KIGRY - 2 Companies I Believe Poised To Deliver Triple-Digit 5-Year RoR

2023-08-07 06:47:33 ET

Summary

- The article discusses two European companies, Teleperformance and KION, that have strong potential for double and triple-digit returns.

- Teleperformance is a global leader in outsourced customer experience management services and has a track record of consistent improvement. The company is undervalued and has a minimum triple-digit upside.

- KION is the world leader in industrial truck and supply chain solutions and has recently shown signs of a turnaround. I expect a significant return on investment in the next 1-3 years.

Dear subscribers,

After some movements last week, both on the positive and the negative side, I want to update some assumptions I have. These companies I review in this article are not REITs - nor are they found in NA. They're a mix of European companies.

Their yield is relatively low, but what they do have is a rock-solid foundation and an upside that, if materialized, could see you double and triple your money with ease. What's more, I consider such outperformance realistic on a forward basis.

And, in the case of one of them, some movements in the last week, and over this year, have already confirmed that the lowest times are indeed behind us.

These two businesses are some of my overall highest-conviction current buys. I have been allocating more and more capital to both, and my commercial position in one of them is closing on its limit.

Triple-Digit RoR is possible in these two businesses

Investing for triple-digit RoR requires patience and a contrarian viewpoint. It requires investors to take a long position in a stock that's generally, at the time, viewed as being dubious by the market. Potentially even by other investors. This cannot, if you want to do this sort of investment, faze you.

You need to be comfortable with a stance going clearly against the grain. Also, it's unlikely that you'll catch the company at its lowest point. The only way I've found to do this reliably is to split investments into smaller portions over time instead of investing everything into a company at one time. While the downside risk of this approach is that you end up missing out as the company climbs up quicker than you anticipated (which has happened to me), the upside is that you may miss some mistakes that I did where companies have continued dropping for a significant amount of time before stabilizing.

So, for the most part, I've elected to use this approach and allocate portions at a time as the company moves up, or down.

What I can tell you is that:

- The upside in these businesses is not based on dividends but on capital appreciation. The dividend is a footnote.

- These businesses are both extremely solid with what I view as good long-term forward visibility.

- The demand for their products and services is in no way disappearing - I believe with a high conviction that the reversal for these businesses is extremely likely.

And in the case of such a reversal, the upside here is massive.

Let's begin with potential #1.

