O - 2 REITs Dumped In The Bargain Bin

2023-04-26 17:55:12 ET

Summary

- Both down more than 35%.

- Both get bullish outlooks.

- These REITs are my portfolio.

I want to highlight two REITs that were left in the rubbish pile. To get included in this list, the REIT must be down substantially from its 52-week high. That narrows the list down from all REITs to almost all REITs.

First REIT

The first REIT on the list is Crown Castle International ( CCI ). If you have alerts turned on for CCI, you're used to getting a burst of articles once per month followed by several weeks of silence. How about we touch on some deeper topics? I just wrote a new report on CCI's Q1 2023 results for our members. That's not a summary of the earnings release, but most people probably expect that for an earnings update.

We contacted investor relations at Crown Castle International yesterday to request clarification on some of the commentary from the earnings call. No response yet, but it's only been about 24 hours.

Valuation

I want to highlight something I found very interesting. In my opinion, this is the most interesting recent development. I pulled two high-quality REITs that have delivered respectable growth over the last decade. These are both REITs that are not strongly tied to net asset value. Instead, it is usually more useful to look at them with AFFO multiples.

The comparison is CCI vs. Realty Income ( O ).

Here are the metrics:

- CCI has a 5.10% dividend yield and a 16.07 AFFO multiple.

- O has 4.93% dividend yield and a 15.57 AFFO multiple.

Note: Prices were pulled during market hours. At the market close, it was 16.00x AFFO for CCI and 15.55x AFFO for O.

I will regularly tell investors not to focus on yield, but there's a good point in this one little niche scenario. We have two very different REITs, but they have similar AFFO multiples and similar yields. Consequently, they also must have similar payout ratios. These are very different businesses, but on these metrics, they are similar.

The following chart compares the AFFO multiples across time:

TIKR.com

You'll notice that CCI had a much higher multiple from early 2020 through early September 2022. There's one thing that would generate such a vast disparity in AFFO multiples. Investors expected significantly different growth rates in AFFO per share.

Growth Rates

I'm going to skip over a few of the charts and jump to the growth rates.

We can compare the average growth rate for 2015 to 2022 with the growth rate from 2022 to 2027 consensus estimates:

| Growth Rates |

| 2015 to 2022 |

| 2022 to 2027 |

| CCI |

| 8.10% |

| 1.11% |

| O |

| 5.27% |

| 5.92% |

Is that quality forecasting? Only if you consider "low quality" to be a form of quality. These forecasts imply that CCI's growth rate would drop to 1.11% over the span of five years. That's not realistic. I believe this is why management repeated six times on the call that they expected to see a return to 7% to 8% annual growth rates.

These consensus estimates also assume that Realty Income's growth rate in AFFO per share will accelerate now that interest rates are much higher and it is more difficult to create accretive acquisitions due to higher interest rates.

Bad analysts.

Shares of CCI traded below $122 today. I responded precisely how an analyst should respond when they see a sale:

Charles Schwab

That was disclosed in real-time in the CCI trade alert for members of The REIT Forum, and it was explicitly foreshadowed in the update we posted yesterday.

We already owned a significant position in CCI. That trade increased it even further.

Second REIT

The next REIT we will discuss is Alexandria Real Estate ( ARE ).

