KRE - 2 Dividend-Growing Regional Banks To Buy In The Banking Panic

2023-03-16 10:43:57 ET

Summary

- Silicon Valley Bank and Signature Bank didn't collapse because of bad loans. They collapsed because of a certain form of financial mismanagement.

- During the speculative tech boom of 2021, deposits at venture capital-focused SVB and crypto-friendly Signature soared, leading the bank managers to invest in long-term government securities.

- Those long-term government securities cratered in value as interest rates rose, and when depositors wanted their money out, the banks had to sell at steep losses.

- Bar Harbor Bank and Prosperity Bank are two examples of solid, lower-risk regional banks.

- Both banks have solid dividend growth track records spanning about two decades.

In the wake of the Silicon Valley Bank (and subsequent Signature Bank) collapse, investors seem to be selling regional bank stocks first and asking questions later.

In the last month, while the S&P 500 ( SPY ) has slid around 6%, the S&P Regional Banking ETF ( KRE ) has plunged nearly 30%, and certain constituents like First Republic Bank ( FRC ) have nosedived by over 75%.

But the onus of the damage (so far) appears to be concentrated in the banks most heavily exposed to venture capital. This is not because of problems with venture capital per se. Indeed, the venture capital firms themselves appear to be doing just fine (or at least they were prior to these bank collapses). In other words, it was not loan defaults that triggered SVB's failure.

The problem, instead, stems from how certain banks handled the huge influx of deposits in 2021 during the speculative tech frenzy.

In the second half of 2020 and throughout 2021, the combination of ultra-easy monetary policy and ultra-generous fiscal policy made the nation flush with cash and inflamed the animal spirits in Silicon Valley. Capital raising for venture capital firms became easier than ever, and much of this newly raised capital got deposited in the bank for later use.

Below we see that SVB's deposits more than tripled from Q1 2020 to Q1 2022, before beginning to taper off as the Fed began to douse water on the VC capital raising environment.

{kind=link}

It would be nearly impossible for a bank to responsibly put this much money to work in well-underwritten loans.

So instead, with this massive surge in deposits, SVB chose (foolishly, in retrospect) to invest billions in long-term government securities. As interest rates soared higher with each 75-basis-point Fed hike in 2022, the market value of these long-term securities continued to plummet.

{kind=link}

Meanwhile, the deposit base remained largely uninsured by the FDIC (in excess of the $250,000 insured amount) and available to be drawn by depositors. As interest rates surged into 2022 and capital raising became harder, VC depositors began withdrawing their funds from the bank, causing SVB's total deposits to shrink.

If SVB had the option to simply hold these securities to maturity, they would have been fine. But deposit outflows forced them to sell the securities at a steep loss. This big hit spurred SVB to attempt to raise equity capital in order to rebalance their financial position.

But this emergency capital raise spooked depositors, many of whom had deposits well in excess of the FDIC-insured amount of $250,000, leading to a bank run as VC-backed company founders pulled millions of dollars out all at once. The deposit outflow sealed SVB's fate, as the bank quickly became insolvent.

That's when the FDIC stepped in and took receivership of SVB.

Something very similar happened with Signature Bank, which had a substantial depositor base from crypto clients.

Now that the FDIC has guaranteed 100% of deposits at these failed banks (a move that will surely be seen by some as a bailout of a high-risk sector of the economy at the expense of the rest of the banking industry), depositors of average banks around the country should be able to rest easy and refrain from rushing to pull their money out.

While nearly all regional banks have some non-FDIC-insured deposits and varying degrees of unrealized securities investment losses, most banks did not have massive influxes of deposits to put to work exactly when interest rates were at their lowest levels in history.

Take, for example, these two strong regional banks:

BHB is based out of its namesake Bar Harbor on Mount Desert Island in Maine. Though the bank is based out of a tourist town on the edge of Acadia National Park, it has branches across the Southern half of the state and has expanded into New Hampshire and Vermont.

BHB February 2023 Presentation

{kind=link}

It's a well-managed and efficiently run bank, exemplified by its 2022 efficiency ratio of 59%, 3.36% net interest margin, and 0.17% ratio of non-performing assets as a share of total assets / 0.23% ratio of non-performing loans to total loans.

