VNQ - 2 REITs Aggressively Repurchasing Shares

2023-12-05 08:05:00 ET

Summary

- REITs are priced at their lowest valuations in over a decade.

- And many of them are buying back shares to create value.

- I highlight 2 of my favorite opportunities.

In our recent articles , we have explained that real estate investment trusts, or REITs (VNQ), are today priced at their lowest valuations in a decade.

Their share prices have crashed over the past 2 years even as their cash flows kept on rising. As a result, there are many REITs that are now priced at large discounts relative to their net asset values:

The best proof of that is the many REITs that are now buying back shares and insiders who are loading up on their own stock to take advantage of the low valuations.

Here are two such opportunities:

Farmland Partners Inc. ( FPI )

Farmland Partners is a farmland REIT.

In short, we are very bullish on the company because:

- We think that farmland is a great investment that's likely to keep gaining value over the long run because of the supply/demand imbalance that's caused by the growing population, rising middle class, changing diets, global warming, and declining supply due to better-use conversions.

- Farmland Partners is a leveraged play on this long-term appreciation.

- The shares are today trading at $12, but we estimate their NAV per share at around $18, meaning that it is priced at 67 cents on the dollar.

- The management is today taking advantage of this discount by selling properties and buying back shares - all while paying down debt.

- They are also building an asset management business that we expect to earn significant fee income in the long run as they scale up their external assets under management.

- Finally, farmland provides nice diversification benefits to our portfolio.

And the interesting thing is that farmland has kept gaining value in 2023:

{kind=link}

But despite that, FPI's share price has dropped to lower levels:

As a result, the discount to NAV has actually expanded in recent months, and the management is now doubling down on its efforts to unlock this value by selling properties and buying back stock.

Just recently, they announced that it had sold another $70 million worth of properties. This brings the total to $120 million year-to-date, which is very significant given that the company only has a $500 million market cap.

These sales happened at a 17% average gain, and that's despite selling some of their weaker non-core properties in water-challenged areas.

The Chairman of the company made this clear on their recent conference call :

"Please recognize that we are not selling our very best farms. We are selling farms where we are concerned of water challenges or market volatility challenges or they are outliers for some reason in our portfolio. The appreciation we have in the parts of the portfolio, we are not selling are even stronger than those that we are selling."

The CEO of the company made the following additional comments concerning their most recent asset sales (emphasis added):

"We sold more than 30 farms this summer - many of which were in water challenged areas - and captured strong asset appreciation returns for our shareholders," said Luca Fabbri, FPI's President and CEO. "These sales show the continued strength of the farmland market and enabled us to create value for our shareholders through stock repurchases at a discount to their underlying value, and to redeploy capital on other priorities like debt repayment and new acquisitions in more sustainable locations."

So they are selling assets at a premium to NAV to buy back shares at a large discount to NAV - all while paying down their floating-rate debt.

That's a great move and it shows that the company is managed in the best interest of shareholders. They are not just trying to grow the portfolio to justify higher salaries. On the contrary, they do not hesitate to scale down operations to create value for shareholders.

And it gets better:

FPI's Chairman, Paul Pittman, just bought an additional $1 million worth of shares in the open market. That's despite already owning $25 million worth of shares, which represents the bulk of his net worth.

Paul Pittman is one of the most knowledgeable farmland investors in the world so you couldn't ask for a stronger vote of confidence than this:

{kind=link}

He said the following on a recent call (emphasis added):

"As all of you know, I'm a large shareholder myself, and we are taking actions that are fundamentally arbitraging very high values for Farmland against a deeply discounted stock. We will continue to do that as long as it takes to get our shareholders rewarded. "

We believe that as they continue to sell assets, buy back shares, pay down debt, and interest rates eventually return to lower levels, the shares of FPI will rerate at a materially higher level. The upside potential could be more than 50% given how discounted the shares have become, and much more in the long run, especially if they manage to create the asset management business that they have been talking about.

RCI Hospitality

RCI Hospitality Holdings, Inc. ( RICK ) is not officially structured as a REIT, but it essentially functions as one. It is the only publicly listed company that specializes in the ownership and management of nightclubs. In case you are not familiar with the company, you can start by reading our investment thesis by clicking here.

