RILYP - 2 Bonds For Your Retirement Yields Up To 9%

2023-12-04 07:35:00 ET

Summary

- Baby bonds provide accessible entry into the highest tier of the corporate capital structure.

- Known for their steady CD-beating interest payments, these securities can offer substantial capital upside if purchased at today’s deeply discounted prices.

- Baby bonds are a must-have in a diversified portfolio, and we are building a custom maturity ladder at HDO.

Co-authored with “Hidden Opportunities”

"Baby bonds" typically refer to fixed-income securities or debt instruments that are issued in small-dollar denominations with a face value of less than $1,000, making them accessible to the average investor for their income needs.

These instruments are higher up in the issuer’s corporate capital structure, providing income safety and making them relatively less volatile in response to the issuer’s everyday activities or news cycle surrounding it. Source

Stonebridge Advisors LLC

Whether or not you are an income investor, baby bonds are a must-have in a diversified portfolio as they offer much-needed stability through regular interest payments. In addition, they present several advantages outlined below.

They Trade Like Stocks: Baby bonds trade on an exchange just like common stock, making them accessible to almost everyone with a conventional brokerage account.

Higher Liquidity: The low face value of baby bonds makes them more accessible while providing higher liquidity than traditional bonds.

They Are More Accessible: Small investors cannot afford traditional bonds whose unit sizes can be in the $100,000 range. Moreover, traditional bonds only trade on the bond markets, reserved for institutional investors. Baby bonds provide liquidity and access to the general public.

Lower Credit Risk: Baby bonds often carry ratings from credit agencies. In fact, they are often a company’s only rated security that is accessible to the public, presenting lower credit risk than common stock or preferred shares.

Lock In the Yield Until Maturity: Unlike dividends that can be suspended or reduced based on management’s evolving priorities with the company’s cash flows, a bond coupon is fixed and critical for the company to maintain. Investors get to lock in a steady yield backed by the company’s creditworthiness, providing a consistent return until maturity.

Interest, not Dividends: Since baby bonds pay interest (not dividends), they can be a good fit for international investors as they will not incur the unpleasant dividend withholding tax.

Amidst elevated interest rates, bonds are trading at pennies on the dollar. We see a generational buying opportunity and will now examine two deeply discounted baby bonds for steady interest income through rocky market conditions.

Pick #1: RILY Baby Bonds - Up To 9.4% Yields

B. Riley Financial ( RILY ) has had an exciting few weeks, with its common stock tumbling down almost 50%, erasing +$500 million in market cap for the diversified financial services provider.

Why is RILY taking a hit?

On November 2, 2023, the SEC (Securities Exchange Commission) charged John Hughes, President and Chief Compliance Officer of Prophecy Asset Management, for his involvement in a multi-year fraud that concealed losses of hundreds of millions of dollars from investors between 2015 and 2020.

Hughes said he worked with two co-conspirators, and one of them is identified as Franchise Group Inc. CEO Brian Kahn.

Franchise Group, Inc. (‘FRG’) was taken private in August 2023 by management, with RILY being a lead financier and underwriter in the transaction. While RILY invested $216.5 million of new capital in the transaction, the rest was mainly funded by management and other institutional, financial, and strategic investors. RILY owns over 30% private equity interest in FRG.

FRG operates six distinct brands across 3,000 locations, with over $4.2 billion in global sales across +12 countries.

Franchise Group (Author's Creation)

Bryant Riley, CEO of RILY, emphasized that FRG is not all about one individual but six different management teams with their own infrastructure and that RILY’s confidence in these businesses and their continued ability to churn cash flows remains intact.

RILY’s Q3 Performance

Seeking Alpha

When investors saw this headline, they automatically assumed RILY’s dividend was at risk and must be cut sharply, and remained convinced about cannibalization when the company declared a $1/share quarterly dividend.

