MDV - 2 Of My Biggest Investments

2023-10-31 08:05:00 ET

Summary

- My investment strategy is rather boring.

- Most of the time, I am just buying more shares of the same companies.

- I highlight two of my largest holdings.

I often feel pressured to find new investment opportunities that I could present here on Seeking Alpha.

I know that many of you have followed my writings for years because there's always something new and exciting to learn about in the vast world of REITs. A good example of that is our recent interview with the CEO of Modiv Industrial ( MDV ).

But the reality is that there are times when simply sticking to what you already own and adding more capital to those picks is the best strategy.

That's the case today.

We have worked hard to cherry-pick the real estate investment trusts, or REITs ( VNQ ), that we currently own and for us to justify a new investment, it would need to either be: (1) more attractive than what we own already; or (2) it would need to add something new and unique to our portfolio to further diversify risks and optimize its risk-to-reward.

I am doing my best to not leave any stones unturned, and that's still not easy to find. I could, of course, present something new and exciting to you, but it wouldn't do you any good if its prospects were actually inferior to those of the holdings that we already own.

Therefore, I will take the boring route and keep covering what we own already. There will again come times in the future when the market presents us with exceptional new opportunities that we can't let pass by, but until then, we will keep accumulating as much of our current holdings as possible.

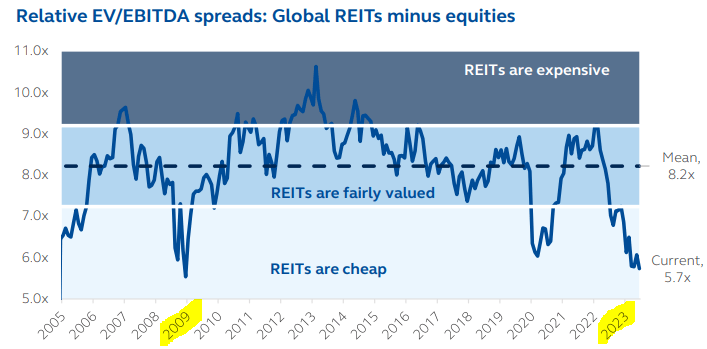

Valuations are literally at their lowest since 2008-2009 relative to the S&P 500 (SP500), and in what follows, we will highlight two of our largest investments at the moment.

{kind=link}

RCI Hospitality Holdings, Inc. ( RICK )

RCI Hospitality is our nightclub investment. It is not officially structured as a REIT, but it essentially functions as if it was one. It makes real estate investments, which it then operates to earn cash flow.

In case you are not familiar with the company, you can start by reading our recent interview with one of the company's CEO by clicking here.

RCI Hospitality

The company has kept earning significant free cash flow, growing its cash pile, but its share price has kept dipping lower along with the rest of the listed real estate market:

The management made it clear on their most recent earnings call that they are back on the negotiating table and ready to make new club acquisitions.

Here is an interesting section from the most recent Q&A (emphasis added):

Joseph Gomes (Analyst)

Hey. So, you guys kind of answered most of mine, but I just kind of want to see how just the overall environment is just looking like for any just new potential club acquisitions, how are owners being obviously in this kind of cautionary environment?

Eric Langan (RICK's CEO)

Yes, I mean, we haven’t pursued, so I don’t really know. I’ve told almost everyone that has called me in the last 2 months that we’ve got to get this other acquisition under our belt (Jussi's addition: RICK has made major acquisitions recently and been working on integrating those, which kept them busy) . We’re working on it. Let’s talk at EXPO (Jussi's addition: this is a major club conference) . Let’s talk at EXPO. Seeing the hotel room count full already, means there’s going to be lots of people there. So I’m very optimistic that – and I’ve got some meetings set up, and some people that I’m going to make sure we talk to, while we’re out there. And people that want to talk to us while we’re out there.

So I think we’ll get a kind of a list put together and we’ll talk multiples and locations and try to figure out what’s the quickest and easiest for us in timing and what the best deal is . And, cherry pick the best clubs like we’ve been doing for the last 10, 15 years. But EXPO – every year at EXPO, we always make someone and we always start the process. So, the reality is just how quickly we can do it. We’re ready now, so we could close something pretty quick quickly.

I think we have, if I’m correct, approximately $45 million or $46 million worth of unencumbered real estate or under encumbered real estate we could roll in to a loan. At 70% loan to value that would pull about $28 million. With the under encumbered parts probably $4 million, $5 million we’d have to pay off. So we could easily pull a $20 million down payment out from our bank right now if we need it.

