SRCE - 1st Source Corporation: Superb Dividend Growth Potential But Not At This Price

2023-11-01 05:28:12 ET

Summary

- 1st Source Corporation announced record-breaking net income numbers in its most recent quarterly report.

- Despite this, the stock is trading substantially above its book value and management has a bleak future outlook.

- The financial sector is going through cyclical swings, making it a risky time to invest in the stock.

1st Source Corporation (SRCE) is an excellent dividend compounder and announced record-breaking net income numbers in its most recent quarterly report. Despite this development, I give it a 'Hold' rating. This recommendation comes amid it trading substantially above its book value, management's bleak future outlook, and the cyclical swings the financials sectors are going through at the time of writing.

Aside from some (relatively minor) valuation concerns, I think SRCE is in an excellent position regarding its fundamentals and should be considered in every dividend investor's portfolio.

Company Overview

1st Source Corporation is a financial services company founded in 1863 and headquartered in South Bend, Indiana. It primarily focuses on providing banking and financial solutions to individuals and businesses.

As a regional community bank, a unique feature of 1st Source is its specialized lending services, which include aircraft and auto fleet financing. The bank operates over 75 banking centers, primarily in Indiana and Michigan in the United States.

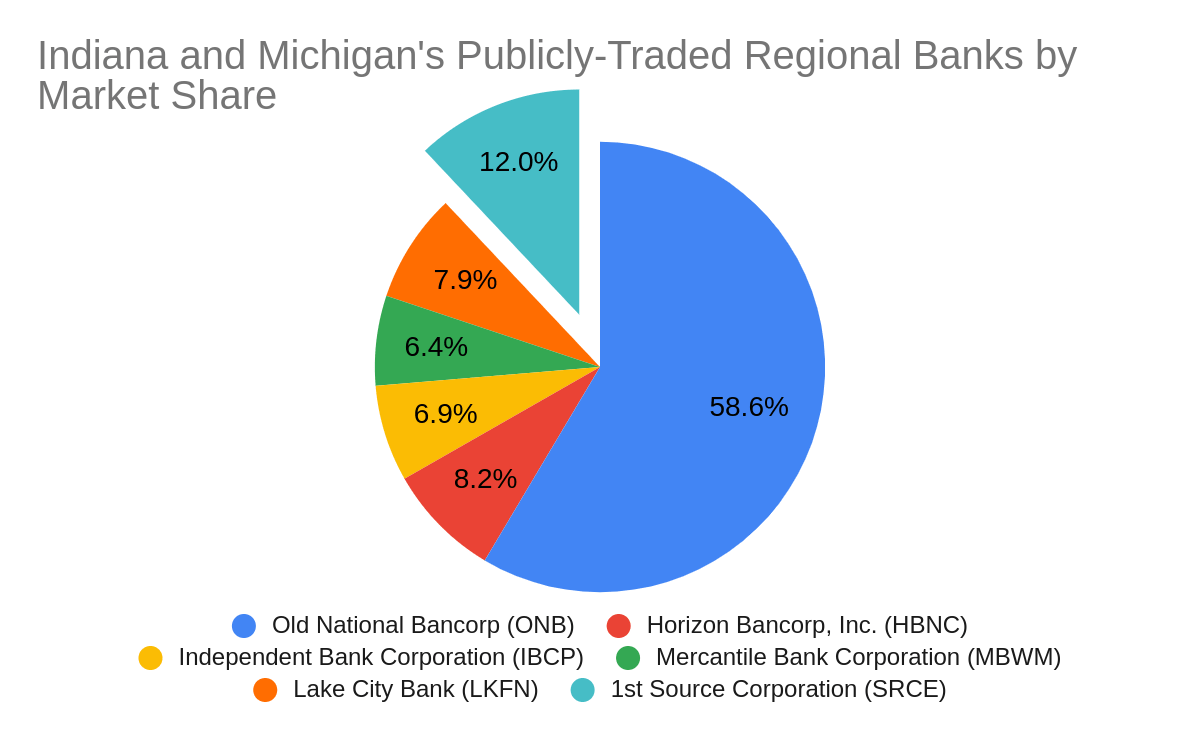

Some of 1st Source's publicly traded competitors in the Indiana and Michigan region include the following:

