MAIN - 2 Best-In-Class 10% Yielders To Own Through Thick And Thin

Summary

- High yield investing is hard enough. Why take a risk on a company without a strong track record of success?

- While there are certainly some undervalued and misunderstood high-yielders out there offering enough margin of safety to be worth the risk, it's also smart just to own the best-in-class.

- We present two best-in-class stocks that pay 10% dividend yields.

Co-produced by Austin Rogers for High Yield Investor.

After years of living in a low-yield, low-interest rate world, finding high-income dividend stocks is finally possible right now.

But investors should never forget that high yield comes with elevated risk. That's why it's important to choose income investments wisely. The priorities of every income investor ought to be:

- Capital preservation (don't lose money!)

- Generate the maximum amount of income without compromising on Point #1.

At High Yield Investor, we have multiple strategies for accomplishing these two points. Frequently, we home in on deeply undervalued companies with ample margins of safety built into their stock prices. This way, we minimize downside risk while maximizing income upside.

But another, more obvious way we achieve these priorities is by finding the best-in-class companies in their respective industries and make those long-term, core holdings in our portfolio.

Today, we present two arguably best-in-class companies trading 12% or more below their highs...

...that also offer dividend yields of around 10%.

For income investors looking for relatively safe high yields, there are far worse places to look than these two names.

Arbor Realty Trust, Inc. ( ABR )

- Dividend Yield: 10.7%.

ABR is a specialty mortgage REIT that focuses on bridge loans for multifamily real estate properties, but the company has also been growing its number of loans to single-family rental projects as well.

But ABR has multiple streams of income. As explained in a recent article from one of our analysts, ABR has three primary business segments:

- Balance sheet loans , originated and held on the balance sheet.

- Government-sponsored agency (Fannie/Freddie) loan origination , a capital-light way to generate income without long-term ownership risk.

- Loan servicing , which offers loan asset management services to other investors who want a piece of the action but don't have their own infrastructure to manage it.

{kind=link}

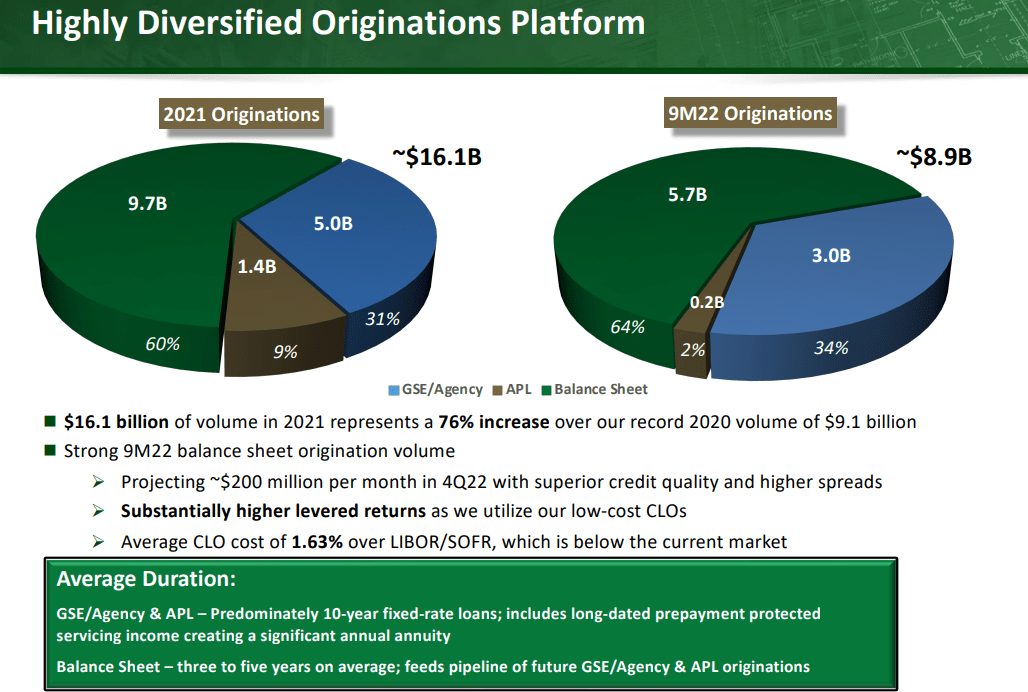

As you can see above, nearly 2/3rds of loan originations are kept on ABR's balance sheet and become part of its own investment portfolio.

