PHM - 2 Incredible Dividend Blue Chips Potentially Set To Soar And Too Cheap To Ignore

- This bear market probably isn't over, but even if the market has bottomed, it's always and forever a market of stocks, not a stock market.

- LNC and PHM are two incredible dividend blue chips trading at 5X earnings, priced as if we were already in a severe recessionary bear market low.

- LNC is a very safe 3.4% yielding A-rated insurance company growing at 12% trading at 5.5X earnings.

- PHM is trading at the lowest P/E in 20 years, 4.5X earnings. The last time it was this cheap, it delivered 57X returns over the next 15 years.

- Both LNC and PHM represent deep value, anti-bubble "fat pitch" investing done right. They offer 50% annual return potential over the next three years. More importantly, within a diversified and prudently risk-managed portfolio, they could turbocharge your returns and help you retire in safety and splendor.

Many of us are eager to "be greedy when others are fearful." Or at least we say we are. Who doesn't want to score a Buffett-like blue-chip bargain when the market is selling off a blind panic?

{kind=link}

YCharts

A lot of people, and not just those who are terrified the market will keep on falling lower. I've recently heard from some Dividend Kings members who are 10% to 62% in cash because it seems just so obvious that stocks have to fall lower.

Why? There are so many reasons.

- the 2-10 yield curve is now 44 basis points inverted, the most since August 2000

- that means the bond market is the most confident in 22 years that a recession is coming relatively soon

- the Fed is hiking at the fastest rate in 40 years

- some analysts (like Cambridge's Mohamed A. El-Erian) think the Fed will hike 75 points three more times by the end of the year (4.5%)

- the Fed has never succeeded in achieving a soft landing when inflation started above 5% (it's 9.1% now)

- the economic data says a recession MIGHT begin in 4.5 to 5 months

- the average recessionary bear market bottom is -36% since 1960

- the blue-chip consensus is that if we get a recession, stocks bottom at -30% to -53%, depending on its severity

- that's potentially 18% to 45% lower than now

But do you know what? It's possible that we might still avoid a recession and that June 16th's -24% low on the S&P 500 was the ultimate bottom.

How on earth is that possible? As Citigroup points out , there's still a road to a soft landing for the Fed.

- the job market is so strong that consumers have plenty of money to spend

- gas prices have fallen 20% from their peak, and consumer sentiment is likely to rise as a result

- supply chains are steadily de-tangling themselves, and commodity prices are falling rapidly

- the Fed hiking to 4% or even 5% is no guarantee of a recession

- in the 1990s, we had rates as high as 6% with a booming economy

And even IF we get a recession, Goldman and Citi still think the June 16th bottom might have been as low as stocks fall. How on earth is that possible?

{kind=link}

Ben Carlson

Because in the 1953 recession, stocks fell only 15%, not a bear market.

In the 1957 recessionary bear market, stocks fell 21%, just as they did in the 2018 bear market with no recession.

In the 1960 recession, stocks fell about what they have so far.

In the 1980 recession, they fell 17%, less than in 2011's and 2018's non-recession bear markets.

In 1990 the market narrowly avoided a bear market entirely.

Does it make logical sense for stocks to have bottomed on June 16? To many investors, it doesn't seem so. It seems so obvious that stocks just have to fall a lot more than it might seem reckless or even downright stupid to be buying stocks right now.

The main purpose of the stock market is to make fools of as many men as possible." - Bernard Baruch

When everyone agrees on the same thing on Wall Street, often the opposite happens.

