SPG - 2 New Buy Alerts With A 6% Dividend Yield And High Potential Upside

2023-05-15 09:00:00 ET

Summary

- REITs are today priced at historically high dividend yields.

- Even blue-chips now yield 6%.

- We highlight two high-yielding blue-chip REITs that we are buying.

REIT (real estate investment trust) dividend yields are today a lot higher than they were just a year ago.

That's because REIT ( VNQ ) share prices have crashed...

...even as most REITs kept growing their cash flow and increasing their dividends:

{kind=link}

A higher dividend + a lower share price = higher dividend yield.

As a result, many of the high-quality, blue-chip REITs that used to yield 2-3% are now offered for sale at up to a 6% dividend yield.

That's very attractive coming from a blue chip!

I am talking here about companies that have:

- An investment grade-rated balance sheet

- High-quality assets

- A great track record

- And steady growth prospects.

These are the type of REITs that rarely come on sale... and so when they do, you don't want to miss out these opportunities.

We are heavily investing in them at High Yield Landlord, and in what follows, we highlight two of our latest purchases:

Crown Castle: 5.5% Dividend Yield

Crown Castle Inc. ( CCI ) is the second largest cell tower REIT, coming right behind American Tower Corporation ( AMT ).

Historically, CCI has typically traded at a low 2-3% dividend yield because of its ability to consistently grow its dividend at ~8% per year.

{kind=link}

Its business model is very consistent and predictable.

It acquires cell towers that it leases to companies like T-Mobile US, Inc. ( TMUS ) and AT&T Inc. ( T ), and it then earns a return that's well in excess of its cost of capital, pocketing the spread in between.

Data consumption is ever-growing, resulting in more demand for cell towers, and providing CCI will lots of investment opportunities.

Crown Castle

It pairs this defensive business model with an investment grade-rated balance sheet that has low leverage and ample liquidity for future investments.

But despite all of that, the company is today priced at a near 5.5% dividend yield, a historic high for the company. All it would take is one more dividend hike and the yield would get near 6%:

Why is it now offered at such a high yield?

The market soured on CCI because its growth will slow down for the next 2-3 years due to T-Mobile's acquisition of Sprint. It will lead to some lease cancellations and impact its near-term results.

But here's the thing: this is just temporary.

The company has clearly guided that it will return to faster growth quickly thereafter. Here is a recent quote from the company CEO (emphasis added):

"So to wrap up, we are excited about the strength of our business and our ability to execute on our strategy to deliver the highest risk-adjusted returns for our shareholders by growing our dividend over the long-term and investing in assets that will help drive future growth. We have delivered 9% compound annual and dividend per share growth since we established our 7% to 8% dividend per share growth target in 2017. And I believe that we are positioned well to return to 7% to 8% dividend per share growth as we move beyond the Sprint decommissioning impacts in 2025. "

We think that this is a great opportunity because we get to a earn a high yield, and we have a clear timeline for the return to faster growth, which should serve as a clear catalyst for future upside.

Companies of CCI's quality don't typically yield nearly 6%.

As its growth gets back to its historic norm, we expect it to reprice at closer to a 3-4% dividend yield, unlocking up to 50% upside from here.

Finally, we think that the risk-to-reward is especially compelling because this is a recession-proof business with secular growth tailwinds.

Simon Property Group: 6.2% Dividend Yield

Simon Property Group, Inc. ( SPG ) is the blue-chip of mall REITs.

Malls are today feared by many due to the growth of e-commerce and Amazon.com, Inc. ( AMZN ), but the reality is that these are not your typical malls.

These are class A mixed-use retail properties that include stores, but also many other uses that bring consistent traffic to the property. They are located on prime sites, enjoy exceptional demographics, and because real estate is ultimately about "location, location, location...", these properties continue to perform very well.

{kind=link}

If you don't believe it, just take a look at the latest results of the company.

Their sales and rents keep on growing and are hitting new all-time highs.

In the last quarter, the average sales per square foot of its properties rose by 3.3% and the average rent rose by another 3.1%. This allowed the company to hike its full-year guidance and also its dividend by 8.8% year-over-year.

So yes, I understand that malls are hated and avoided by most investors, but at some point, people need to realize that not malls are created equal.

E-commerce is causing great pain to lower-quality malls and it is causing many to close down. This then leads to a lot of negative headlines, highlighting the "retail apocalypse."

But this actually benefits high-quality malls as it reduces competition between malls and consolidates traffic and sales towards the best malls.

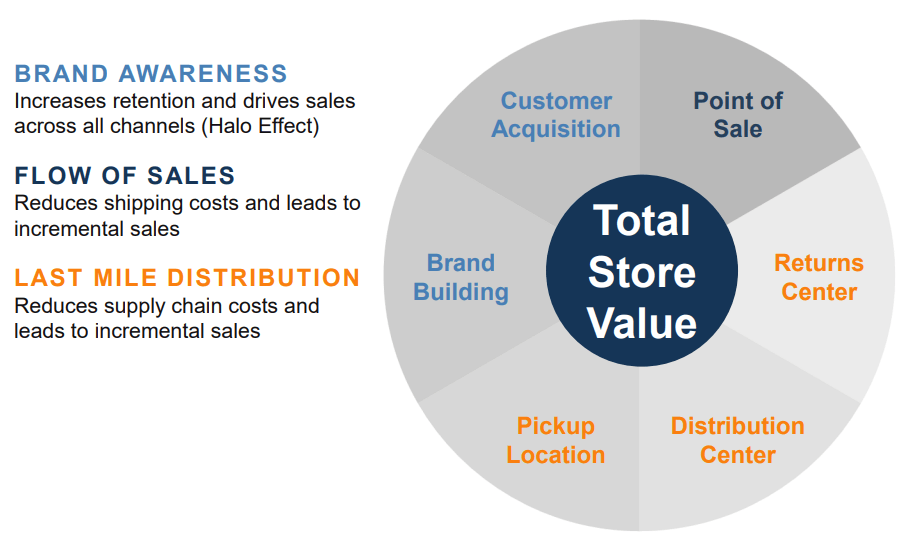

In other words, the weak get weaker and the strong get stronger. Even the digitally-native brands are leasing space at Simon's class A malls because they offer many benefits in an omnichannel world. Brookfield Asset Management Ltd. ( BAM ) has a nice slide about this:

{kind=link}

I would add that SPG has an A-rated fortress balance sheet , lots of liquidity, many growth opportunities, and a great track record.

Despite that, SPG is today priced at a 6.2% dividend yield, which is quite exceptional for a blue-chip that just hiked its dividend by 8.8% year-over-year.

I think that as SPG keeps proving the market wrong, eventually, it will reprice at closer to a 4% dividend yield, unlocking 50% upside from here.

Bottom Line

Crown Castle Inc. and Simon Property Group, Inc. both have strong investment grade-rated balance sheets, exceptional track records, class A assets, and growing dividend payments.

Despite that, they are now priced at high dividend yield and offer significant upside potential in a future recovery.

That's exactly what we like to target at High Yield Landlord.

For further details see:

2 New Buy Alerts With A 6% Dividend Yield And High Potential Upside