VNQ - 2 New Buy Alerts With A 9% Dividend Yield And High Upside

2023-04-06 08:05:00 ET

Summary

- Not all REITs have a low dividend yield.

- Some yield as much as 10%.

- I highlight two such REITs that I am buying.

Today, the average dividend yield of real estate investment trusts, or REITs ( VNQ ), is 3.7%.

That surprises many investors who would hope to earn a higher yield from a real estate investment, especially in today's high interest rate environment.

But they need to understand that yields are so low because of three key reasons:

- Reason #1 - Payout ratios are low: most REITs retain a large portion of their cash flow to reinvest in growth. There is this common misconception that REITs must payout 90% of their cash flow in the form of dividends, but in reality, the rule is that they must pay 90% of their "taxable income," which is a lot lower than cash flow because of non-cash depreciation. This explains why many REITs retain up to 50% of their cash flow to reinvest in growth, resulting in lower dividend yields. To give you an example, Camden Property Trust ( CPT ) has a 3.8% dividend yield, but it also retains 40% of its cash flow. So the real "cash flow yield" is actually a lot higher at 7%.

- Reason #2 - Focus on high-growth assets: Moreover, most REITs are today invested in lower-yielding, high-growth property sectors like cell towers, e-commerce warehouses, and data centers. Such high-growth properties come with lower yields, but they then grow their rents at a faster pace. Equinix ( EQIX ), for instance, has a low 2% dividend yield, but it has consistently been able to grow its cash flow at 8-12% per year.

- Reason #3 - REIT balance sheets are the strongest ever: You can achieve high yields with real estate if you use a lot of leverage, but REITs today use very little of it. On average, their LTV is just 35%. That compares very favorably to the 60-70% LTVs which are common for private equity real estate investors. Lower yield... but greater safety. To give you an example, Public Storage has a low 15% LTV and so it isn't so surprising that it yields just 3.8%.

But fortunately, there are also higher-yielding REITs out there.

But the challenge is to find high-yielding REITs that retain enough cash flow for growth, own good assets, and aren't overleveraged.

That's what we attempt to do at High Yield Landlord.

Our Portfolio yields 6.6% on average, and we achieve this higher yield by investing in REITs that are undervalued:

High Yield Landlord

Some of our highest-yielding holdings have dividend yields approaching 10%. In today's article, we want to highlight two of them to show you that it is possible to achieve such high yields by investing in REITs.

Not all REITs have low yields and these two REITs are proof of that:

EPR Properties ( EPR ): 8.9% Dividend Yield

EPR is a REIT that invests in net lease properties, just like Realty Income Corporation ( O ).

Net lease properties are generally single-tenant service-oriented properties such as McDonald's ( MCD ) restaurants, Walgreens ( WBA ) pharmacies, and Dollar General ( DG ) convenience stores.

They can be very attractive investments because net lease properties enjoy:

- Very long terms: 10+ years in most cases.

- No property expenses: the tenant is responsible for them.

- Steady rent growth: contractual rent escalations of 1-2% each year.

- Recession-resistant: high rent growth coverage of 2-3x.

- Technology-proof: most properties are service-oriented or experiential.

McDonald's

As a result, net lease properties typically enjoy highly consistent and predictable cash flow and the REITs that specialize in this sector have historically earned some of the best risk-adjusted returns in the entire REIT sector.

One of my favorites is EPR Properties.

EPR is a net lease REIT that focuses on experiential properties. This includes things like water parks, amusement parks, ski areas, golf complexes, and high-quality movie theaters.

{kind=link}

EPR Properties

EPR Properties

EPR intentionally focuses on this niche of the net lease market because it is less competitive and it allows it to earn even greater risk-adjusted returns.

Individually, these assets are riskier, but as part of a well-diversified portfolio, the risks are mitigated and the returns are above-average:

- Higher cap rates

- Higher lease escalations

- True triple-net

- Master lease protection

- Longer lease terms.

Here is its performance since going public relative to other REITs:

EPR Properties

Historically, the market has rewarded EPR with a healthy valuation, trading at a premium to its NAV during most times, and this allowed it to raise more capital and reinvest it in an accretive fashion.

But this changed with the pandemic.

Its experiential properties suffered a lot early into the pandemic due to the social distancing guidelines, and to this day, most investors remain very pessimistic about EPR.

But here's the reality:

EPR's experiential properties survived the pandemic, which was the worst possible crisis for them, and they then quickly recovered from it.