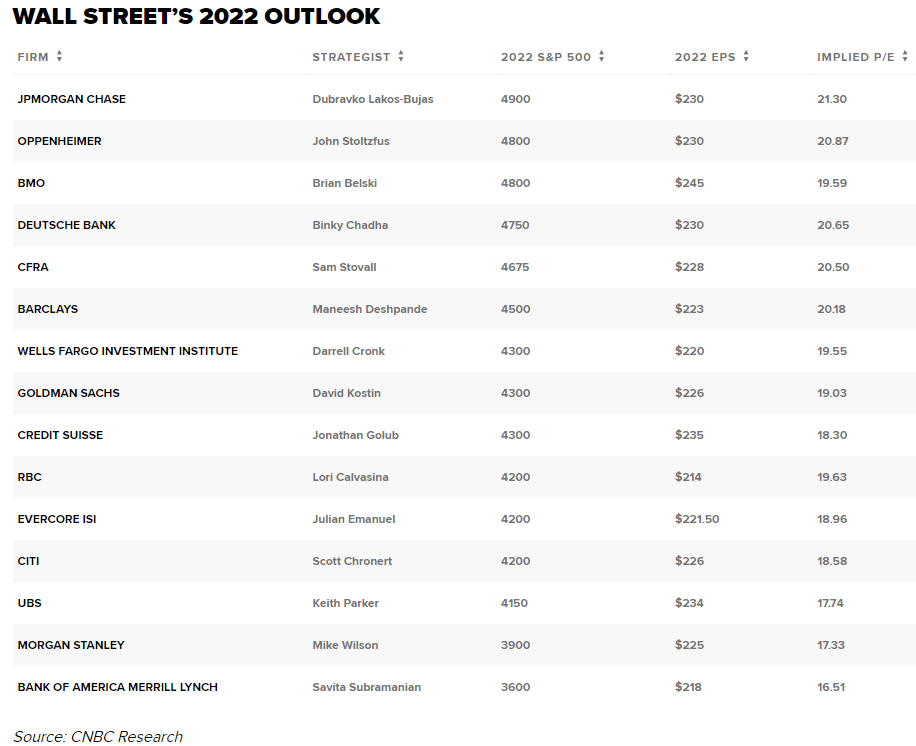

Does that mean that the current rally is destined to continue? Potentially all the way to new record highs? JPMorgan believes so, with a 4,900 price target on the S&P for the end of the year.

- new record highs this year

- the bear market lasting less than a year

- and potentially followed by a 2023 bear market

{kind=link}

But what if neither extreme is right? What if the job market is too strong for the Fed to stop tightening but not weak enough for us to fall into a recession? What if stocks just trade sideways for a year, cycling up or down a bit but never hitting new highs or lows?

Sounds crazy right? But in this Pandemic, we've seen a lot of crazy things that once were thought impossible.

{kind=link}

Business Insider

On April 20, 2020, oil hit -$38 per barrel for a single day. So is it crazy to believe there is at least a chance that stocks don't make anyone look like a genius in the next year?

Is it implausible to think the market might frustrate the bulls AND the bears?

In that case, there will be no winners.. . except for:

- long-term investors who ignore this crazy noise and just hold

- dollar-cost averagers

- dividend re-investors

- individual blue-chip bargain hunters

It doesn't take a recessionary bear market low for great dividend blue-chips to trade at crazy low valuations.

So let me show you why you might want to consider today PulteGroup ( PHM ) and Lincoln National ( LNC ) are two incredible bear market blue-chip bargains.

Both are rapidly growing companies, and both trade at under 5X earnings today, pricing in deeply negative growth.

This creates the opportunity for Buffett-like return potential from blue-chip bargains hiding in plain sight.

- including the potential for 50% CAGR returns through 2024

- and a quadruple within five years

Lincoln National: One Of The Best Insurance Companies You've Never Heard Of

Further Reading:

- Lincoln National: A Buffett-Style Anti-Bubble Hidden Gem

- a comprehensive look at LNC's investment thesis, growth outlook, risk profile, valuation, and total return potential

Reasons To Potentially Buy LNC Today

- 87% quality low-risk 12/13 Super SWAN (sleep well at night) insurance company

- the 121st highest quality company on the Master List (76th percentile)

- 90% dividend safety score

- 12-year dividend growth streak (every year since the Great Financial Crisis)

- 3.9% very safe yield

- 0.5% average recession dividend cut risk

- 1.5% severe recession dividend cut risk

- 28% historically undervalued (potential very strong buy)

- Fair Value: $80.24

- 5.5X forward earnings vs. 8.5X to 9.5X historical (Anti-bubble blue-chip priced for -6% growth)

- A- negative outlook credit rating = 2.5% 30-year bankruptcy risk

- 70th industry percentile risk management consensus = good

- 7% to 17% CAGR margin-of-error growth consensus range

- 12.3% CAGR median growth consensus

- 5-year consensus total return potential: 20% to 29% CAGR

- base-case 5-year consensus return potential: % CAGR (X more than the S&P consensus)

- consensus 12-month total return forecast: 30%

- Fundamentally Justified 12-Month Returns: 76% CAGR

LNC 2024 Consensus Total Return Potential

{kind=link}

(Source: FAST Graphs, FactSet)

If LNC grows as expected and returns to its historical 9X earnings, it could triple by 2024 and deliver 51% annual total returns.

