BYLOF - 2 REITs All Investors Should Own

2023-11-06 08:05:00 ET

Summary

- There are a handful of REITs that could fit most portfolios.

- They offer a combination of high yield, growth, upside, and safety.

- We highlight two such REITs that we are buying heavily.

The real estate investment trust, or REIT (VNQ), market is vast and versatile.

Some REITs are ideal for income investors.

Others are better suited for growth investors.

And some are very speculative and only intended for deep-value investors.

With over 200 REITs in the U.S., there is truly something for everyone.

But there are some exceptions that could make sense for most investor's portfolios. I am here referring to a handful of REITs that check all the boxes:

- They have resilient fundamentals,

- They enjoy attractive growth prospects.

- They offer good value for money.

- They pay a high dividend yield.

- And offer some upside potential to top it all off.

Put simply, they offer the potential for above-average returns with below-average risk, which is precisely what "alpha" is all about.

Here are two examples of such REITs that most investors should consider for their portfolio:

Big Yellow Group Plc (BYLOF) [BYG]

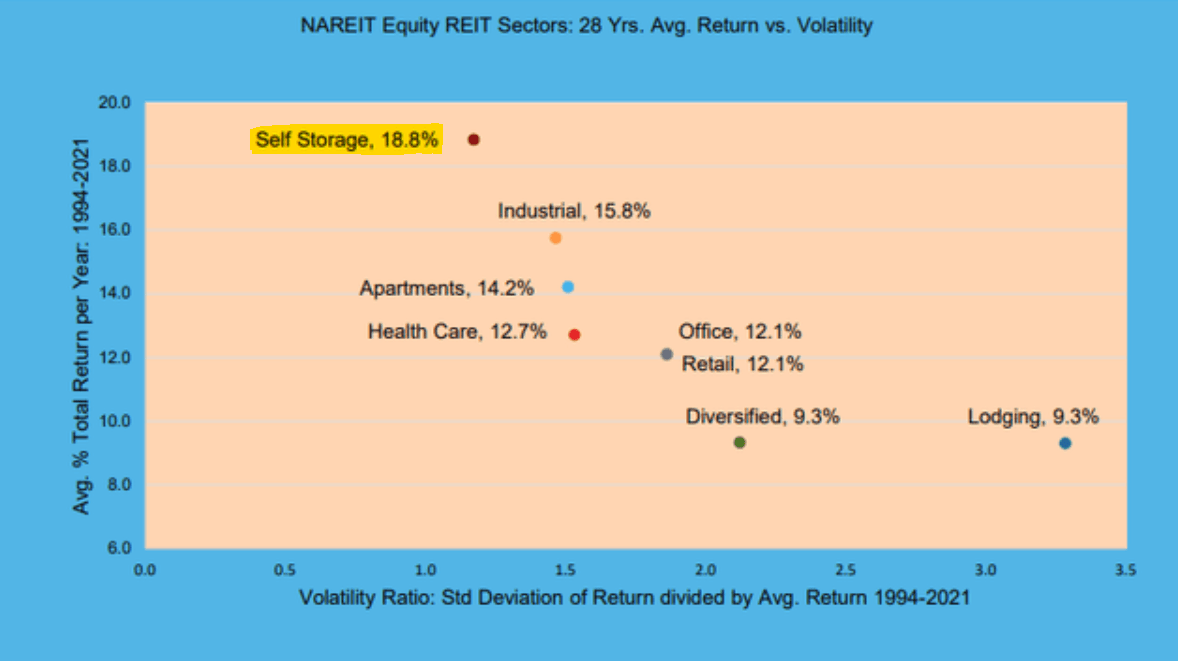

Big Yellow is our favorite self-storage investment.

U.S. self-storage REITs have been incredibly rewarding over the past ~30 years, returning nearly 20% annually.

They were so rewarding because they were able to earn abnormally large spreads over their cost of capital as they developed new properties and took over the operations from unsophisticated owners and materially improved their cash flows thanks to revenue-management systems, national advertising, economies of scale, etc.

{kind=link}

But now the U.S. market is very competitive and the opportunity isn't as compelling anymore.

