VNQ - 2 Of My Favorite REITs For 2024

2024-01-08 08:05:00 ET

Summary

- Good investing should be boring.

- I keep buying the same REITs over and over again.

- Here are of two of my favorite REITs for 2024.

I often feel pressured to find new investment opportunities that I could present here on Seeking Alpha.

I know that many of you have kept following my articles for years because there's always something new and exciting to learn about in the vast world of REITs ( VNQ ).

But the reality is that there are times when simply sticking to what you already own and adding more capital to those picks is the best strategy.

That's the case today.

We have worked hard to cherry-pick the REITs that we currently own and for us to justify a new investment, it would need to either be (1) more attractive than what we own already or (2) it would need to add something new and unique to our portfolio to further diversify risks and optimize its risk-to-reward.

I am doing my best to not leave any stones unturned, and that's still not easy to find. I could of course present something new and exciting to you, but it wouldn't do you any good if its prospects were actually inferior to those of the holdings that we already own.

Therefore, I will take the boring route and keep covering what we own already. There will again come times in the future when the market presents us with exceptional new opportunities that we can't let pass by, but until then, we will keep accumulating as much of our current holdings as possible.

Here are two of our favorite REITs to accumulate today:

NNN REIT ( NNN )

Our analyst, R. Paul Drake, has previously described NNN as " almost perfect " and for a good reason. He has highlighted the following attributes in a previous article :

- Investment-grade BBB+ credit rating

- Substantially no secured debt

- Negligible debt maturities in the coming years

- 13.7-year weighted-average debt maturity

- 10.4-year weighted-average lease term

- Ample liquidity

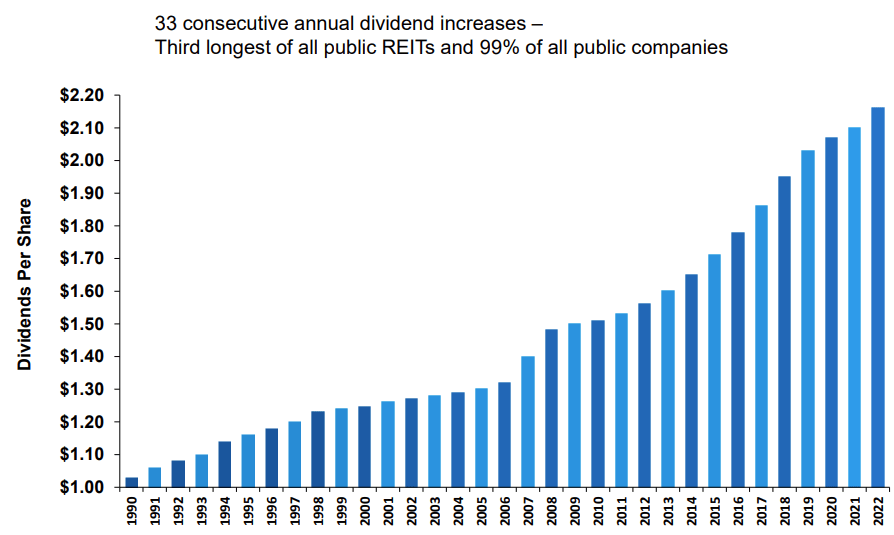

- 33 years of increased dividends

- Sustained very high occupancy (now 99.4%)

- Middle-market focus (on firms that cannot sell bonds)

- Dominantly (71% since 2006) relationship-based acquisitions

- Outstanding diversification by geography and line of trade

{kind=link}

I would add the following to its long list of strong attributes:

- Focus on properties with low rents, discount to replacement cost, and high land value per asset to mitigate risks in case of rare vacancies

- Focus on high-growth states. Texas and Florida make up nearly 30%

- Defensive concepts: convenience stores, automotive sectors, and restaurants make up ~50% of the portfolio. 7-11 is the biggest tenant

- Landlord-friendly lease terms with above-average lease escalators and absolute triple net lease with no landlord responsibilities

- They can achieve most of their ~5% annual growth target organically without having to raise much or any equity in the open market

- Able to consistently recycle capital by selling assets at low cap rates with their propriety disposition channels, including their own website targeting 1031 buyers.

- Strong focus on FFO per share growth, putting higher hurdles on their cost of equity when raising new capital

- Ultimately, they have managed to generate above-average returns with below-average risk and superior income for 30+ years and we think that they can keep this going for decades to come

{kind=link}

You will note that this is also one of the few net lease REITs that have longer debt maturities than lease terms and therefore, it is not heavily impacted by the surge in interest rates.

Yet, they are now priced at a historically low valuation of 13.4x FFO and a high 5.3% dividend yield with a low 69% payout ratio.

My expectation is that in a typical year, they will grow their FFO per share and dividend by roughly 4-5%, resulting in double-digit total returns when coupled with today's high dividend yield:

5.3% dividend yield + 4-5% FFO per share growth = 9.3-10.3% expected annual total return

That on its own is very attractive, coming from such a low-risk strategy.