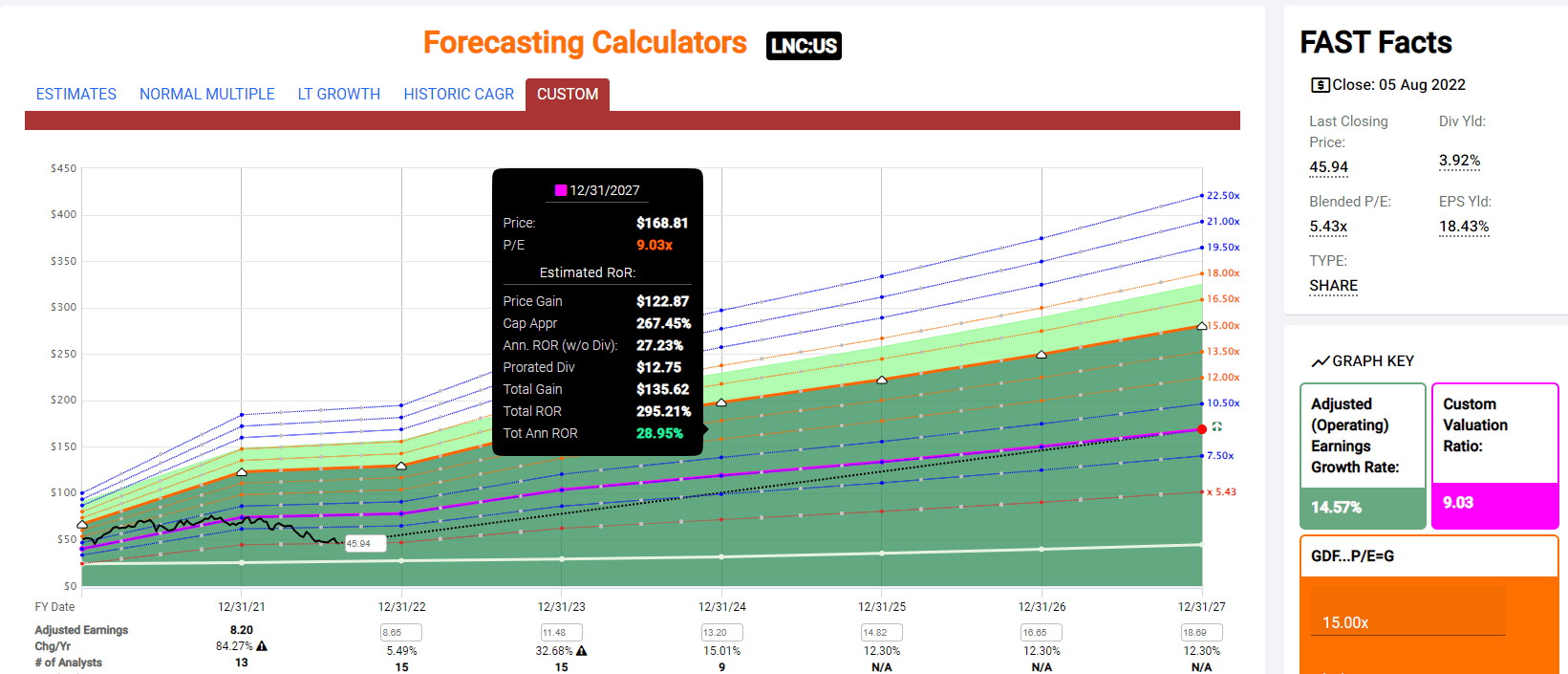

LNC 2027 Consensus Total Return Potential

{kind=link}

(Source: FAST Graphs, FactSet)

If LNC grows as expected through 2027 and returns to its historical 9X earnings, it could quadruple and deliver 29% annual returns.

- Buffett-like returns from a blue-chip bargain hiding in plain sight

Why is LNC such an incredible bargain?

{kind=link}

FAST Graphs, FactSet

Because it's priced as if we were in a severe recession, the only times it's traded at such a low P/E is during the Pandemic, the GFC, and the 2011 bear market, a recession scare that began with the market trading at 13X earnings.

Won't falling interest rates hurt insurance companies' ability to grow earnings?