I like BHB because of its dominant market position in its namesake Summer tourist town as well as its expanding presence across New England.

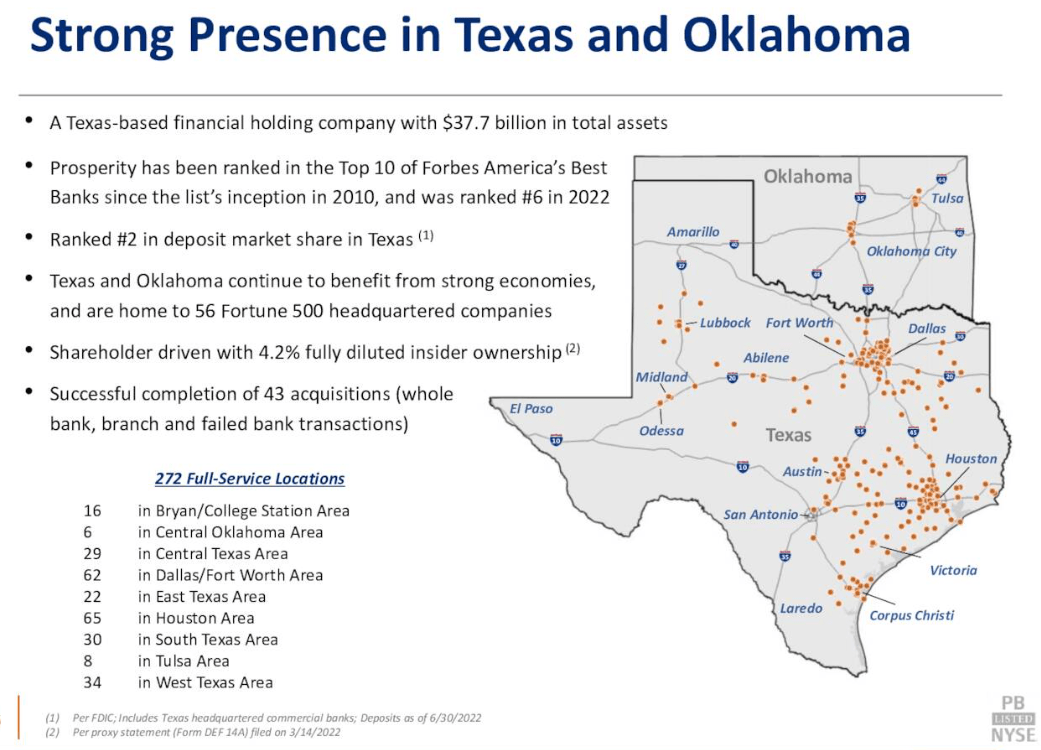

Meanwhile, PB is a fast-growing Texas bank headquartered in Houston but with a strong presence across the state and into Oklahoma. Among banks headquartered in Texas, PB enjoys the second largest market share of deposits.

{kind=link}

PB is another well-managed bank with an even lower efficiency ratio of 42.2% in 2022 and non-performing assets to total loans & owned real estate of 0.15%. While PB's net interest margin of 3.05% is lower than BHB's, there's a case to be made that PB makes up for this lower NIM with high asset quality.

I like PB because of its strong market positions in three of the fastest growing metro areas in the country: Houston, Dallas/Fort Worth, and Austin.

Both banks enjoyed healthy, normal levels of deposit growth from 2020 through 2022:

Though deposits are retracing a little bit right now, it is nowhere near the outflows suffered by SVB or Signature Bank.

