DIBS - 1stdibs.Com: We'll Pass On This One Until An Improving Sales Outlook

2023-11-11 06:54:17 ET

Summary

- 1stdibs.com has seen a 30% rally in recent weeks, with the Q3 results highlighted by a narrowing loss.

- Growth has been a challenge with declining revenues and weak operating metrics.

- We expect shares to remain volatile until there is evidence of an improving sales outlook.

1stdibs.com Inc ( DIBS ) has crossed our radar with a 30% rally in recent weeks suggesting a new wave of bullish momentum. The company operates a global marketplace specializing in fine goods across contemporary furniture, vintage decor, antiques, jewelry, and fashion.

Drawing parallels to platforms like Etsy Inc ( ETSY ) or even eBay Inc ( EBAY ), 1stdibs stands out through a more curated collection including a seller vetting process and enhanced customer support. Overall, we like the concept but are a bit more skeptical about the stock as an investment.

The company just reported its latest quarterly results, where we highlight an ongoing decline in sales while profitability remains elusive. Furthermore, some of the key operating metrics are moving in the wrong direction, adding to doubts that the financial strategy is on track. DIBS is still down more than 80% from its 2021 IPO and we expect shares to remain volatile.

DIBS Q3 Earnings Recap

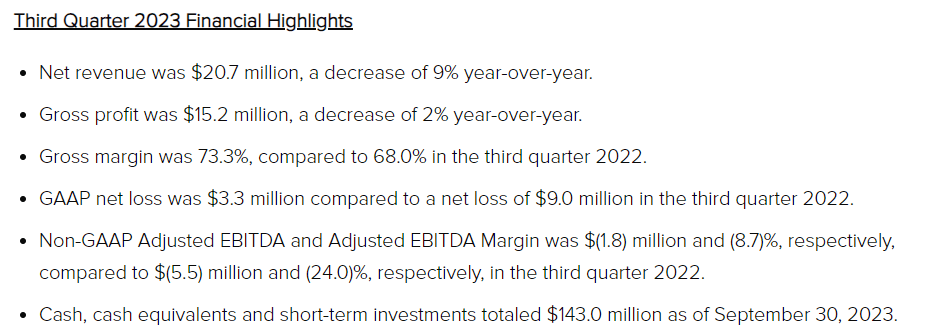

DIBS reported a Q3 GAAP EPS loss of -$0.08, although this measure came in ahead of the consensus estimate by $0.05, an improvement compared to the -$0.23 result last year. Revenue of $20.7 million declined by -8.9% year-over-year.

Overall, it's fair to say that the stock rally off of the report considered that expectations were already low and the company was able to outperform by a bit. In this case, the gross profit saw a narrower decline of just -2%, driven by a jump in the gross margin reaching 73.3% compared to 68% in Q3 2022. The impact translated to a narrowing adjusted EBITDA loss at -$1.8 million, from -$5.5 million in the period last year.

Management is citing efforts at cost controls and engineering a more streamlined operation as positioning the company to better navigate what remains a "choppy demand environment".

{kind=link}

From a high level, the understanding is that particular softness in the luxury housing market has pressured demand. Here is where we get into the more concerning operating metrics for the group.