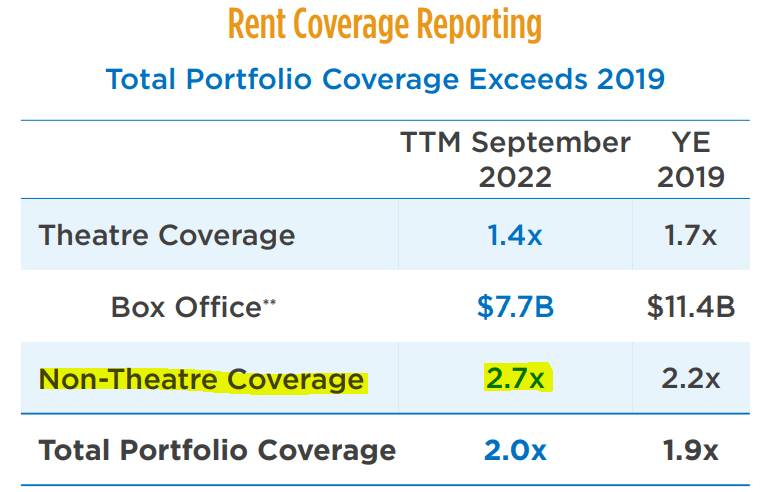

Today, the rent coverage ratio of most of its properties is near 3x, which is far more than prior to the pandemic. This means that its tenants are able to earn large profits that easily cover their rent payments.

{kind=link}

There's only one segment of its portfolio that hasn't yet fully recovered and that's movie theaters.

Their rent coverage is now at 1.4x, meaning that its tenants are already profitable at the property level, but it is down from 1.7x pre-pandemic.

The market worries a lot about this because movie theater operators like AMC Entertainment Holdings, Inc. ( AMC ), Cinemark ( CNK ), and Regal ( CNNWQ ) are going through severe difficulties.

But here's why the fears are misplaced when it comes to EPR:

- EPR owns some of the most productive movie theaters in the nation. We may have too many theaters and some of the lower quality theaters may even close down, but this would actually benefit the higher quality theaters because it would lead to traffic consolidation.

- EPR is the landlord, not the operator. EPR earns steady rent checks and it gets paid first. As long as the rent coverage is positive, which it is already today, EPR can expect to earn steady rent payments from its tenants.

- The rent coverage is already positive today with a low box office. Movie producers like Paramount ( PARA ), Disney ( DIS ), Warner ( WBD ) and others took time to get back to speed, and so theaters had fewer blockbusters to monetize in the recent years. But now things are getting back to normal. Movie producers have all come to the realization that direct-to-streaming and other digital strategies don't work and so they are returning to theaters.

- The reality is that if you like blockbuster movies, then theaters are essential to monetize their production. Streaming and video-on-demand does not work because as soon as you put the movie online, it gets pirated, and at best, you only get one person to buy the movie and then the rest of the family watches it for free.

- Now, even Amazon ( AMZN ) and Apple ( AAPL ) have announced that they would start spending billions on producing movies for theaters. It has even been rumored that AMZN could buy out AMC due to the synergies with Prime and its other businesses.

- As the box office recovers, we can expect the rent coverage of EPR's tenants to also increase from here.

- But even if I am wrong: it is important to remember that its theaters only makes up about 1/4 of its NAV... Most of them are doing perfectly fine... Others could be converted into other uses... And in some cases, these properties are more valuable empty than occupied.

EPR Properties

Yet, the market is discounting the entire company over its exposure to movie theaters. We think that this is unfair due to the reasons that we discussed earlier. EPR has proven that its strategy could survive the worst potential crisis, a pandemic, and today, its business has already recovered. It is doing well and it is growing.

Despite that, you can now buy shares of the company at just 8x funds from operations ("FFO"), a 32% discount to its NAV, and an 8.9% dividend yield.

The dividend payout is just 75% and EPR hiked its dividend by 10% last year. Therefore, we have all the reasons to think that its dividend is sustainable and set for more growth in the years ahead.

EPR's rents keeps getting hiked by ~2% annually and it has the liquidity and balance sheet (investment grade rated) to keep acquiring more properties to grow its cash flow.

Global Medical REIT ( GMRE ): 9.4% Dividend Yield

I will keep this one shorter because the thesis is easier.

GMRE is a small-cap REIT that specializes in medical office buildings.

Global Medical REIT

Medical office buildings are some of the safest real estate investments because doctors are great tenants. They operate recession-resistant businesses, the demand for healthcare is ever-growing, and doctors pay in full and on time because these properties are essential for them to operate their business.