However, Europe is still 20 years behind. and I think that Big Yellow is set to replicate this successful model in the UK.

Today, there is 10x less storage space per capita in the UK than in the U.S., but the concept is rapidly growing in popularity and Big Yellow is capitalizing on this opportunity as the market leader.

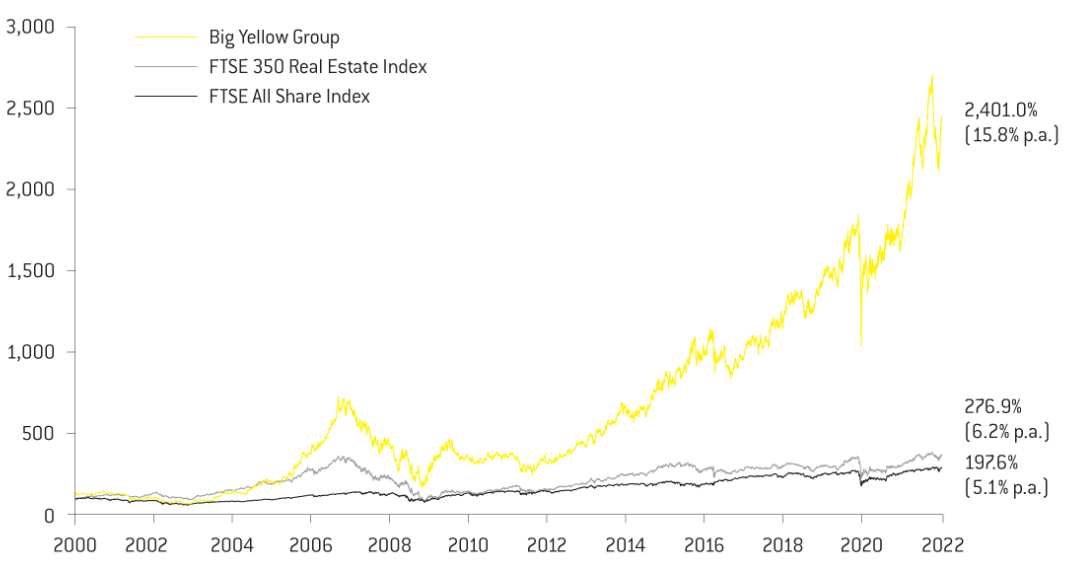

Its early results have been phenomenal, compounding investors' capital by ~16% per year, despite suffering a big setback during the great financial crisis. Importantly, it is today still early in its growth phase with its $2.5 billion market cap vs. $43 billion for Public Storage (PSA) in the U.S.:

Big Yellow Group Big Yellow Group

{kind=link}

Therefore, whenever Big Yellow is offered at a discount, I buy more shares. I first started buying shares following the Brexit crash in 2016 at around 650 British Pence, and I have repetitively bought more shares whenever it would dip and it has been one of my best investments ever.

Today, the shares are priced at around 1,00 British Pence (down from 1,707), a 25% discount to our estimate of NAV, and a 4.5% dividend yield.

It is not the cheapest REIT out there, but it has a long runway of rapid growth potential, which I expect to result in above-average returns with below-average risk over the long run.

A simple rule of thumb is to buy shares whenever the dividend yield crosses the 4% level and we just crossed it recently.

Essential Properties Realty Trust, Inc. (EPRT)

Net lease properties are some of my favorite real estate investments and I invest heavily in them as part of my REIT portfolio. In case you are not familiar with net lease properties, these are typically freestanding, single-tenant, service-oriented properties such as CVS (CVS) pharmacies, Dollar General (DG) convenience stores, or Chevron (CVX) gas stations:

Realty Income Essential Properties Realty Trust

{kind=link}

{kind=link}

What makes these properties uniquely attractive is that their leases are structured in a way to generate highly resilient cash flow:

- Very long leases of over 10 years

- Pre-set annual rent escalations

- The tenants pay all property expenses, including maintenance.

Moreover, because the property is the tenant's profit center, they are unlikely to want to ever move out as long as they can turn a profit, and the rent coverage ratios are typically over 3x, meaning that there is a significant margin of safety even in the case of a recession.

