DIBS - 1stDibs: Long Term Play Favorable Risk Reward

2023-06-09 10:42:32 ET

Summary

- 1stDibs.com, a luxury furnishing e-commerce platform, is grappling with pandemic reset softness in the luxury market due to macro headwinds.

- The company continues to roll out initiatives to accelerate GMV trends, strengthen its supply chain, and improve retention among active subscribers.

- Despite current market softness, I believe 1stDibs.com's long-term growth opportunity is favorable, with a strong track record in revenue and margins.

- With more than $150 mn in cash balance and applying a modest EV/ Revenue of 0.5x, we initiate this at Buy with target price of $5.5.

Investment Thesis

1stDibs.com ( DIBS ) operates a high-end luxury furnishing e-commerce platform connecting over 7k+ third-party sellers with ~68k active buyers. Post a stellar listing with shares popping up over $30, the stock is settling at its all-time lows as the lux furnishing market shifts to a pandemic reset.

It offers a wide range of vintage, antique, and contemporary furniture, home décor, jewelry, watches, art, and fashion products with 5.5 million registered users along with 1.5 million listings and an AOV of $2,700 (substantial within the e-commerce space). We believe the company is poised to perform well as the luxury market turns around driven by their positive unit economics, inventory light model, user retention (with a third being frequent buyers) and strong supply chain. We believe at current valuations the risk reward is favorable with its current market cap of ~$150 million despite having cash balance of $150 million. We initiate a buy at 0.5x EV/ Revenue to reflect the near term economic downturn and assign a target price of $5.50.

Growth Drivers in Place

Despite a fall in GMV due to softness in luxury home good market as a result of the macro headwinds, DIBS has been able to maintain its take rate and sustain its revenue while not going too aggressive on augmenting marketing expenses and jacking up losses. Its strong reliance on trade buyers and repeat orders have sustained despite the current downturn helping them drive organic growth and improve conversion.

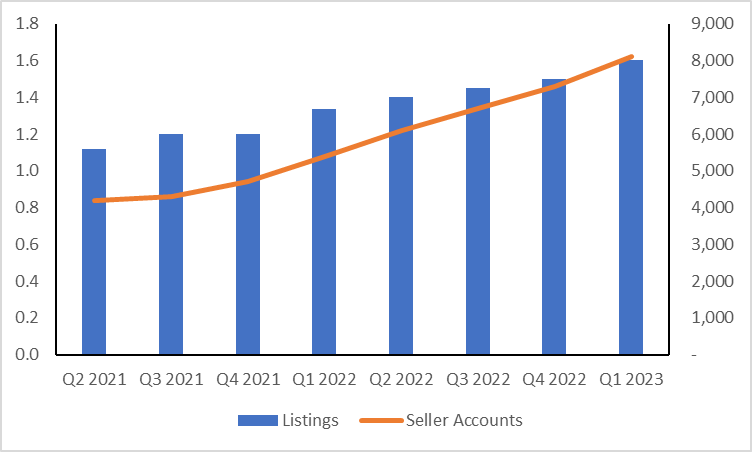

In Q1 2023, DIBS reported a GMV of $97 million , a decline of 17% YoY on the back of lower active consumers at 66k, a decline of 6% YoY and AOV of $2,674, a decline of 8% YoY, although it improved sequentially. Take rate remained fairly stable at 22.86% vs 23.41% in Q1 2022 while revenue declined by 17% YoY at $22.2 million. Operating loss came in at -$10.2 million as a result of lower marketing expenses partially offset by lower gross margins due to one-time amortization cost (which impacted gross margins by 2%). Organic traffic increased to nearly 75% of total, up several percentage points, driven by continued SEO strength and pull back on performance marketing. Supply chain remained strong where in it added 800 new sellers and listings grew 20% YoY to 1.6 miln. Sub fees remained flat sequentially after a continued decline in past 3 quarters which also is an encouraging sign. It expects Q2 revenue of $20.7 mn at mid point, a decline of 16% YoY, while adjusted EBITDA of ($6.4) mn as it does not expect a meaningful impact on expense structure.

DIBS continues to rollout out initiatives that could accelerate GMV trends when the core luxury furnishings and home goods market returns to growth. Refined pricing formula has led to better conversion (new order growth up 11% sequentially in auctions) and management has been able to strengthen its supply chain and improve retention amongst its active subscribers (trade buyers share has improved by 500 bps in 2 years).