{kind=link}

YCharts

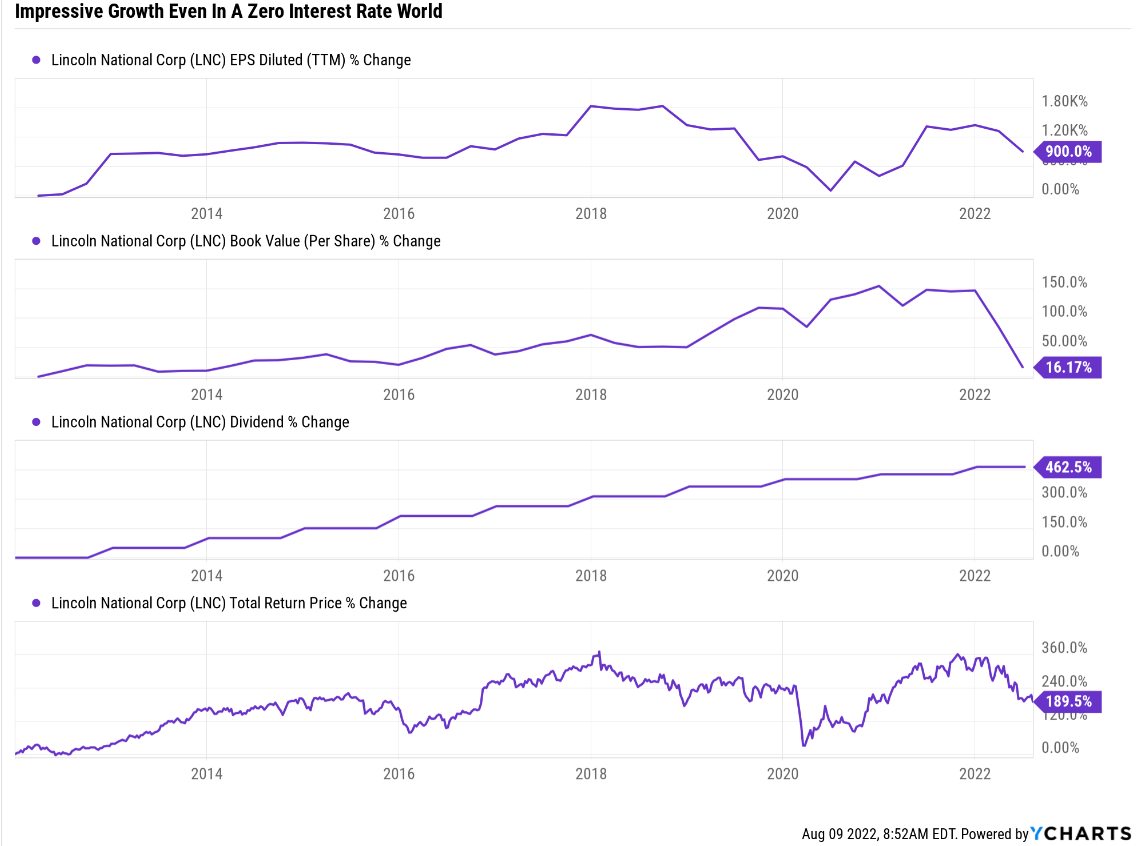

A-rated insurance companies like LNC have come out of a decade of stricter regulations and interest rates that were the lowest in human history.

LNC managed to grow its earnings 900% over the last decade and its dividend by almost 6X.

And that was in the worst possible interest rate environment in the history of the insurance industry.

Moody's expects 10-year treasury yields to normalize to 4% over time, which would be a boon to the insurance industry.

- their cost of capital is basically insurance float, i.e. "free"

- and long-term yields determine the net yields on their investment portfolios

- rising rates = pure profit for insurance companies

What if Moody's is wrong and 10-year yields don't go back to 4%?

FactSet Research Terminal

The FactSet blue-chip economist consensus is for 10-year yields to crash in 2025, possibly due to growth concerns and increased bond demand from retirees.

However, if rates simply normalize to the 2% to 3% range we saw in the 2010s, as economists expect, then LNC will still be able to keep growing at its 8% to 9% post-GFC rate.

For a company priced at 5.5X earnings, literally some of the lowest valuations in its history, LNC is a very compelling high-yield value proposition.

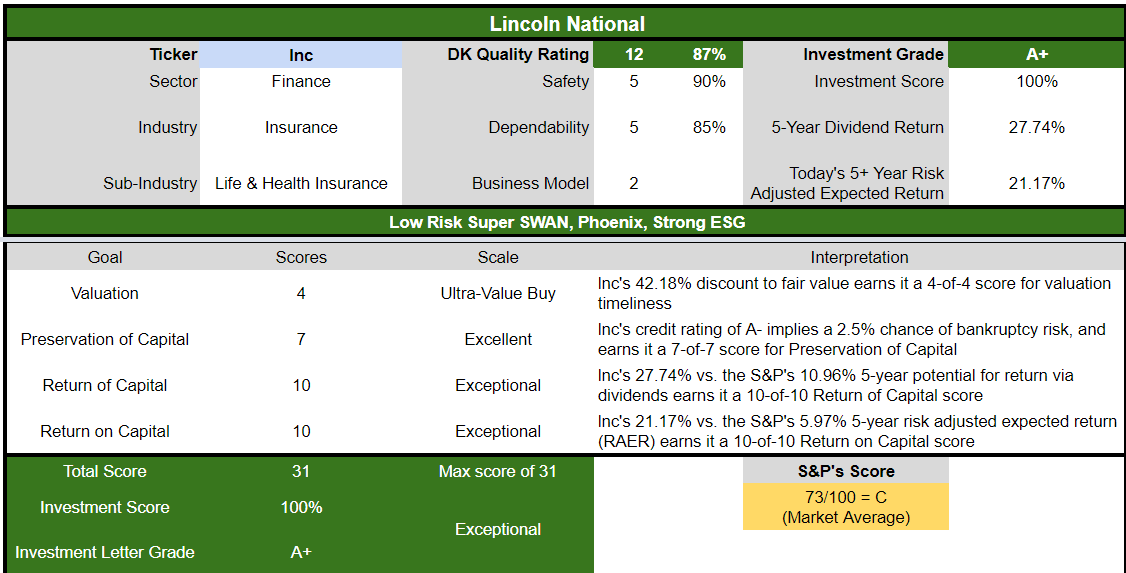

LNC Investment Decision Score

{kind=link}

DK

{kind=link}

(Source: DK Automated Investment Decision Tool)

LNC is an exceptional, high-yield monthly blue-chip option for anyone comfortable with its risk profile.

- 42% discount vs. 5% market premium = 47% better valuation

- 3.9% yield vs. 1.6% yield

- 70% better consensus long-term return potential

- 3.5X better risk-adjusted expected return over the next five years

- 2.5X higher consensus dividends over the next five years

And what if long-term rates do come down significantly in the coming years? Then guess what's likely to benefit? Home builders.

