CUZ - 2 New Buy Alerts With 10% Monthly Dividend Yield And Potential Upside

Summary

- REITs are cheap today.

- Some are so cheap that they trade at a near 10% dividend yield.

- We highlight 2 such high-yielders that pay monthly dividends.

Before I get started, let me clarify that I have not yet invested in these REITs.

I recently upgraded them to a "Buy" rating after doing some more due diligence, and we are considering initiating a position at High Yield Landlord, but for now, we are still favoring other REITs to which we give a "Strong Buy" rating.

What REITs ( VNQ ) are we here talking about?

The first one is SL Green ( SLG ) and the second one is Broadmark Realty Capital ( BRMK ).

Both yield around ~10% at the moment and that's despite cutting their dividend in 2022. They yield so much because their share prices have recently collapsed:

We think that they both offer good risk-to-reward to investors who have a higher tolerance for risk, and below we explain why that is:

SL Green

SLG is an office REIT that owns Class A properties in New York City.

The office sector is experiencing very significant uncertainty right now due to the growth of remote/hybrid work. Companies are rethinking their office footprint and many are deciding to not renew their leases or at the very least, downsize their current offices.

That has caused all office REITs to collapse. Boston Properties ( BXP ), Cousins Properties ( CUZ ), and Paramount ( PGRE ) are all down very significantly because of that:

But SLG has done even worse than its peers because NYC is even more heavily affected by this uncertainty than other markets.

NYC is expensive, it is cold, it has high taxes, and if you can work remotely, why would you stay there?

That's what a lot of business owners / wealthy individuals are now asking themselves, and some are making the decision to move down south to Florida.

Just to give you a few examples: JPMorgan ( JPM ), Blackstone ( BX ), and Goldman Sachs ( GS ) have all shifted a lot of their hiring/growth projects to Florida instead of NY. Billionaire investor Carl Icahn is relocating his entire asset management firm there...

This is the main reason why we decided to sell our position in SLG in April of 2021 at High Yield Landlord. Back then it still traded at $72... and the risk-to-reward wasn't particularly appealing.

High Yield Landlord

But today, the share price is less than half of that.

SLG is back down to its Covid lows, trading at just $34 per share, and I think that the risk-to-reward is getting compelling for long-term-oriented investors:

Yes, New York City is experiencing some pain right now, but it is not going anywhere. I think that the following quote is very fitting to SLG:

“The death knell has been sounded for cities many times in the past—the future of New York alone was questioned by many during the fiscal crisis of the 1970s, the crime waves of the 1980s and 1990s, the aftermath of 9/11 and the Global Financial Crisis. Of course, New York not only weathered these storms but emerged stronger, for one simple reason: People young and old want to enjoy the vibrancy of a great city.” Bruce Flatt of Brookfield ( BAM )

Eventually, NYC will bounce back and the demand for office space also won't disappear.

Remote work is a good addition to the office space, but it is not a complete replacement in most cases. Zoom calls ( ZM ) are great, but you still need to also meet in person to train people, collaborate, brainstorm, and close deals.

The office sector will go through a transformation phase, but I have little doubt that SLG's Class A assets will still remain very desirable for major global companies like Amazon (AMZN) and Google ( GOOG ) (GOOGL) in the long run.

One consequence of hybrid work that actually favors SLG is that increasingly many companies are leaving older buildings and we are seeing a flight to quality. SLG owns the highest quality assets in NYC so it benefits from this demand:

SL Green

Therefore, we think that the short-term uncertainty could actually be a historic long-term opportunity.