Its share price has dropped significantly over the past year, even as its cash flow kept rising:

RCI Hospitality

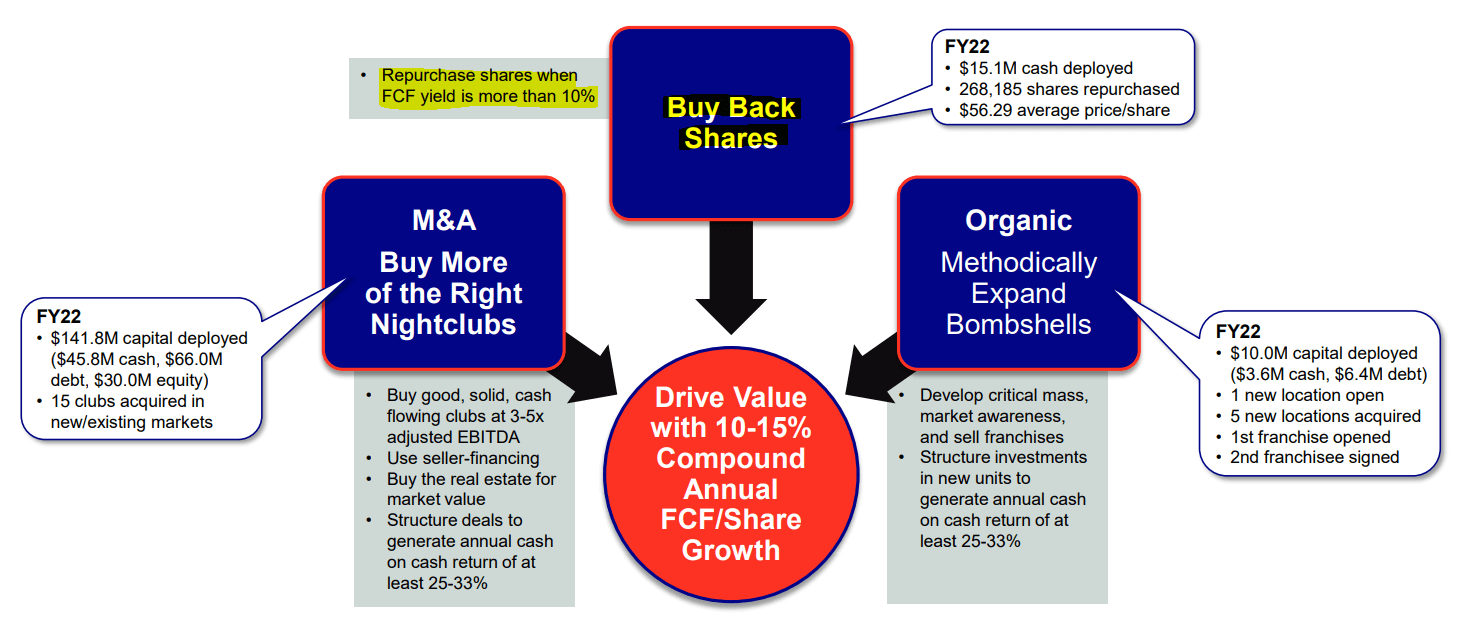

As a result, the management is now buying back shares.

RICK has a clear capital allocation plan to buy back shares whenever they are priced at a >10% FCF cash flow yield and we are well in excess of that today.

{kind=link}

Earlier this year, they said that they would buy back shares if they traded at $72 per share or less.

Today, they trade at around $550, and so they have been buying about $100,000 worth of shares each day.

I think that now could be a particularly good time to buy more shares of the company because we are now approaching the end of the period of tough comps, which is really what caused this recent sell-off. Their same-property numbers dropped in recent quarters because things had been normalizing in the post-COVID world. Here is what the CEO tweeted recently (emphasis added):

"Many things have been affecting us. Bombshells had huge post Covid surge so we are up against tough comps. We have some labor tightness we have had to deal with and most recently extreme temperatures in Texas which killed out late night. Which is mainly appetizers and Liquor.

On the club side, comps have been great for about 2 years with free money and low rates. Slowing economy always hurts for a couple of quarters as we adjust from quality of guest to quantity of guests. summer vacations and a return to a more normal business cycle I think added additional pressure on SSS. Adjustments have been made and comps get easier in mid November. Let's see what it all looks like in December. If you listen to the last earnings call you will hear me warn that this quarter would be weaker and that I expect to recover in 1Q24. "

So the comps should be getting better starting in November and they expect a recovery in same-property sales in early 2024.

Then on top of that, RICK has many tailwinds going into 2024. The new casinos will open and are expected to add ~$1 per share to free cash flow ("FCF") once they are stabilized. This is huge for a company that's currently earning $7-8 of FCF per share.

Finally, they have hinted at new club acquisitions in recent calls and they have the cash for it. If they announced another major deal, this would only add more upside.

So, all in all, we think $55 per share is way too cheap and we are happy to get the chance to accumulate more shares at these low levels.

Insiders have also made a number of purchases over the past month:

{kind=link}

Bottom Line

The management knows best what's the fair value of their assets.

If they are aggressively buying shares, that's a strong hint that perhaps their stock might be undervalued.

But if on top of that, you also have significant insider purchases, then that's a very strong vote of confidence.

There are many such cases in the REIT sector today.

For further details see:

2 REITs Aggressively Repurchasing Shares