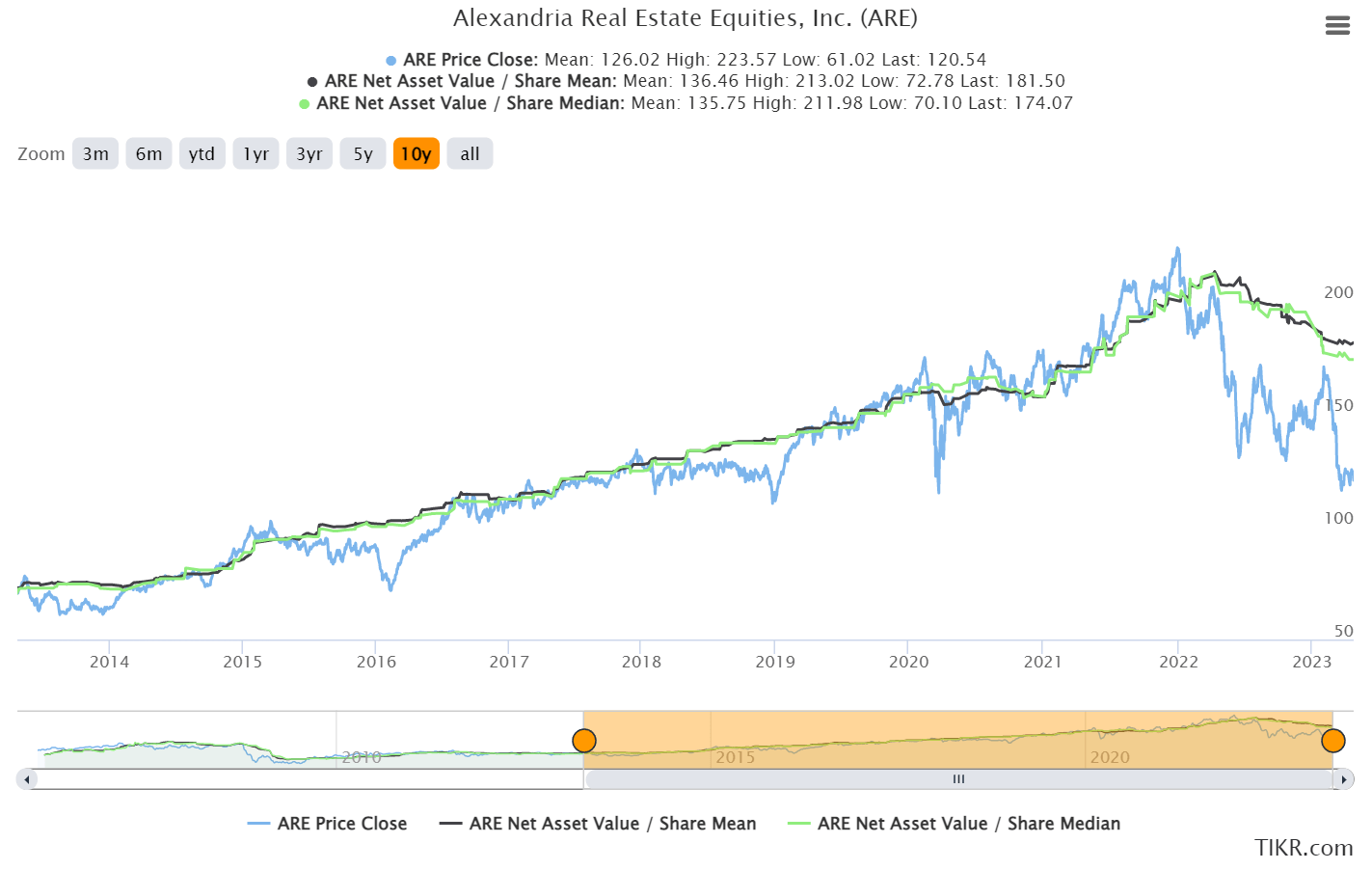

ARE trades at a big discount to consensus estimates of NAV (Net Asset Value). You can see it's big, because you can see how these lines diverge:

{kind=link}

TIKR.com

That makes it pretty easy. It's interesting to note that in the prior 10 years, shares often traded pretty close to NAV. Even during the pandemic, they rapidly recovered most of the decline.

As interest rates increased, we've seen a decline in estimates for NAV per share. Those estimates dropped from around $212 down to $181.5 for the average and $174.07 for the median. That's a pretty big drop. While the trend is clearly down, the median is already down about 18%. That's far enough to account for much higher interest rates pressuring real estate values.

As I'll cover later in the article, there's plenty of doubt about interest rates climbing much further.