I’m not counting our line of credit, so we could hit – we paid down our line of credit a little bit so we could probably hit that line of credit again if we needed to. So we’re in good shape. And we still have $25 million cash on the books. So we’re in great shape to make an acquisition. Obviously, we’re not using equity at these prices. So it would be a debt, in cash acquisition right now.

I don’t – unless, of course, the stock [indiscernible] runs back up over $80 over the next few weeks, which, the market where it’s at, some of the uncertainty out there. I think that’s probably unlikely. So I would love that it did, because it would give us even more ammunition, as we go to EXPO in a few weeks.

But, if it stays under, then we’ll just continue to buy back a little bit every week with some of our cash and , just keep following our capital allocation strategy. We’ve proven from 2015 on, it works. And there’s no there’s no flaw on it so far at this point. So I think we’ll just keep doing what we do."

RCI Hospitality

So, in short, they are telling us that their team is now ready for new acquisitions, which wasn't the case for most of 2023 because they were too busy integrating their latest acquisitions.

This is very good news.

Moreover, they now have about $30 million of cash today (they have earned some more since their last Q&A) and could get another $20 million from banks.

That's $50 million.

Then RICK typically also gets seller financing when buying clubs so overall, its buying power is likely over $100 million right now and it is ready to make new deals.

That's very significant considering that they target 25-33% annual cash-on-cash returns on their new acquisitions, and their current cash flow is just around $80 million annually. This is just to say that they could create significant value in the near term if and when they announce some new club acquisitions.

These acquisitions are the number #1 reason behind RICK's huge returns these past years, and so I remain very optimistic:

{kind=link}

While we wait for acquisitions, RICK is also buying back $100,000 of shares each day, creating value for patient long-term-oriented investors.

Priced at 7x free cash flow ("FCF") and offering 20% annual growth prospects, we continue to think that RICK will likely be one of our biggest winners over the next 10 years.

We have bought the dip and will continue to accumulate more shares of the company.

Alexandria Real Estate Equities, Inc. ( ARE )

For most of the past two years, ARE has been closely correlated to office REITs, despite actually investing in life science buildings.

Alexandria Real Estate

It created an opportunity when office REITs crashed because it dragged ARE down with them.

But recently, this opportunity became even more compelling because most office REITs recovered quite a bit, but ARE kept trading at its 52-week lows:

YCHARTS

As a result, the valuation gap between office REITs like Boston Properties (BXP) and Alexandria Real Estate is now historically small:

| BXP |

| ARE |

| FFO Multiple |

| 8.5x |

| 10.8x |

| P/NAV (consensus estimates) |

| 0.66 |

| 0.61 |

That's despite the fact that:

- BXP has far more debt than ARE

- It also has much greater debt maturities

- Its properties face larger capex needs

- They also require more TI

- Cap rates for offices are expanding a lot more

- Refinancing will be a lot costlier

- Its mark-to-market opportunity is a lot smaller

- It is experiencing declining FFO per share

- It enjoys no growth in its dividend

- And its future growth is far less certain.

| BXP |

| ARE |

| Debt-to-EBITDA |

| 7.2x |

| 5x |

| Maturities in the coming two years |

| 12% |

| 0% |

| Same property NOI growth |

| ~0% |

| ~5% |

If you adjust for all those factors, BXP is actually more expensive than ARE following its recent recovery, which makes little sense.

We believe that this recent disparity in performance is an opportunity.

The market doesn't seem to know what to do with ARE because most investors still perceive it as an office REIT, but a minority of investors understand that this isn't the case, and therefore, it still trades at a slightly higher FFO multiple.

Short sellers would argue that this FFO multiple is too high for an office REIT.

Long investors would counter that this isn't an office REIT and if you make the right adjustments for leverage, capex, and growth, it is actually even cheaper than some of the office REITs...

The indecisiveness of the market has resulted in a once-in-a-decade chance to build a position in ARE at its lowest valuation since the great financial crisis.

At 10.8x FFO, ARE is far below its average valuation multiple of about 22x (Note: not its peak, but its average multiple), and we believe ARE has roughly 75% upside to fair value. The 5.4% yield and mid-single-digit growth rate provide solid returns while investors wait for that upside to materialize.

We recently bought some more shares to take advantage of the dip.

Closing Note

Good investing should be boring and this is why it requires a lot of patience and discipline.

Seeking excitement when investing capital can easily deviate you to a path that's less desirable over the long run.

This is why we call our strategy the "landlord approach to REIT investing."

We keep it simple and boring because that's likely what will lead to the greatest reward in the long run.

For further details see:

2 Of My Biggest Investments