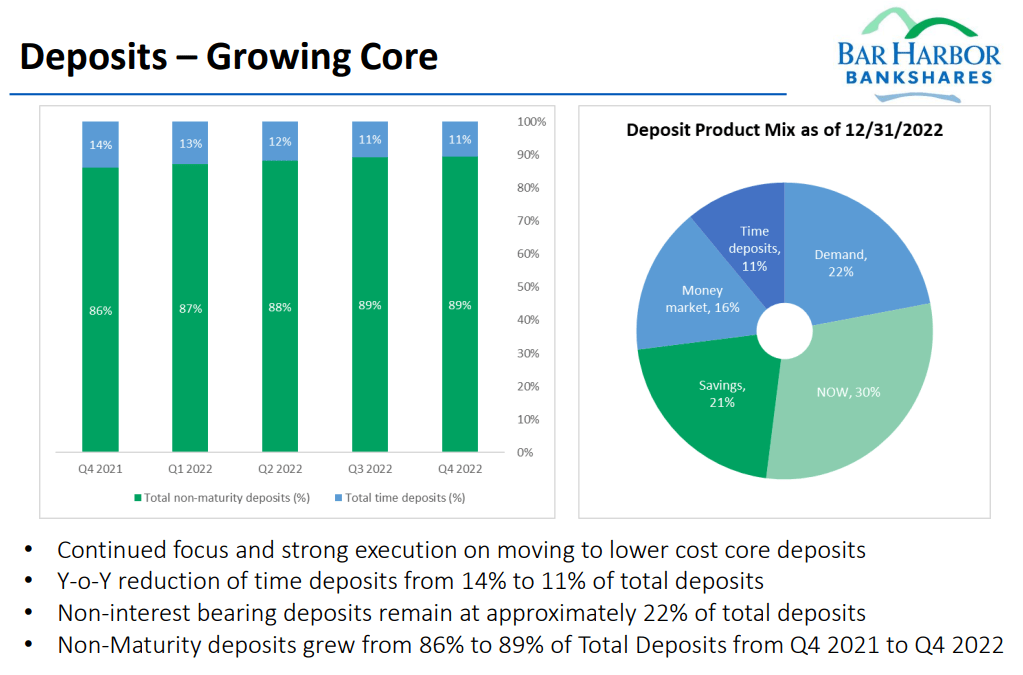

Most of BHB's deposits have no maturity, meaning that depositors could withdraw their money in droves if they wanted to. But why would they want to? BHB has a strong reputation in the region, and particularly in Bar Harbor, many of its larger depositors have been banking with BHB for decades.

BHB February 2023 Presentation

{kind=link}

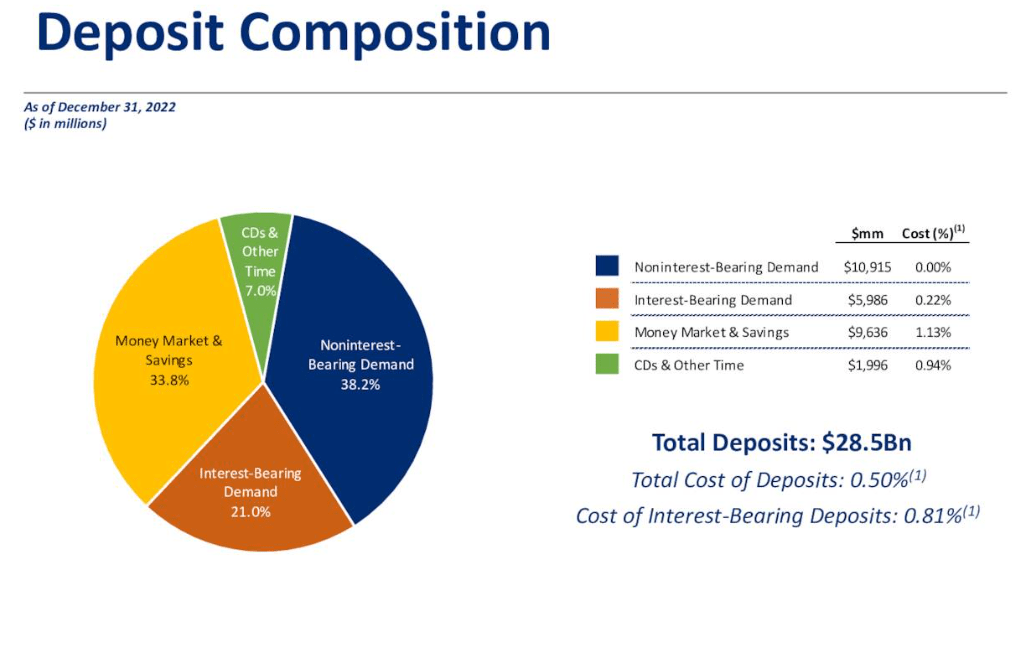

PB has an even higher amount of non-maturing deposits at 93% of the total, while its money market & savings account share of 34% is slightly lower than BHB's 37%.