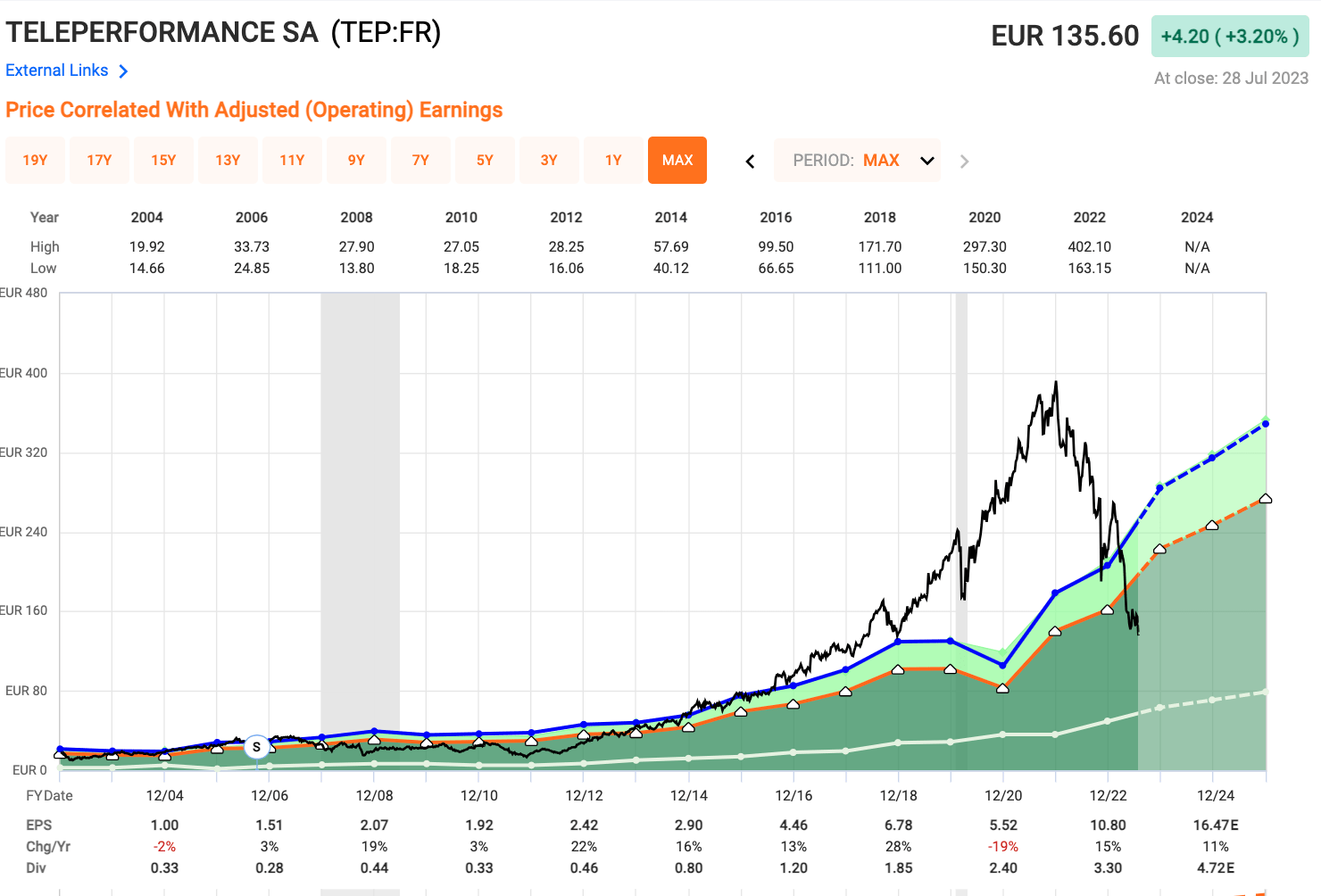

1. Teleperformance ( OTCPK:TLPFY )

I've written about Teleperformance a few times at this point. My entries into the company as an investment have ranged from €131.5 on the low side to around €152 on the higher side, locking in a yield in my position of about 2.7% - not bad at all.

In fact, you may recall articles where I've pointed this company out to you. There is a reason for that. Whenever I've done these picks and tried to highlight the company, I often get the feeling that not enough investors took my stance seriously enough until the company actually reversed.

So I'm reiterating here, with one of the greatest and certainly largest call center/business outsourcing companies on earth. The company employs over 400,000 people across the world and has representation around the entire globe.

Teleperformance IR (Teleperformance)

It's without a doubt, especially with the recent M&A of Majorel, the #1 global leader In outsourcing for customer service and citizen experience, with a 50%+ home-based workforce in 91 countries, over 300 languages, and with over 1,200 global clients.

While the company's share price has Jojoed in an interesting manner, this has absolutely nothing to do with earnings. It's all perception and irrationality. I could have told you years ago that this company is not worth 40-60x P/E. That's why I didn't touch it during COVID-19 when it was trading at those levels. The company is cycling out of irrationality, and that drop is "done". I'm very pleased that I did not go in earlier than I have.

Teleperformance Valuation (F.A.S.T graphs)

{kind=link}

Visual representations like these are very helpful. It's entirely possible that the company will take years to cycle back up - which is why I'm saying 3-5 year RoR. That's how long I intend to hold, if necessary - or even longer. What's important to me is buying a great company at a great price.

And we certainly get that here.

TEP recently reported its earnings results , and the company dropped 14% on that day. So how bad were those results?

Well, the company grew revenues by 7%, saw 30 bps margin improvements in both EBITA and EBITDA on a YoY comparison, and saw further client growth, now expecting the Majorel M&A to go through with regulators in 4Q. No high-level negatives at all.

The company did see some delayed contract signings but was weighed up by strong demand for its off-shore services. Also, on the political front, the Colombian government has closed its investigation into the company, and more agreements with unions have been signed - 3 of them. The market reaction is, to me, an odd one, but it could be (and probably was) that better results were simply expected here.

You can probably already guess that such a reaction doesn't faze me - quite the opposite. I've been busily adding Teleperformance to my portfolio here, and in my commercial portfolio am close to a 2.5% company stake.

You may look closer at my more basic TEP articles for more core info. Here, I want to talk about upside scenarios and potentials. Base cases, bearish cases, and bullish cases.

