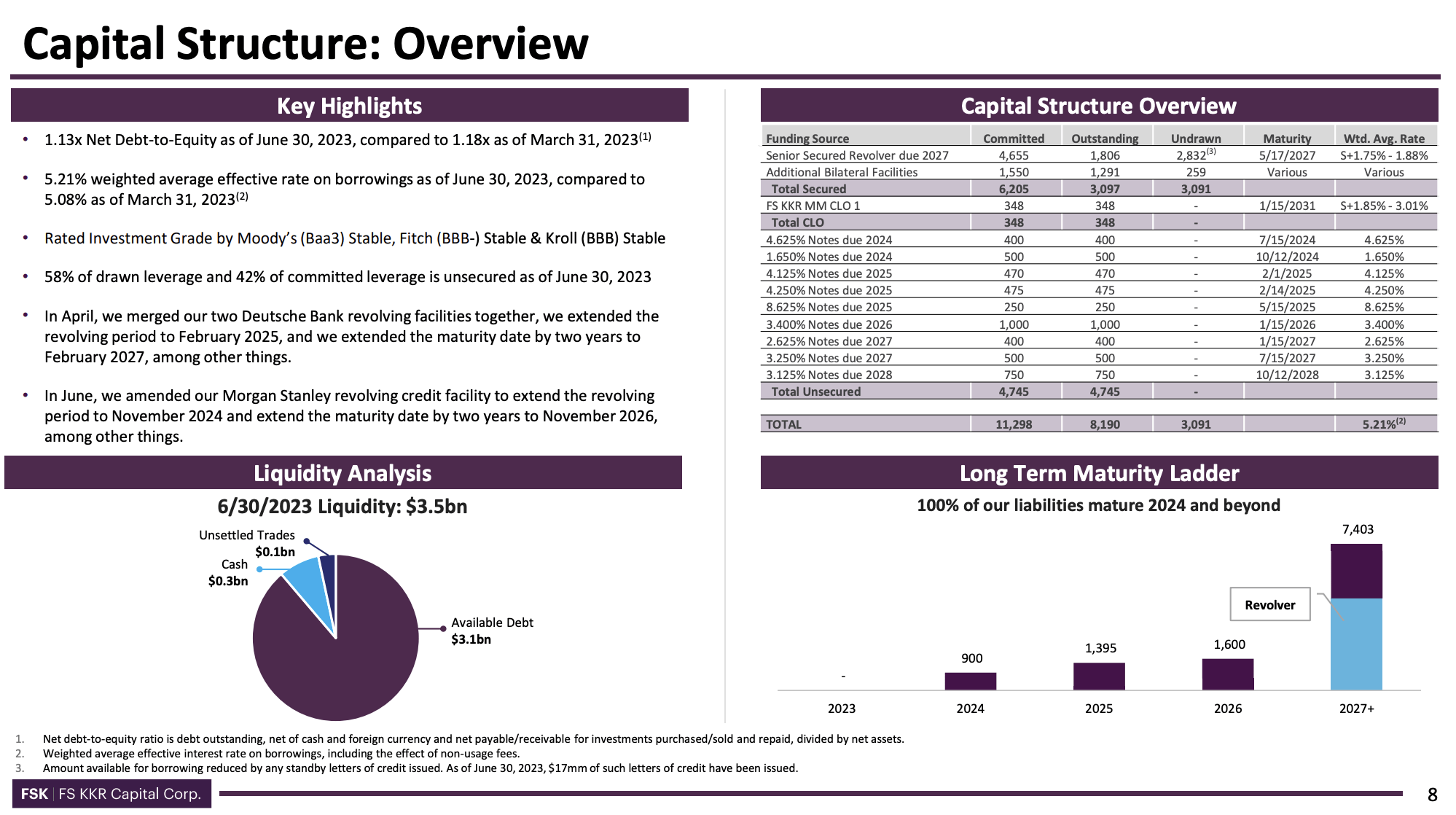

As of June 30, 2023, the gross and net debt to equity levels were disclosed as 118% and 113%, respectively, a notable decrease from the previous quarter. In the prior quarter, these numbers were 125% and 118%, respectively.

This reduction was attributed to the sale of approximately $500 million of assets to a third party during the second quarter. These strategic asset sales played a crucial role in reshaping the financial structure of the organization.

Moreover, the effective weighted average cost of debt remained steady at 5.2%.

The available liquidity increased to $3.5 billion at the end of the second quarter, a substantial rise from the $3 billion reported at the end of the first quarter. This surge in available liquidity indicates enhanced financial flexibility and potential for investment activities.

{kind=link}

The company has no debt maturities in 2023 and less than $1 billion in maturing debt in 2024.

The Verdict

FSK is trading below its book value. Earlier in this article, I gave three potential reasons that could have caused this:

- Poor Investment Performance

- High Leverage

- Lack of Dividend Growth

I believe that all of these have been debunked. The company does not have a poor performance anymore. The new and improved FSK is a top-tier BDC with a strong portfolio that comes with high yields. It has a well-protected dividend and a portfolio with healthy financials - even in this environment.

While I wouldn't make the case that FSK should trade way above its book value, I think it's too cheap.

The current consensus price target is $21.70. This is 12% above the current price.

I agree with that and will maintain a Buy rating.

However, and this is important, I have given other strong performers like Hercules Capital a Hold rating despite their stellar performance.

The Buy rating for FSK is based on its strong performance and its attractive valuation.

I believe that elevated economic risks should not be underestimated.

As such, I do NOT advise anyone to aggressively buy BDCs. We could enter a period of stagflation, which could hurt the stability of BDC portfolios and provide us with some correction opportunities.

So, if you decide that FSK (or any BDC) is right for you, please be careful. Start small and add gradually over time.

Also, please be aware of the risks that come with buying BDCs. As much fun as the elevated yields are, risks are higher compared to some of the blue chips you may hold in your portfolio.

Takeaway

In this article, I explored the intriguing case of FS KKR Capital Corp, a business development company that's been flying under the radar for many investors.

What makes FSK particularly interesting is that it's trading at a substantial discount, despite its impressive performance.

First, we dissected the reasons why some BDCs trade at a discount, considering factors like poor historical performance, high leverage, and stagnant dividend growth. FSK has debunked these concerns with its (somewhat) recent transformation into a top-tier BDC.

With a strong portfolio, well-protected dividends, and solid financials even in today's economic climate, FSK is a gem. While I wouldn't make the case that an elevated premium valuation is warranted, I do believe it's undervalued.

The consensus price target supports this view, presenting a 12% upside potential.

However, we must remember that BDCs, including FSK, come with higher risks compared to conventional blue-chip investments.

With potential economic uncertainties ahead, caution is advisable.

For further details see:

14% Yield, 20% Below Book Value - FS KKR Is A BDC Gem