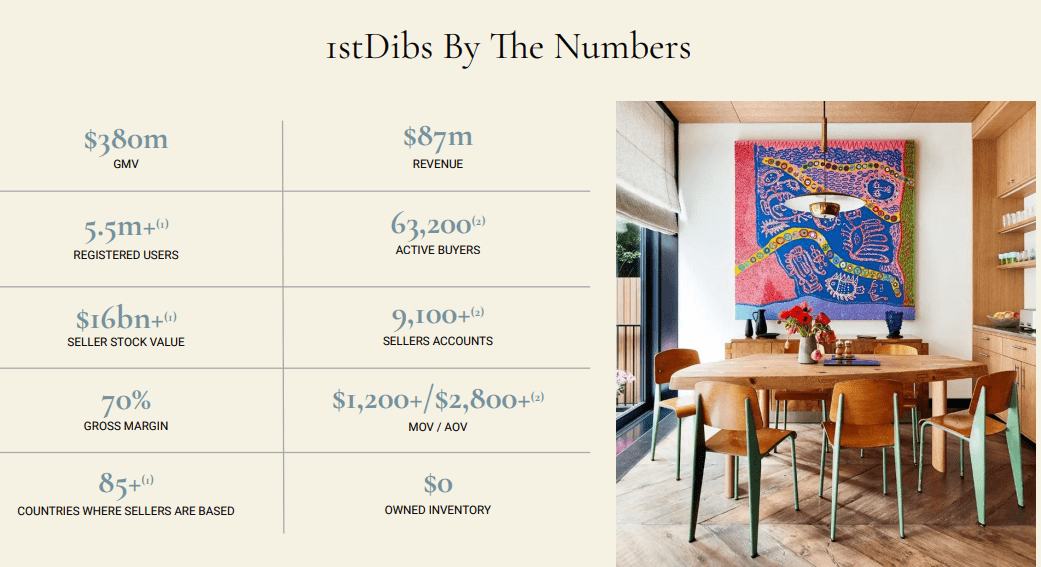

The number of active buyers on the platform at 63k in Q3 declined by -7% y/y. This group contributed to 31k new orders, down 11% y/y while the gross merchandise value ((GMV)) transacted on 1stdibs at 89 million is down by -10%. During the earnings conference call , management noted alternative measures like site visits and conversion rates, but otherwise soft trends.

{kind=link}

In terms of guidance, 1stdibs is targeting Q4 revenue between $19.7 and $20.8 million, representing a -12% decline from $22 million in Q4 2022. The expectation is that a negative adjusted EBITDA margin between -13% and -8% comes in a bit lower than the Q3 figure.

1stdibs ended the quarter with $143 million in cash, against effectively zero financial debt beyond $19 million in lease liabilities. The understanding is that despite the recurring cash flow bleed, the balance sheet position provides some flexibility and time for the company to move forward.

Some of that cash position has been directed at a $20 million stock buyback authorization. Year today, the company has repurchased approximately $1.4 million in shares.

What's Next For DIBS?

As commendable as the efforts at cost savings and expense control in support of margins have been, the reality is that the company will need to begin generating stronger growth sooner rather than later.

We can connect some of the poor operating metrics and decline in active customers to the macro environment, but it also raises the question of brand momentum and broader macro opportunity.

Some of the strategy initiatives include expanding into new markets including bringing in sellers in new foreign markets. There is also a push to expand the number of product verticals and categories.

From there, the challenge will be to expand the pie of active customers and generate a sustainable rebound in the number of orders and the gross merchandise value. As an investment opportunity, we haven't seen enough to suggest a new round of growth is incoming.

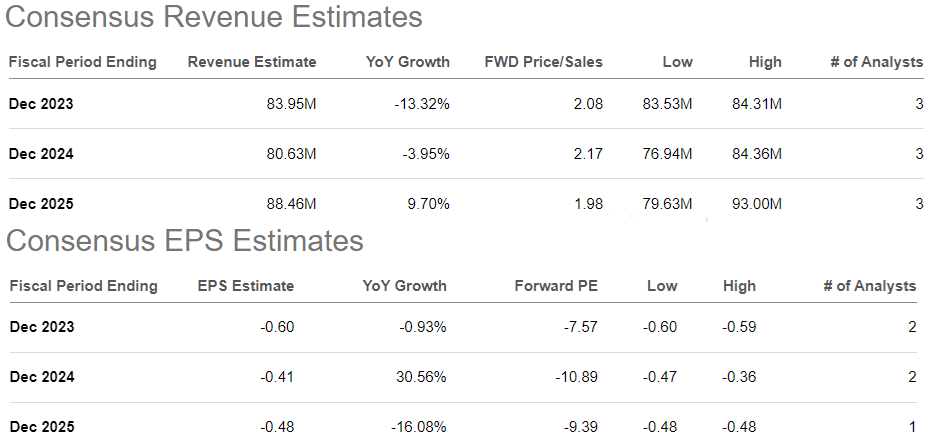

According to consensus, the forecast is for the company to not generate a profit through fiscal 2025. Compared to an estimated -13% decline in revenue this year, the trends suggest another decline on the top line in 2024.

{kind=link}

Final Thoughts

We're not convinced about 1stdibs and suggest readers simply avoid the stock. The company's strong balance position is likely enough to brush aside any near-term liquidity concerns and can support the stock around its current $180 million market cap, although we believe the poor growth outlook is a bigger headwind likely limiting a sustained rally.

The risk here is that operating and financial metrics continue to disappoint, leading to an accelerating cash burn, and opening the door for a deeper selloff. Trends in adjusted EBITDA and the number of active buyers are key monitoring points.

For further details see:

1stdibs.Com: We'll Pass On This One Until An Improving Sales Outlook