As a result, net lease properties tend to generate equity-like returns with bond-like risk and significant income.

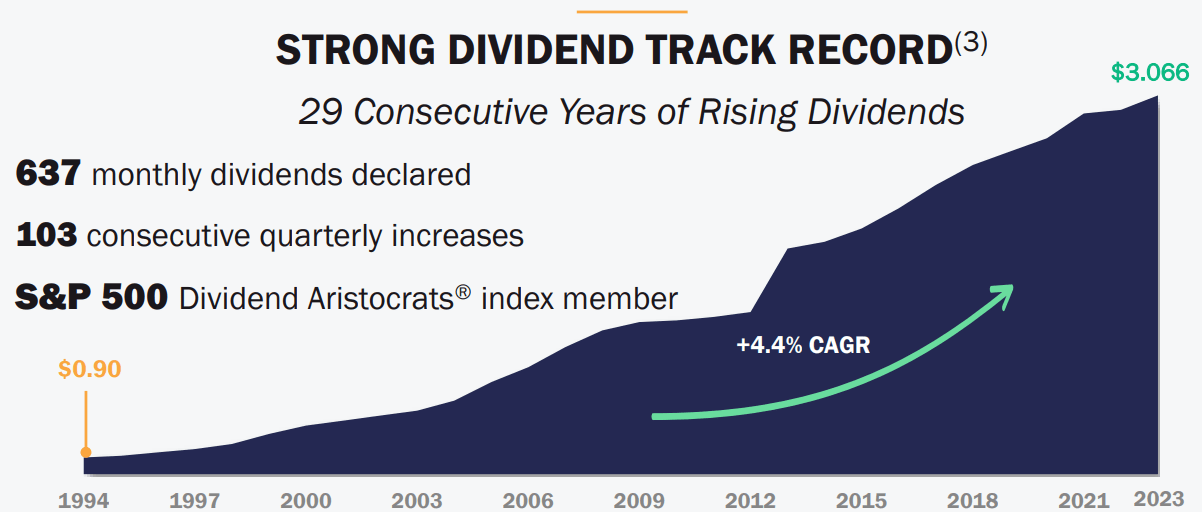

The track record of the biggest net lease REIT, Realty Income (O), is proof of that as it has managed to generate 15% average annual total returns since going public all while growing its dividend for nearly 30 years in a row. Not even the dotcom crash, the great financial crisis, or the pandemic could stop its growth:

{kind=link}

Well, Essential Properties Realty Trust puts this same strategy on steroids.

Instead of targeting net lease properties that are occupied by big-name tenants like CVS and Dollar General, it tends to go after properties that are leased to smaller and lesser-known middle-market tenants.

The reason why it does this is because there is far less competition for these assets, and this allows it to acquire these assets with even better lease terms to target higher returns:

| Typical net lease property |

| Essential Properties Realy Trust |

| Cap rate |

| ~6% |

| ~8% |

| Lease term |

| ~10 years |

| ~15 years |

| Lease escalations |

| ~1% |

| ~2% |

| Landlord responsibility |

| Potentially for the maintenance of the roof, structure, and parking lot |

| Zero |

| Access to tenant's financials |

| No |

| Yes |

| Additional protection from master leases or corporate guarantees |

| No |

| Yes |

The risks of these properties are of course slightly higher, but the difference is not significant because:

- What really matters is the unit-level profitability of the tenants and the coverage metrics are comparable.

- Moreover, because EPRT enjoys stronger bargaining power it is able to demand additional protections in the form of master leases, corporate guarantees, and access to the tenant's financials.

- Finally, EPRT includes these higher-yielding properties as part of a well-diversified portfolio that's actively managed to mitigate the risks of individual assets.

In the end, EPRT earns above-average returns without taking significant incremental risk. The proof is that even the pandemic, which was the worst possible crisis for a company like EPRT, didn't put it down. The company kept growing its cash flow and dividend throughout the crisis and has massively outperformed its peer group since going public:

I believe that this outperformance is set to continue for a long time to come because EPRT is today still relatively small in size (8x smaller than Realty Income), it has the least leverage in its peer group and has significant liquidity to keep acquiring more properties.