{kind=link}

BHB's cost of deposits in 2022 was 0.24%, and PB's cost of deposits was almost exactly the same, rounding to 0.24%. In the fourth quarter, however, both were roughly double their average for 2022.

Meanwhile, BHB's marketable securities portfolio makes up only 14.3% of total assets, while PB's marketable securities portfolio account for a larger 38.4% of total assets.

In 2022, BHB has unrealized losses on securities of $74.4 million. When compared to a marketable securities value of $559.5 million, we find that BHB's marketable securities portfolio is sitting on an unrealized loss of 11.4%.

Here is what BHB's securities portfolio looks like arranged by maturities:

BHB 2022 10-K

Unfortunately, BHB does have quite a bit of securities maturing in 10 years or more, and it is these securities that have taken the biggest hit in fair value. But notice that the timing of some securities have been more fortunate. Bonds with maturities of between 5 and 10 years have actually appreciated in fair value.

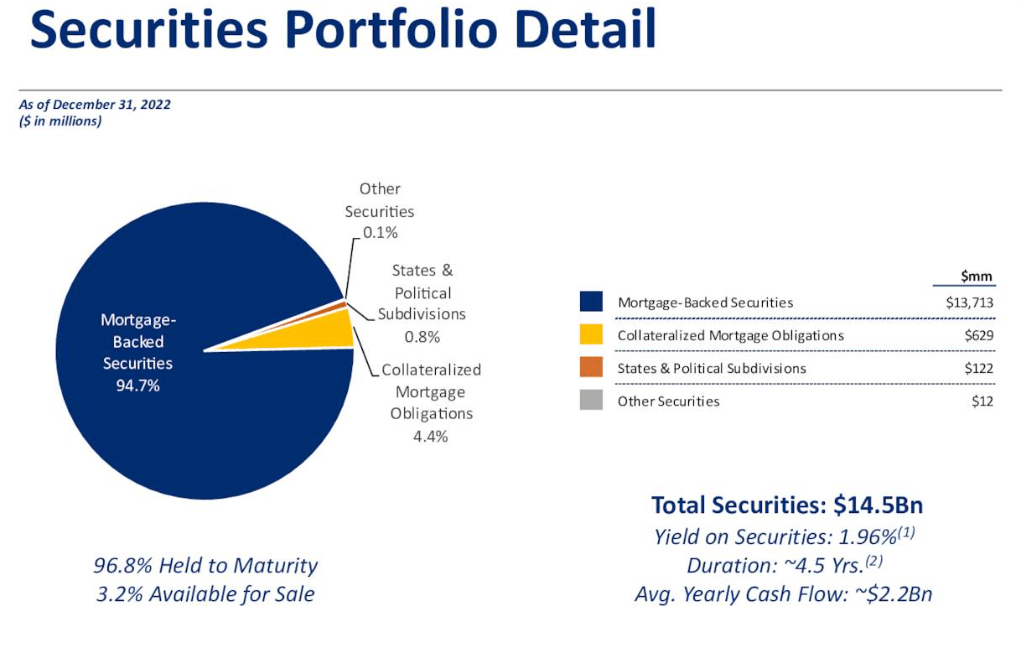

Meanwhile, PB's securities portfolio being held to maturity ended 2022 with a fair value of $12.4 billion, compared to a cost basis of $14.0 billion. That results in an unrealized loss of 11.6%.

Also, though PB's securities portfolio makes up a larger share of total assets than BHB's, PB's securities portfolio does have a lower remaining duration of ~4.5 years, compared to BHB's weighted average duration closer to 10 years.

{kind=link}

I could hold forth longer, but the preceding should suffice in demonstrating that the deposit bases and securities portfolios of BHB and PB look very different than those of the speculative tech-heavy SVB and Signature Bank.

Total Returns And Dividend Growth

Perhaps the best and simplest measure of a bank's quality is its total return performance against its peer group.

On this measurement, neither BHB nor PB disappoint. Both regional banks have handily outperformed both KRE and the broader SPDR Financial Sector ETF ( XLF ), which includes the big national banks, over the last two decades:

And both banks have done so while paying a growing dividend to shareholders.