But RILY’s operating revenues increased to $472.9 million ($278 million from services and fees), the highest in the firm’s history (both quarterly and YTD basis), a 48% YoY increase. Operating adjusted EBITDA, the metric management uses to determine its dividend payments, increased to $107.5 million ($267.8 million YTD), providing 3x coverage to the $30 million quarterly dividend spend. RILY reported $2.05 billion in cash and investments at the end of Q3, with a $252.3 million cash balance.

Author’s Calculations

RILY operates an amalgamation of highly diverse yet compatible business segments, and several of them are well-positioned in the current environment, specifically the liquidation and bankruptcy, and the financial consulting segments which reported a 10x and 64% YoY increase in revenues.

Taking advantage of the profitability in their business segments, RILY’s board authorized a $50 million share repurchase plan. The company maintains ample liquidity and is evaluating its allocation priorities for maximum shareholder value creation.

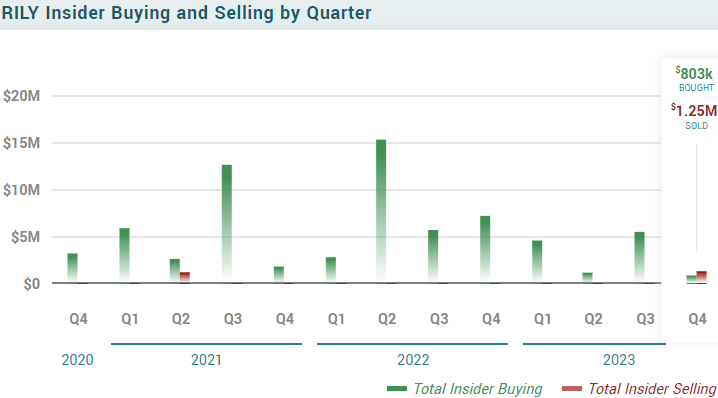

It is notable that management (insiders) own almost 34% of the common stock, indicating confidence in the company’s execution, an overall alignment of decision-making towards activities that benefit shareholders. Insiders have been aggressively buying RILY stock in recent months, and we expect the trend to continue through this sell-off. Source

{kind=link}

MarketBeat

RILY’s baby bonds also declined materially in sympathy and present excellent bargains amidst the fearful sell-off.

- 5.0% Senior Notes Due 12/31/2026 ( RILYG ), yield 7.9%

- 5.5% Senior Notes Due 3/31/2026 ( RILYK ), yield 7.7%

- 6.375% Senior Notes Due 2/28/2025 ( RILYM ), yield 7.5%

- 6.5% Senior Notes Due 9/30/26 ( RILYN ),yield 9.6%

- 6.75% Senior Notes Due 5/31/2024 ( RILYO ), yield 7.1%

- 6.0% Senior Notes Due 1/31/2028 ( RILYT ), yield 9.4%

- 5.25% Senior Notes Due 8/31/2028 ( RILYZ ), yield 9.1%

RILYZ currently yields 9.1% and offers 75% upside to par value. Similarly, RILYT currently pays 9.4% and offers 57% upside to par. Both have a YTM of ~19%.

In 9 months of FY 2023, RILY spent $6 million on preferred dividends, and $140 million interest expenses, both adequately covered by the company’s $267.8 million operating EBITDA.

RILY‘s largest business segments are service and fee-based, recurring, and collectively immune to economic uncertainties. Moreover, the company has a proven track record of taking equity positions and realizing massive gains through the power of brands in the portfolio. FRG happens to be one of RILY’s investments, and while it is still an unproven allegation regarding the FRG CEO’s involvement in the Prophecy Asset Management fraud, a $400 million market-cap loss in a few trading days is almost like the market writing off the FRG investment. We thank Mr. Market for the irrational reaction and consider the fixed-income securities to be terrific bargains at this time.