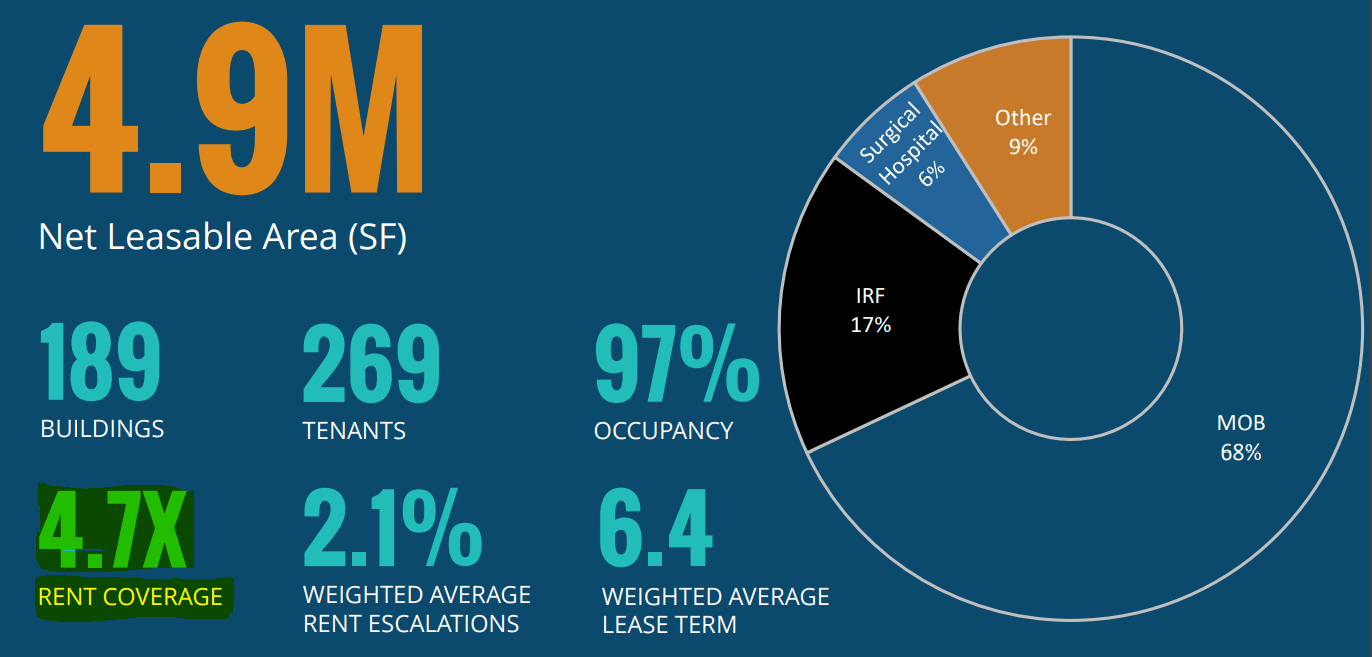

Importantly, the rent coverage ratios of medical office buildings are typically very high at around 5x. This means that they cover their rent obligations with ample profits.

{kind=link}

Despite that, GMRE's share price has dropped very significantly over the past year. We suspect this is primarily because of a misconception: the market is putting all healthcare REITs in one basket and failing to differentiate medical office buildings from hospital, skilled nursing facilities, or senior housing communities.

But their risk profiles are very different.

To give you an example: the skilled nursing facilities of Omega Healthcare ( OHI ) have a low 1.2x rent coverage ratio, leaving little margin of safety in today's inflationary world. Understandably, OHI should be priced at a fairly low valuation because the risks are high.

Similarly, Medical Properties Trust ( MPW ), the owner of hospitals, should trade at a fairly low valuation because hospitals are suffering today from labor shortages, which is putting great pressure on its tenants. Investing in MPW is a high risk bet in today's environment.

But GMRE is very different, and yet, it has dropped almost in lock-step with MPW and others:

We think that this is an opportunity.

Right now, GMRE is priced at an estimated 8.9x FFO, a 30% discount to its NAV, and a 9.4% dividend yield.

Now, it is true that GMRE has risks as well. It is a small-cap REIT... It has a bit more leverage than your average REIT... and it focuses on secondary markets that could face oversupply if and when a large amount of traditional offices are converted into medical office buildings.

But the risk-to-reward is very compelling at these valuations. The REIT has a great track record and today, its share price is unfairly beaten down.

Bottom Line

I like to invest in high yielding REITs like EPR and GMRE because I want to get paid while I wait for long-term upside.

Of course, individual REITs like EPR have risks, but I get to diversify these risks by holding many similar REITs as part of a well-diversified portfolio.

That's what we do at High Yield Landlord.

For further details see:

2 New Buy Alerts With A 9% Dividend Yield And High Upside