ESGR - 2 Extremely Mispriced Undervalued Preferred Stocks In The Insurance Sector

- We present two preferred stocks that we believe are bargains relative to other preferred stocks with the same credit ratings.

- The first is very high quality, has a higher yield than other similar quality preferred stocks, and has huge upside price potential.

- The second is the most undervalued preferred stock in the entire stock market now, based on current yield.

Co-produced with Preferred Stock Trader

Introduction

One of the ways we identify undervalued preferred stocks is to screen all preferred stocks within the various credit ratings to find outliers. In this case, we screened fixed-rate preferred stocks that pay " qualified" dividends from high-quality investment-grade companies . We believe we have found two excellent undervalued preferred stocks.

Athene Holdings Preferred Stock - Yield 5.9%

Athene Holding Ltd 4.875% Series D Non-Cumulative Preferred Shares ( ATH.PD )

Athene Holdings is an insurance company that specializes in retirement products. It offers annuities, re-insures annuities, and offers other savings products. It is owned by Apollo Global Management ( APO ) which is a strong "A-" rated company. Athene also has its own separate rating which is the same "A-" credit rating. Athene Preferred "D" shares, symbol ATH-D , is one of two fixed-rate preferred stocks issued by Athene.

As is typical, the preferred stocks of Athene are rated two notches lower than their "A-" rated unsecured bonds, a rating of "BBB". So even the preferred stocks of Athene are investment grade. There are only two corporations that have issued preferred stocks with higher credit ratings than Athene at "BBB+", just one notch higher than ATH-D. So ATH-D is an extremely strong preferred stock. Here is how ATH-D stacks up against other "BBB" rated preferred stocks.

Author's screenshot

As can be seen from the chart, only AAM-A and AAM-B have higher yields, but AAM-A is callable now and trades well over par. Thus, a loss will occur on a call and it is hard to imagine any price upside from its current price. AAM-B will be callable soon and carries only a 0.3% yield-to-call. Again, we see nothing attractive here.

ATH-D, on the other hand, has huge upside price potential at its current price of $20.64, and its current stripped yield is better than all of the remaining "BBB" preferred stocks, even those with little or no price upside.

ATH-D is also quite undervalued even versus its sister preferred ATH-B ( ATH.PB ). Normally, the preferred stock with less price upside (ATH-B) has a higher current yield to compensate. But in this case, we have a reverse of normal. Despite a hugely better price upside situation with ATH-D, ATH-D also provides you with a higher current yield than ATH-B. This is a pretty big mispricing in favor of ATH-D. It is hard to understand why investors would be buying ATH-B when ATH-D is better in every way. So the out-of-whack market pricing we are seeing provides an excellent opportunity here.

And just to drive home the ATH-D gross undervaluation thesis, we looked at REIT preferred stocks. Most are unrated but KIM-L and KIM-M are "BBB-", one notch lower than ATH-D and Moody's has them equivalent to ATH-D. The current yield on these KIM preferred stocks is around 5.2% versus 5.9% for ATH-D, and KIM preferreds have nowhere near the upside price potential of ATH-D as they trade around par. And to make it worse for KIM preferreds, their dividends are not qualified and thus taxed at a higher rate than the ATH-D dividends.

If ATH-D traded with the average yield of "BBB" preferred stocks, around 5.5%, it would trade at $22.25 and would still have more price upside than most of its peers. Thus, we consider the current fair value of ATH-D to be at least $22.00 per share.

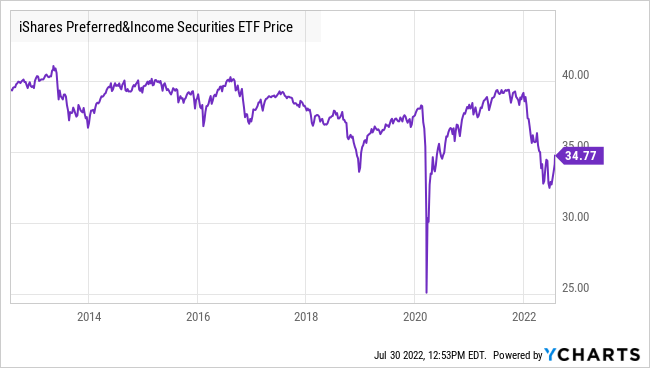

After the large fixed-income selloff we have seen, we are particularly focused on undervalued preferred stocks with large capital gains potential. In every past selloff, preferred stocks have ultimately rallied back to par.

{kind=link}

As can be seen above on the 10-year PFF price chart, every selloff has been followed by a very strong rally. Whether it was the 2013 taper tantrum, the 2016 and 2018 selloffs, or the COVID selloff, they were all followed by sharp rallies. And of course, in 2008, many preferred stocks rallied 300% to 400% from their bottoms to get back to par.