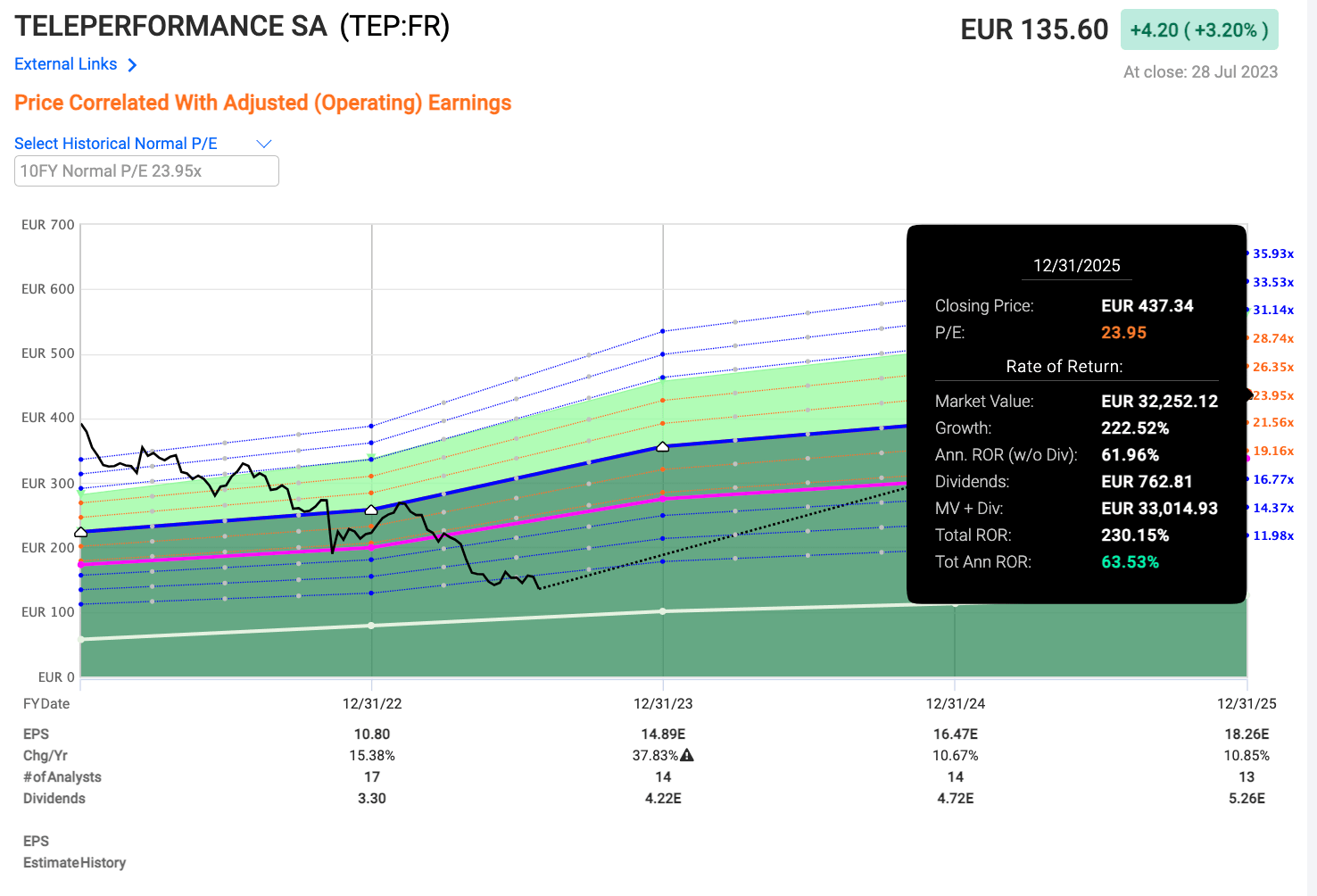

My base case is a longer-term normalization to the growth-relevant P/E of 18-19x. This is based on a double-digit 15% annualized EPS growth rate for the next few years. This comes with a 2-year forecast accuracy of 91% including company beats and a 20% margin of error.

This forecast would give 49.4% annualized RoR, or an RoR of 169% in 3 years. That's my base case.