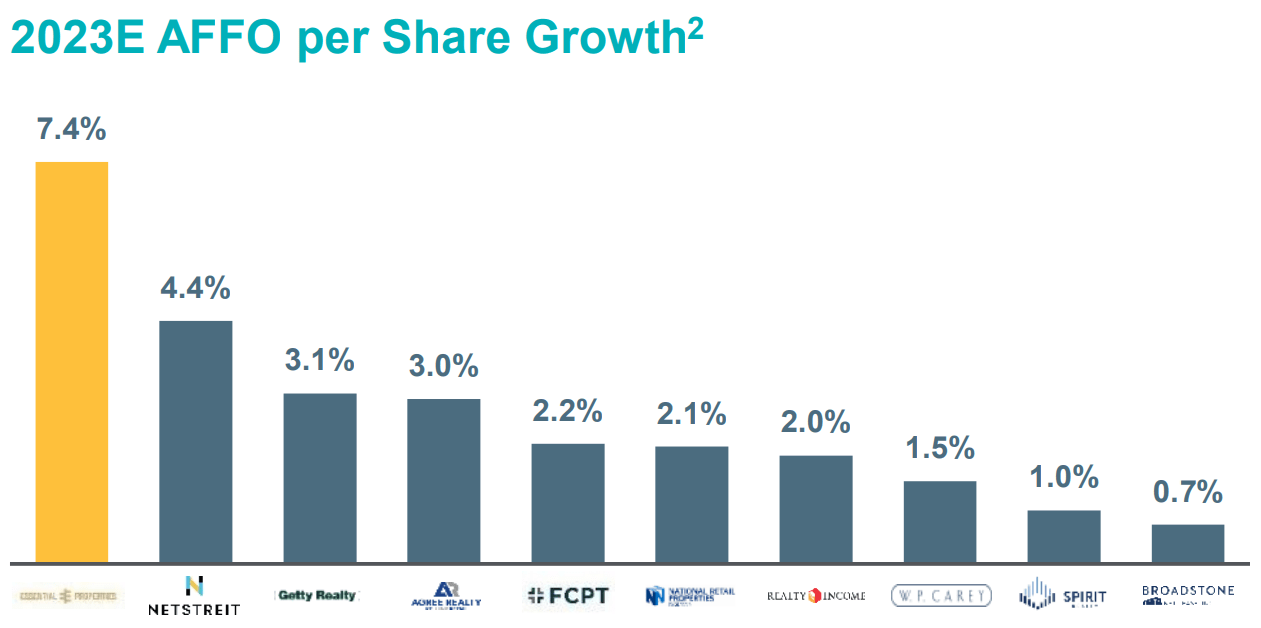

This year, it has guided to grow its AFFO per share by 7.4%, which is the fastest growth rate in its sector:

Essential Properties Realty Trust

{kind=link}

Moreover, the management has guided for steady growth to continue in 2024 and 2025 because it isn't materially impacted by the surge in interest rates.

Even then, today it is priced at a slight discount relative to its close peers, despite growing faster and having less leverage.

| Net lease REITs |

| Essential Properties Realy Trust |

| P/FFO |

| 13x FFO |

| 12.5x |

EPRT is priced at just 12x FFO and it pays a 5% dividend yield.

Add to the yield the 7% growth rate and you get to a 12% annual total return without any upside from repricing.

But over time as the market learns more about EPRT, we expect it to eventually price the company at a premium valuation given its faster growth prospects.

If its valuation multiple expands to 15x over the next 3 years, this would result in 15-20% average annual total returns when you include the yield and the growth.

That's very compelling coming from a REIT with less risk than average and this is why EPRT is a big anchor in our Portfolio.

Bottom Line

Some REITs really stand out and EPRT and BYG are two great examples.

Both focus on property niches that have historically been far more rewarding than the average and they implement unique strategies that are expected to result in above-average returns with below-average risk.

Even then, the market is today pricing them at very reasonable valuations, which makes them interesting investment opportunities for most investors.

For further details see:

2 REITs All Investors Should Own