- Old National Bancorp ( ONB )

- Horizon Bancorp ( HBNC )

- Independent Bank Corporation ( IBCP )

- Mercantile Bank Corporation ( MBWM )

- Lake City Bank ( LKFN )

Calculated using total revenue numbers from 2022, SRCE has a sizable presence in the region by market share at around 12%. It's the second-largest regional bank, and on average, its share is 1.5 times larger than its equivalent competitors. Still, its market share is dwarfed by ONB, which commands a 58.6% stake.

{kind=link}

| Bank |

| 2022 Total Revenue (Thousands) |

| Old National Bancorp ( ONB ) |

| 1,727,715 |

| Horizon Bancorp, Inc. ( HBNC ) |

| 241,558 |

| Independent Bank Corporation ( IBCP ) |

| 204,571 |

| Mercantile Bank Corporation ( MBWM ) |

| 190,321 |

| Lake City Bank ( LKFN ) |

| 231,923 |

| 1st Source Corporation ( SRCE ) |

| 354,731 |

With the exclusion of ONB, 1st Source's revenue growth over the last ten years has been about average at 5.35%, keeping up with its peers.

One point of contention with this stock is that its EPS has not grown since 2019. Its EPS growth over this period is 0%. This is despite reporting record net income last quarter. Some of its peers have done far better, while others struggled significantly.

Therefore, on an industry level, compared with its regional banking peers, its performance can be seen as below average. Still, it is not falling significantly behind to such an extent that it would cause me worry.

Quarterly Financial Performance

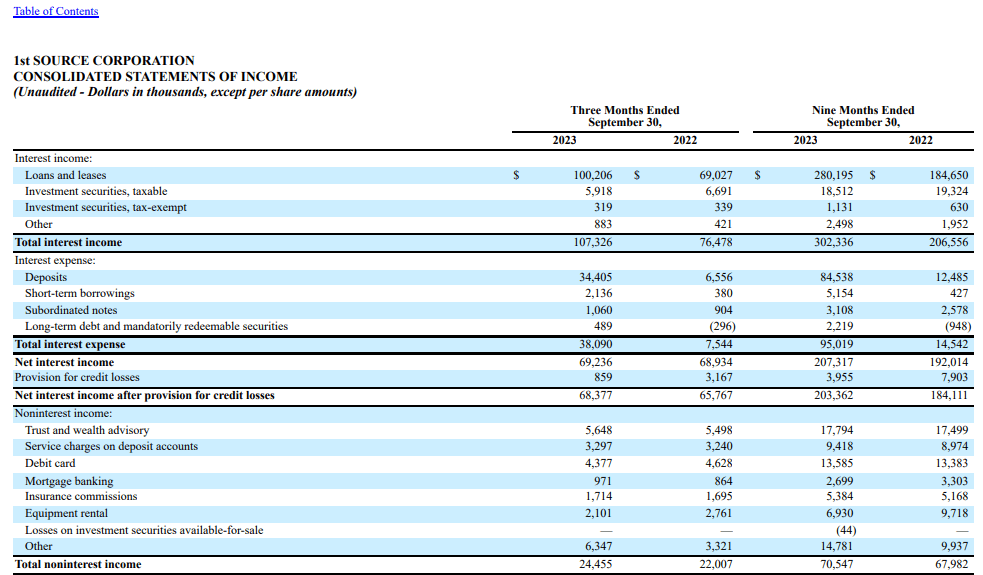

In the recent quarter, the company achieved a record net income of $32.94 million, marking a 0.62% increase from the third quarter of 2022. Each common share earned a diluted net income of $1.32, consistent with the previous year's third quarter.