Listings and Seller Accounts continue to rise

{kind=link}

It has also been able to drive growth internationally, having increased its order growth by double digit in France and Germany this quarter, and also plans to enter Italy and Spain in Q3. Auctions has also been performing well, up 10% sequentially, which although is currently at a lower base, could well be a contributor to the GMV going forward due to continued traction.

Investment Highlights

1) Positive unit economics: Company is able to generate positive unit economics from the first order itself and able to drive better returns as the customer comes back to order every year.

Company filings

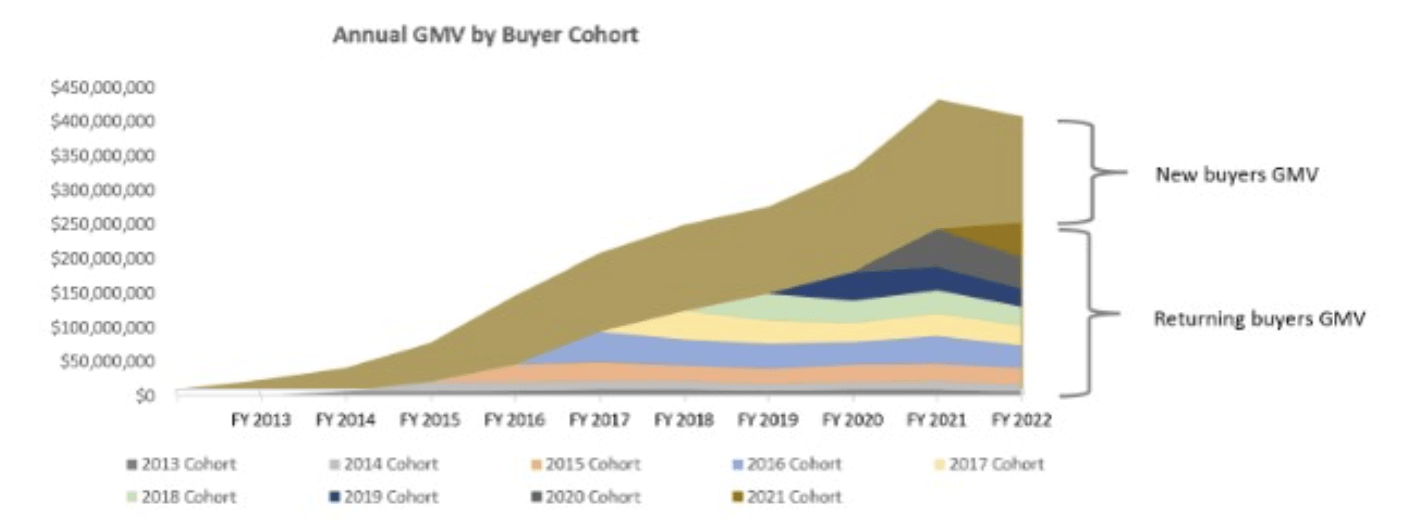

2) Strength in user retention: DIBS has been able to retain most of its trade buyers and actively adding to its GMV (up 500 bps), with repeat orders continuing to grow. Trade buyers remain about a third of the total buyers as the company increasingly focuses on priority Trade 1st program offering better incentives and priority support.

Trade buyers (contribution % of total GMV)

Company filings Company filings

{kind=link}

3) Strong seller retention: Sellers have been a major driver of growth with increasing buyers, even amidst a softness in luxury market, and listings growing in HDD leading to a strong supply network and seller's increasing reliance on the platform.

4) New revenue opportunities: It has new revenue opportunities across a wide range of categories, segments, geographies and formats. DIBS is increasingly looking to expand internationally which has received strong reception as demonstrated in France and Germany. Its focus on other high value segments such as jewelry, art and custom furniture, could lead to further upsides to GMV. Its auction model could also contribute meaningfully to the GMV as trends remain strong.

5) Inventory light model to enable margin upside: As a third party e-commerce player, DIBS has no inventory and has a capital light model with negligible capex. As the GMV turns, we believe the company will be able to expand its operating margins which could lead to multiple expansion.

Would it turn profitable?