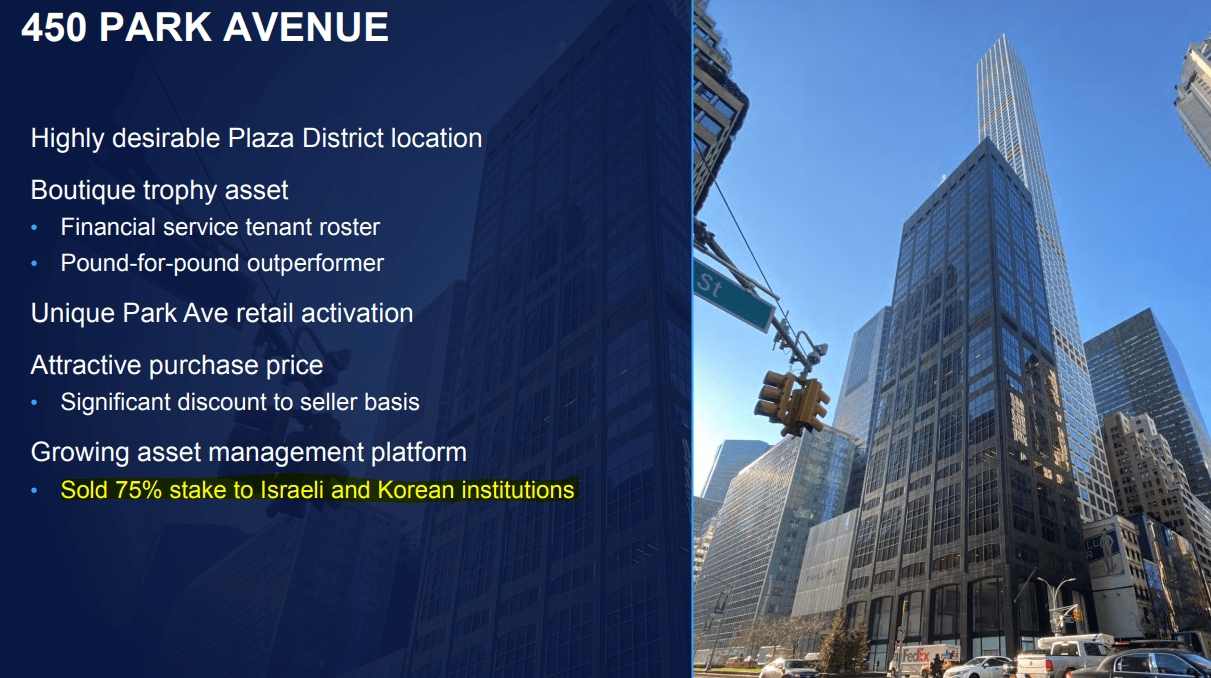

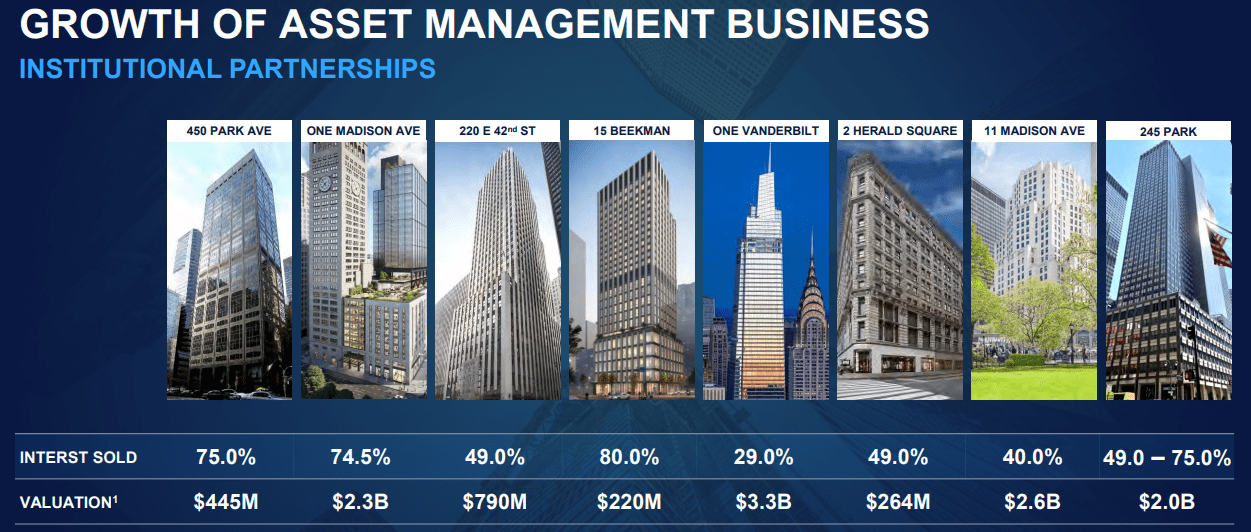

Right now, SLG is priced at a 55% discount to its net asset value according to our estimate, and I love how SLG's management is taking advantage of this discount.

It is currently in the process of setting up funds and selling interest in its properties to other institutional investors in order to capture the discount and it will also earn asset management fees going forward.