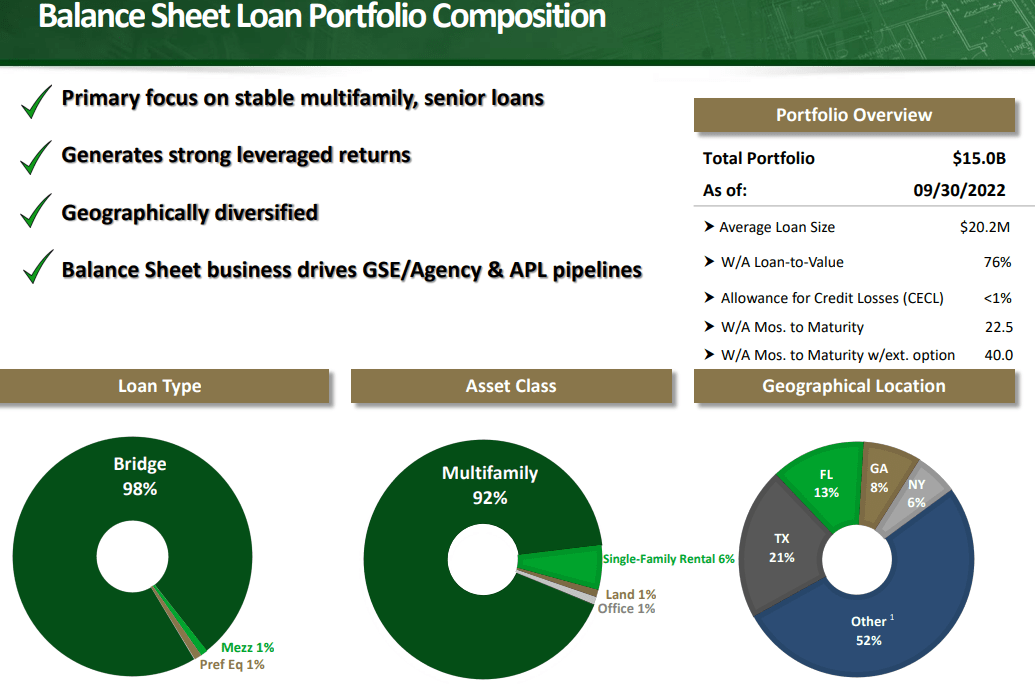

This portfolio of retained loans is about $15 billion in size, with a weighted average remaining maturity of 22.5 months, just shy of two years. Virtually the entire portfolio is made up of multifamily or SFR bridge loans, nearly half of which are located in Sunbelt states like Texas, Florida, or Georgia.

{kind=link}

Bridge loans are a short-term (2-4 years in duration, typically) type of debt that usually comes after construction loans and before long-term financing, like a mortgage. Alternatively, it can be a form of temporary financing for the buyer of an existing property that is only meant to last for as long as necessary to obtain long-term financing.

Notice in the above image that ABR's credit losses amount to less than 1%. Despite extending high-yield loans (in the 7-8% range), the mREIT enjoys very little leakage in interest on those loan assets. This demonstrates the quality of ABR's underwriting standards.

