VNQ - 2 Once-In-A-Decade REIT Buying Opportunities

2023-12-12 08:05:00 ET

Summary

- REITs are today offering a historic opportunity.

- Valuations are at their lowest in a decade and are set to surge as interest rates return to lower levels.

- We present 2 once-in-a-decade buying opportunities.

Co-produced by Austin Rogers

Investor sentiment about real estate investment trusts ("REITs") is lower than it has been since the Great Financial Crisis of 2008-2009.

That has translated into a wide divergence in performance between the public real estate sector ( VNQ ) and the S&P 500 ( SPY ):

Over the past 2 years, REITs have underperformed the market by nearly 25 percentage points, even after the recent rebound!

As we have done many times in the past, we remind investors that this huge divergence in price performance does not signify fundamental weakness but rather merely investor pessimism.

Consider a few facts about REITs, courtesy of NAREIT :

- REITs' average loan-to-value ratio sits at about 36%.

- REITs' weighted average debt term to maturity is 6.5 years.

- 91% of REITs' debt is fixed-rate.

- Because of the above factors, REITs' weighted average interest rate on debt is only 4.0%.

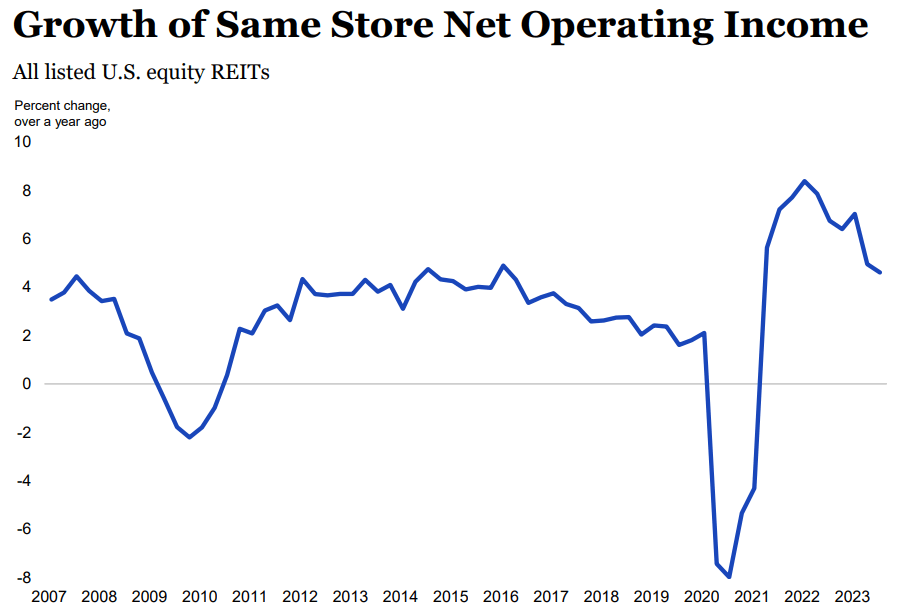

- Same-store / comparable-property net operating income ("NOI") continues to rise.

Rising interest rates are a headwind for REITs, but they are a more modest headwind than many investors think. And they are felt with a lag. Higher interest rates create incrementally increasing interest expenses, while rent growth is felt much faster.

Hence we find that REITs' same-store NOI growth continues at a strong pace of about 5% YoY in Q3 2023. That is higher than at almost any point in the last 15 years!