A cash dividend of $0.34 per common share was approved, reflecting a 6.25% increase from the previous year. The average loans and leases experienced a growth of $104.73 million, a 1.71% quarterly increase, and a notable 10.98% increase year-over-year. The company also repurchased 260,887 shares for the treasury at a total expenditure of $10.29 million.

The cause of the record performance came from the growth in the loans and leases category. There was also a noticeable increase in noninterest expenses, mainly in salaries and employee benefits. Despite these increased costs, the bank has managed to maintain a stable EPS, with slight improvements in noninterest income categories.

{kind=link}

The new loan originations came from various portfolio sectors but were overwhelmingly concentrated in Commercial and Agricultural, Solar, Auto, and Light Truck. The Solar sector shows a notable increase in origination in 2023 at $129.39 million, highlighting a surge in activity or focus in this area.

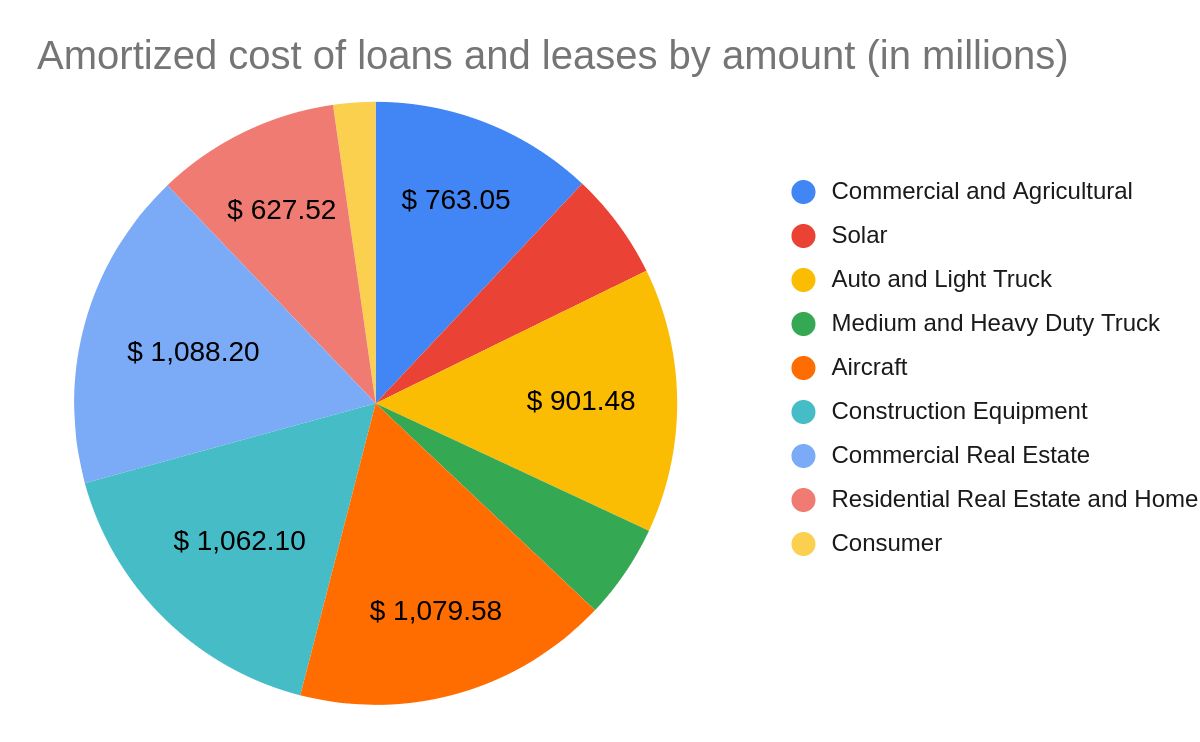

The total amortized cost of loans and leases shows a healthy and diversified loan portfolio. The weakness of the riskier consumer segment, which is the smallest and accounts for only 2.68% of its loan portfolio, is also a welcome sight.

Its loans are instead focused on high-value sectors such as Aircraft, Commercial Real Estate, and Construction Equipment, which have significant growth potential.