Pick #2: OXLC Baby Bonds – Up To 7.2% Yields

Oxford Lane Capital Corporation ( OXLC ) is a CEF (Closed-End Fund) that primarily invests in CLO (Collateralized Loan Obligations) equity tranches. The CEF issues subordinated notes and term-preferred shares to leverage its portfolio and invest in more CLO equity. We have discussed OXLC’s business extensively in our previous articles, and will confine this discussion to its bonds alone.

It is to be noted that CEFs are strictly limited by law in how much leverage they can employ. For every $1 borrowed through the issue of preferred securities, the fund must have $2 in total assets. As such, preferred investors are not just protected by corporate governance and oversight, but there are statutory limits on the fund’s borrowings. As a result of these regulatory protections, the preferreds and baby bonds from CEFs provide very reliable income.

C-corps sometimes change their capital allocation priorities and suspend dividends and buybacks to focus on growth opportunities. But CEFs don’t have that choice. Unlike a C-Corp, CEFs are legally required to distribute 90% of the dividends collected, interest earned, and realized capital gains they generate from their holdings. Hence, as long as they are in business and turn a profit, they must distribute it out to common shareholders.

As with all CEFs, there are regulatory limits on leverage that such funds can employ. This adds a safety layer to the bonds and the preferred shares. Looking at OXLC’s Core Net Investment Income over past quarters and the distributions paid, we see a comfortable buffer.

For FY 2022, OXLC generated $153 million NII (after interest payments), paid $17.7 million towards preferred distributions, and $120.6 million on common share distributions (excluding the $20 million from the dividend reinvestment plan). Considering OXLC generated ample NII after preferred distributions to support common share distributions, we see sustainability in the income stream from the CEF’s fixed-income securities.

Author’s calculations

OXLC recently hiked its common share distribution by 6.7%, and the CEF’s ability to support a larger distribution is good news for its fixed-income investors.

-

Oxford Lane Capital Corp., 6.75% Notes due 2031 ( OXLCL ), yield 7.2%

-

Oxford Lane Capital Corp., 5.00% Notes due 2027 ( OXLCZ ), yield 5.5%

Both baby bonds, OXLCL and OXLCZ , make excellent additions to a custom-created bond ladder due to their maturity dates four years apart. Between the two, OXLCL offers higher current income prospects with its 7.2% yield.

Issues with baby bonds

- Not backed by collateral: Despite being higher up on the corporate capital structure, baby bonds are typically categorized as unsecured debt, meaning the issuer or borrower does not pledge any collateral to guarantee interest and principal repayments in the event of default. If the issuer defaults on its payment obligations, baby bondholders will get paid only after the claims of secured debt holders are met.

- Interest gets taxed as regular income: Unlike dividends that can enjoy favorable tax treatment depending on your situation, bond interest payments are taxed as regular income.

- Refinancing risk: Companies can access better financing deals when interest rates are lower. The issuer can redeem the security if the prospectus allows it, and it can be several years before maturity, unlike CD (Certificates of Deposit). This means it may be hard to find a replacement income source if the bonds mature in a low-interest environment.

Conclusion

As we approach the end of the current interest rate cycle, investors should consider purchasing discounted baby bonds as they offer the advantage of fixed returns over the bond's term, shielding investors from potential future interest rate declines.

Several quality baby bonds offer CD-beating income and are well-positioned to provide significant capital upside, making it a must-have for investors of all age groups.

These securities enjoy safety as they sit within the upper levels of the issuer’s capital structure, and failure to make payments would result in a default. This would make the issuer seriously consider all options before pushing the self-destruct button.

W e are loading up on deeply discounted fixed-income picks from high-quality issuers and have a custom-built maturity ladder comprising 21 baby bonds and term-preferred securities with staggered maturities through 2029. Interest rates may sharply drop tomorrow, but our portfolio is well-positioned to churn significant interest income and reward us with sizable capital upside upon maturity. You can also build your custom bond ladder – these two picks with +7.2% yields can get you started.

For further details see:

2 Bonds For Your Retirement, Yields Up To 9%