PulteGroup: Double-Digit Growth That's Crazy, Stupid, Cheap

Further Reading:

- PulteGroup Is A Table Pounding Strong Buy

- a comprehensive look at LNC's investment thesis, growth outlook, risk profile, valuation, and total return potential

Reasons To Potentially Buy PHM Today

- 78% quality medium-risk 12/13 Super SWAN (sleep well at night) home builder

- 84% dividend safety score

- 2-year dividend growth streak

- 1.4% very safe yield

- 0.5% average recession dividend cut risk

- 1.85% severe recession dividend cut risk

- 35% historically undervalued (potential very strong buy)

- Fair Value: $67.16

- 4.5X forward earnings vs. 10.5X to 11.5X historical (Anti-bubble blue-chip priced for -9% growth)

- 4.3X cash-adjusted trough earnings (factoring in the recession)

- BBB- stable outlook credit rating = 11% 30-year bankruptcy risk

- 56th industry percentile risk management consensus = average

- 8% to 13% CAGR margin-of-error growth consensus range

- 11% CAGR median growth consensus

- 5-year consensus total return potential: 24% to 30% CAGR

- base-case 5-year consensus return potential: % CAGR (X more than the S&P consensus)

- consensus 12-month total return forecast: 22%

- Fundamentally Justified 12-Month Returns: 57% CAGR

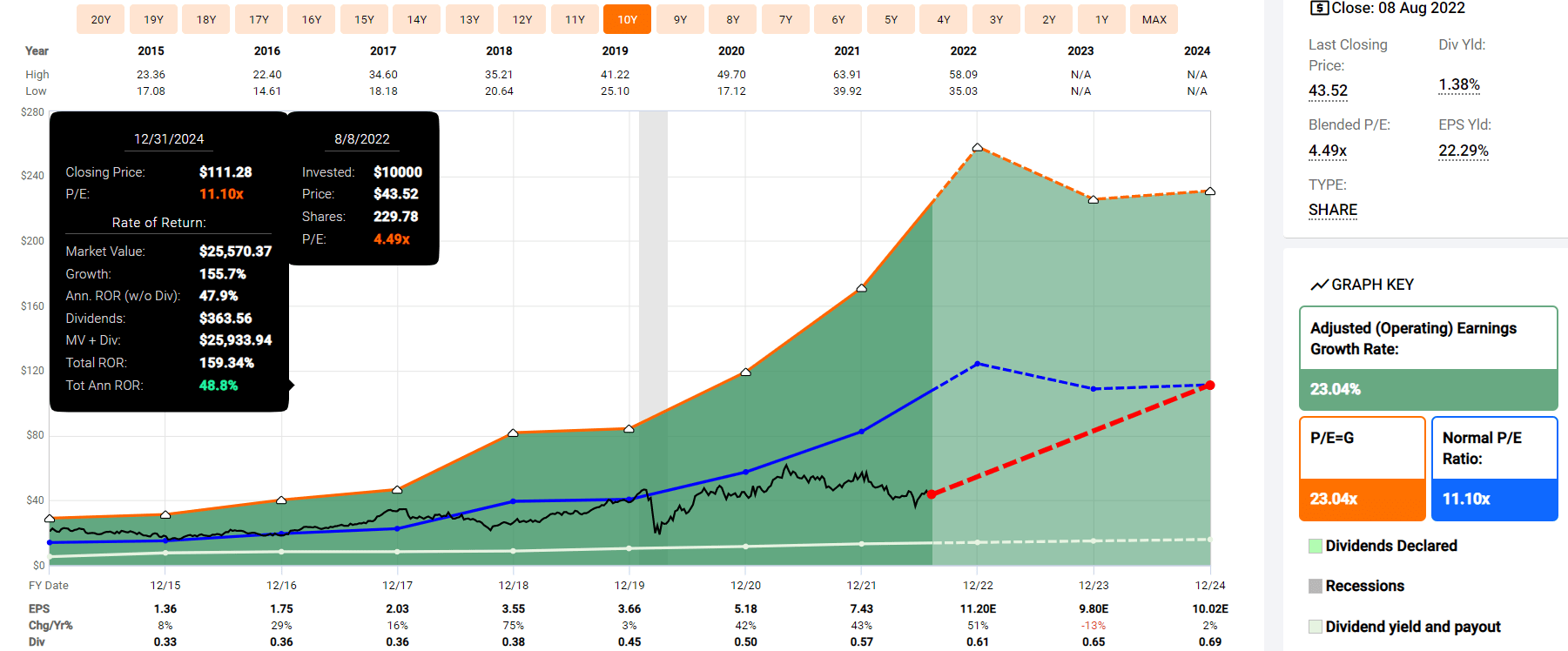

PHM 2024 Consensus Total Return Potential

{kind=link}

FAST Graphs, FactSet

If PHM grows as expected and returns to its historical P/E multiple, it could almost triple by 2024 and deliver 49% annual total returns.