My bearish case assumes despite the growth the company will remain at a P/E of 15x or thereabouts. Earnings will grow, but the multiple will stay the same. This in turn gives us annualized returns of 36.7%, or 113% in 3 years. Even the bearish case, as such, has a significant triple-digit upside.

The bullish case, which I am always careful with is based on a reversal to the 15-year P/E average premium of around 22-24x P/E. A reversal towards this would entail 63.54% RoR annually, or 230% RoR in 3 years from the current native share price of €135.6.

I tend to generally stick to my base cases, though in this specific one, I'd say the bullish one is entirely possible because there are either very few or no negative downsides on a fundamental level for this company.

Teleperformance is rated BBB, it now has a 2.8% yield, and its upside, I will argue to anyone, is at least triple digits on a 3-year basis. That's the minimum. If it underperforms, it'll likely be due to some market lag, or more unlikely - something unforeseen and negative on the part of this company.

But my expectation is outperformance - and that's why I consider this company one of my strongest buys here. As of writing this article, I've recently purchased a non-trivial position increases as the company dropped below €135/share for the native ticker.

{kind=link}

I believe you should look into Teleperformance, and it's my hope this article can cause you to do that.

2. KION ( OTCPK:KIGRY )

This is more of an "I hope you already invested in this one"-sort of case.

Why?

Because KION is already up 36.68% this year , vastly outperforming indexes. As has my position, much of which I've held since 2022.

However, the upside is not over.

KION is the world leader in industrial truck and supply chain solutions - either world leader or #2nd, depending on what sub-segment you're looking at. KION's problems have been well-covered by me in previous articles. It has, in fact, not been all that long - about 1.5 months - since I highlighted KION for you here on iREIT. But the company very recently reported 2Q and the stock bounced almost double-digits on the news.

So this might be a good "last chance" to get in on the ground floor in this investment, and I don't want you, our subscribers, to miss out on what I view as a superb opportunity.

What marks a superb opportunity in this context is a massive upside, backed by great fundamentals and a great tailwind potential. KION may only be BBB- rated, and its yield has compressed due to its earnings drop to €0.75/share to a per-share basis for 2022 - that's an 83% drop YoY.

But things are about to change.

The recent report pretty much confirms what I have suspected for several quarters. The turnaround is currently building. FactSet expects a potential RoR of 86% per year in the next few years.

Remember, when I've updated on KION what I've wanted to see is a turnaround. YoY comps are still somewhat difficult, especially in the early quarters - because KION dropped most in the latter part of the year.

But in this quarter, we do have a turnaround.

Order intake grew 17% QoQ , with the flat order book. Revenue is now up both YoY and QoQ, and the adjusted EBIT margins are recovering.

Free cash flow is positive again - more than tripling YoY, with EPS up 10% YoY.

Favorable supply chain changes are driving the changes here, as well as benefits from some of the company's internal changes, driving what management - and me as well - are characterizing as a "strong 2Q performance".