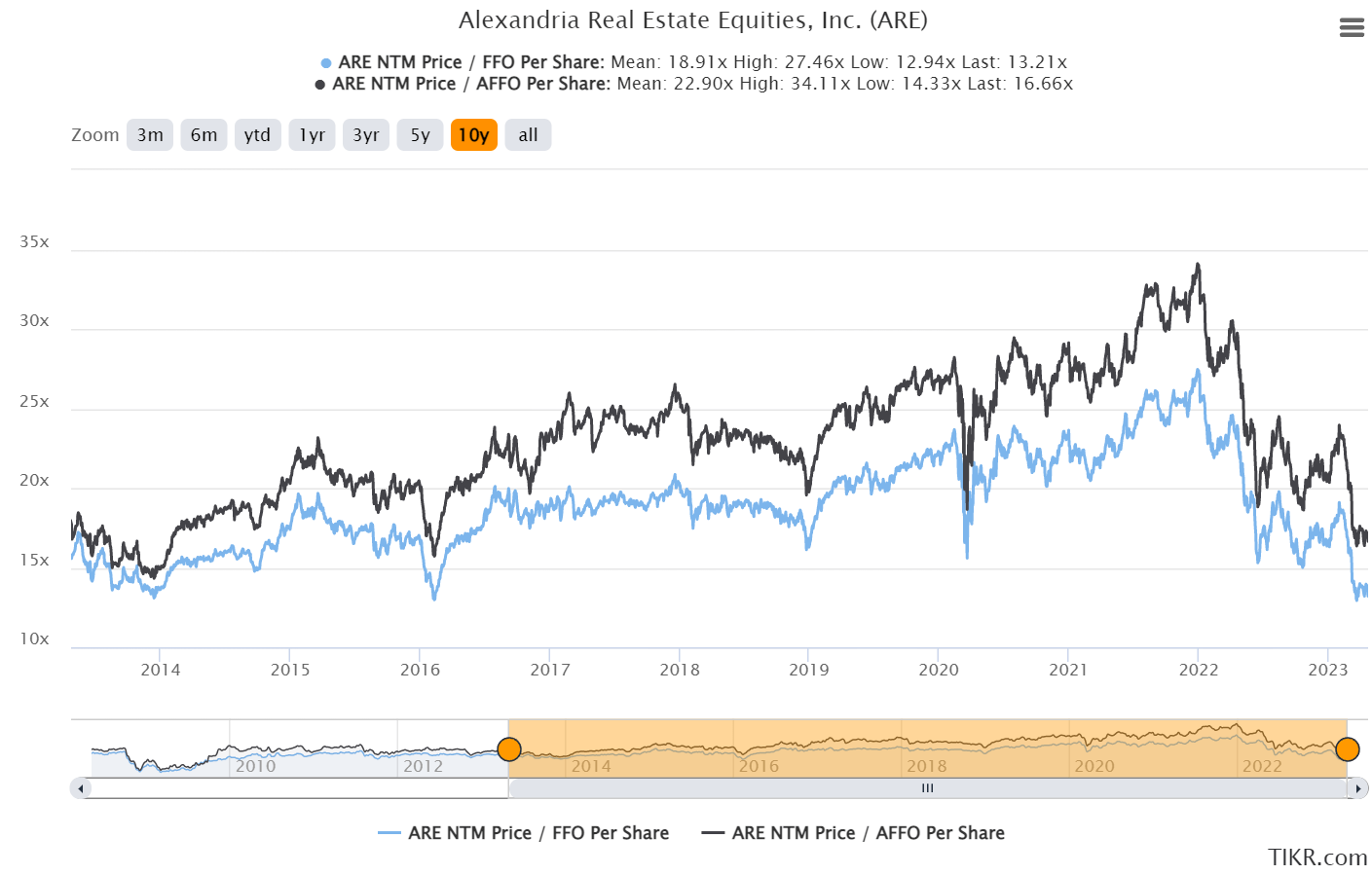

We can also evaluate ARE's valuation using FFO and AFFO multiples. Those are at historically low levels:

{kind=link}

TIKR.com

Remember when investors thought ARE was worth 34 times AFFO and 27 times FFO? I do. What did we do? Obviously, we didn't buy shares. Not at those valuations. However, when share prices plunged, we picked up shares:

Charles Schwab

Why is ARE so despised? One reason is probably that so many investors love to refer to it as an office REIT. It has very little exposure to office real estate. They had an office property in the portfolio and already decided to sell it. They took an impairment related to that one property.