But then on top of that, as interest rates eventually return to lower levels, we expect significant upside as its valuation expands closer to its historic range of 16-20x FFO.

Assuming that its multiple expands to a conservative 16x FFO, this would add another 20% of upside to the returns. Assuming that it takes 3 years for it to return to this valuation, this would bring the expected annual total returns to 15-20%:

5.3% dividend yield + 4-5% FFO per share growth + 6% annual repricing upside = 15.3-17.3% expected annual total return

And again, I think that these assumptions are fairly conservative.

NNN sure won't cut its dividend. Its ~4-5% growth target can be achieved almost organically in most cases. And it actually traded at 20x FFO prior to the pandemic. If anything, its performance during the pandemic should add further assurance to the market because it showed that even the worst possible crisis didn't break NNN's business model.

For all these reasons, we believe that NNN offers great risk-to-reward for most conservative investors. I have never lost money buying a REIT like NNN at a discounted valuation, and don't think that this time will be any different.

EPR Properties ( EPR )

EPR Properties ((EPR)) is a net lease REIT just like NNN REIT ((NNN)), but it is riskier because it specializes in experiential properties such as movie theaters, ski resorts, and golf complexes.

EPR Properties

We think that now is a good time to buy more shares because it remains heavily discounted, despite recently benefiting from a lot of positive news.

Firstly, the Regal bankruptcy has been resolved in a way that's very favorable for EPR. In short, the rent was raised (yes, raised!) on the majority of the theatres that they will continue to operate (41 out of 57) and will be covered under a single master lease that will be a lot safer following the restructuring of the tenant's finances. Then 5 other theaters will be operated by other companies and the rest will be sold. All in all, the impact on revenue is very small, but it significantly reduced risks because it strengthened their portfolio, and more importantly, it also validated the thesis that high-quality theaters are here to stay. It shows us what to expect if another tenant like AMC ( AMC ) files for bankruptcy someday in the future. (Note that AMC's master lease was already renegotiated during the pandemic in a way that should mitigate risks in case of such an event.)

So that's very good news.

Then on top of that, Barbie and Oppenheimer broke new records, AMC reported its first quarterly profits since 2019, and it raised a bunch more capital.

But despite that, EPR's share price still hasn't fully recovered, and as a result, it still offers some of the best combination of value, growth, income, and upside in today's market:

| EPR Properties |

| Value |

| 9.3x FFO |

| Growth |

| 9% FFO per share growth in 2023 |

| Income |

| 7% dividend yield |

| Upside |

| 50% upside to 14x FFO multiple |

Over time, as they keep proving the market wrong, further diversify their portfolio away from theaters, interest rates return to lower levels, and the movie theater industry finishes its recovery, it could very well reprice higher at closer to 14x FFO, which would unlock 50% upside from here.

From there on, EPR will also enjoy strong growth prospects as its current properties enjoy a near 2% average annual rent escalation, and it can buy properties at >8% cap rates, resulting in a nice spread over its cost of capital.

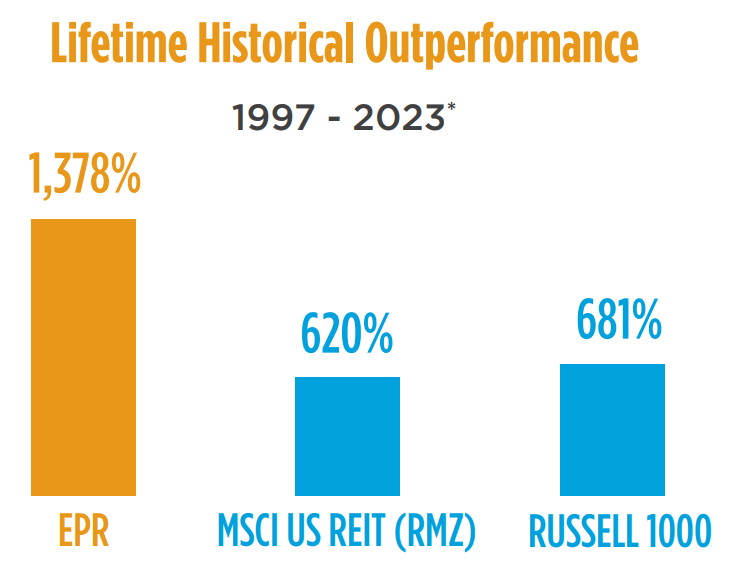

EPR has done just that in the past and massively outperformed the broader market. The Covid crisis led to a 2-year hiccup, but things are now returning to normal, and it still remains discounted:

{kind=link}

Closing Note

Good investing should be boring, and this is why it requires a lot of patience and discipline.

Seeking excitement when investing capital can easily deviate you to a path that's less desirable over the long run.

This is why we call our strategy the "landlord approach to REIT investing".

We keep it simple and boring because that's likely what will lead to the greatest reward in the long run.

For further details see:

2 Of My Favorite REITs For 2024