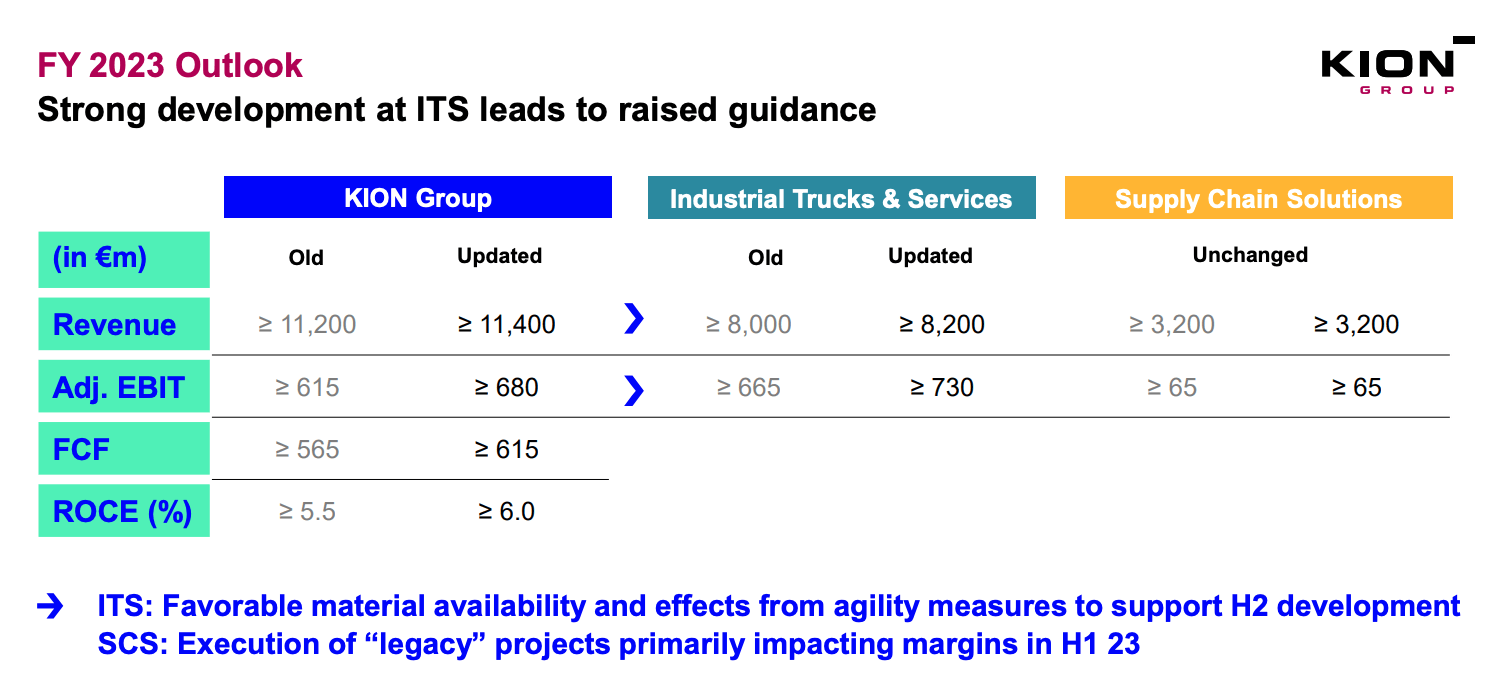

The company increased its FY23 outlook for all major KPIs in the group.

It's fair to question myself at this juncture if I've waited too long to expand this position to my overall 2.5-3% portfolio target. That double-digit intra-day movement was a very strong contrarian indicator. My hope is that we see some downturn again in the near term - but this is always dicey. It might as well continue upward, based on these expectations and trends.