{kind=link}

| Portfolio Sector |

| Amount (in millions) |

| Commercial and Agricultural |

| $ 763.05 |

| Solar |

| $ 364.95 |

| Auto and Light Truck |

| $ 901.48 |

| Medium and Heavy Duty Truck |

| $ 323.20 |

| Aircraft |

| $ 1,079.58 |

| Construction Equipment |

| $ 1,062.10 |

| Commercial Real Estate |

| $ 1,088.20 |

| Residential Real Estate and Home Equity |

| $ 627.52 |

| Consumer |

| $ 143.57 |

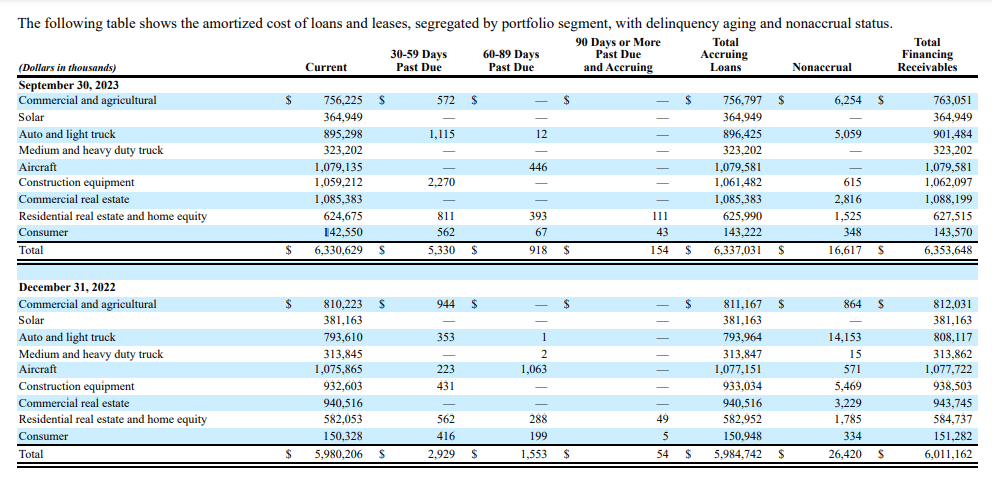

There are aspects of SRCE's risk profile that I find appealing in today's "higher for longer" interest rate environment. The average high-risk percentage across all portfolio segments is approximately 1.71%, as reported in the company's quarterly annual report.

Examining the loan and lease data, it's evident that most of SRCE's portfolio segments are current, with minimal delinquencies. The commercial and agricultural segment has shown a slight decrease in total financing receivables compared to the previous period. In contrast, segments like auto and light trucks and construction equipment have seen an increase.

{kind=link}

Looking ahead, due to economic headwinds like sluggish growth, inflation, and geopolitical uncertainties, the company foresees potential risks and variability in its future loan and lease portfolio losses.

Sourced from its quarterly report:

As of September 30, 2023, the most significant economic factors impacting the Company's loan portfolios are a sluggish domestic growth outlook, exacerbated by persistent inflation, higher interest rates, and global conflicts and resultant elevated geopolitical uncertainty.

The Company remains concerned about the impact of tighter credit conditions on the economy and the effect that may have on future economic growth. The forecast considers global and domestic economic impacts from these factors as well as other key economic factors such as change in gross domestic product and unemployment which may impact the Company's clients. The Company's assumption was that economic growth will slow during the forecast period and inflation will remain above the 2% Federal Reserve target rate resulting in an adverse impact on the loan and lease portfolio over the next two years.

As a result of geopolitical risks and economic uncertainty, the Company's future loss estimates may vary considerably from the September 30, 2023 assumptions.

The above outlook is a crucial reason I maintain a 'Hold' rating for the stock. Due to the cyclical swings the financial sector goes through, I don't see much better alternatives for investors to rotate their capital, especially if that rotation involves a realized loss.

The good news is that SRCE is an excellent dividend stock to hold on to, and its conservative loan portfolio risk profile and free cash flow metrics will give it the stability it needs to hold on while the markets recover.