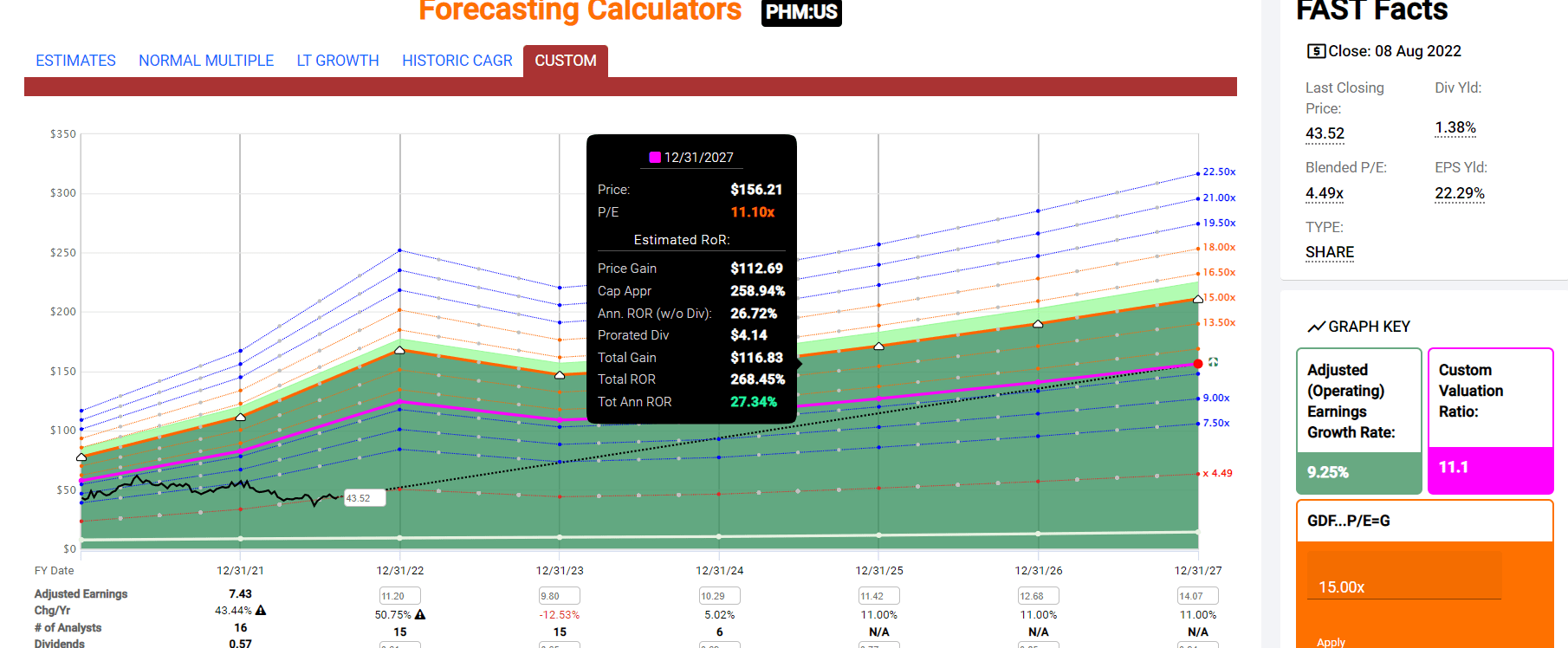

PHM 2027 Consensus Total Return Potential

{kind=link}

FAST Graphs, FactSet

If PHM grows as expected through 2027 and returns to its historical P/E, it could almost quadruple and deliver 27% annual returns.

- Buffett-like returns from a blue-chip bargain hiding in plain sight

Why is Pulte such a potential Buffett-style anti-bubble "fat pitch?"