DIBS has not been operationally profitable since founding typical of a growth led e-commerce startup which is currently operating at a small scale. However, we believe its inventory light model with negligible capex along with its ramping up of GMV in new geographies (45% of total sellers are outside the US currently and growing) and categories with strong seller network and customer loyalty could entail them to become the go-to player in "All Things Luxury". It continues to make investments within customer acquisition, infrastructure and technology expenses and new categories to drive GMV and revenue growth leading them to continued losses. Baring Etsy, several of other competitors such as Farfetch ( FTCH ) continue to remain largely unprofitable despite being of a larger size than DIBS. While we believe profitability is still some time away for DIBS, we believe in the medium to long term, it has drivers in places to turn into black driven by higher gross profits and optimizing SG&A expenses, in particular marketing expenses.

1) Gross Profit Margins of DIBS is much higher than FTCH and in line with Etsy as it focuses on higher margin products. In addition, AOV of FTCH is $632 and Etsy is known for its value products, DIBS' AOV is much higher at $2,700 which essentially would entail if the company is able to continually retain more of its buyers on the platform, higher GMV would entail much higher gross profits.

2) It has been increasingly focused on refining its sales and marketing expense and pulling back on performance marketing increasing its efficiency thresholds.

The strategic pull back on marketing and continued SEO strength has led to organic search driving strong traffic to the website which bodes well for the platform.

SEC filings

Despite that, Selling and Marketing expenses continue to remain elevated (at ~45% of revenue) compared to ~25-30% of its peers, and would have further cushion to curtail costs while maintaining sustainable growth.

Valuation

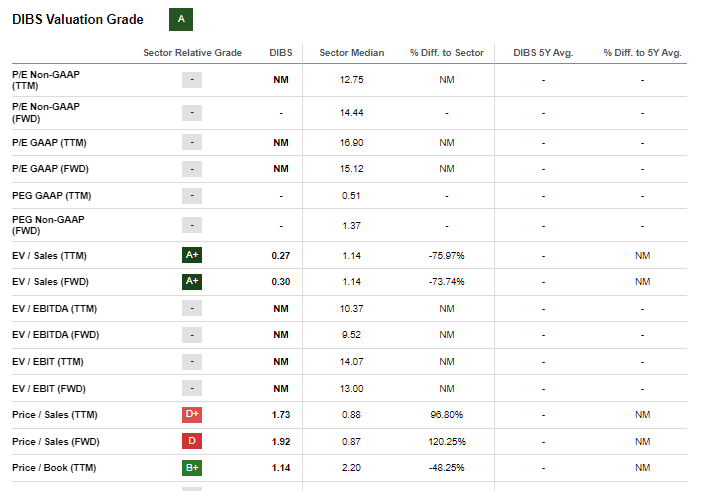

DIBS' current levels of $4 factors in cash/ share value of $3.87 as of March 2023. We believe despite the softness in current luxury market and profitability still some time away, the current price reflect a favorable risk reward for long term growth opportunity. As for any growth led digital focused third party e-commerce player who is not yet profitable, we believe EV/ Revenue is an appropriate valuation metric to value the company. We believe DIBS has had a strong track record in revenue and margins than Thredup, however, even factoring a conservative 0.5x EV/ Revenue (in line with Thredup), we arrive at a price target of $5.5 per share. There, I initiate this as a Buy.

DIBS valuation grade also reflects an attractive 'A' driven by valuation comfort relative to its peers.

{kind=link}

Risks to Rating

Risks to the rating include 1) continued deterioration of macros leading to softness in luxury home goods and furnishing market which will result in deceleration of GMVs 2) DIBS is unable to expand meaningfully in international markets leading to write-offs 3) small scale currently that could lead to competitive pressures and 4) Elevated costs in marketing amidst declining GMV could lead to profitability being pushed for several more years

Final Thoughts

DIBS is pained by a significant headwinds in the current macro uncertainty as a result of higher interest rates and housing market volatility coupled with geopolitical tensions. However, its focus on the high income users and high order value could be rewarding when the market turns. Its inventory light model and expansion of GMV in new models (such as auction models), new geographies and new categories (jewelry grew double digit this quarter albeit on a small base) would drive GMV and revenue growth, while higher gross margins, average order value and continued optimization of marketing spends could eventually lead them to be profitable, although that is still several quarters away. We believe the current price provides a favorable risk reward for long term investors, even after applying a modest 0.5x EV/ Revenue to factor in the near term challenges that the company faces. We initiate this at Buy with Target price of $5.5 per share.

For further details see:

1stDibs: Long Term Play, Favorable Risk Reward