Dividend Excellence

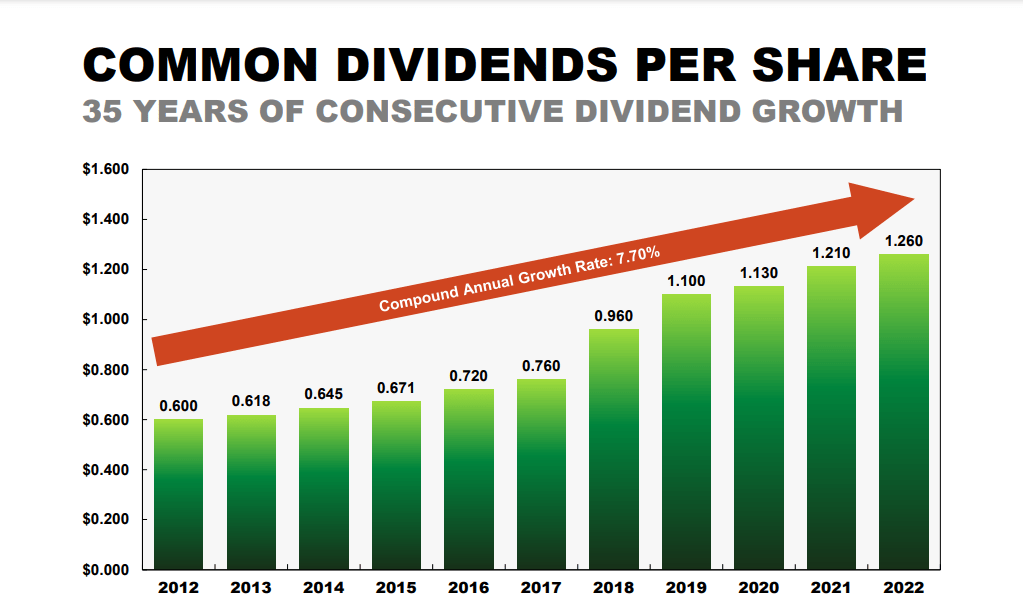

Regarding dividend growth, SRCE is an excellent pick, with over 35 (coming up to 36) years of consecutive dividend growth. Dividends have grown at a CAGR of 7.70% from 2012 to 2022.