{kind=link}

So it is slowly becoming an asset-lighter business that will earn both, fees and rents going forward. I think that it is a great plan to unlock value for shareholders:

{kind=link}

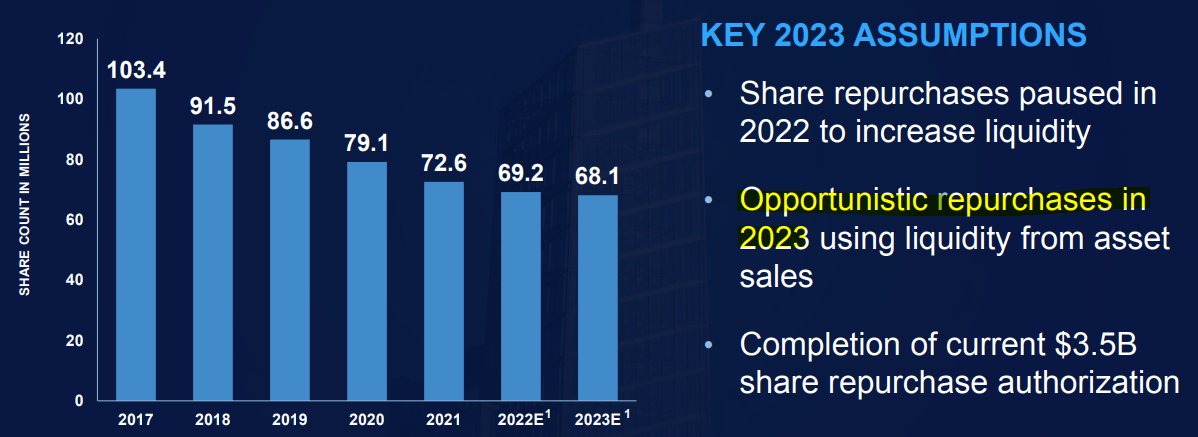

These proceeds can then be reinvested into buybacks, deleveraging, and anything else that creates value for shareholders:

{kind=link}

So in short, the industry is going through severe disruption, and the near-term results will be volatile, but SLG owns great assets that should do well in the long run, and SLG has a great plan to benefit from this environment.

Priced at less than half of its current NAV, I think that it is opportunistic.

While you wait, you also earn a near 10% dividend yield, and it is paid monthly!

I like the risk-to-reward and I am considering a small position for our Core Portfolio.

Broadmark Realty Capital

BRMK is a mortgage REIT that specializes in hard money lending and we have lost money on it in the past.

We used to own it but sold it at around $5.5 in October of 2022 and cited the following reasons:

"Its fundamentals have deteriorated and at least part of its recent drop is justified. Hard money lending has become more competitive and as a result, BRMK's yields have come down even as interest rates have risen, resulting in smaller spreads. Meanwhile, the risk of its loans is also getting larger as we potentially head into a recession and inflation continues to put pressure on new construction projects. Finally, the company discontinued its non-traded REIT likely because it couldn't find enough loans that met its lending criteria. All of this is putting the dividend at high risk of being cut sometime in the near future. That's bad news, but even then, we remain bullish and give it a Buy rating due to its low valuation, but our conviction level has come down due to the changing environment. At the same time, GMRE has come down even more, despite enjoying far stronger fundamentals."

Since then, the REIT made the right decision to cut its dividend which was excessive for a long time.

I think that the dividend cut is good news for the company, but it caused its share price to crash even lower.

As a result, the company now still yields around 10% and that's after cutting its dividend in half.

The halving of the dividend will allow them to retain cash to deal with non-performing loans and they also recently announced a big buyback program, which has the potential to create significant value for long-term oriented shareholders.

Priced at just around half of its net asset value, I think that the risk-to-reward is getting compelling now that they actually retain cash flow and can buy back shares.

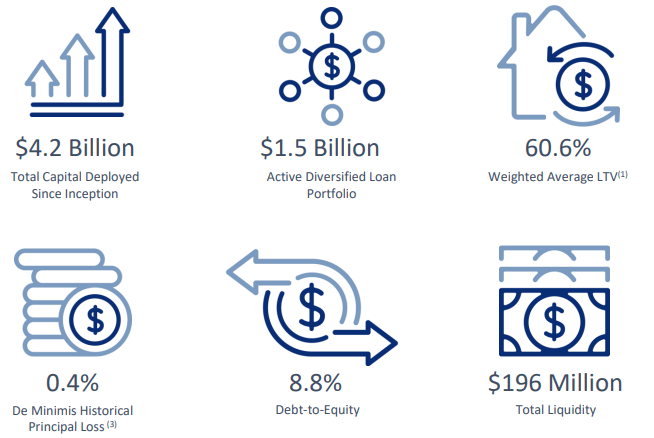

Its net asset value is also fairly resilient since these are property-backed loans and the company has very little debt at just 8% of its balance sheet.

{kind=link}

You earn a near 10% monthly dividend yield while you wait for long-term upside.

Bottom Line

Needless to say that a ~10% yielder is never a safe or conservative investment.

These are higher risk / higher (potential) reward investments with attractive risk-to-reward and this is why we give them a "Buy" rating at High Yield Landlord.

For now, we continue to favor some other investments, but we are strongly considering investing in these two REITs.

For further details see:

2 New Buy Alerts With 10% Monthly Dividend Yield And Potential Upside