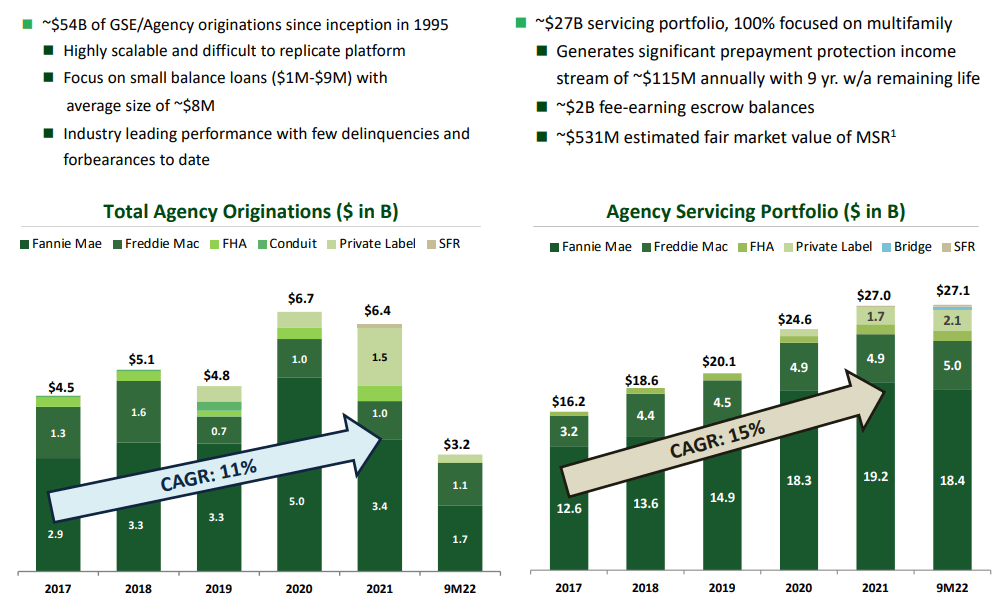

In addition to its portfolio of retained loans, ABR also generates stable and annuity-like income streams from the loans it originates and sells into the secondary market. Most of these are guaranteed by a government agency such as Fannie Mae, Freddie Mac, or the FHA.

{kind=link}

ABR also has a growing asset management business wherein it services loans for third-party investors. This servicing portfolio is likewise 100% focused on multifamily real estate.

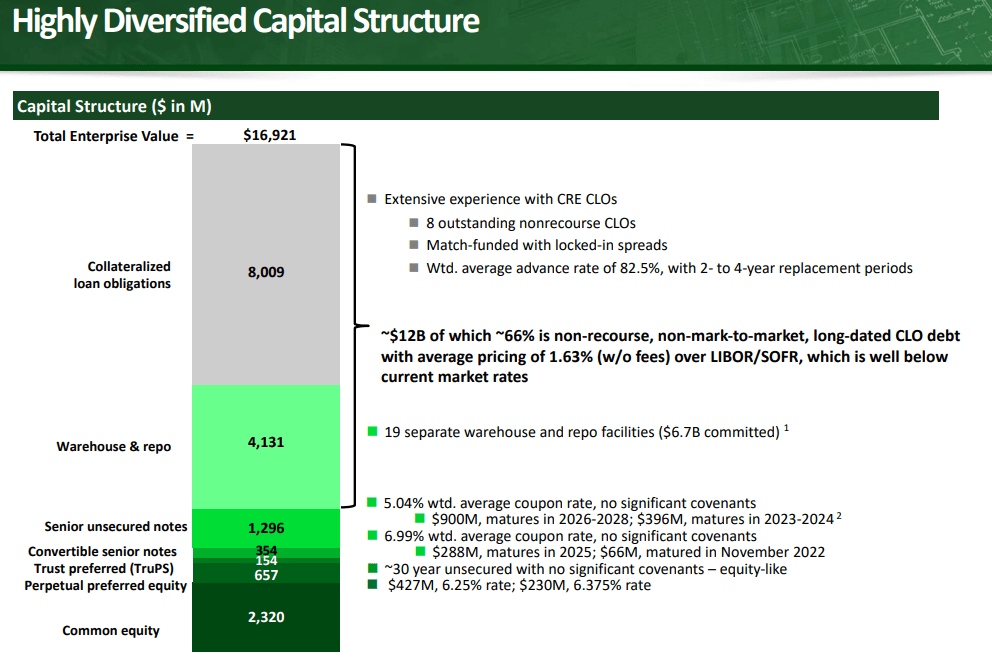

ABR's balance sheet is somewhat complex, with the mREIT's own financing coming from a variety of sources, from securitized collateralized loan obligations, or CLOs, to perpetual preferred equity.