{kind=link}

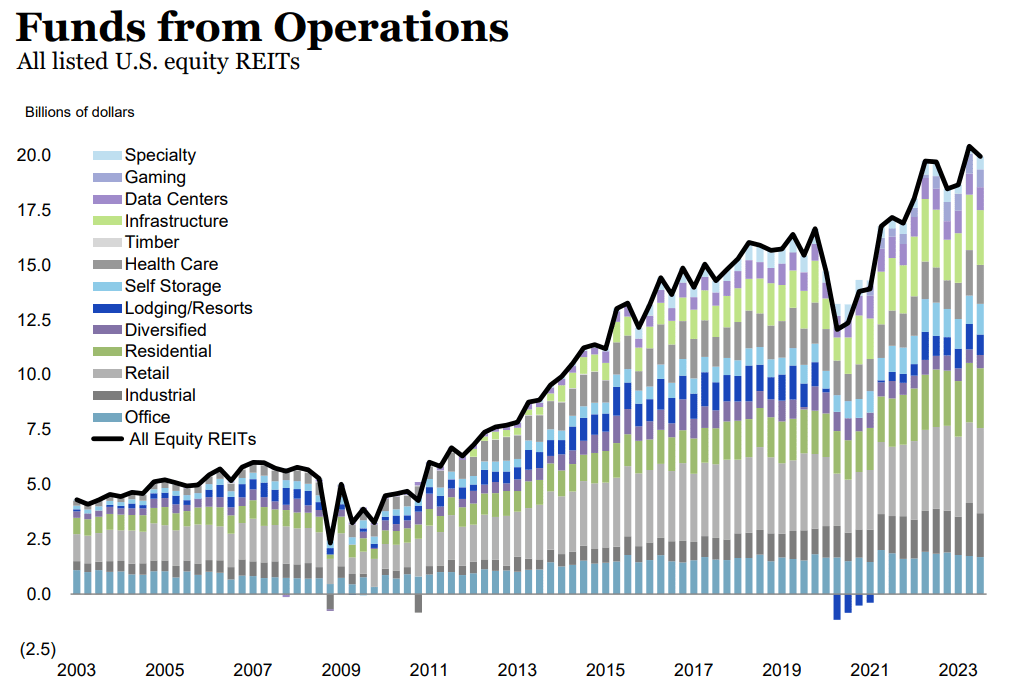

But, of course, NOI does not account for interest expenses. One might object that SSNOI looks only at the positive side of the equation for REITs while ignoring the rising expenses from interest payments.

Funds from operations ("FFO") does incorporate interest costs. When it comes to FFO, again, total REIT profits are near an all-time high and continue to grow:

{kind=link}

You would think that this backdrop would lead to at least a somewhat positive investor sentiment toward REITs. But the opposite is true.

Valuations have compressed significantly and are now at near their lowest levels since the great financial crisis.

This valuation might make sense in a "higher for longer" scenario in which interest rates go even higher and stay there for longer. But the likelihood of that scenario playing out appears to be falling every day as inflation slides downward and the economy weakens.

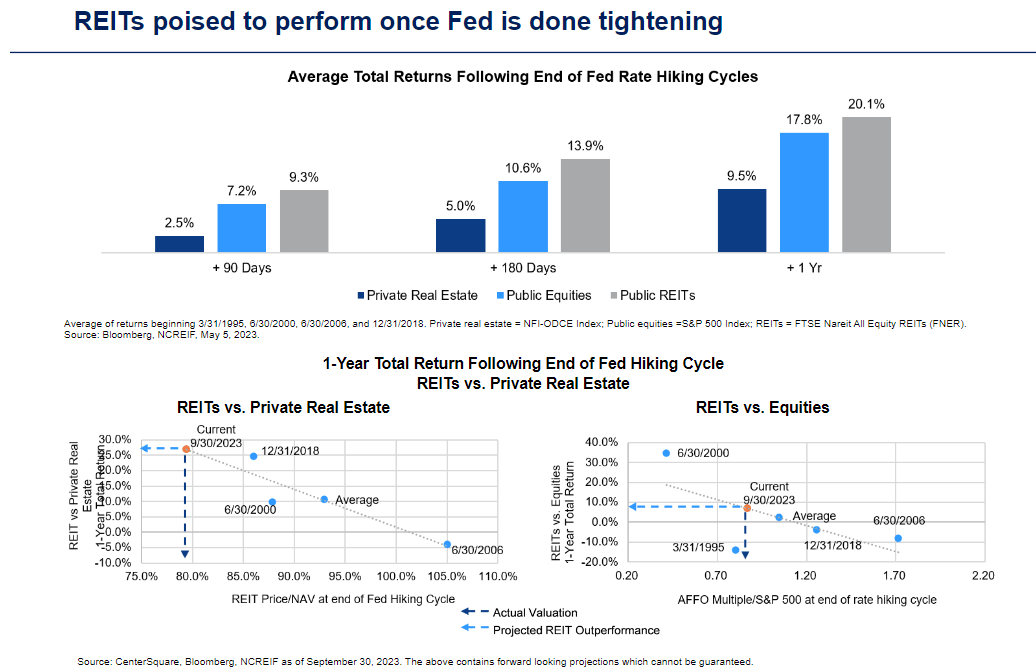

A consensus is forming that the Federal Reserve is completely done with rate hikes and that the next Fed move will be a rate cut .