The vast majority of the portfolio is in labs. Labs are different than office because labs are useful. Office real estate is a place some people commute to so they can do work in a louder environment than if they were working from home. Most of the time it's because their boss required them to do it. That makes it more difficult to recruit talent, which is a pretty bad outcome for spending the money to rent a fancy office building.

Try to do office work from home and see how you do. Did you manage to browse the internet? Send an e-mail? Maybe write an article about three REITs?

Simple enough.

Try to do lab work from home. I'll wait while you collect your specimens and run the tests. Yeah, that's not so easy to do from home. Lab real estate is in demand because the work cannot be done from home.

What if artificial intelligence enables breakthroughs that reduce the amount of lab time required for medical discoveries? Will that reduce the demand for labs? The tests will still need to be done for safety. If new medicines can be discovered faster, that should increase the output.

As it stands, a huge cohort is retiring and will be looking for new and better treatments that have yet to be developed.

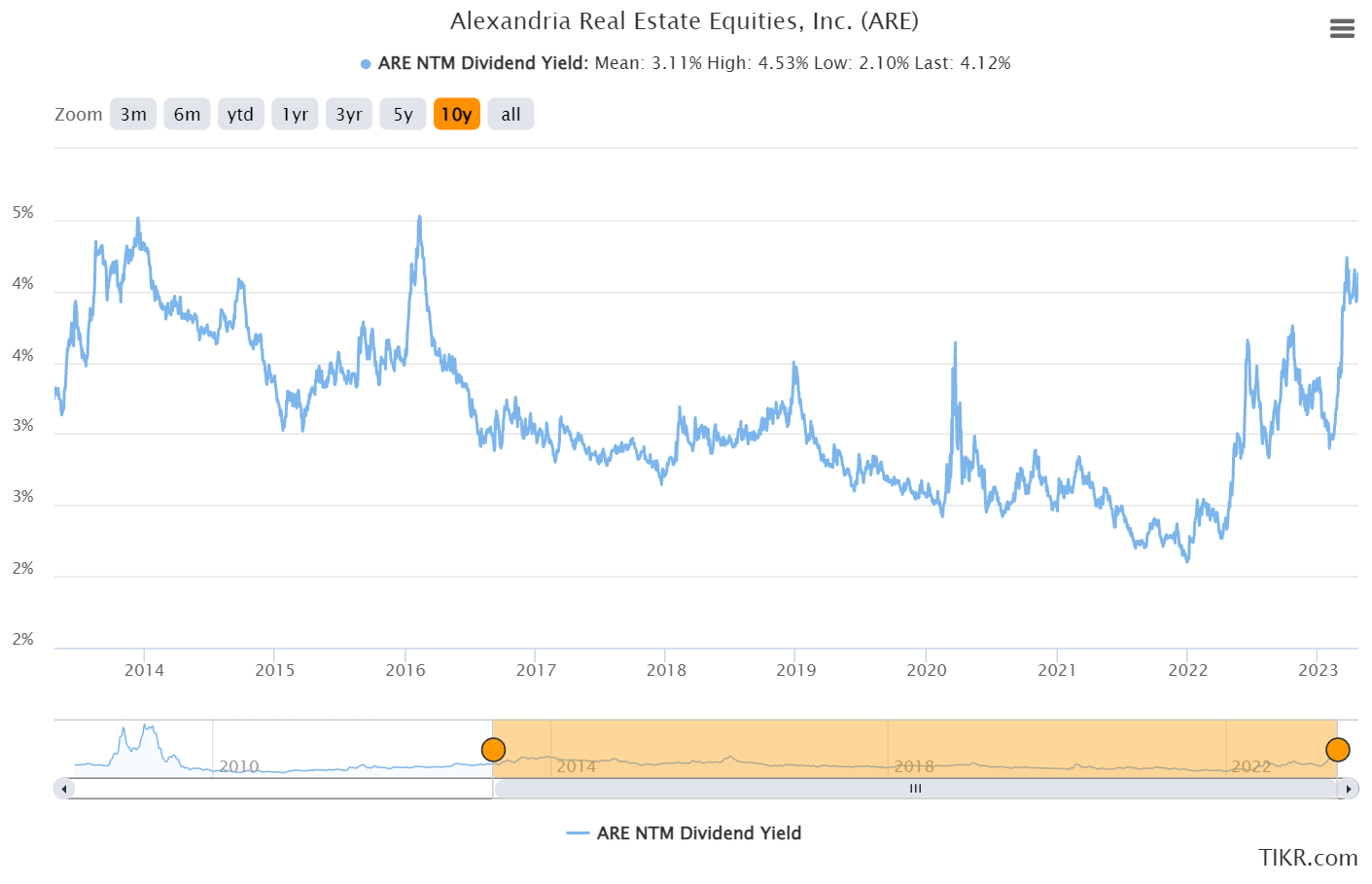

Maybe the 4% dividend yield isn't enough for you? We haven't seen it get much higher because ARE's share price tends to climb over time:

{kind=link}

TIKR.com

There are no cuts in there. The last time ARE had a dividend cut was in 2009. As I covered previously, ARE's balance sheet today is dramatically superior to its condition back then.

Forward Interest Rates

If interest rates remain elevated for a decade, that could put major pressure on interest expenses. That's not a realistic scenario. Even if it were, we've been picking REITs with strong balance sheets. Because these REITs have less debt, they are less exposed to a spike in interest rates.

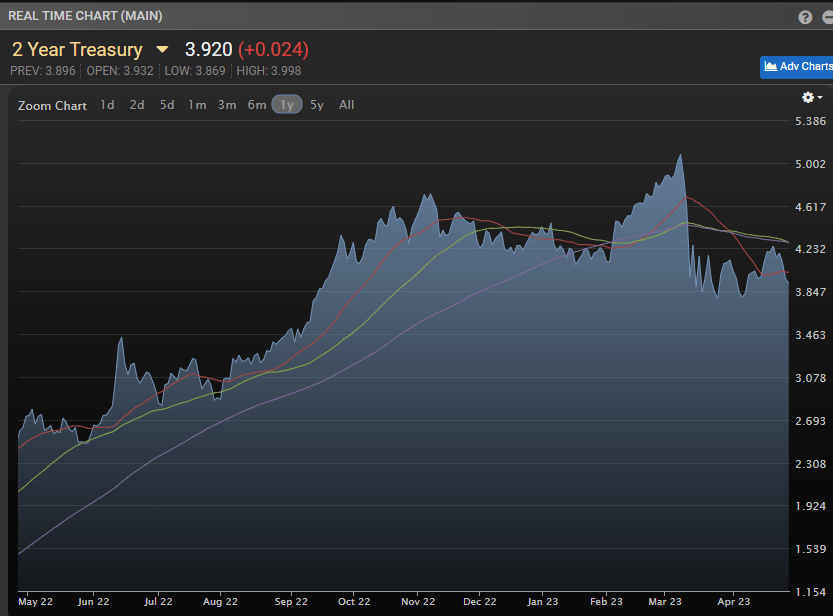

Even the 2-year Treasury rate has been falling as investors realize there won't be any justification for continuing hikes after the next few months.