{kind=link}

Common equity makes up only 13.7% of total capitalization. The good news is that ABR's largely floating rate debt enjoys locked in spreads with its floating rate loan assets, which means that ABR should continue to earn a profit whether interest rates rise or fall.

One of ABR's greatest strengths is its skilled and shareholder-aligned management team, which owns about 12% (~$307 million) of ABR's common equity. The team is led by longtime CEO and industry leader, Ivan Kaufman, along with a deep bench of experienced professionals. We appreciate that, rather than trying to be "jacks of all trades," Kaufman's team are masters of one: multifamily, and residential real estate more broadly.

Case in point: ABR's return on equity of 17.7% for the first nine months of 2022 is unparalleled in its industry (Q4 not released yet).

ABR's 10.7% dividend yield is well-covered by distributable earnings and made even safer by the company's defensive and stable portfolio of residential loans.

Ares Capital ( ARCC )

- Dividend Yield: 9.7%.

ARCC is one of the highest quality business development companies ("BDCs") by a number of measurements. The BDC is externally managed by Ares Management Corporation ( ARES ), and while external management would normally be a red flag for us, we think ARES does a great job stewarding ARCC.

For proof of this skillful and shareholder-friendly management, consider the degree to which ARCC has outperformed the BDC index ( BIZD ) over the last decade:

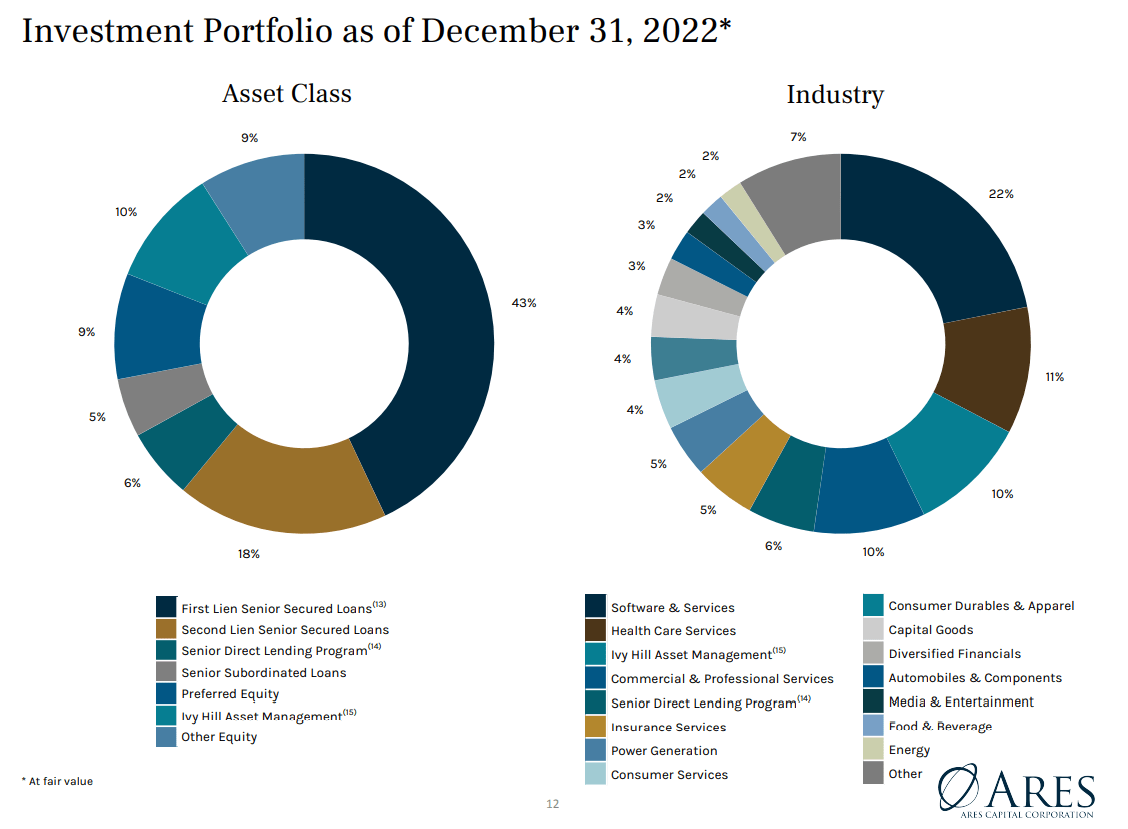

ARCC extends senior secured loans to middle-market companies across a wide variety of industries, with a particularly heavy emphasis on defensive sectors like software, healthcare, insurance, and electric power generation.