{kind=link}

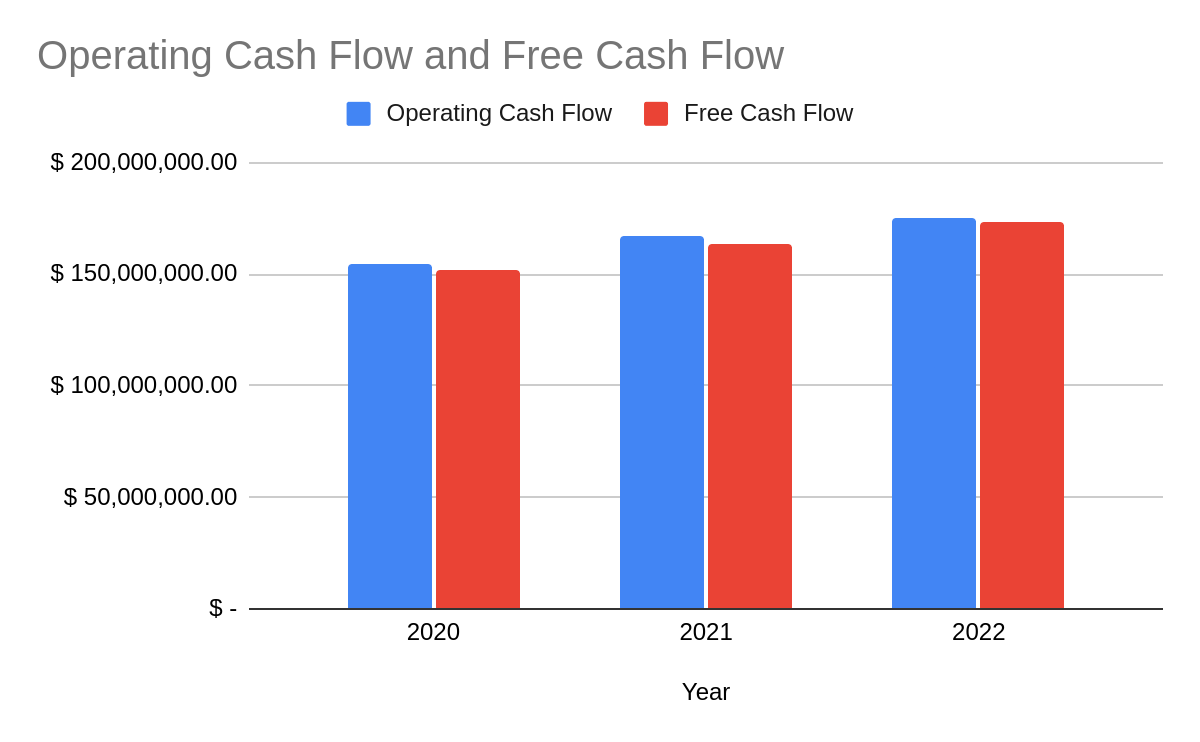

This dividend growth is supported by expanding operating and free cash flows, which have steadily risen since 2022. Making it one of the best financial ratios when assessing the health and attractiveness of a dividend growth stock.

{kind=link}

The dividend is extremely well-covered by free cash flow, and its payout ratio is tiny at just 0.25.

In addition to its fast-growing dividend, management is committed to delivering value back to investors in other ways. Shares outstanding have decreased by 8.69% since 2014, which will keep investors interested if the markets dip further.

When the total return of SRCE is compared with the SPY, we can see what makes the company a safe pick during market drawdowns. Although the total return is lower over the period, with highly safe consecutive dividend compounding, SRCE delivers returns over periods when the market dips.

SRCE also managed to eke out an advantage over the SSPS financials index over the same period.

Valuation

I don't believe now is the right time to start a position in SRCE due to trading appreciably above its book value. Over time, SRCE has consistently reverted to this level, so it seems more likely that this will also happen.

Its stock price is historically more disconnected than it has been on average.

Waiting for some dips around the $40ish level may reward patient investors with a better yield on cost. Part of the reason I believe its stock price has shown resilience is its superb cash generation ability and its efforts to return value to shareholders.

When examined alongside its peers, SRCE's book value is about average, and its current dividend yield of 2.12% is the lowest.

However, the consistency and safety of SRCE's dividend policy, along with its share buybacks and its low-risk profile, makes it a better option overall for dividend investors.

It should be noted its forward dividend yield is higher at 3%. Patient investors could snap up a better yield on cost than this if they are patient.

Risks

The main risk of staying invested in SRCE is the expected loss of capital in the short term. Its reversion back to its book value has remained consistent over the years, but it shouldn't be particularly alarming.

Additionally, the company's future loss estimates are variable due to these unpredictable economic conditions. Investors should also consider the cyclical nature of the financial sector, which could impact the company's performance.

Another risk is the regional concentration of SRCE's operations, primarily in Indiana and Michigan. Economic downturns or industry-specific challenges in these regions could disproportionately affect SRCE's loan portfolio and overall financial health, potentially leading to underperformance compared to more geographically diversified banks.

Takeaway

SRCE holds a stable position with a diversified portfolio and consistent dividend growth despite economic challenges. The odds of its dividend being cut or its dividend growth slowing down are exceptionally minimal due to a mix of its free cash flow metrics and management's commitment to delivering value to shareholders.

However, investors should consider regional and sectoral risks and await a more favorable valuation. The reversion back to book value is expected to provide investors with a better yield on cost and the opportunity to buy new shares. Existing investors should hold tight and wait for the cyclical swings to be over.

For further details see:

1st Source Corporation: Superb Dividend Growth Potential, But Not At This Price