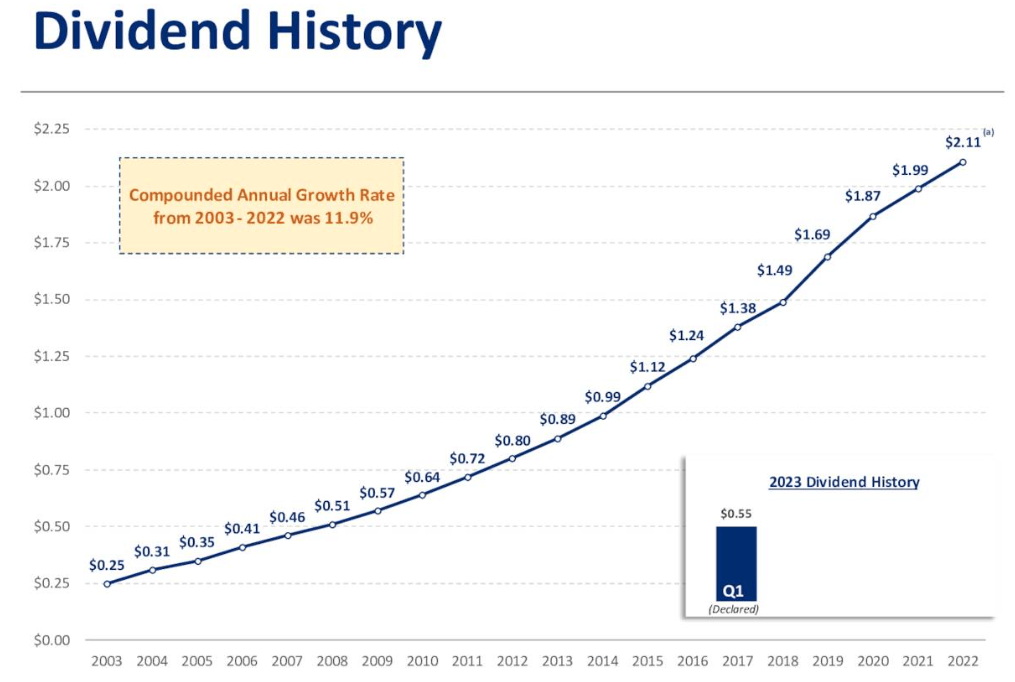

BHB has increased its dividend for 19 consecutive years (a number that should tick up to 20 years at the next dividend announcement in April) at a compound annual growth rate of about 6% over that time span. The latest hike was over 8%, though.

Currently, BHB offers a dividend yield of 3.9%, well above its 5-year average yield of 3.44%.

Meanwhile, PB has grown its dividend for 23 consecutive years at a compound annual growth rate of 12% over the last two decades. The latest hike represented growth of "only" 5.8%.

{kind=link}

Currently, PB's dividend yield of 3.4% is likewise well above its 5-year average yield of 2.74%.

Bottom Line

Not all regional banks are created equal. Most operate basically like old-fashioned savings & loan businesses, taking depositors' savings and loaning them out as home mortgages and business loans with good, solid collateral. Most of these kinds of banks are not susceptible to the same downfall that SVB and Signature Bank suffered.

The few banks that are failing right now have one thing in common: Their deposit bases surged massively during the speculative tech boom of 2021, when lots of money was chasing ridiculous, unprofitable tech and crypto ventures.

But the unprofitable ventures haven't really been the problem. SVB and Signature didn't fail because of bad loans. They failed because that influx of depositor money was invested in long-term securities at exactly the all-time low in interest rates, exposing them to bigger losses as the market value of those securities dropped with rising interest rates.

Your average regional bank, such as BHB or PB, did not see such a massive surge in deposits in 2021 and therefore did not have nearly the same capacity as SVB or Signature to invest in securities at ultra-low interest rates.

Of course, I do not see why the bank managers did not simply invest in shorter maturity securities rather than locking in ultra-low interest rates at multi-year terms. Perhaps they were reaching for yield, or perhaps they genuinely did not foresee interest rates rising significantly from the level at which they bought the securities.

In any case, BHB and PB are not SVB and Signature. They are solid banks with much less risk.

For dividend growth investors, these are two regional banks I recommend considering.

For further details see:

2 Dividend-Growing Regional Banks To Buy In The Banking Panic