{kind=link}

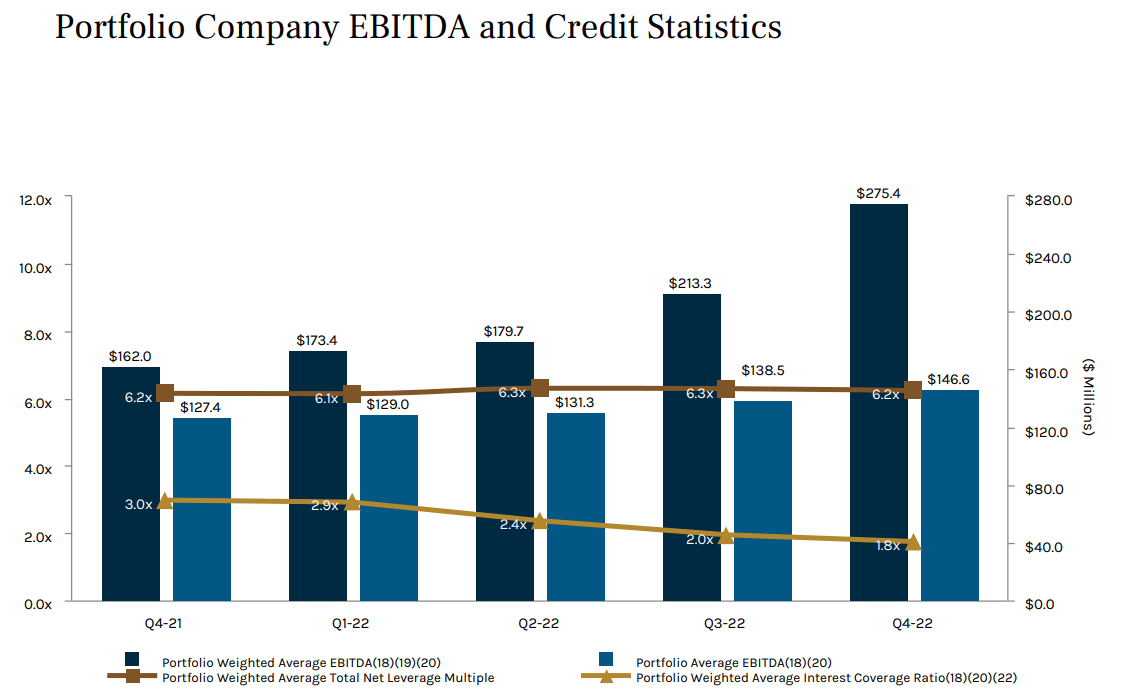

ARCC's largely floating rate loan portfolio benefits greatly from rising interest rates, hence the weighted average yield on investment cost increasing from 2021's 7.9% to 2022's 10.5%.

On the other hand, rising interest rates have also had the negative effect of reducing its portfolio companies' interest coverage ratio from 3.0x in Q4 2021 to 1.8x in Q4 2022.

{kind=link}

As a percentage of investments at fair value, ARCC's number of loans on non-accrual status (switched to cash accounting to reflect the doubtfulness of receiving the full contractually obligated amount of payment) has increased from 0.5% in Q4 2021 to 1.1% in Q4 2022.

This slight increase does not come close to threatening the dividend, but it does reflect the downside of a floating rate loan portfolio during a period of rising rates. So long as borrowers can pay those higher rates, it's beneficial. But eventually, higher interest rates are likely to cause defaults to rise.