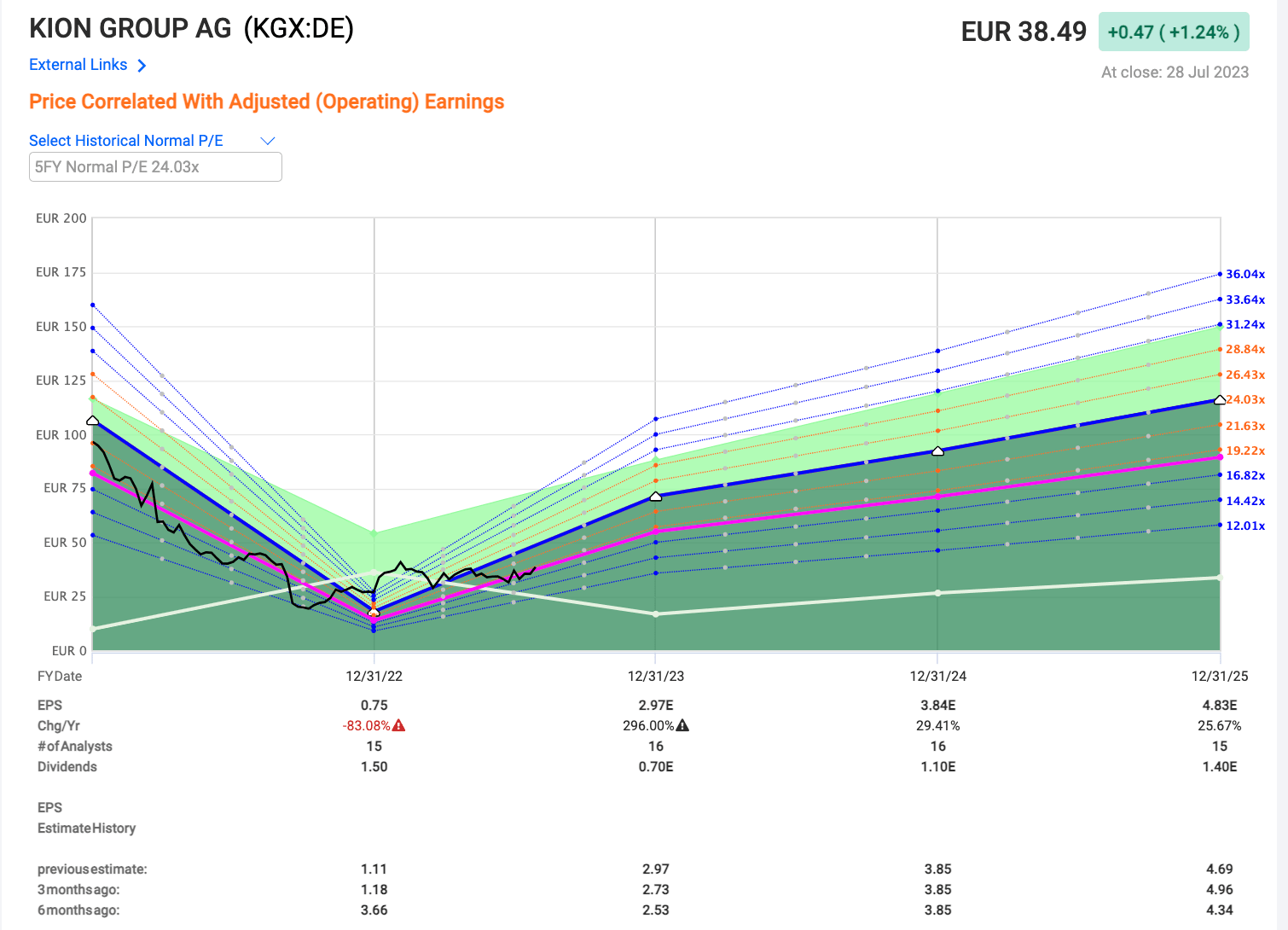

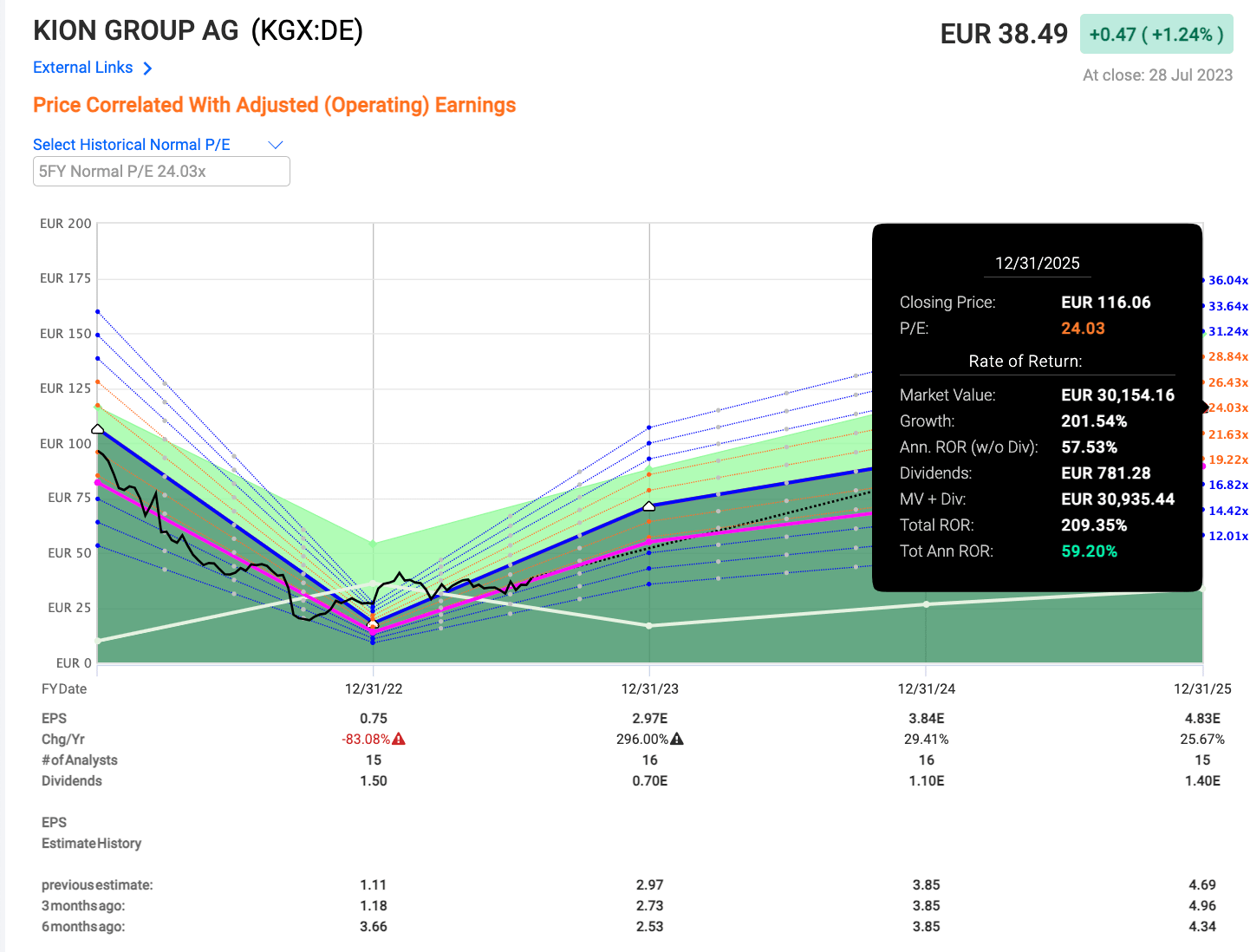

KION forecasts (F.A.S.T Graphs)

{kind=link}

Things have turned around. This is confirmed by the strongest order intake in 12 months, both in units and in terms of euros. Services contributed to stabilizing the overall results. Order book trends are expected to continue in a positive manner, both from the ITS and the SCS segment. NWC is almost stable for this quarter - and leverage levels have significantly improved.

Outlook is improved as follows.

{kind=link}

With ITS performance better than expected, material and SCM trends far more favorable at this time, and SCS still improving in terms of agility and resilience, the company now expects profit normalization in the next few quarters.

Based on this, I give you my base, bullish and bearish thesis for KION at this time.

The base case is an 18-20x P/E based both on historical trends and on the fact of reversal, assuming that 50-60% annualized upside in EPS. Based on the 20x P/E, that's at least a 160% RoR upside or 50% per year.

That's what I expect "most" at this time. Most of my position has a 250%+ RoR because it was bought much cheaper than the current €38/share.

The bearish case is at 14-15x P/E despite a 50-60% EPS growth - that would imply a 25%-31% annualized upside, and a TSR of around 96%. So even in the bearish case, it's close to a triple-digit upside.

For the bullish case , we use the 5-year premium of 24-25x P/E. This calls for a 3-year upside of 209%.

{kind=link}

What I expect for KION is yet another 150-180% RoR in the next 1-3 years. That's why I keep investing and may increase my pace of investing in the company here.

This is my currently second-highest "BUY" in Europe, for the totality of the upside, while based on significant overall safety.

Wrapping up