In our macro view, we believe that the Fed rate hikes will ultimately damage the economy, pushing the U.S. into recession and cutting consumer demand. The higher prices for essentials like food and energy are already reducing consumers' ability to buy anything other than the basics. Recently, AT&T reported disappointing earnings because their customers are having trouble paying their cell phone bills. Walmart also reported a terrible quarter. These are bad indicators for the economy in general.

Once consumer demand is crushed, the supply chain issues should resolve themselves and inflation should come down substantially. The market seems to also believe this scenario which is why long-term interest rates have dropped so much in the past weeks. Ultimately, fierce global competition will reassert itself keeping prices in check as it has over the last 30 years.

We believe that ATH-D could easily see a 15% total return over the next 12 months and will ultimately return close to par.

One of the reasons ATH-D is one of the best ways to play this is that they are relatively recession resistant. In fact, most of Athene's assets are invested in high-quality corporate bonds which have been rallying. Thus, ATH is a beneficiary of a lower long-term interest rate environment that a recession is likely to bring about.

Although we mostly consider ATH-D to be a total return story (capital gains plus current yield), we should not forget that the current yield is high relative to peers and is "qualified" for a lower tax rate. Thus, the after-tax yield of ATH-D is currently equivalent to a 6.6% bond if you are in the 24% tax bracket and a 7.2% bond after-tax yield if you are in the 32% tax bracket. Try to find a "BBB" bond that provides a 7.2% yield, or even a 6.6% yield. If you do, certainly put it in the comment section and I will be a buyer.

To play this coming rally, and the high total returns that will result, we believe that you want to be in high-quality names. Preferred stocks from cyclical companies or poor credit names will likely not participate in this rally due to the increased operational and credit risk that comes with a recession.

Enstar Group Preferred Stock - Yield 7.0%

Enstar Group 7.00% Series E Perpetual Redeemable Non-Cumulative Preferred ( ESGRO )

Enstar Group ( ESGR ) is also an insurance company but it operates as a property/casualty insurance company specializing in the business of runoff. That is, they take over insurance companies that want to close up shop but still have policies (obligations) outstanding that makes it impossible to cease operations. ESGR captures the payments on these outstanding policies until these policies expire.

ESGR has one fixed-rate preferred stock with the symbol ESGRO . Like ATH-D, ESGRO is also a "qualified" dividend payer. ESGR has an investment credit rating of "BBB" which means that ESGRO preferred stock has a credit rating of "BB+". Below is a chart that shows that ESGRO is extraordinarily undervalued relative to all of the other fixed-rate "BB+" rated preferred stocks.

Author's screenshot

As you can see, ESGRO's 7.17% current stripped yield is outstanding, even relative to the 2nd best "BB+" rated preferred stock. And it has a yield that is more than 2% better than the lowest yielder among the "BB+" rated preferred stocks. To put it another way, ESGRO has a yield that is a whopping 40% better than FITBO.

In my research, ESGRO is the most undervalued preferred stock in the market using the current yield relative to its credit rating group. If it traded at a 5.7% yield, which is still about average for "BB+" rated preferred stocks, it would trade at $31.00. Of course, due to the fact that it is eventually callable at $25.00, it will never trade that high. But it did trade as high as $27.50 eight months ago before the fixed-income market went into a tailspin.

One of the great things about being so undervalued is that the downside price risk of ESGRO should be extremely low relative to other preferred stocks.

While we're looking at the chart of "BB+" preferred stocks, it also highlights the huge undervaluation of ATH-D . Although "BB+" preferred stocks are rated two notches below ATH-D's very strong "BBB" credit rating, ATH-D still has a higher yield than most "BB+". Why would you buy any of these "BB+" preferred stocks (except ESGRO) when you can buy ATH-D with a similar or better yield, a higher credit rating, and more price upside than most of these "BB+" preferred stocks.

And to emphasize the value of ESGRO's qualified dividend payments, its after-tax yield is equivalent to a 7.9% bond if you are in the 24% tax bracket and an 8.7% bond if you are in the 32% tax bracket.

Shutterstock

Summary/Conclusion

One of the best ways to find undervalued fixed-income securities is to screen them within various credit ratings to find the outliers. Our screening has turned up two high-quality "qualified dividend" paying preferred stocks that are extraordinarily undervalued relative to their credit-rating peers.

"BBB" rated ATH-D is an excellent buy based on its current yield relative to peers, and a super buy based on total return potential. We believe that the coming recession will continue to bring down long-term interest rates which could boost ATH-D's price by more than 20% over time. ATH-D has even better yield metrics than most preferred stocks with credit ratings two notches below that of ATH-D. We have the current relative fair value of ATH-D at $22.00 with the belief that it will ultimately trade much higher than that.

ESGRO is also extraordinarily undervalued relative to its "BB+" rated preferred stock peers. In fact, our work shows that it is the most undervalued preferred stock in the market based on current yield within its credit rating group. If it wasn't callable, fair market value would be $31.00 and it traded as high as $27.50 just eight months ago before the fixed-income market started to sell off.

For further details see:

2 Extremely Mispriced, Undervalued Preferred Stocks In The Insurance Sector