Historically, REITs have strongly outperformed in the 3-12 months following the definitive end of rate hikes.

{kind=link}

We do not see any reason to believe this time will be different.

In fact, given the level of underperformance REITs have suffered over the last few years, we believe REITs should outperform the broader stock market by a significant degree in the next year.

But not all REITs will perform equally well, of course. Some will have a tepid recovery, while others will soar, generating huge gains for those who opportunistically bought during the downturn.

Here are two of those REITs that we think will rebound magnificently in the quarters and years ahead. We truly believe the current prices represent once-in-a-decade buying opportunities.

1. Alexandria Real Estate Equities ( ARE )

ARE is a REIT every dividend growth investor should at least be familiar with. With over 30 years of sectoral focus, the company has established itself as the leading landlord-developer of Class A, state-of-the-art, unbeatably located life science real estate in the United States. These are buildings used for biotech research and development.

ARE doesn't just own standalone life science buildings. They own multi-building campuses that benefit from the innovation-enhancing effects of clustering together, typically adjacent to world class research universities.

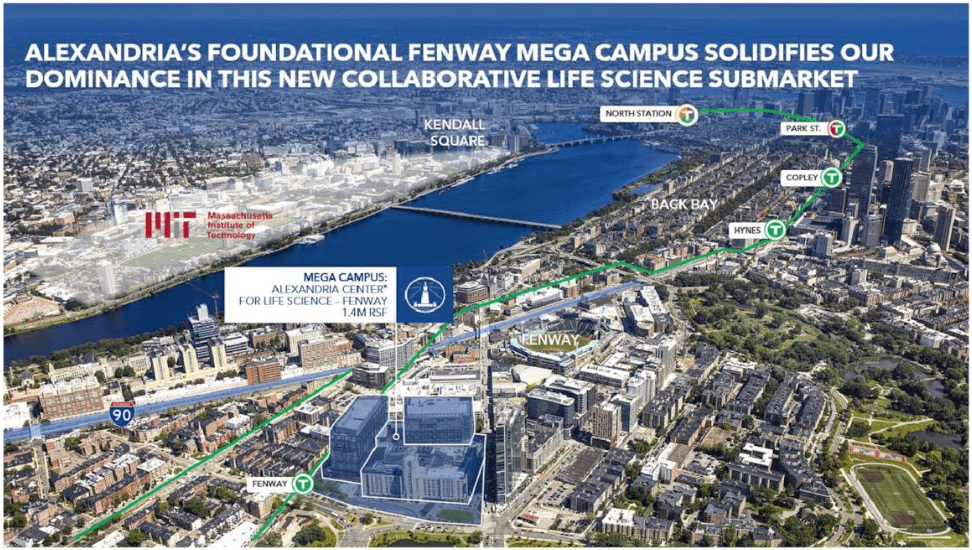

Take, for example, ARE's mega-campus located right across the bay from MIT and just a short walk from Fenway Park in Boston, Massachusetts, perhaps the most preeminent life science market in the world.

{kind=link}

Or take ARE's near-monopoly on life science properties directly adjacent to UC San Francisco.

{kind=link}

ARE's stock price has dropped ~45% since the beginning of 2022, largely because the market is concerned about the amount of new life science real estate properties under development. COVID-19 spurred a big wave of new development in this space. Plus, the market fears that a continuous supply of traditional office buildings will be converted into life science facilities in the coming years, adding further to the supply glut.

What we believe the market misunderstands is that location, building quality, and landlord reliability are collectively a powerful competitive advantage .