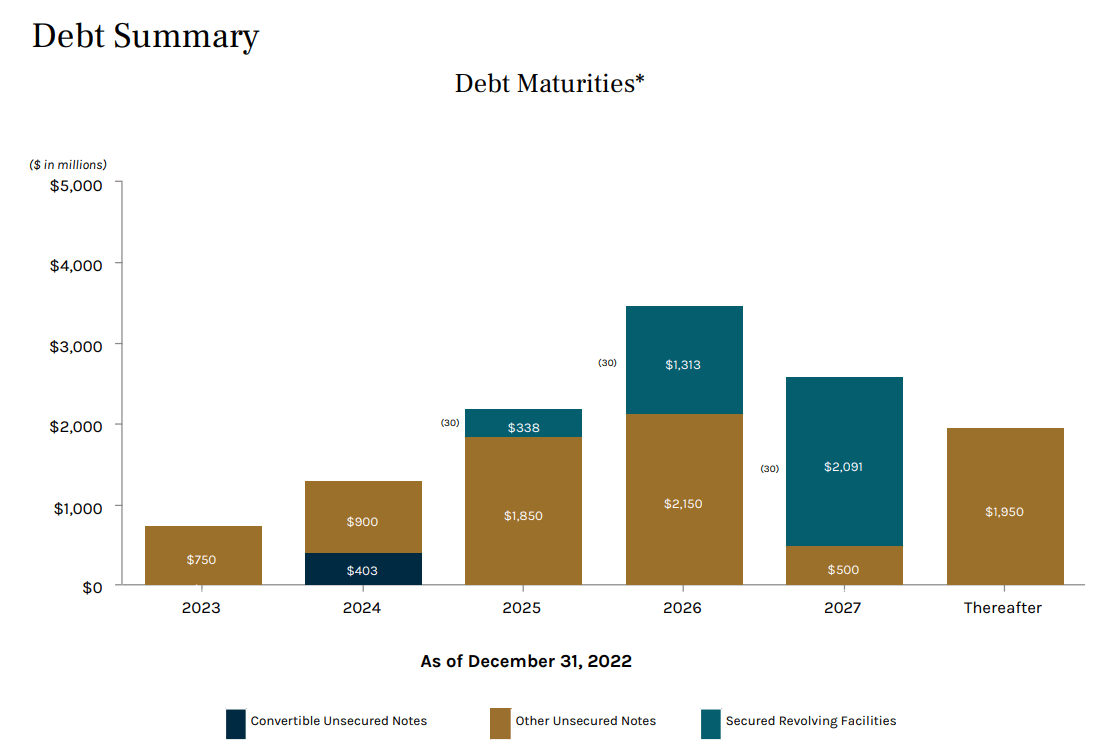

Luckily for ARCC, the BDC remains well-capitalized and highly liquid, with relatively little by way of debt maturities in 2023, reflecting little refinancing risk.

{kind=link}

ARCC's debt-to-equity of 1.29x is on the high side of its normal historical range, so the company will likely perform an equity capital raise in the near future in order to bring down that ratio closer to 1x.

The external manager's base management fee and other administrative fees together amount to about 15% of total investment income. Compare that to the cash- and share-based compensation plus G&A expenses of Main Street Capital ( MAIN ), widely considered to be the highest quality and most conservative BDC, which amount to 18% of total investment income.

Moreover, the $1.92 annual regular dividend remains very safe, as it is not only covered by earnings (e.g. $2.02 in core EPS in 2022) but also by the $1.27 per share in spillover cash available for distribution in 2023.

Bottom Line

Income investors should never forget that any sort of high-yield investing inherently features some sort of above-average risk. Whether it is on the equity or debt side, consistently generating strong returns from high yield assets is challenging. Thus, it is always a good idea to identify the smartest managers with the best track records of actually succeeding in their high-yield investments, whatever those may be.

ABR and ARCC are two examples of high-yield investment managers that perform well over time because of their skill and conservatism. We think that strong performance should continue for many years to come.

For further details see:

2 Best-In-Class 10% Yielders To Own Through Thick And Thin