These are, simply put, two great companies with what I view as excellent overall upsides. My investments in both of them are at relatively high levels. Both for TEP and KION, my position is well in excess of 1% of my total commercial portfolio, with targets of 2-3% in each going forward due to the massive potential RoR.

Another way to put my conviction is that the likelihood of losing your capital is low - that's my view, not an official recommendation. But I do view both of these companies, based upon what they actually do and what we can expect from them going forward, as extremely safe investments despite what can be seen as very volatile trends.

Warren Buffet did something at the beginning of his investment career called cigar-butt investments. This was the equivalent of smoking a puff of a soggy cigar butt you found on the street. He's been known to vocally propose not to do this , but act more conservatively.

I don't view what I do here as cigar-butt investing. I view it as picking industry leaders and companies trading significantly below anything approaching a fair value.

In order to invest in this fashion, you need to be able to tolerate several years of volatility - because these sorts of investments are never truly stable during recovery. But if you share my conviction that quality market leaders do recover, then these are investments you could and should consider.

The advantage of these investments is simple. If you want to grow your capital safely, this is the way to do it on the market, I believe. I've done so in the past - turning over $100,000 to double, triple, and quadruple the amount over time as I've invested. This is, as I see it, the way to do that.

Not 15%-yielding high-risk investments. Not hopium "growth" stocks. These sorts of investments.

Any questions?

Let me know!

For further details see:

2 Companies I Believe Poised To Deliver Triple-Digit 5-Year RoR