The locations seen above are very close to world class research universities, from which biotech companies can tap a continuous output of scientists. Moreover, these are all supply-constrained markets with limited available land or redevelopment opportunities near the locus of innovation.

Moreover, building quality is immensely important in attracting biotech tenants. ARE designs its buildings to be highly secure and energy efficient? That latter element is important because life science research requires a lot of energy usage.

Finally, ARE has established itself as a leading life science landlord over the last three decades. Put simply, "Alexandria" means quality in this space. ARE has brand power.

Most of the new supply of life science space entering the market is not directly competitive with ARE because of its subpar location, building quality, or landlord trust.

Add to this ARE's top-notch balance sheet strength as defined by these metrics...

{kind=link}

...and you've got a REIT that exudes strength on both sides of the balance sheet.

In terms of valuation, ARE has not been nearly this cheap since the Great Financial Crisis.

ARE currently trades at a strikingly low 11.6x AFFO. That's almost half of its average (not peak!) P/AFFO ratio of about 21.5x from the last five years. Just reverting to its 5-year mean would generate an 85% upside, but even if ARE only returned to a 18x valuation multiple, the upside is still high at 55%.

And that's on top of an almost 5% dividend yield and mid-single-digit AFFO per share growth!

2. Camden Property Trust ( CPT )

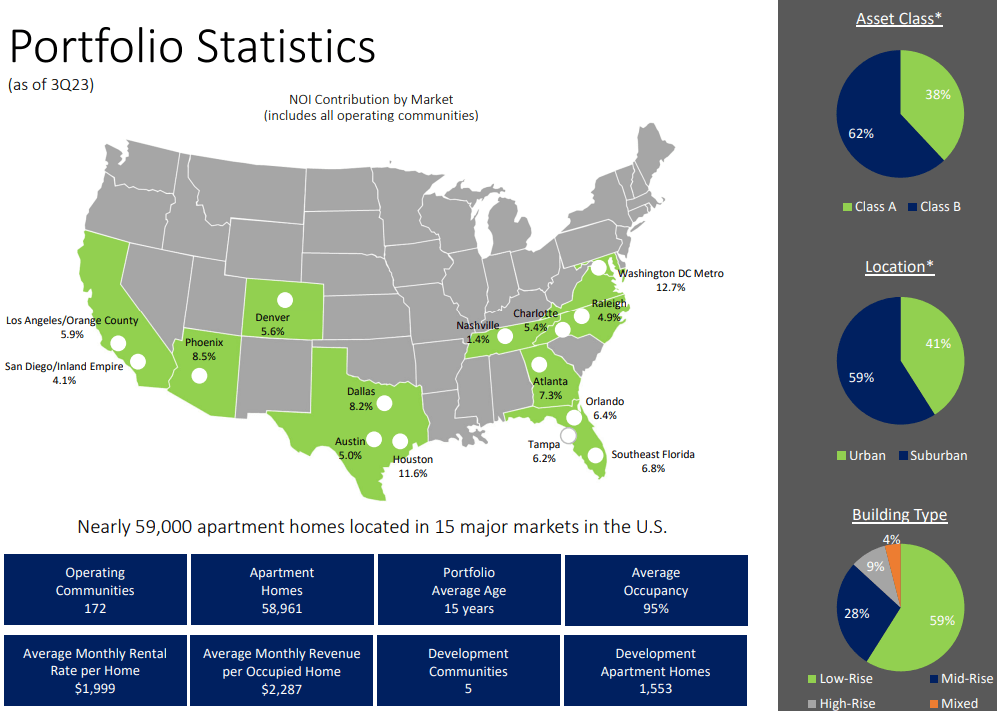

CPT is a blue-chip multifamily landlord-developer in the Sunbelt. Aside from exposure to Washington DC and Denver, CPT is entirely focused on the fast-growing Sunbelt region with a heavily diversified portfolio.

{kind=link}

Due to lower costs of living, lower taxes, and greater job growth, the Sunbelt region has enjoyed a strong population influx in recent years and likely will continue to do so for the foreseeable future.

CPT stands to gain from this, whether people are moving into urban areas (41% of the portfolio) or suburban areas (59%), whether they opt for higher rent Class A apartments (38%) or moderately priced Class B units (59%).