{kind=link}

MBS Live

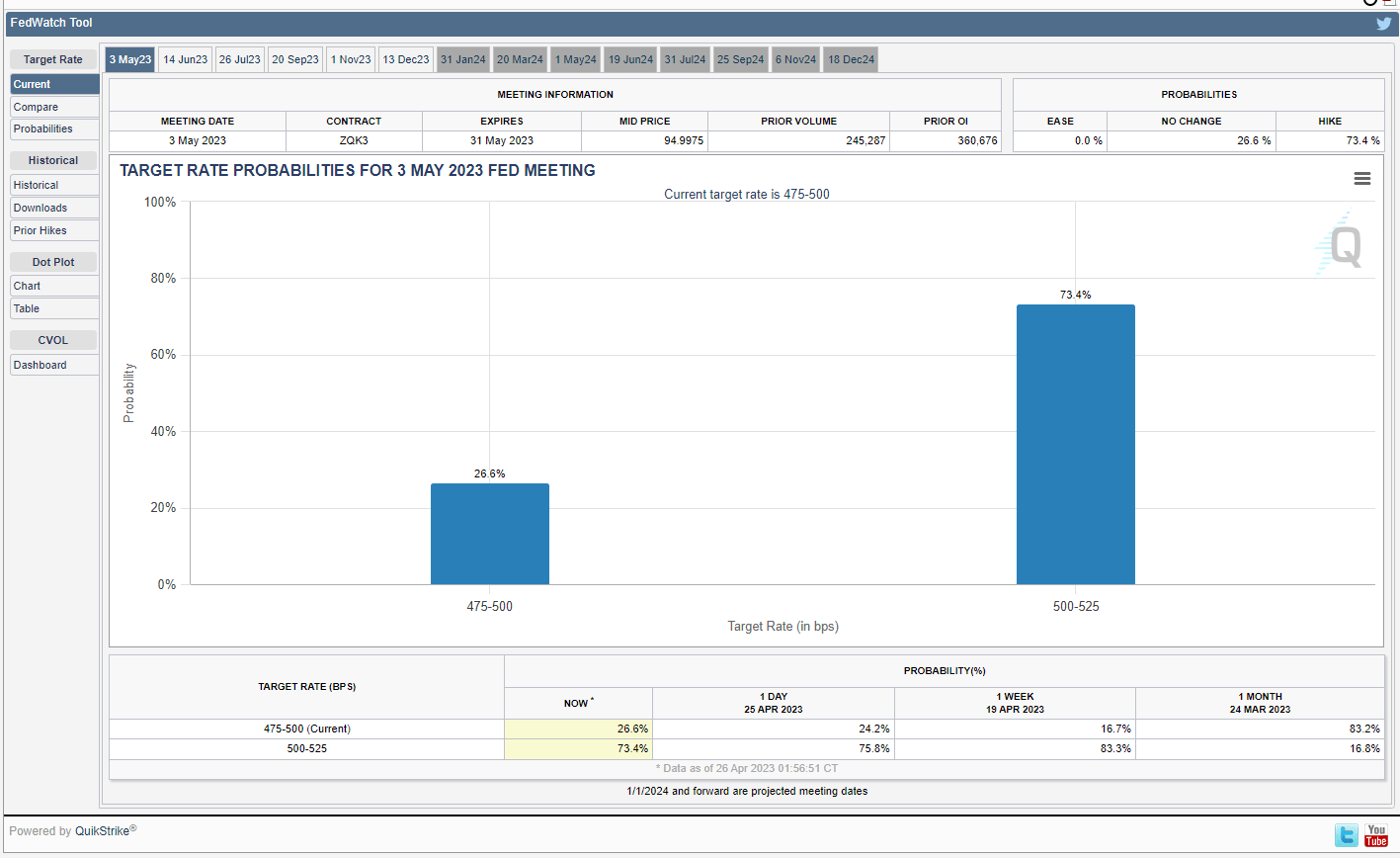

That 2-year Treasury rate of 3.924% is still higher than the 10-year rate of 3.42%. It is also much lower than the current fed funds target rate of 4.75% to 5%, or the expected target following the next meeting, 5% to 5.25%.

{kind=link}

CME Fed Watch Tool

If you look out to the end of the year, the debt markets strongly expect rates to fall:

{kind=link}

CME Fed Watch Tool

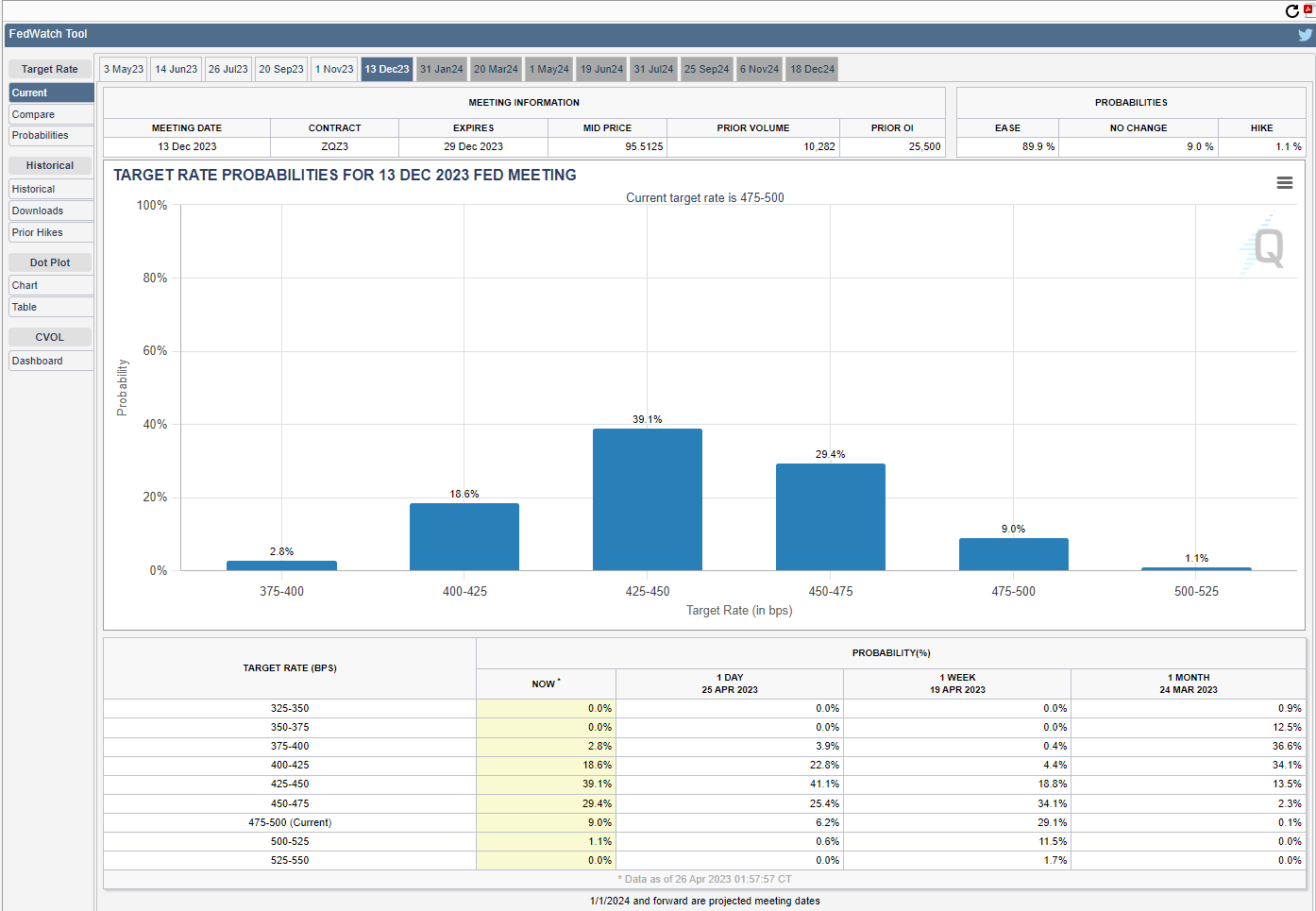

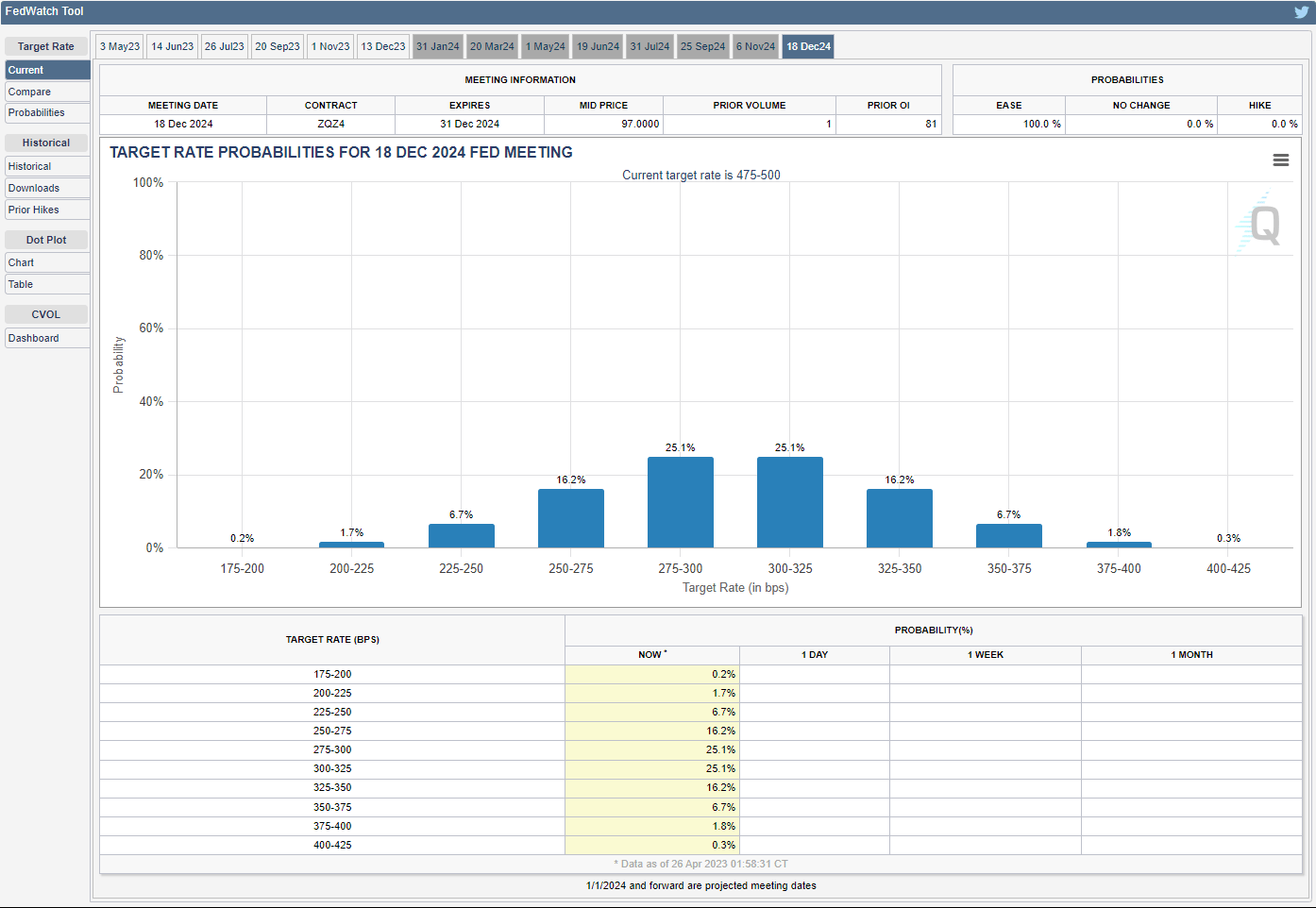

Going out to December 2024, the market really expects rates to be down materially:

{kind=link}

CME Fed Watch Tool

Conclusion

These are three REITs that saw dramatic declines in their share prices over the last 52 weeks.

- CCI is at 62% of the 52-week high.

- ARE is at 63% of the 52-week high.

Those are big drops. Sure, the market is scary.

The Federal Reserve is shoving interest rates higher and already has driven a few banks into failure. Higher rates are going to pressure earnings for many companies. As it stands, CCI is already dealing with the pressure from higher rates. That's already baked into their 2023 guidance. ARE has it factored it into their guidance as well, but their exposure is only slightly above none. That's not enough to be concerned about.

We also have a pending showdown over the negative $32 trillion in our sovereign wealth fund (national debt). That probably won't get resolved until the last minute because politicians stand to gain from creating a standoff. It leads to more cameras on them while they talk, so they have an incentive to milk it for as long as possible. There's also some risk that they actually fail to get a deal done. The political environment is much worse than a decade earlier, and the parties are more fractured.

While I recognize those fears, we prefer to invest when the market is already down significantly. That doesn't mean we're going to catch the bottom perfectly. It simply means that we will spot good companies at bargain prices and build our positions.

- Ratings: Strong Bullish view on CCI and ARE

For further details see:

2 REITs Dumped In The Bargain Bin