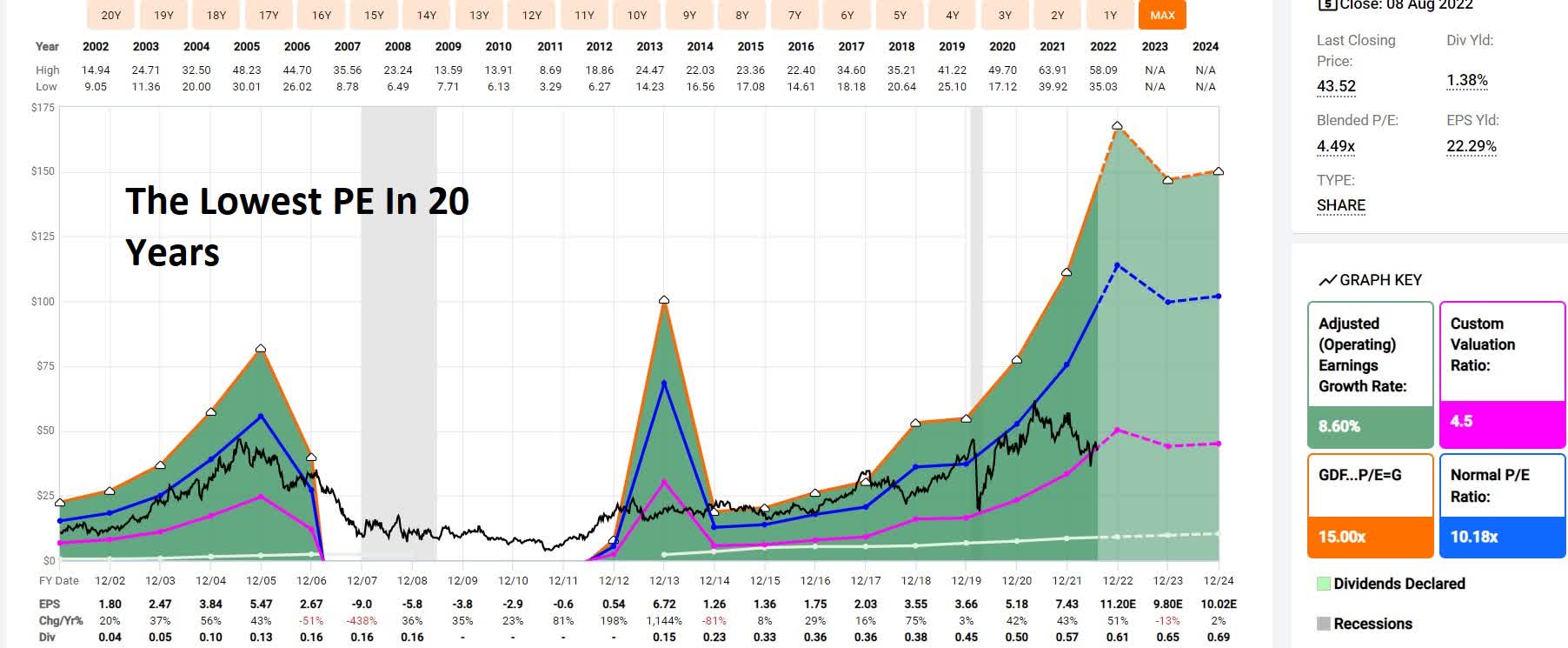

{kind=link}

FAST Graphs, FactSet

Because it's trading at a lower P/E than during the Pandemic crash and at the best P/E in 20 years. Is the housing market dead? Maybe in the short term, but the long-term demographics are exceptional.

Morgan Stanley thinks that housing will see a 10-year to 20-year secular mega-boom, and here's why.

-

There are 150 million Millennials and Gen Zers vs. 75 million boomers

-

And over the next 20 years, they will almost all be starting families and reaching peak earnings

The Census Bureau estimates that the US needs 1.5 million new housing starts each year to keep up with the population demand. But since the Great Recession, from 2007 through 2020, we've had fewer housing starts than this. To be precise, a total supply shortfall of between 3 million and 5 million homes.

Do you know what this means? If home builders increased capability by 33% to 2 million per year, it could take up to 10 years to close the supply gap.

What does this potentially mean for Pulte?

- $1.8 billion in consensus buybacks in 2022 and 2023: 10% of existing shares

A continued supply shortage for as the next few years, if not the next decade.

And of course, let's not forget that long-term rates are expected to fall significantly in the coming years (2.2% consensus in 2025).

Pulte is the ultimate blue-chip coiled spring and is literally trading at the best P/E in two decades.

Over the long term, analysts expect PHM to deliver 12.5% CAGR long-term returns.