CPT even has a few irons in the single-family build-to-rent fire through two SFR developments in Texas.

Just as for ARE, the market's primary concern with CPT is the wave of new supply coming to market over the next year or so. But again, location within each individual market is a competitive advantage for CPT, because the best locations in most cities have already been built out, leaving mainly the less well located land for development.

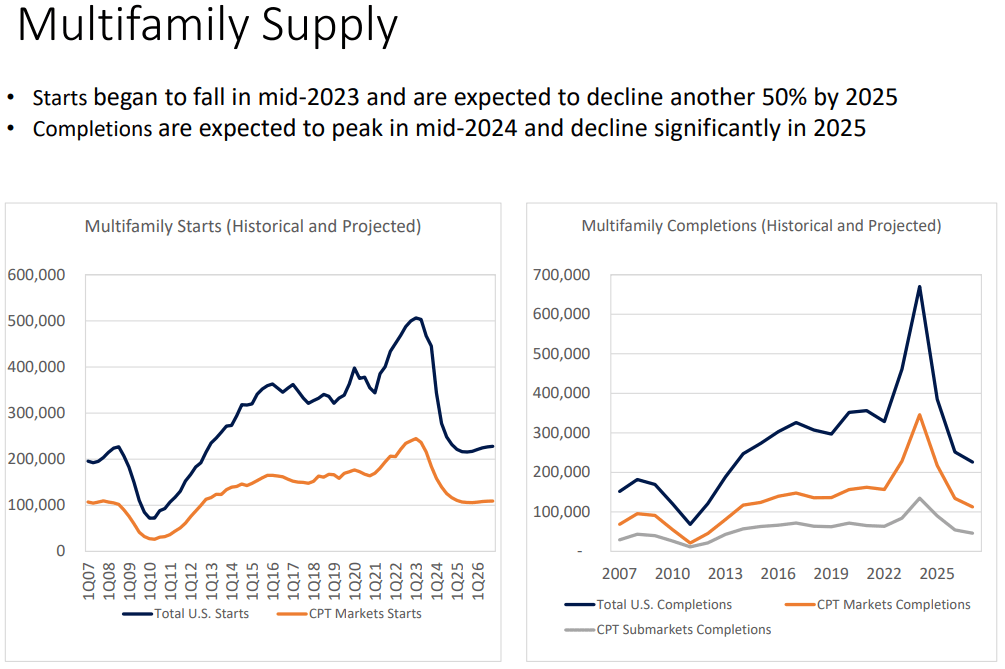

Moreover, because of the sharp increase in interest rates over the last year, new multifamily starts have fallen off a cliff, which means that in 2025 and after, completions should be even lower than during the post-GFC period from 2014 through 2022.

{kind=link}

This means that there is light at the end of the tunnel. Supply headwinds are temporary, while population growth and housing unaffordability are longer-term tailwinds.

The market also seems to worry about the fact that 23% of CPT's debt is floating rate, but management is unperturbed, viewing the current period in which short-term rates are higher than long-term rates as an anomaly that won't last forever.

CPT's A- credit rating speaks to its balance sheet strength.

This is another REIT trading at a once-in-a-decade low valuation.

The REIT's current price/core FFO of 13.0x sits well below its 5-year average of 20.5x, implying an upside of 58% if CPT just returns to its recent average valuation. But even just getting back to an 18x multiple would generate roughly a 40% stock price upside on top of CPT's 4.5% yield and mid-single-digit growth rate.

Bottom Line

The rising interest rate cycle has dealt a heavy blow to investor sentiment toward REITs. But fundamentals have held up just fine, and as the narrative changes from "rising rates" to "falling rates," REITs should enjoy a nice period of outperformance.

Don't take our word for it. Look at the historical record.

Right now, REITs are overlooked in favor of bonds and mega-cap tech stocks, but that won't always be the case. We are confident that REITs will enjoy their time in the sun again.

In the meantime, we will keep loading up on these once-in-a-decade opportunities.

For further details see:

2 Once-In-A-Decade REIT Buying Opportunities