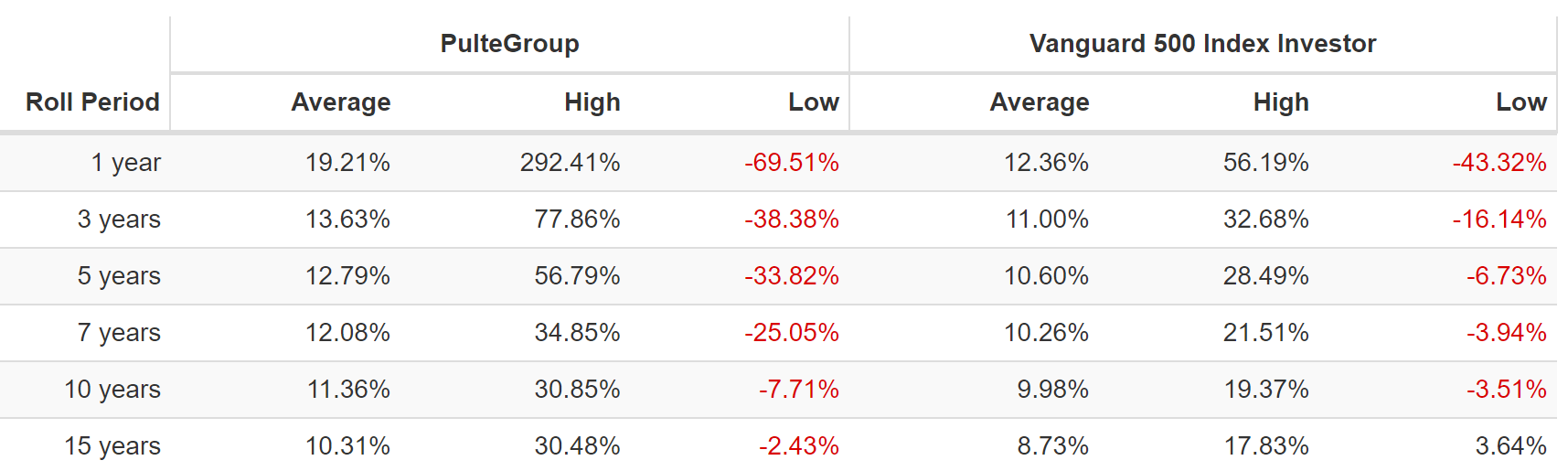

PulteGroup Rolling Returns Since 1985

{kind=link}

(Source: Portfolio Visualizer Premium)

That's similar to its average rolling returns over the last 37 years.

But from bear market lows? Like we're in now? PHM is capable of 31% annual returns for the next 10 to 15 years.

- 57X return potential over 15 years

You don't need crypto to achieve life-changing, mind-blowing gains - you just need the ultimate coiled spring blue-chip bargain.

Bottom Line: Whether The Market Trades Up, Down, or Sideways, These 2 Dividend Blue-Chips Are Potentially Set To Soar And Too Cheap To Ignore

Is the bear market over? Most economists don't think so - historically, the worst is yet to come.

{kind=link}

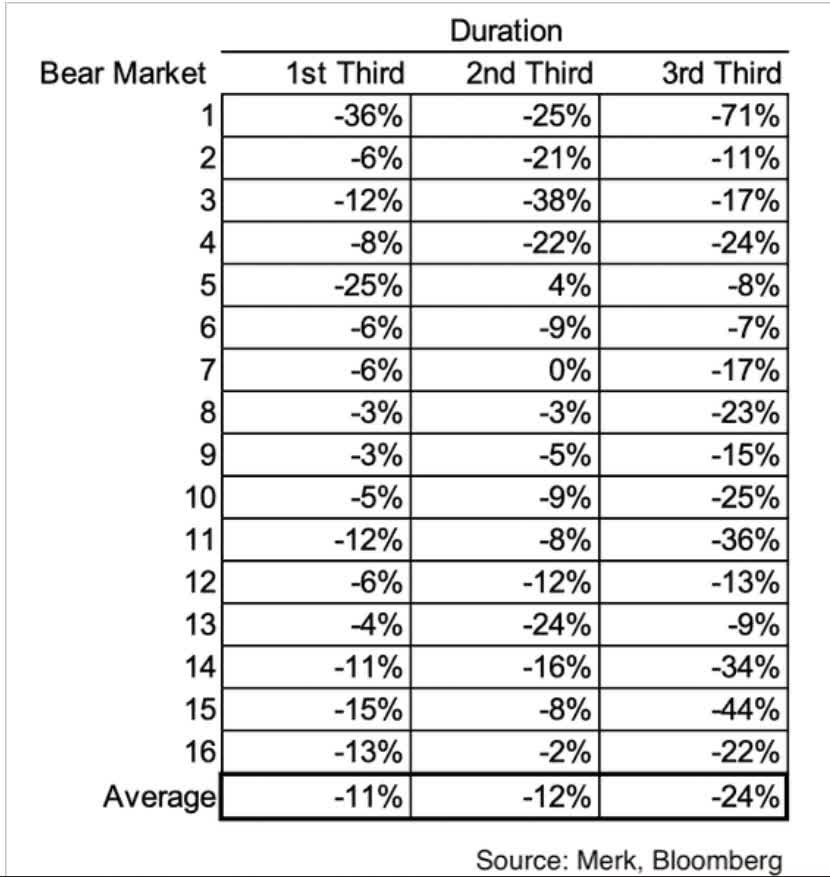

Daily Shot

60% of historical bear market downturns tend to be in the final third of a bear market.

That's why it's important to be prepared for anything, whether stocks trade up, down, or sideways.

If we get a recession and stocks fall another 20% to 40%? Then everything will go on sale.

If we avoid recession and June 16 proves to be the ultimate low? Well then LNC and PHM are still trading at valuations you only ever see in severe recessionary bear market lows.

It's always and forever a market of stocks, not a stock market. Something great is always on sale, and in the case of LNC and PHM, they aren't just on sale; they are face slapping, table pounding, potentially great buys.

I have no interest in value traps or cigar butts. A dying business is of no interest to me even at 2X earnings. But 5X earnings for world-class businesses like these growing at double-digits? Now that's something I can get excited about.

The difference between great deep value investing and the next bankrupt piece of trash is pure fundamentals, margin of safety, and prudent risk-management.

For anyone comfortable with LNC and PHM's risk profiles, these are two incredible dividend blue-chips potentially set to quadruple within five years.

For further details see:

2 Incredible Dividend Blue Chips Potentially Set To Soar And Too Cheap To Ignore